Milk Protein Market Size

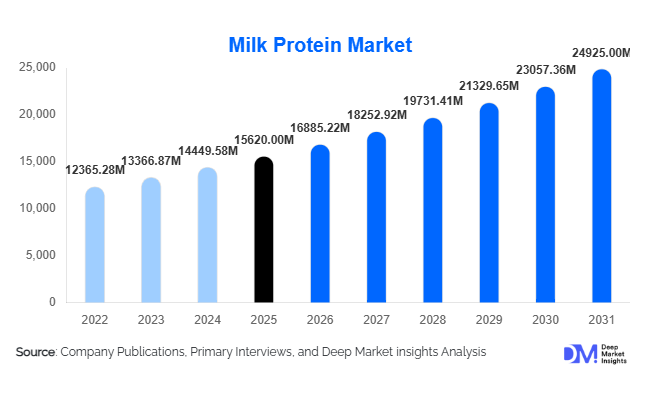

According to Deep Market Insights, the global milk protein market size was valued at USD 15,620 million in 2025 and is projected to grow from USD 16,885.22 million in 2026 to reach USD 24,925 million by 2031, expanding at a CAGR of 8.1% during the forecast period (2026–2031). The milk protein market growth is primarily driven by rising global demand for protein-enriched foods, expanding sports and clinical nutrition consumption, and increasing use of functional dairy ingredients across processed food applications. Manufacturers are increasingly incorporating milk proteins into fortified beverages, infant nutrition products, and ready-to-eat foods, positioning milk protein as a critical ingredient within the global nutrition ecosystem.

Key Market Insights

- Protein fortification trends are accelerating globally, with milk protein becoming a preferred ingredient due to its complete amino acid profile and superior digestibility.

- Sports and active nutrition applications are expanding rapidly, driving strong demand for whey protein concentrates and isolates.

- North America dominates the global market, supported by mature supplement industries and strong consumer awareness regarding protein intake.

- Asia-Pacific represents the fastest-growing region, fueled by rising middle-class income and expanding infant nutrition demand.

- Technological advancements in membrane filtration and protein fractionation are improving functionality and enabling premium product innovation.

- Sustainability and traceable dairy sourcing are emerging as key purchasing criteria among multinational food manufacturers.

What are the latest trends in the milk protein market?

Shift Toward Functional and High-Protein Foods

Food manufacturers worldwide are reformulating products to include higher protein content as consumers increasingly prioritize health, fitness, and weight management. Milk proteins are widely used in functional snacks, protein beverages, dairy alternatives, and fortified bakery products due to their emulsification, texture enhancement, and nutritional benefits. High-protein labeling has become a major marketing strategy, encouraging adoption across mainstream food categories rather than niche sports nutrition products. The trend is particularly visible in ready-to-drink beverages and protein-enriched convenience foods, where demand continues to expand among urban consumers seeking balanced nutrition options.

Premiumization Through Specialized Protein Ingredients

Manufacturers are increasingly moving toward high-value protein isolates and hydrolyzed proteins offering enhanced solubility, digestibility, and targeted nutritional benefits. Clinical nutrition and elderly-focused dietary products are driving innovation in fast-absorbing proteins designed to support muscle maintenance and recovery. Companies are investing in advanced processing technologies such as ultrafiltration and enzymatic hydrolysis to differentiate products and command higher margins. Premium milk protein ingredients are also being developed for lactose-sensitive consumers and specialized dietary applications, expanding market reach.

What are the key drivers in the milk protein market?

Growing Global Demand for Protein-Rich Diets

Consumers across developed and emerging markets increasingly associate protein intake with improved health outcomes, including muscle development, metabolic balance, and satiety. This shift has accelerated demand for protein-enriched packaged foods and beverages, directly supporting milk protein consumption. The expansion of fitness culture and wellness awareness has further strengthened demand among younger demographics and working professionals seeking convenient nutritional solutions.

Expansion of Sports and Clinical Nutrition Industries

The global sports nutrition sector continues to expand, supported by rising gym participation, endurance sports engagement, and lifestyle changes favoring active living. Milk proteins, particularly whey proteins, remain the benchmark ingredient for performance nutrition due to superior bioavailability. Additionally, aging populations are driving clinical nutrition demand, where milk proteins are used in medical foods designed for recovery, muscle preservation, and therapeutic diets.

What are the restraints for the global market?

Volatility in Raw Milk Prices

Milk protein production is directly influenced by fluctuations in raw milk supply and feed costs. Climate variability, dairy farm consolidation, and rising operational expenses can increase ingredient prices, impacting manufacturer margins and pricing stability across global markets.

Competition from Alternative Proteins

The growing popularity of plant-based proteins introduces competitive pressure, particularly in price-sensitive markets. While milk proteins maintain functional and nutritional superiority, sustainability concerns and dietary preferences are encouraging some brands to diversify protein sources, creating market challenges for traditional dairy ingredient suppliers.

What are the key opportunities in the milk protein industry?

Personalized and Functional Nutrition Growth

The emergence of personalized nutrition platforms presents strong opportunities for milk protein manufacturers to develop targeted formulations addressing specific health outcomes such as muscle recovery, aging support, and metabolic wellness. Customized protein blends supported by digital health monitoring are expected to generate premium product categories with higher profit margins.

Rising Demand Across Emerging Economies

Rapid urbanization and increasing disposable incomes across Asia-Pacific and Africa are driving demand for protein-enriched foods. Governments promoting nutritional awareness and food security programs are encouraging adoption of high-quality dairy proteins. Localization of processing facilities and partnerships with regional food manufacturers present strong growth opportunities for industry participants.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 15620 Million |

| Market Size in 2026 | USD 16885.22 Million |

| Market Size in 2031 | USD 24925 Million |

| CAGR | 8.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Whey protein concentrates continue to dominate the global milk protein market, accounting for nearly 32% of total demand in 2025, primarily driven by their optimal balance between protein concentration, functional performance, and cost efficiency. Their widespread adoption across sports nutrition formulations, fortified beverages, dairy alternatives, and processed food products positions them as the leading commercial protein ingredient. The growth of active lifestyles, increasing gym participation, and rising consumer preference for affordable high-protein formulations have significantly accelerated the uptake of whey protein concentrates among manufacturers seeking scalable nutrition solutions. Additionally, their superior emulsification, solubility, and flavor compatibility make them suitable for diverse industrial applications, further reinforcing segment leadership.Milk protein isolates are witnessing accelerated adoption due to their high protein purity, low lactose content, and superior amino acid profile, making them particularly suitable for infant nutrition, clinical nutrition, and premium functional foods. Increasing demand for clean-label and high-protein dietary solutions is encouraging manufacturers to incorporate isolates into specialized formulations targeting health-conscious consumers. Casein and caseinates remain essential ingredients within cheese production and slow-digesting nutritional products, as their sustained amino acid release supports muscle recovery and satiety-focused dietary applications. Furthermore, technological advancements in hydrolyzed whey proteins are expanding opportunities in medical nutrition, elderly care formulations, and hypoallergenic dietary products, enabling manufacturers to address highly specialized consumer health needs.

Application Insights

Sports and clinical nutrition applications represent one of the fastest-growing areas of milk protein utilization, contributing approximately 27% of total market demand in 2025. Growth in this segment is primarily driven by rising global awareness surrounding protein intake, muscle health, and preventive healthcare nutrition. Increasing participation in fitness activities, coupled with expanding demand for recovery-focused supplements and personalized nutrition solutions, continues to elevate milk proteins as core functional ingredients. Clinical nutrition applications are also expanding rapidly due to increasing incidences of chronic diseases, post-surgical recovery requirements, and growing elderly populations requiring protein-enriched dietary support.Traditional dairy products remain a major application segment supported by ongoing innovation in yogurt, cheese, and fortified milk beverages designed to enhance nutritional value and texture. Bakery and confectionery manufacturers are increasingly integrating milk proteins to improve moisture retention, structure stability, and protein enrichment claims, aligning products with evolving consumer health expectations. Ready-to-drink beverages have emerged as a key growth application as consumers increasingly favor convenient, on-the-go nutrition formats that combine functionality with portability. In addition, meat processing applications continue to expand as milk proteins provide essential water-binding, emulsification, and texture-enhancing properties, enabling improved product consistency and yield optimization across processed meat formulations.

Distribution Channel Insights

Business-to-business (B2B) ingredient supply remains the dominant distribution channel, accounting for nearly 70% of total market share, as milk proteins are primarily traded as functional ingredients supplied directly to food manufacturers, nutrition brands, and pharmaceutical companies. Long-term industrial contracts between dairy processors and multinational food corporations ensure consistent procurement volumes, price stability, and integrated supply chain efficiency. The growing scale of global food processing operations further strengthens the importance of bulk ingredient distribution models.Retail distribution channels are expanding steadily with the rapid growth of protein powders, ready-to-mix supplements, and fortified consumer nutrition products. The expansion of e-commerce platforms and direct-to-consumer nutrition brands has significantly improved accessibility to protein-based products across both developed and emerging markets. Foodservice channels are also witnessing gradual adoption as restaurants, cafés, and beverage chains introduce protein-enriched menu offerings, smoothies, and functional beverages to cater to health-conscious consumers seeking nutritional value alongside convenience.

End-Use Industry Insights

The food and beverage manufacturing industry remains the largest end-use sector, accounting for approximately 52% of total milk protein consumption. The segment’s dominance is driven by continuous product innovation focused on protein fortification, clean-label formulations, and functional ingredient integration across packaged foods and beverages. Manufacturers increasingly utilize milk proteins to enhance nutritional profiles while maintaining desirable taste and texture characteristics, supporting widespread adoption across mainstream consumer products.The global sports nutrition industry, valued at over USD 55 billion, represents one of the fastest-growing end-use sectors due to rising consumer focus on performance nutrition, muscle recovery, and weight management solutions. Infant nutrition applications continue expanding, particularly across Asia-Pacific markets, where premium infant formula demand is rising alongside increasing disposable incomes and heightened parental awareness of early-life nutrition. Clinical nutrition and elderly care foods are emerging as high-growth areas supported by aging global populations and healthcare-driven dietary management strategies. Additionally, export-oriented dairy economies benefit from growing international demand for high-quality protein ingredients, strengthening cross-border trade and industry expansion.

Explore more data points, trends and opportunities Download Free Sample Report

Milk Protein Market Segmentations

By Product Type

- Whey Protein Concentrates

- Whey Protein Isolates

- Milk Protein Isolates

- Casein Caseinates

- Hydrolyzed Milk Proteins

By Application

- Sports Clinical Nutrition

- Dairy Products

- Bakery Confectionery

- Beverages

- Meat Processing Functional Foods

By Distribution Channel

- B2B Ingredient Supply

- Retail Nutrition Products

- Foodservice Industrial Supply

Regional Insights

North America

North America accounted for nearly 31% of global market share in 2025, led predominantly by the United States, which maintains strong leadership in sports nutrition innovation and functional food development. Regional growth is driven by high consumer awareness regarding protein consumption, widespread adoption of fitness-oriented lifestyles, and strong penetration of ready-to-drink nutritional beverages. Advanced dairy processing infrastructure, continuous product innovation, and strong research investments by nutrition companies support the commercialization of specialized milk protein formulations. Additionally, well-established retail and e-commerce distribution networks enable rapid product availability, further accelerating regional demand growth.

Europe

Europe held approximately 28% market share, supported by leading dairy-exporting nations including Germany, France, Ireland, and the Netherlands. Regional growth is driven by stringent quality standards, advanced dairy technologies, and strong cooperative dairy systems that ensure consistent raw milk supply. European manufacturers benefit from well-developed export channels supplying premium milk protein ingredients to Asia-Pacific and Middle Eastern markets. Increasing consumer preference for clean-label, sustainably sourced proteins and regulatory emphasis on product traceability further strengthen regional competitiveness and support long-term market expansion.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, expanding at over 9% CAGR, fueled by rapid urbanization, rising disposable incomes, and increasing awareness of protein-rich diets. China remains the largest demand center due to strong infant formula consumption and expanding clinical nutrition markets, while India is experiencing significant growth supported by expanding dairy processing capacity, government initiatives promoting nutrition security, and growing adoption of sports nutrition products among younger populations. Southeast Asian countries are increasing imports of milk protein ingredients to support fast-growing processed food and beverage industries, further strengthening regional demand dynamics.

Latin America

Latin America accounts for roughly 9% of global demand, with Brazil and Mexico serving as primary growth engines. Regional expansion is supported by rising consumption of packaged foods, increasing urban middle-class populations, and growing investments in food processing infrastructure. Manufacturers are increasingly incorporating functional dairy ingredients into beverages, bakery products, and nutritional snacks to align with shifting dietary preferences toward higher protein intake. Improving retail penetration and modernization of supply chains are also enhancing product accessibility across the region.

Middle East & Africa

The Middle East and Africa region is experiencing steady market growth driven by increasing dependence on imported dairy proteins for large-scale food manufacturing. Countries such as Saudi Arabia, the UAE, and South Africa are witnessing expanding food processing industries supported by population growth, urbanization, and rising disposable incomes. Growing awareness of nutritional health, combined with government initiatives promoting food security and local manufacturing capabilities, is encouraging adoption of fortified food products containing milk proteins. Expansion of modern retail formats and rising demand for premium nutritional products further contribute to sustained regional market development.

Key Players in the Milk Protein Market

- Fonterra Co-operative Group

- Arla Foods Ingredients Group

- Lactalis Group

- FrieslandCampina Ingredients

- Glanbia plc

- Saputo Inc.

- Kerry Group plc

- Royal A-Ware

- AMCO Proteins

- Idaho Milk Products

- Leprino Foods Company

- Hilmar Cheese Company

- Agropur Cooperative

- Milk Specialties Global

- Ornua Co-operative Limited