Mung Bean Market Size

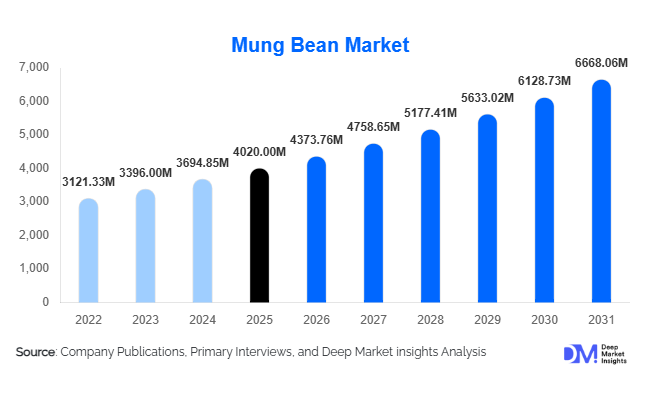

According to Deep Market Insights, the global mung bean market size was valued at USD 4,020 million in 2025 and is projected to grow from USD 4,373.76 million in 2026 to reach USD 6,668.06 million by 2031, expanding at a CAGR of 8.8% during the forecast period (2026–2031). The mung bean market growth is primarily driven by rising demand for plant-based protein, increasing consumption of traditional pulse-based foods, and expanding applications in processed food and nutraceutical industries. Growing awareness around clean-label, gluten-free, and high-protein diets is further accelerating global demand, particularly in developed markets.

Key Market Insights

- Plant-based protein demand is transforming the mung bean market, with increasing use in meat substitutes, dairy alternatives, and protein isolates.

- Asia-Pacific dominates global production and consumption, led by India, China, and Southeast Asia due to traditional dietary reliance.

- Food processing applications account for the largest share, driven by rising demand for ready-to-eat and convenience foods.

- North America is the fastest-growing region, supported by the rapid expansion of vegan and flexitarian diets.

- Organic mung beans are gaining traction, particularly in Europe and North America, despite higher costs and limited supply.

- Technological advancements in processing, including protein extraction and starch refinement, are enabling higher-value applications.

What are the latest trends in the mung bean market?

Expansion of Plant-Based Food Innovations

The mung bean market is witnessing a strong shift toward plant-based food innovations, particularly in developed economies. Food manufacturers are increasingly utilizing mung bean protein isolates in products such as egg substitutes, dairy alternatives, and meat analogs due to their functional properties and neutral taste. This trend is being supported by growing vegan and flexitarian populations, especially in North America and Europe. Startups and established food companies alike are investing in mung bean-based formulations to cater to evolving consumer preferences for sustainable and high-protein diets. The scalability of mung bean protein extraction technologies is further enhancing its commercial viability across global markets.

Growth in Processed and Convenience Foods

Another key trend is the rising incorporation of mung beans in processed and convenience foods. Urbanization, busy lifestyles, and increasing disposable incomes are driving demand for ready-to-cook and ready-to-eat products. Mung bean flour, starch, and split variants are widely used in noodles, snacks, and bakery products. This trend is particularly strong in Asia-Pacific, where traditional consumption patterns are merging with modern food processing techniques. Manufacturers are focusing on product innovation, packaging improvements, and shelf-life enhancement to capture a larger share of this growing segment.

What are the key drivers in the mung bean market?

Rising Demand for Plant-Based Protein

The increasing global shift toward plant-based diets is a major driver for the mung bean market. Consumers are actively seeking alternatives to animal protein due to health, environmental, and ethical considerations. Mung beans offer a cost-effective, nutrient-rich solution, making them highly attractive for both consumers and manufacturers. The growing adoption of vegan and flexitarian lifestyles is significantly boosting demand across developed and emerging markets.

Expansion of Food Processing Industry

The rapid growth of the food processing industry, particularly in Asia-Pacific, is driving demand for mung beans in various processed forms. Mung bean derivatives such as flour, starch, and protein isolates are increasingly being used in packaged foods, snacks, and beverages. This expansion is supported by rising urbanization, increasing disposable incomes, and changing dietary habits, which are collectively fueling the demand for convenient and functional food products.

What are the restraints for the global market?

Price Volatility and Supply Fluctuations

The mung bean market is highly dependent on agricultural output, making it vulnerable to climatic conditions such as droughts and irregular rainfall. These factors can lead to inconsistent supply and significant price fluctuations, posing challenges for both producers and consumers. Seasonal variations further exacerbate supply chain uncertainties, impacting overall market stability.

Limited Processing Infrastructure

In many developing regions, inadequate processing infrastructure limits the ability to produce value-added mung bean products. This restricts market growth by confining producers to low-margin raw exports. Investments in processing facilities and technological advancements are required to overcome this limitation and enhance competitiveness in global markets.

What are the key opportunities in the mung bean industry?

Integration into Functional Foods and Nutraceuticals

The increasing focus on health and wellness is creating opportunities for mung beans in functional foods and nutraceuticals. Rich in protein, fiber, and antioxidants, mung beans are being incorporated into health supplements, fortified foods, and dietary products. This trend is expected to open new revenue streams for market participants, particularly in developed markets where health-conscious consumers are driving demand.

Government Support and Agricultural Initiatives

Government initiatives promoting pulse cultivation and food security are providing significant growth opportunities. Programs aimed at increasing agricultural productivity and supporting farmers are ensuring a stable supply of mung beans. These initiatives are also encouraging investments in storage, logistics, and processing infrastructure, thereby strengthening the overall value chain.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4020.00 Million |

| Market Size in 2026 | USD 4373.76 Million |

| Market Size in 2031 | USD 6668.06 Million |

| CAGR | 8.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global mung bean market is characterized by a diverse product portfolio that reflects both traditional consumption patterns and emerging industrial applications. Whole mung beans continue to dominate the market, accounting for approximately 42% of the global market share in 2025. This dominance is largely attributed to their entrenched role in staple diets across key Asian economies such as India, China, and Southeast Asian countries, where they are consumed in a wide variety of forms, including soups, curries, desserts, and sprouted preparations. The inherent versatility, affordability, and nutritional profile of whole mung beans—rich in protein, fiber, and essential micronutrients—further reinforce their sustained demand across both rural and urban populations.In addition to traditional uses, the demand for whole mung beans is increasingly supported by rising awareness around clean-label and minimally processed foods. Consumers are showing a growing preference for whole food ingredients that retain their natural nutritional integrity, which has further strengthened the position of this segment. Moreover, government initiatives promoting pulse consumption for food security and nutritional balance in emerging economies have also contributed to its continued leadership in the product mix.However, the market is gradually witnessing a structural shift toward processed and value-added forms. Split mung beans, commonly used in convenience cooking and packaged food products, are gaining traction due to their shorter cooking time and ease of preparation. Similarly, mung bean flour is emerging as a key ingredient in gluten-free and specialty food formulations, particularly in bakery and snack segments. The increasing prevalence of gluten intolerance and celiac disease, along with broader consumer interest in alternative flours, is accelerating demand for mung bean-based flour products.Overall, the product landscape is evolving from a predominantly commodity-based market toward a more diversified ecosystem that includes both traditional and high-value applications. This transition is expected to improve profit margins for manufacturers and create new growth opportunities across the value chain.

Application Insights

The application landscape of the mung bean market is heavily skewed toward the food and beverages segment, which accounts for over 70% of the total market share. This dominance is rooted in the long-standing culinary significance of mung beans across multiple cultures, particularly in Asia-Pacific. Mung beans are widely used in the preparation of traditional dishes, confectioneries, fermented foods, and beverages, making them an indispensable ingredient in regional cuisines.The leading driver for this segment is the increasing global demand for plant-based and functional food products. Consumers are actively seeking healthier dietary alternatives that offer high protein content, low fat, and added health benefits. Mung beans, being naturally rich in protein, antioxidants, and essential nutrients, align well with these evolving preferences. This has led to their growing incorporation into modern food products such as plant-based meat substitutes, dairy-free milk, protein bars, and ready-to-eat meals.Beyond conventional food applications, the nutraceutical and dietary supplement segment is emerging as a promising growth avenue. Mung beans are recognized for their health-promoting properties, including anti-inflammatory, antioxidant, and cholesterol-lowering effects. As consumers become more proactive about preventive healthcare and wellness, the demand for functional ingredients derived from natural sources is increasing. This is driving the use of mung bean extracts and proteins in dietary supplements, health drinks, and fortified foods.Additionally, the use of mung beans in animal feed and cosmetic formulations, although relatively niche, is gaining attention due to their nutritional and functional benefits. Overall, the application spectrum of mung beans is expanding beyond traditional boundaries, supported by innovation and shifting consumer preferences toward health and sustainability.

Distribution Channel Insights

The distribution landscape of the mung bean market is dominated by direct or B2B channels, which account for nearly 60% of total sales. This dominance is primarily driven by bulk procurement by food processing companies, ingredient manufacturers, and large-scale distributors. These entities require consistent supply volumes and standardized quality, which are efficiently facilitated through direct sourcing arrangements with producers and suppliers.At the same time, retail channels are experiencing significant growth, driven by the rising popularity of packaged and branded mung bean products among end consumers. Supermarkets and hypermarkets remain key distribution points, offering a wide range of products including whole beans, split beans, flour, and ready-to-cook variants. The increasing penetration of organized retail in emerging markets is further supporting this growth.E-commerce platforms are playing an increasingly important role in expanding market reach and accessibility. Online retail offers consumers the convenience of purchasing a variety of mung bean products, including organic and specialty variants, from the comfort of their homes. The growing adoption of digital technologies, coupled with improvements in logistics and delivery infrastructure, is accelerating the shift toward online channels. Additionally, the availability of detailed product information and customer reviews is enhancing consumer confidence and driving online sales.Overall, the distribution landscape is becoming more dynamic and multi-channel in nature, with both traditional and modern channels contributing to market expansion. The integration of digital platforms with conventional supply chains is expected to further enhance efficiency and customer engagement.

End-Use Industry Insights

The food processing industry represents the largest end-use segment in the mung bean market, accounting for approximately 50% of the global market share. This dominance is driven by the increasing demand for processed and convenience foods that incorporate mung beans as a key ingredient. The leading driver for this segment is the growing consumer preference for ready-to-eat and easy-to-prepare food products, particularly in urban areas where busy lifestyles are influencing dietary habits.The nutraceutical industry is emerging as a high-growth segment, driven by increasing awareness of health and wellness. Mung beans are being utilized in the production of dietary supplements, protein powders, and functional foods aimed at improving overall health and preventing chronic diseases. The rising incidence of lifestyle-related conditions such as obesity, diabetes, and cardiovascular diseases is prompting consumers to adopt healthier diets, thereby supporting the growth of this segment.Household consumption remains a stable and significant segment, especially in Asia-Pacific, where mung beans are a staple food. Despite the growth of processed and industrial applications, traditional consumption continues to play a crucial role in sustaining overall market demand. This balance between traditional and modern end-use industries is a defining characteristic of the mung bean market.

Explore more data points, trends and opportunities Download Free Sample Report

Mung Bean Market Segmentations

By Product Type

- Whole Mung Beans

- Split Mung Beans

- Mung Bean Flour

- Mung Bean Starch

- Mung Bean Protein Isolates & Concentrates

- Sprouted Mung Beans

By Application

- Food & Beverages

- Animal Feed

- Nutraceuticals & Dietary Supplements

- Cosmetics & Personal Care

By Distribution Channel

- Direct/B2B Sales

- Supermarkets/Hypermarkets

- Convenience Stores

- Specialty Stores

- Online Retail

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global mung bean market, accounting for approximately 68% of the total market share in 2025. The region’s leadership is anchored by countries such as India, China, Myanmar, and Thailand, which are both major producers and consumers of mung beans. India alone contributes nearly 30% of global demand, driven by its large population and deep-rooted dietary traditions that incorporate pulses as a primary source of protein.Furthermore, the rising awareness of health and wellness is driving demand for plant-based and protein-rich foods across the region. This is encouraging manufacturers to innovate and develop new products that cater to evolving consumer preferences. Overall, Asia-Pacific is expected to maintain its dominance over the forecast period, supported by strong domestic demand, favorable government policies, and expanding industrial applications.

North America

North America holds approximately 12% of the global mung bean market share, with the United States being the primary contributor. The region is also the fastest-growing market, with a projected CAGR exceeding 10% during the forecast period. This rapid growth is largely driven by the increasing adoption of plant-based diets and the rising demand for alternative protein sources.A key driver in North America is the growing consumer shift toward vegan, vegetarian, and flexitarian lifestyles. As consumers become more conscious of the environmental and health impacts of animal-based products, they are seeking plant-based alternatives that offer comparable nutritional benefits. Mung bean protein, with its high protein content and functional versatility, is gaining popularity as an ingredient in plant-based meat and dairy substitutes.Another important factor is the increasing awareness of clean-label and allergen-free products. Mung beans are naturally gluten-free and non-GMO, making them an attractive option for health-conscious consumers. The expansion of retail and e-commerce channels is also enhancing product accessibility and contributing to market growth.

Europe

Europe accounts for approximately 10% of the global mung bean market, with countries such as Germany, the United Kingdom, and France leading demand. The region is characterized by a strong emphasis on sustainability, health, and organic food consumption, which is driving the adoption of mung bean-based products.The regulatory environment in Europe also supports market growth, with policies promoting sustainable agriculture and the use of plant-based ingredients. Additionally, the growing popularity of ethnic cuisines is introducing mung beans to a wider audience, further boosting demand.The expansion of the vegan food industry and the presence of innovative food manufacturers are contributing to the development of new mung bean-based products. As awareness continues to grow, the market is expected to witness steady expansion across the region.

Middle East & Africa

The Middle East and Africa region is emerging as a significant market for mung beans, with demand concentrated in countries such as the United Arab Emirates and South Africa. The region’s growth is primarily driven by increasing imports, as local production remains limited.Additionally, rising awareness of health and nutrition is encouraging consumers to incorporate more plant-based foods into their diets. Government initiatives aimed at improving food security and diversifying food sources are further supporting market growth.The development of modern retail infrastructure and the increasing availability of imported products are also enhancing market accessibility. As a result, the Middle East and Africa region is expected to witness steady growth over the forecast period.

Latin America

Latin America is experiencing gradual growth in the mung bean market, with countries such as Brazil and Mexico emerging as key contributors. The region’s growth is supported by increasing awareness of plant-based nutrition and the rising demand for alternative protein sources.The expansion of the food processing industry is also playing a significant role in driving demand. Manufacturers are exploring the use of mung beans in various applications, including snacks, bakery products, and functional foods. Additionally, the increasing influence of global food trends is encouraging the adoption of plant-based diets in the region.Although the market is still in its early stages compared to other regions, the potential for growth remains significant. Continued investment in awareness, distribution, and product innovation is expected to drive market expansion in the coming years.

Key Players in the Mung Bean Market

- Archer Daniels Midland Company (ADM)

- Cargill Incorporated

- Bunge Limited

- Olam Group

- AGT Food and Ingredients

- Wilmar International

- Louis Dreyfus Company

- SunOpta Inc.

- Ingredion Incorporated

- Roquette Frères

- Ebro Foods

- Tata Consumer Products

- ITC Limited

- Adani Wilmar

- Bühler Group