Muscle Gainer Protein Powder Market Size

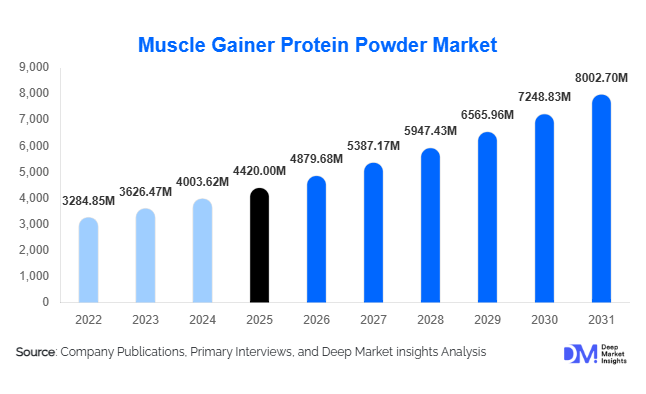

According to Deep Market Insights,the global muscle gainer protein powder market size was valued at USD 4,420 million in 2025 and is projected to grow from USD 4,879.68 million in 2026 to reach USD 8,002.70 million by 2031, expanding at a CAGR of 10.4% during the forecast period (2026–2031). The market growth is primarily driven by increasing global gym penetration, rising participation in strength training and bodybuilding, expanding e-commerce supplement sales, and growing awareness of high-calorie nutrition for muscle hypertrophy and weight gain. The shift toward performance-focused lifestyles, influencer-led fitness trends, and greater adoption of structured bulking programs among young consumers are further accelerating global demand.

Key Market Insights

- Whey-based formulations dominate the market, accounting for over 50% of total revenue due to superior bioavailability and rapid muscle recovery benefits.

- Online retail channels contribute nearly 38% of global sales, driven by subscription models and direct-to-consumer brand strategies.

- North America leads the global market, supported by mature supplement consumption patterns and strong sports nutrition culture.

- Asia-Pacific is the fastest-growing region, registering double-digit growth due to expanding gym chains in India and China.

- High-calorie (500–1,000 kcal) gainers remain the preferred product category, balancing caloric surplus with digestibility.

- Plant-based and clean-label formulations are gaining traction, especially in Europe and North America.

What are the latest trends in the muscle gainer protein powder market?

Shift Toward Clean-Label and Plant-Based Gain Formulas

Consumers are increasingly demanding allergen-free, lactose-free, and vegan muscle gainers formulated with pea, rice, and multi-plant protein blends. Manufacturers are reducing artificial sweeteners and incorporating digestive enzymes, probiotics, and micronutrient fortification to enhance absorption. Sustainable sourcing, transparent labeling, and non-GMO certifications are becoming major purchasing criteria, particularly across Europe and North America. Premium plant-based gainers are priced 20–30% higher than conventional whey products, reflecting strong consumer acceptance.

Direct-to-Consumer and Subscription-Based Sales Expansion

Digital-first brands are reshaping distribution through subscription models that offer personalized macro-calculated mass gainers. E-commerce marketplaces and brand-owned platforms are integrating AI-driven nutrition recommendations and bundled pricing strategies. This model improves customer retention and raises average order value, while allowing manufacturers to maintain stronger margins compared to traditional retail distribution.

What are the key drivers in the muscle gainer protein powder market?

Rising Global Gym Membership and Strength Training Adoption

Global health club memberships have surpassed 200 million members, with strength training emerging as a dominant fitness trend. Muscle hypertrophy-focused training regimens require caloric surplus and protein supplementation, directly driving demand for high-calorie gainers. Growing participation in bodybuilding competitions and physique sports further supports repeat consumption patterns.

Expansion of E-Commerce and Cross-Border Supplement Trade

Online retail has significantly reduced market entry barriers and expanded access to premium international brands. Cross-border exports from the U.S., Germany, and India are increasing, particularly to Southeast Asia and the Middle East. Subscription pricing, influencer marketing, and fitness app integrations are reinforcing sustained product demand.

What are the restraints for the global market?

Raw Material Price Volatility

Whey protein concentrate and isolate prices fluctuate based on dairy supply dynamics, skimmed milk powder trends, and global trade conditions. Rising milk procurement costs can pressure manufacturer margins, particularly in price-sensitive markets.

Regulatory and Quality Compliance Challenges

Stringent labeling standards, protein spiking scrutiny, and varying country-specific supplement regulations pose compliance challenges. Certifications such as NSF and Informed-Sport are increasingly required for professional athlete markets, adding operational costs.

What are the key opportunities in the muscle gainer protein powder industry?

Emerging Market Penetration in Asia and Latin America

India, China, Brazil, and Mexico are witnessing double-digit expansion in gym infrastructure and youth fitness participation. Market penetration remains relatively low compared to the U.S., offering substantial whitespace opportunities. Government-backed sports programs and rising middle-class disposable incomes support long-term growth prospects.

Personalized Performance Nutrition Platforms

Integration of wearable fitness devices and AI-based macro tracking presents opportunities for customized muscle gain solutions. Brands offering personalized caloric blends and subscription-based refills can capture higher lifetime customer value while differentiating from commoditized mass products.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4420 Million |

| Market Size in 2026 | USD 4879.68 Million |

| Market Size in 2031 | USD 8002.70 Million |

| CAGR | 10.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Protein Source Insights

Whey protein-based muscle gainers dominate the global market, accounting for approximately 54% of total revenue in 2025. The leadership of this segment is primarily driven by whey’s superior biological value, rapid digestibility, and high leucine concentration, which directly stimulates muscle protein synthesis and accelerates post-workout recovery. Whey isolate and concentrate blends are widely preferred among bodybuilders and strength athletes due to their ability to deliver fast-acting amino acids during the anabolic window. Additionally, strong clinical validation, widespread brand adoption, and established supply chains further reinforce whey’s dominant position. Multi-source blends combining whey and casein are steadily gaining traction among advanced athletes seeking both immediate and sustained amino acid release for prolonged muscle recovery. Meanwhile, plant-based protein blends derived from pea, rice, and soy are expanding steadily in Europe and North America, supported by rising veganism, lactose intolerance prevalence, and demand for clean-label, allergen-friendly formulations.

Caloric Density Insights

High-calorie formulations providing between 500 and 1,000 kcal per serving represent nearly 47% of the 2025 market, making them the leading caloric density segment. Their dominance is driven by their ability to offer an optimal caloric surplus required for lean mass gain without causing excessive digestive discomfort or bloating, which is often associated with ultra-high-calorie products. These formulations balance carbohydrates, proteins, and fats in ratios suitable for controlled bulking cycles, appealing to both intermediate and advanced users. Ultra-high-calorie variants exceeding 1,000 kcal per serving remain popular among professional bodybuilders and hard gainers during aggressive mass-gain phases, although their adoption is comparatively niche due to digestive tolerance considerations and higher price points.

Distribution Channel Insights

Online retail holds approximately 38% of global sales in 2025, emerging as the leading distribution channel. Growth in this segment is driven by expanding e-commerce penetration, subscription-based supplement models, influencer marketing, competitive pricing, and the availability of detailed product comparisons and customer reviews. Brand-owned websites and major e-commerce platforms have enabled manufacturers to reach a wider consumer base while offering personalized recommendations and promotional discounts. Despite rapid online expansion, offline specialty nutrition stores continue to play a critical role, particularly for first-time buyers seeking expert guidance, product sampling, and trust-building interactions. Brick-and-mortar retail remains especially relevant in North America and Europe, where established supplement chains maintain strong brand loyalty and credibility.

End-User Insights

Bodybuilders and strength athletes account for nearly 41% of total market demand, making them the leading end-user segment. This dominance is driven by structured training regimens, performance-oriented nutrition strategies, and consistent supplementation cycles aimed at maximizing hypertrophy and strength gains. Competitive bodybuilding culture and social media-driven physique aspirations further reinforce demand within this group. Recreational gym users represent the fastest-growing segment, fueled by rising global fitness awareness, increasing gym memberships, and the mainstream adoption of protein supplementation among young adults. Growth in emerging economies is particularly strong as urbanization, disposable income expansion, and lifestyle shifts encourage regular fitness participation.

Formulation Type Insights

Powder-based muscle gainers dominate the market with over 82% share, supported by their cost efficiency, extended shelf life, ease of transportation, and flexibility in serving size customization. Consumers favor powder formulations because they allow precise calorie adjustments and stacking with additional supplements such as creatine and amino acids. Manufacturers also benefit from lower production and packaging costs compared to ready-to-drink formats. Ready-to-drink muscle gainers are gradually expanding in urban, convenience-driven markets where time-constrained consumers prefer portability and immediate consumption. However, higher pricing and shorter shelf stability currently limit their overall market penetration compared to powders.

Explore more data points, trends and opportunities Download Free Sample Report

Muscle Gainer Protein Powder Market Segmentations

By Protein Source

- Whey Protein-Based

- Casein-Based

- Soy Protein-Based

- Plant-Based Blends

- Multi-Source Protein Blends

By Caloric Density

- Standard

- High-Calorie

- Ultra-High Calorie

By End-User

- Bodybuilders & Strength Athletes

- Recreational Gym Users

- Professional Athletes

- Underweight Individuals

- Military & Tactical Training Personnel

By Distribution Channel

- Online Retail

- Specialty Nutrition Stores

- Supermarkets & Hypermarkets

- Pharmacies & Health Stores

By Formulation Type

- Powder

- Ready-to-Mix Sachets

- Ready-to-Drink (RTD) Shakes

Regional Insights

North America

North America accounts for approximately 34% of the 2025 global market, with the United States alone contributing nearly 28%. Regional dominance is driven by high disposable incomes, a deeply rooted supplement culture, and a strong presence of competitive bodybuilding and collegiate sports programs. Advanced retail infrastructure, widespread gym penetration, and aggressive digital marketing strategies further support consistent product uptake. The region also benefits from established domestic manufacturing capacity, continuous product innovation, and export leadership, enabling brands to maintain premium positioning and rapid product rollouts.

Europe

Europe represents around 25% of global demand, led by Germany, the United Kingdom, and France. Regional growth is primarily supported by increasing health consciousness, expansion of fitness club memberships, and rising adoption of clean-label and plant-based formulations. Stringent regulatory frameworks enhance product quality standards, encouraging premiumization and consumer trust. Innovation in lactose-free, vegan, and low-sugar variants aligns with shifting dietary preferences, while strong sports nutrition distribution networks across Western Europe sustain stable long-term demand.

Asia-Pacific

Asia-Pacific holds nearly 27% share in 2025 and is the fastest-growing region, expanding at an estimated CAGR of 12–13%. China and India serve as primary growth engines due to expanding gym networks, a large youth demographic, rising middle-class disposable incomes, and increasing awareness of sports nutrition benefits. Rapid digital commerce penetration and influencer-driven fitness culture significantly accelerate product visibility and trial rates. Additionally, urbanization and the growing popularity of bodybuilding competitions and fitness expos across Southeast Asia contribute to sustained regional expansion.

Latin America

Brazil and Mexico dominate regional demand, supported by strong bodybuilding participation rates, growing fitness awareness, and increasing adoption of performance-oriented supplements among young consumers. Expanding retail availability and rising social media fitness trends further stimulate market penetration. Although periodic economic volatility may moderate short-term purchasing power, long-term consumption trends remain positive due to demographic advantages and an expanding urban fitness community.

Middle East & Africa

The United Arab Emirates and Saudi Arabia are emerging as high-value markets driven by premium supplement imports, expanding luxury gym chains, and rising investments in sports infrastructure aligned with national health initiatives. Increasing expatriate populations and high per-capita income levels support demand for international sports nutrition brands. South Africa leads demand within the African continent, benefiting from a well-established retail network and growing participation in strength sports. Across the broader region, increasing lifestyle-related health awareness and government-backed fitness campaigns are expected to gradually strengthen market expansion over the forecast period.

Key Players in the Muscle Gainer Protein Powder Market

- Optimum Nutrition

- MuscleTech

- BSN

- Dymatize

- Myprotein

- Universal Nutrition

- Labrada Nutrition

- GNC Holdings

- Rule One Proteins

- BPI Sports

- REDCON1

- MusclePharm

- Isopure

- Applied Nutrition

- AllMax Nutrition