Native Collagen Market Size

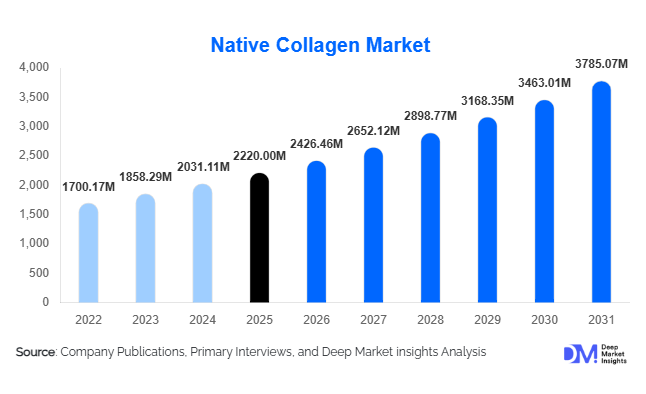

According to Deep Market Insights,the global native collagen market size was valued at USD 2,220 million in 2025 and is projected to grow from USD 2,426.46 million in 2026 to reach USD 3,785.07 million by 2031, expanding at a CAGR of 9.3% during the forecast period (2026–2031). Market growth is primarily driven by the rising adoption of collagen-based biomaterials in wound care, orthopedic repair, regenerative medicine, and aesthetic dermatology. Increasing surgical volumes, expanding elderly populations, and technological advancements in tissue engineering are accelerating demand for high-purity, structurally intact native collagen across global healthcare systems.

Key Market Insights

- Bovine-derived native collagen dominates, accounting for over 40% of global demand due to availability, cost efficiency, and established processing infrastructure.

- Type I collagen remains the leading product type, widely used in skin, bone, and wound healing applications.

- Wound care and tissue engineering represent the largest application segment, supported by rising chronic wound prevalence globally.

- North America leads the market, driven by high surgical volumes and advanced regenerative medicine adoption.

- Asia-Pacific is the fastest-growing region, supported by expanding healthcare infrastructure and domestic biomaterial manufacturing initiatives.

- Recombinant and marine collagen innovations are reshaping premium medical and aesthetic product segments.

What are the latest trends in the native collagen market?

Expansion of Regenerative Medicine Applications

Native collagen is increasingly integrated into regenerative medicine platforms, including 3D bioprinting scaffolds, stem cell therapies, and advanced tissue engineering matrices. Its ability to retain triple-helix structural integrity makes it highly suitable for supporting cellular adhesion and differentiation. Pharmaceutical and biotech companies are developing collagen-based matrices for cartilage regeneration, dermal substitutes, and drug delivery systems. Growing investment in regenerative therapies, particularly in North America, Europe, Japan, and South Korea, is reinforcing collagen’s role as a foundational biomaterial in next-generation therapeutic solutions.

Shift Toward Marine and Recombinant Collagen

Marine-derived native collagen is gaining traction due to lower zoonotic risk, cultural acceptability, and improved sustainability profiles compared to bovine or porcine sources. Meanwhile, recombinant collagen produced through biotechnology platforms is emerging as a premium alternative, offering batch consistency and reduced contamination risk. These innovations are particularly relevant in aesthetic and high-precision surgical applications where purity and safety are paramount. Companies investing in ethical sourcing and sustainable production are gaining competitive advantages in regulated healthcare markets.

What are the key drivers in the native collagen market?

Rising Prevalence of Musculoskeletal Disorders

Increasing global incidence of osteoarthritis, sports injuries, and cartilage degeneration is significantly driving demand for Type II native collagen in orthopedic and cartilage repair applications. Aging populations in the U.S., Germany, Japan, and China are contributing to higher joint replacement and regenerative therapy volumes, directly stimulating market expansion.

Growth in Advanced Wound Care

The rising burden of chronic wounds, particularly diabetic ulcers and pressure sores, is fueling demand for collagen-based wound dressings and hemostatic agents. Collagen accelerates tissue repair and reduces infection risk, making it a preferred biomaterial in hospital settings. Increasing diabetes prevalence worldwide further supports long-term demand growth.

Expansion of Aesthetic Procedures

The global increase in minimally invasive cosmetic procedures, including dermal fillers and skin rejuvenation treatments, is strengthening demand for native collagen matrices. Growing disposable incomes, medical tourism, and social media influence are supporting higher adoption rates across developed and emerging markets.

What are the restraints for the global market?

Raw Material Price Volatility

Native collagen production relies heavily on livestock-derived raw materials. Disease outbreaks, regulatory trade barriers, and supply chain disruptions can lead to price fluctuations and impact profit margins for manufacturers.

Regulatory and Compliance Complexities

Medical-grade native collagen products require stringent regulatory approvals, including FDA clearances and CE marking certifications. Lengthy clinical validation processes and high compliance costs may delay commercialization and increase entry barriers for new participants.

What are the key opportunities in the native collagen industry?

Emerging Market Manufacturing Expansion

Countries such as China and India are expanding domestic biomaterial manufacturing capabilities under government-backed initiatives. Local production reduces dependency on imports and improves price competitiveness. Establishing regional manufacturing facilities can significantly improve margins and supply chain stability.

Personalized and Application-Specific Collagen Solutions

Customized collagen scaffolds tailored to patient-specific regenerative requirements represent a high-margin opportunity. Integration with growth factors, antimicrobial agents, or bioactive compounds can create differentiated product offerings. As precision medicine expands, demand for application-specific native collagen formulations is expected to rise steadily.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2220 Million |

| Market Size in 2026 | USD 2426.46 Million |

| Market Size in 2031 | USD 3785.07 Million |

| CAGR | 9.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Source Insights

Bovine native collagen dominates the global native collagen market, accounting for approximately 42% of total demand in 2025. The leadership of this segment is primarily driven by abundant availability of cattle-derived raw materials, well-established supply chains, and cost-efficient extraction technologies that enable large-scale commercial production. In addition, bovine collagen has a long history of clinical validation and regulatory approvals across wound care, orthopedic implants, hemostatic agents, and surgical biomaterials, which strengthens physician confidence and procurement consistency. Its proven biocompatibility and mechanical performance in medical-grade formulations further reinforce its dominant position. Meanwhile, marine collagen is emerging as the fastest-growing source segment, supported by increasing safety concerns related to zoonotic diseases, growing demand for sustainable and traceable biomaterials, and expanding acceptance in advanced regenerative and aesthetic applications.

Product Type Insights

Fibrous native collagen holds nearly 35% of the global market share in 2025, making it the leading product type segment. Its dominance is attributed to its preserved triple-helix structure, which retains high tensile strength and structural integrity compared to denatured or hydrolyzed forms. This structural stability enables extensive use in surgical sponges, tissue scaffolds, guided bone regeneration membranes, and advanced regenerative matrices. The growing demand for load-bearing biomedical materials in orthopedic and reconstructive procedures further drives adoption. As regenerative medicine and tissue engineering continue to expand globally, fibrous native collagen remains the preferred material due to its superior mechanical properties and ability to mimic the natural extracellular matrix.

Type Insights

Type I native collagen leads the market with approximately 48% share in 2025, reflecting its widespread biological presence and compatibility with human connective tissues. As the most abundant collagen type in skin, bone, tendons, and ligaments, Type I collagen demonstrates excellent structural strength and cellular adhesion properties. Its extensive application in skin regeneration, bone graft substitutes, wound management products, and dental biomaterials drives segment growth. Increasing orthopedic surgeries, cosmetic reconstructive procedures, and chronic wound treatments globally further support demand. The segment’s dominance is reinforced by strong clinical evidence validating its safety, regenerative efficiency, and long-term performance in biomedical applications.

Application Insights

Wound care and tissue engineering collectively represent nearly 30% of global market share in 2025, making them the leading application segment. The primary growth driver is the rising prevalence of chronic wounds, including diabetic foot ulcers, pressure ulcers, and venous leg ulcers, particularly among aging and diabetic populations worldwide. Collagen-based dressings and regenerative matrices promote faster healing by supporting cellular proliferation and maintaining a moist wound environment. Additionally, the expansion of tissue engineering research, increasing trauma cases, and higher surgical intervention rates contribute to strong demand. Continuous innovation in bioactive and composite collagen scaffolds further enhances treatment outcomes, strengthening this segment’s market position.

End-Use Industry Insights

Hospitals and specialty clinics account for approximately 40% of total market demand in 2025, positioning them as the leading end-use segment. High surgical volumes, increasing inpatient wound treatment procedures, and growing adoption of regenerative biomaterials in orthopedic and reconstructive surgeries support this dominance. Institutional procurement systems and reimbursement coverage in developed healthcare markets further facilitate steady consumption. Cosmetic clinics represent the fastest-growing end-use segment, expanding at over 11% CAGR, driven by rising global demand for minimally invasive aesthetic treatments, dermal fillers, and skin rejuvenation procedures. Increasing consumer awareness of anti-aging solutions and expanding disposable incomes in emerging economies are accelerating adoption across private aesthetic centers.

Distribution Channel Insights

Direct B2B sales dominate the distribution landscape with nearly 55% share in 2025. This leadership is primarily supported by long-term procurement contracts between manufacturers and hospitals, specialty clinics, and medical device companies. Direct distribution ensures consistent product quality, regulatory compliance, traceability, and volume-based pricing advantages. Additionally, customized product development partnerships between collagen manufacturers and biomedical device firms strengthen supply chain integration. As regulatory scrutiny and quality assurance requirements increase globally, institutional buyers continue to prefer direct sourcing models, reinforcing the segment’s market dominance.

Explore more data points, trends and opportunities Download Free Sample Report

Native Collagen Market Segmentations

By Source

- Bovine Native Collagen

- Porcine Native Collagen

- Marine Native Collagen

- Poultry Native Collagen

- Recombinant & Other Sources

By Product Form

- Fibrous Native Collagen

- Gel-Based Native Collagen

- Sponge/Matrix Native Collagen

- Powdered Native Collagen

- Injectable Native Collagen Solutions

By Type

- Type I Native Collagen

- Type II Native Collagen

- Type III Native Collagen

- Type IV & V Native Collagen

By Application

- Wound Care & Tissue Engineering

- Orthopedic & Cartilage Repair

- Aesthetic & Dermatology Treatments

- Hemostats & Surgical Applications

- Drug Delivery & Regenerative Medicine

- Research & Cell Culture Applications

By End-Use Industry

- Hospitals & Specialty Clinics

- Cosmetic & Aesthetic Clinics

- Pharmaceutical & Biotech Companies

- Medical Device Manufacturers

- Research Institutes & CROs

By Distribution Channel

- Direct B2B Sales

- Third-Party Distributors

- Online/Institutional Procurement Platforms

Regional Insights

North America

North America holds approximately 34% of the global native collagen market share in 2025, with the United States accounting for nearly 80% of regional demand. The region’s leadership is driven by advanced healthcare infrastructure, strong funding for regenerative medicine research, and high volumes of surgical and orthopedic procedures. The presence of leading biomedical companies, well-defined regulatory pathways, and favorable reimbursement frameworks further strengthen market growth. Rising cases of diabetes-related chronic wounds and increasing adoption of advanced wound care solutions also contribute significantly to regional expansion.

Europe

Europe represents around 28% of global demand, led by Germany, France, and the United Kingdom. Growth in this region is supported by a rapidly aging population, increasing prevalence of musculoskeletal disorders, and strong demand for orthopedic and reconstructive procedures. Established healthcare systems and stringent quality standards promote the adoption of clinically validated collagen biomaterials. Additionally, ongoing research collaborations between academic institutions and medical device manufacturers enhance innovation in tissue engineering and regenerative therapies, sustaining long-term regional demand.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, expanding at over 10.5% CAGR. China, Japan, South Korea, and India are key contributors to growth. The region benefits from expanding healthcare infrastructure, rising healthcare expenditure, and increasing awareness of advanced wound management solutions. Government-backed domestic manufacturing initiatives and favorable policies supporting biomedical innovation are strengthening supply capabilities. Furthermore, the rapid growth of medical tourism, particularly in cosmetic and reconstructive procedures, is driving higher demand for collagen-based products across hospitals and aesthetic clinics.

Latin America

Latin America accounts for approximately 6–7% of global demand, with Brazil and Mexico leading regional adoption. Growth is primarily driven by expanding private healthcare facilities, rising demand for aesthetic procedures, and improving access to advanced wound care products. Increasing awareness of regenerative therapies and gradual modernization of hospital infrastructure are further supporting market penetration. As healthcare investments continue to increase, the region is expected to demonstrate steady medium-term growth.

Middle East & Africa

The Middle East & Africa region holds around 4–5% of the global market share. The United Arab Emirates and Saudi Arabia are emerging as high-growth markets due to expanding private healthcare investments, medical infrastructure modernization, and rising demand for cosmetic procedures. Government initiatives aimed at strengthening healthcare capacity and attracting medical tourism are further contributing to adoption. Although the market remains comparatively smaller, increasing awareness of advanced wound care and regenerative treatments is expected to support gradual expansion across the region.

Key Players in the Native Collagen Market

- Integra LifeSciences Corporation

- GELITA AG

- Collagen Solutions Plc

- Advanced BioMatrix, Inc.

- Nippi Incorporated

- DSM Biomedical

- Collagen Matrix, Inc.

- Symatese Group

- Nitta Gelatin Inc.

- Koken Co., Ltd.

- Shanghai Haohai Biological Technology Co., Ltd.

- Medtronic Plc

- Smith & Nephew Plc

- Evonik Industries AG

- Baxter International Inc.