Monosodium Glutamate (MSG) Market Size

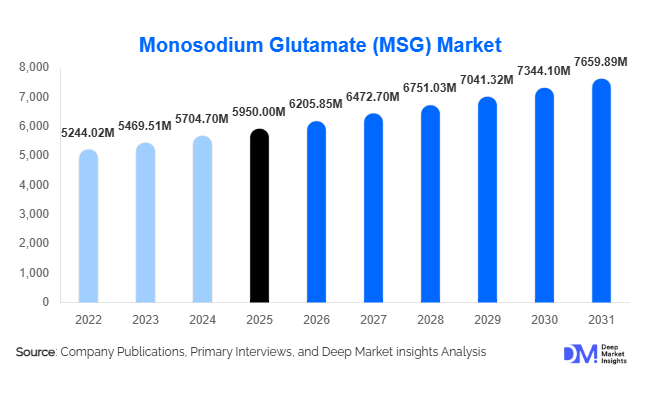

According to Deep Market Insights, the global monosodium glutamate (MSG) market size was valued at USD 5,950 million in 2025 and is projected to grow from USD 6,205.85 million in 2026 to reach USD 7,659.89 million by 2031, expanding at a CAGR of 4.3% during the forecast period (2026–2031). The MSG market growth is primarily driven by rising global consumption of processed and convenience foods, expanding quick-service restaurant (QSR) chains, and the increasing use of flavor enhancers in sodium-reduction formulations.

Monosodium glutamate remains one of the most cost-efficient umami enhancers used across packaged foods, seasoning blends, meat processing, and foodservice applications. Asia-Pacific dominates global production and consumption, supported by large-scale fermentation capacity and strong demand for instant noodles and savory snacks. Meanwhile, North America and Europe are witnessing stable demand growth, driven by reformulation strategies aimed at lowering sodium content without compromising taste. Continuous improvements in fermentation technology, raw material optimization, and plant automation are enhancing production efficiency and supporting long-term margin stability across leading manufacturers.

Key Market Insights

- Fermentation-based production accounts for over 95% of global MSG output, driven by cost efficiency and scalability advantages.

- Asia-Pacific dominates the global market, contributing approximately 62% of total demand in 2025.

- Processed and packaged foods represent the largest application segment, accounting for nearly 55% of overall consumption.

- Direct B2B bulk sales dominate distribution channels, contributing around 75% of total market revenue.

- Sodium-reduction reformulation in Western markets is emerging as a key demand driver.

- The Middle East & Africa are the fastest-growing regional markets, supported by expanding food processing industries.

What are the latest trends in the monosodium glutamate (MSG) market?

Sodium-Reduction Reformulation Across Processed Foods

Food manufacturers are increasingly incorporating MSG into reformulated products to reduce overall sodium content while maintaining flavor intensity. As MSG contains roughly one-third the sodium of table salt, it serves as an effective tool in meeting regulatory sodium reduction targets across North America and Europe. This trend is particularly visible in soups, ready meals, and savory snacks. Governments promoting public health campaigns on sodium intake are indirectly boosting MSG demand, as manufacturers seek cost-effective reformulation strategies without sacrificing taste profiles.

Advancements in Fermentation Technology

Technological advancements in microbial strain engineering and continuous fermentation systems are improving yield efficiency and lowering energy consumption. Leading manufacturers are investing in automated bioreactors, real-time process monitoring, and waste heat recovery systems to optimize operational costs. These improvements are enhancing production scalability while stabilizing pricing amid raw material volatility. Integration of digital process controls has improved output consistency and reduced downtime, strengthening global supply reliability.

What are the key drivers in the MSG market?

Rising Consumption of Processed & Convenience Foods

Global processed food sales exceeding USD 2 trillion are significantly driving MSG consumption. Urbanization, dual-income households, and expanding retail penetration are increasing demand for instant noodles, frozen foods, and snack products that rely on standardized flavor enhancement. Asia-Pacific remains the epicenter of instant noodle production, exceeding 120 billion servings annually, directly supporting bulk MSG procurement.

Growth of Quick-Service Restaurants (QSRs)

The rapid expansion of QSR chains across Asia, Latin America, and the Middle East is driving demand for cost-effective flavor enhancers. Centralized kitchens and standardized recipes require consistent seasoning inputs, positioning MSG as a preferred ingredient for maintaining taste uniformity across large-scale operations.

What are the restraints for the global market?

Consumer Perception Challenges

Despite strong scientific consensus on safety, negative perceptions associated with “Chinese Restaurant Syndrome” continue to influence consumer behavior in certain Western markets. Clean-label trends and “No MSG” product claims in premium segments create barriers to growth in retail channels.

Raw Material Price Volatility

MSG production relies heavily on starch and sugar derivatives such as corn glucose, molasses, and tapioca. Fluctuations in agricultural commodity prices can compress profit margins, particularly for producers lacking vertical integration into raw material supply chains.

What are the key opportunities in the MSG industry?

Expansion in Emerging Food Processing Hubs

Rapid industrialization of food processing sectors in India, Indonesia, Nigeria, and Brazil presents strong growth opportunities. Establishing regional fermentation facilities near starch sources can reduce logistics costs and improve supply chain resilience, enabling new entrants to compete effectively.

Plant-Based and Alternative Protein Applications

The global plant-based meat industry, valued at over USD 8 billion in 2025, increasingly relies on MSG to enhance umami profiles in meat alternatives. As plant protein formulations often lack depth of flavor, MSG serves as a critical functional ingredient, creating incremental demand beyond traditional processed food categories.

Grade Insights

Food-grade MSG dominates the global market, accounting for approximately 88% of total revenue in 2025, driven primarily by its extensive application across processed foods, ready meals, instant noodles, savory snacks, seasoning blends, soups, and quick-service restaurant (QSR) formulations. The segment’s leadership is underpinned by rising global consumption of convenience foods, rapid urbanization in emerging economies, and the growing need for cost-effective flavor enhancement in mass food production. Additionally, sodium-reduction reformulation strategies in North America and Europe are further strengthening demand for food-grade MSG, as manufacturers leverage its umami properties to maintain taste while lowering overall salt content.

Industrial and pharmaceutical-grade MSG collectively account for nearly 12% of market revenue. Industrial-grade MSG is primarily used in biochemical synthesis and research applications, while pharmaceutical-grade variants serve as excipients and specialized formulations. Although comparatively smaller in share, these segments benefit from steady demand in laboratory research and specialty manufacturing, offering higher margins relative to bulk food-grade production.

Form Insights

Crystal or granular MSG leads the market with nearly 72% share, largely due to its superior storage stability, longer shelf life, ease of transportation, and compatibility with automated blending systems used by large-scale food processors. The crystalline structure allows for uniform particle size, enabling precise dosing in seasoning blends and processed food manufacturing. This consistency is particularly critical for multinational food brands that require standardized flavor profiles across global production facilities.

Powdered MSG represents approximately 20% of the market and is preferred in certain snack coatings and dry soup mixes where rapid dissolution is required. Liquid MSG solutions occupy a niche segment, mainly utilized in industrial food processing lines that incorporate continuous liquid seasoning systems. Growth in the granular segment remains closely tied to expansion in packaged food manufacturing and export-oriented food production in the Asia-Pacific.

Application Insights

Processed and packaged foods remain the dominant application segment, accounting for roughly 55% of total MSG demand. Instant noodles alone represent a significant share of consumption, particularly across China, Indonesia, Vietnam, and India, where annual production volumes continue to expand. Savory snacks, frozen foods, and seasoning blends also contribute substantially to demand growth. The primary driver for this segment is the increasing global reliance on affordable, shelf-stable convenience foods that require consistent flavor enhancement.

Foodservice applications contribute approximately 22% of total demand, supported by the global expansion of QSR chains and institutional catering services. Meat and seafood processing accounts for around 12%, where MSG enhances flavor retention in processed and cured products. Emerging demand in plant-based and alternative protein products is gradually expanding the application base, as manufacturers seek to replicate umami characteristics traditionally associated with meat-based formulations.

Distribution Channel Insights

Direct B2B sales dominate the MSG market with nearly 75% of total revenue, reflecting bulk procurement by multinational food manufacturers, seasoning producers, and large foodservice chains. This channel benefits from long-term supply contracts, volume-based pricing, and integrated logistics systems that ensure consistent supply for high-output production facilities. Retail-packaged MSG accounts for approximately 20% of market revenue, primarily in Asia-Pacific, where household consumption remains significant. Supermarkets, hypermarkets, and traditional trade outlets remain key retail channels. Online sales are still nascent but expanding steadily, particularly in urban markets where digital grocery platforms are gaining traction. Growth in retail channels is supported by rising home cooking trends and increasing penetration of organized retail in emerging economies.

| By Grade | By Form | By Application | By Distribution Channel |

|---|---|---|---|

|

|

|

|

Regional Insights

Asia-Pacific

Asia-Pacific accounts for approximately 62% of global MSG demand in 2025, maintaining its position as both the largest production and consumption hub. China alone contributes nearly 35% of global consumption, supported by extensive fermentation capacity, vertically integrated corn-processing infrastructure, and strong domestic demand for instant noodles and seasoning products. Indonesia, Vietnam, and Thailand serve as both major consumers and export-oriented producers. India is emerging as one of the fastest-growing markets, expanding at over 6% CAGR, driven by rapid growth in packaged foods, rising disposable incomes, and increasing QSR penetration. Regional growth is further supported by favorable raw material availability, lower production costs, and government-backed food processing initiatives.

North America

North America holds approximately 14% of the global market share, led by the United States, which accounts for more than 80% of regional demand. Growth remains moderate at around 3% CAGR, primarily driven by sodium-reduction reformulation in processed foods and increasing adoption in savory snack manufacturing. The presence of a highly developed packaged food industry and advanced food technology infrastructure supports stable demand. However, clean-label preferences and historical consumer perception challenges moderate growth momentum in retail segments.

Europe

Europe represents nearly 12% of global MSG consumption, with Germany, the United Kingdom, and France being key markets. Growth remains relatively modest at 2–3% annually due to strict food labeling regulations and strong clean-label trends. However, demand is supported by expanding ethnic food consumption, growing ready-meal markets, and sodium-reduction initiatives in processed foods. Eastern European countries are demonstrating comparatively stronger growth due to increasing industrial food production and rising urbanization.

Latin America

Latin America contributes approximately 7% of global demand, led by Brazil and Mexico. The region is expanding at an estimated 5% CAGR, supported by growth in domestic food processing industries, increasing urban populations, and rapid QSR expansion. Rising exports of processed foods from Brazil are also driving bulk MSG procurement. Cost sensitivity in the region further favors MSG as an economical flavor enhancer compared to alternative umami ingredients.

Middle East & Africa

The Middle East & Africa region holds around 5% market share but is the fastest-growing region, expanding at 6–7% CAGR. Saudi Arabia, the UAE, and Nigeria are key growth markets. Rising food imports, increasing establishment of local food manufacturing facilities, and growing urban middle-class populations are primary drivers. Additionally, strong expansion in institutional catering, hospitality, and QSR sectors across the Gulf Cooperation Council (GCC) countries is boosting bulk demand. Government initiatives aimed at enhancing food security and reducing import dependency are also encouraging localized food processing, indirectly stimulating MSG consumption.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Monosodium Glutamate (MSG) Market

- Ajinomoto Co., Inc.

- Fufeng Group

- Meihua Holdings Group

- COFCO Biochemical (Anhui)

- Daesang Corporation

- Thai Fermentation Industry

- Angel Yeast Co., Ltd.

- Lotus Health Group

- Eppen Biotech

- Shandong Qilu Biotechnology

- Bihai Biotechnology

- Shandong Xinle Bioengineering

- Global Bio-Chem Technology Group

- PT Cheil Jedang Indonesia

- Vedanta Limited