Milk Homogenizer Machine Market Size

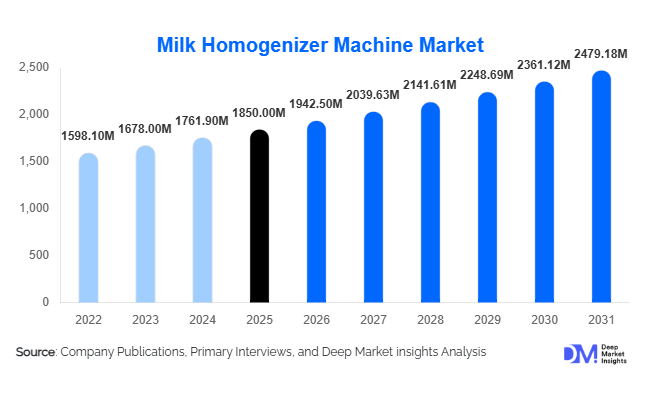

According to Deep Market Insights, the global milk homogenizer machine market size was valued at USD 1,850 million in 2025 and is projected to grow from USD 1,942.50 million in 2026 to reach USD 2,479.18 million by 2031, expanding at a CAGR of 5.0% during the forecast period (2026–2031). The milk homogenizer machine market growth is primarily driven by rising global dairy consumption, increasing demand for value-added dairy products, rapid expansion of plant-based milk alternatives, and modernization of dairy processing infrastructure worldwide.

Key Market Insights

- High-pressure homogenizers dominate the market, accounting for nearly 68% of global revenue in 2025 due to superior fat globule size reduction and industrial-scale efficiency.

- Fully automatic systems lead with over 58% share, reflecting strong adoption of PLC/SCADA-integrated dairy processing lines.

- Asia-Pacific holds the largest regional share (36%), driven by dairy capacity expansion in China and India.

- Medium-capacity homogenizers (5,000–20,000 LPH) account for 42% of installations, catering to expanding mid-sized dairy plants.

- Plant-based dairy processing is emerging as a high-growth application, growing at over 10% CAGR globally.

- Top five manufacturers collectively hold approximately 55% of the global market share, indicating moderate consolidation.

What are the latest trends in the milk homogenizer machine market?

Automation and Smart Dairy Processing Integration

Dairy processors are increasingly integrating homogenizers into fully automated production lines. Smart homogenizers equipped with IoT sensors, predictive maintenance systems, and energy optimization controls are gaining traction. These systems improve process consistency, reduce downtime, and enable real-time monitoring of pressure, temperature, and fat globule size. Industry 4.0 adoption is particularly strong in Europe and North America, where replacement demand for legacy systems is accelerating. Manufacturers are also offering retrofit kits to upgrade older homogenizers with digital control modules, creating additional aftermarket revenue streams.

Rising Demand from Plant-Based Dairy Production

The expansion of plant-based milk alternatives such as oat, almond, and soy milk is reshaping homogenizer demand. These products require fine emulsification and stability, driving investment in high-pressure and ultrasonic homogenization systems. Specialized homogenizers designed for protein-rich, low-fat emulsions are increasingly being deployed in alternative dairy facilities. As plant-based dairy markets grow at double-digit rates, equipment suppliers are customizing solutions for niche formulations and functional beverages, expanding the application scope beyond traditional milk processing.

What are the key drivers in the milk homogenizer machine market?

Rising Global Dairy Production and Consumption

Global milk production continues to expand, particularly in the Asia-Pacific and Latin America. Growing urbanization, increasing protein intake, and rising disposable incomes are boosting packaged milk and processed dairy demand. Industrial homogenization is critical for product stability, mouthfeel, and shelf life, making homogenizers essential equipment in modern dairy plants. Expanding export-oriented dairy production in countries such as New Zealand, Germany, and the United States further strengthens demand.

Growth in Value-Added Dairy Products

Products such as flavored milk, yogurt drinks, lactose-free milk, cream-based beverages, and high-protein dairy formulations require precise homogenization for texture consistency. As dairy processors shift toward premium and functional products with higher margins, investments in high-performance homogenizers are increasing. Medium-pressure (150–300 bar) systems remain popular due to their balance between cost efficiency and product quality.

What are the restraints for the global market?

High Capital Investment Requirements

High-pressure homogenizers, especially those exceeding 300 bar capacity, involve high upfront costs, often exceeding USD 500,000 for industrial-scale systems. This limits adoption among small and regional dairies, particularly in developing economies. Financing constraints and extended payback periods can delay purchasing decisions.

Volatility in Stainless Steel and Component Costs

Milk homogenizers rely heavily on food-grade stainless steel and precision-engineered valves. Fluctuations in raw material prices directly impact manufacturing costs and profit margins. Supply chain disruptions and import dependencies for specialized components also pose operational challenges for manufacturers.

What are the key opportunities in the milk homogenizer machine industry?

Government-Led Dairy Modernization Programs

Governments in emerging economies are prioritizing dairy infrastructure development to improve food safety, export competitiveness, and rural income generation. Initiatives such as “Make in India” and China’s manufacturing modernization programs are supporting investments in automated dairy equipment. Subsidies, tax incentives, and low-interest loans for food processing equipment create favorable conditions for homogenizer manufacturers to expand regional footprints.

Energy-Efficient and Sustainable Equipment Development

Energy consumption remains a high operational cost in dairy processing. Manufacturers that develop energy-efficient homogenizers with optimized valve design and reduced power consumption can gain competitive advantages. Sustainability-focused dairy processors are also seeking equipment with lower carbon footprints and enhanced durability, opening opportunities for innovation in materials and system engineering.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1850 Million |

| Market Size in 2026 | USD 1942.50 Million |

| Market Size in 2031 | USD 2479.18 Million |

| CAGR | 5.0% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Machine Type Insights

High-pressure homogenizers dominate the global milk homogenizer machine market, accounting for approximately 68% of global revenue in 2025. The primary driver behind this dominance is their superior capability to reduce fat globule size uniformly under pressures exceeding 150–300 bar, ensuring enhanced product stability, improved mouthfeel, and extended shelf life. Industrial-scale dairy processors prefer high-pressure systems because they deliver consistent emulsification across large production volumes while meeting stringent food safety and quality standards such as 3-A and EHEDG compliance. The rapid expansion of value-added dairy products, including flavored milk, high-protein beverages, lactose-free milk, and functional dairy drinks, has further strengthened demand for high-pressure systems due to their precision and efficiency. Additionally, export-oriented dairy plants require homogenizers capable of ensuring long shelf life and transportation stability, reinforcing the segment’s leadership.

Ultrasonic homogenizers are gradually emerging in niche applications, particularly in specialty beverages, nutraceutical dairy blends, and plant-based milk alternatives, where fine emulsification at micro-levels is critical. Meanwhile, mechanical and colloid homogenizers continue to serve small-scale dairies and localized processors, especially in developing economies where capital constraints favor lower-pressure, cost-effective solutions.

Capacity Insights

Medium-capacity homogenizers (5,000–20,000 LPH) lead the market with approximately 42% share of global installations in 2025. The growth driver for this segment is the rapid expansion of mid-sized dairy processing facilities across Asia-Pacific, Latin America, and parts of Eastern Europe. These systems provide an optimal balance between operational scalability and capital expenditure, making them suitable for regional dairy cooperatives and private processors scaling production. As dairy consumption increases in urbanizing markets, processors are upgrading from small-capacity systems to medium-range industrial units, driving sustained demand.

High-capacity homogenizers (>20,000 LPH) are concentrated in developed dairy-exporting economies such as Germany, the Netherlands, New Zealand, and the United States. These systems are driven by export demand, large-scale milk pooling operations, and multinational dairy conglomerates operating centralized mega-processing facilities. Low-capacity homogenizers remain relevant in fragmented rural dairy ecosystems and emerging markets, where small processors serve localized demand with limited investment capabilities.

Application Insights

Fluid milk and cream processing accounts for approximately 46% of total market demand in 2025, making it the leading application segment. The primary driver for this segment is the sustained global consumption of packaged milk, particularly in Asia-Pacific and North America. Homogenization is a mandatory step in standardized milk production to prevent cream separation and ensure product consistency. Increasing regulatory oversight on food quality and safety further reinforces homogenizer integration in milk processing lines.

Yogurt and fermented dairy products represent one of the fastest-growing traditional dairy segments, supported by rising probiotic consumption and health-conscious consumer trends. These products require precise homogenization to maintain texture stability and viscosity control. Additionally, plant-based dairy alternatives are the fastest-growing application overall, expanding at over 10% CAGR. The demand for stable emulsions in oat, soy, almond, and coconut milk is creating strong opportunities for advanced homogenization systems specifically engineered for alternative protein structures.

Automation Insights

Fully automatic homogenizers account for approximately 58% of total market revenue in 2025, driven primarily by the dairy industry's shift toward digital process control, operational efficiency, and labor optimization. The leading growth driver for this segment is the increasing adoption of Industry 4.0 practices in food processing plants. Automated systems equipped with PLC and SCADA integration allow real-time pressure monitoring, predictive maintenance, reduced downtime, and enhanced traceability. Regulatory compliance requirements in Europe and North America, along with export certification standards, are accelerating the transition from semi-automatic to fully automated solutions.

Semi-automatic systems continue to maintain demand in cost-sensitive and developing markets; however, their share is gradually declining as processors modernize operations and prioritize efficiency, consistency, and long-term cost savings.

Explore more data points, trends and opportunities Download Free Sample Report

Milk Homogenizer Machine Market Segmentations

By Machine Type

- High-Pressure Homogenizers

- Ultrasonic Homogenizers

- Mechanical/Colloid Homogenizers

By Capacity

- Low Capacity (<5,000 LPH)

- Medium Capacity (5,000–20,000 LPH)

- High Capacity (>20,000 LPH)

By Application

- Fluid Milk & Cream Processing

- Yogurt & Fermented Dairy Products

- Cheese & Processed Dairy

- Ice Cream & Frozen Dairy

- Plant-Based Dairy Alternatives

By Automation

- Semi-Automatic Homogenizers

- Fully Automatic Homogenizers

By Distribution Channel

- Direct OEM Sales

- EPC / Turnkey Dairy Plant Integrators

Regional Insights

Asia-Pacific

Asia-Pacific leads the global milk homogenizer machine market with a 36% share in 2025, making it the largest regional contributor. The primary drivers of growth include rapid urbanization, rising per capita dairy consumption, and strong government support for dairy modernization. China’s investment in industrial food processing infrastructure and India’s cooperative dairy expansion programs are central to regional growth. Government-backed initiatives focused on food safety compliance and cold chain development are encouraging dairy processors to adopt high-pressure, automated homogenization systems. India remains the fastest-growing country in the region, expanding at nearly 7% CAGR, supported by policy incentives, increasing milk production volumes, and the expansion of private dairy brands.

Europe

Europe accounts for approximately 28% of global demand in 2025, driven largely by replacement demand and technological upgrades. Germany, France, Italy, and the Netherlands are major markets due to their strong dairy export industries and established processing infrastructure. A key growth driver in Europe is the emphasis on energy-efficient equipment and sustainability compliance. Dairy processors are upgrading legacy homogenizers to reduce energy consumption and meet stringent EU food safety and environmental standards. Export-oriented dairy production and the strong presence of leading equipment manufacturers further reinforce regional market stability.

North America

North America holds around 22% of the global market share, with the United States contributing nearly 18%. Growth in this region is primarily driven by demand for value-added dairy products, including flavored milk, high-protein beverages, and lactose-free dairy. Automation and plant modernization initiatives are significant contributors, as U.S. dairy processors invest heavily in smart factory technologies. The growing plant-based milk industry in the U.S. is also accelerating demand for specialized homogenization systems. Additionally, strict FDA food safety standards support sustained equipment upgrades.

Latin America

Latin America represents approximately 8% of global revenue. Brazil and Argentina are leading contributors due to expanding dairy exports and improving industrial processing capabilities. The key growth driver in this region is the modernization of medium-scale dairy plants and increased export activity to neighboring markets and Asia. Government incentives supporting agricultural and dairy sector development are also encouraging capital expenditure in processing equipment.

Middle East & Africa

The Middle East & Africa region accounts for roughly 6% of the global market. Saudi Arabia and South Africa are major contributors, driven by dairy self-sufficiency initiatives and investments in large-scale dairy farms. The Middle East’s high reliance on processed and packaged milk products, combined with climate-driven domestic production expansion, is stimulating demand for high-capacity homogenizers. In Africa, the gradual industrialization of dairy processing and increasing foreign investments in food manufacturing are supporting steady, long-term growth.