Meat Substitutes Market Size

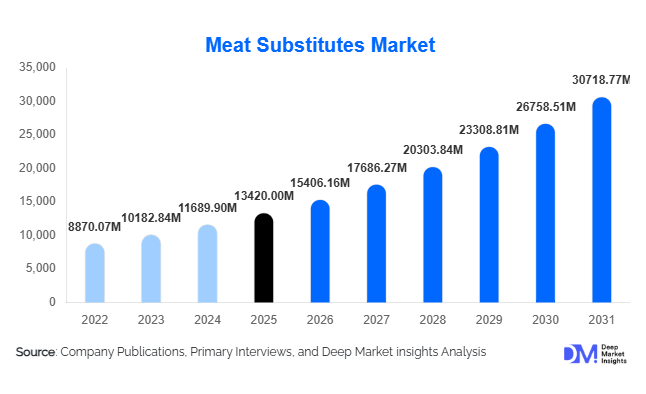

According to Deep Market Insights,the global meat substitutes market size was valued at USD 13,420 million in 2025 and is projected to grow from USD 15,406.16 million in 2026 to reach USD 30,718.77 million by 2031, expanding at a CAGR of 14.8% during the forecast period (2026–2031). The meat substitutes market growth is primarily driven by increasing consumer adoption of plant-based diets, rising environmental awareness associated with livestock production, and rapid innovation in alternative protein technologies that improve taste, texture, and nutritional equivalence to conventional meat products.

Key Market Insights

- Flexitarian consumers are driving mainstream adoption, expanding demand beyond vegan and vegetarian populations.

- Plant-based meat substitutes dominate the market, accounting for the majority of global revenue due to commercial maturity and retail availability.

- North America leads global consumption, supported by strong innovation ecosystems and foodservice partnerships.

- Asia-Pacific is the fastest-growing region, driven by urbanization, protein diversification, and food security initiatives.

- Foodservice integration is accelerating trial rates, with QSR chains incorporating plant-based menu options globally.

- Technological advancements, including precision fermentation and high-moisture extrusion, are improving product realism and reducing production costs.

What are the latest trends in the meat substitutes market?

Shift Toward Clean-Label and Functional Ingredients

Consumers increasingly demand meat substitutes formulated with recognizable and minimally processed ingredients. Manufacturers are reformulating products to reduce artificial additives, improve nutritional density, and enhance protein bioavailability. The inclusion of functional ingredients such as fiber, omega-rich oils, and micronutrients is becoming common, positioning meat substitutes as health-forward alternatives rather than simple meat replacements. Brands are also emphasizing allergen-free formulations, particularly moving away from soy toward pea, fava bean, and chickpea proteins. This clean-label trend is reshaping R&D priorities across the industry and influencing purchasing decisions among health-conscious consumers.

Expansion of Fermentation and Cultivated Protein Technologies

Precision fermentation and cultivated meat technologies are emerging as transformative innovations within the alternative protein ecosystem. Fermentation-derived fats and proteins enable manufacturers to replicate meat flavor and texture more accurately, overcoming historical barriers to adoption. Investment in biotechnology platforms is accelerating commercialization timelines, while partnerships between food manufacturers and biotech startups are expanding production scalability. These technologies also promise long-term cost reductions and improved sustainability metrics, strengthening the competitive positioning of meat substitutes against traditional animal proteins.

What are the key drivers in the meat substitutes market?

Growing Demand for Sustainable Protein Sources

Environmental concerns related to greenhouse gas emissions, land use, and water consumption from livestock farming are encouraging consumers and governments to adopt alternative protein solutions. Meat substitutes require significantly fewer natural resources compared to conventional meat production, aligning with global sustainability and ESG objectives. Food companies and retailers are increasingly committing to carbon reduction goals, which further accelerates adoption of plant-based protein options.

Rise of Flexitarian and Health-Conscious Diets

The rapid expansion of flexitarian diets represents one of the strongest growth drivers. Consumers are reducing meat consumption for health reasons such as cholesterol management and weight control rather than eliminating meat entirely. This behavioral shift significantly broadens the target consumer base, enabling meat substitutes to compete within mainstream protein categories. Increased awareness of lifestyle-related diseases and demand for plant-forward diets are reinforcing long-term growth prospects.

What are the restraints for the global market?

Price Premium Compared to Conventional Meat

Despite economies of scale improving production efficiency, meat substitutes often remain more expensive than traditional meat products. Price sensitivity in emerging economies limits adoption among mass consumers. Achieving cost parity remains a critical objective for manufacturers seeking wider penetration across price-sensitive markets.

Consumer Perception Around Processing Levels

Some consumers perceive meat substitutes as highly processed foods, which can slow adoption among clean-eating segments. Addressing ingredient transparency and simplifying formulations remain essential challenges for producers aiming to build long-term consumer trust.

What are the key opportunities in the meat substitutes industry?

Institutional and Government Procurement Programs

Public institutions such as schools, hospitals, and airlines are increasingly integrating plant-based meals to meet sustainability commitments. Government-backed procurement programs provide stable demand volumes and enable manufacturers to scale production efficiently. Institutional adoption also increases consumer familiarity with alternative proteins, accelerating mainstream acceptance.

Localized Product Innovation in Emerging Markets

Emerging economies present strong opportunities through culturally adapted meat substitute products. Regional flavor customization, affordability-focused formulations, and hybrid protein products tailored to local cuisines are expanding consumer acceptance. Markets such as India, China, and Southeast Asia are witnessing rising experimentation with plant-based proteins as urban populations seek diversified protein sources.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 13420 Million |

| Market Size in 2026 | USD 15406.16 Million |

| Market Size in 2031 | USD 30718.77 Million |

| CAGR | 14.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Plant-based meat substitutes continue to dominate the global meat substitutes market, accounting for approximately 86% of total revenue, primarily driven by mature commercialization, large-scale manufacturing capabilities, and widespread availability across modern retail and foodservice channels. Products formulated using soy, pea, and wheat proteins remain the most widely consumed due to their established sensory performance, affordability, and strong nutritional positioning compared to traditional animal proteins. The leading segment growth is supported by continuous improvements in texture engineering, flavor masking technologies, and clean-label formulations that enhance consumer acceptance among flexitarian and mainstream consumers. Additionally, manufacturers are expanding portfolios with fortified and high-protein variants to align with health-conscious consumption trends.

Fermentation-derived proteins are emerging as a rapidly expanding category, supported by advancements in precision fermentation technologies, increasing venture capital investment, and scalability improvements that enable consistent protein functionality. These products offer advantages such as reduced environmental impact, improved amino acid profiles, and enhanced production efficiency, making them attractive for food manufacturers seeking sustainable ingredient solutions. Cultivated meat remains at an early commercialization stage but demonstrates long-term growth potential as regulatory approvals expand across key markets and production costs gradually decline through bioprocess optimization. Ongoing diversification into ready-to-cook, frozen, and ready-to-eat product formats is further strengthening market penetration by improving convenience and expanding adoption across diverse consumer demographics.

Application Insights

Burgers and patties represent the leading application segment within the global meat substitutes market, driven primarily by strong integration into quick-service restaurant menus and standardized manufacturing processes that enable consistent quality at scale. The leading segment growth is supported by high consumer familiarity with burger formats, ease of substitution from conventional meat products, and extensive promotional partnerships between alternative protein brands and global foodservice operators. These factors have significantly accelerated trial rates and repeat consumption among flexitarian consumers.

Nuggets, sausages, and minced meat alternatives are gaining substantial traction due to their versatility across multiple cuisines and meal occasions, allowing manufacturers to cater to regional culinary preferences. Ready-to-eat meals incorporating meat substitutes are experiencing accelerated growth as global demand for convenient and time-saving meal solutions rises alongside urban lifestyles. Food manufacturers are increasingly introducing hybrid products that combine plant-based and animal-derived ingredients, enabling gradual dietary transitions while maintaining familiar taste profiles. This expansion beyond traditional vegetarian offerings is broadening the consumer base and enhancing category accessibility.

Distribution Channel Insights

Retail supermarkets and hypermarkets dominate global sales, accounting for the largest market share due to extensive shelf visibility, established cold-chain infrastructure, and strong consumer trust associated with organized retail environments. The leading distribution channel growth is driven by expanding private-label product launches, in-store promotional strategies, and improved product placement within mainstream protein categories rather than niche health sections. Retail expansion into emerging markets is further improving accessibility and supporting volume growth.

Online retail and direct-to-consumer platforms are witnessing rapid expansion, supported by increasing digital grocery adoption, subscription-based purchasing models, and enhanced product discovery through e-commerce platforms. Foodservice channels, particularly quick-service restaurants and casual dining establishments, are emerging as critical growth drivers by increasing consumer exposure and normalizing plant-based alternatives through menu integration. Institutional distribution channels, including corporate cafeterias and public procurement systems, are also expanding as organizations adopt sustainability-focused sourcing policies and carbon reduction targets.

End-Use Insights

Household consumption remains the largest end-use segment, supported by rising home cooking trends, growing health awareness, and broader availability of meat substitutes across retail outlets. The leading segment driver is the increasing adoption of flexitarian diets, where consumers seek to reduce meat intake without fully eliminating animal products. Product innovation focused on taste parity, nutritional fortification, and easy-to-cook formats continues to encourage repeat purchases among households.

Foodservice represents the fastest-growing end-use category as restaurants introduce plant-based menu options to diversify offerings, attract younger consumers, and align with sustainability positioning. Food processing companies are increasingly incorporating meat substitutes into frozen meals, snacks, and packaged convenience foods, creating new industrial demand streams and enabling large-scale consumption growth. Institutional catering, including airlines, hospitals, and universities, is emerging as a stable demand contributor as organizations integrate environmentally responsible meal solutions into procurement strategies.

Explore more data points, trends and opportunities Download Free Sample Report

Meat Substitutes Market Segmentations

By Product Type

- Plant-Based Meat Substitutes

- Fermentation-Derived Proteins

- Mycoprotein-Based Products

- Textured Vegetable Protein (TVP)

- Tofu, Tempeh & Soy-Based Alternatives

- Cultivated (Cell-Based) Meat Alternatives

- Hybrid Plant-Animal Protein Products

By Application

- Burgers & Patties

- Sausages & Hot Dogs

- Nuggets, Strips & Cutlets

- Ground/Minced Meat Alternatives

- Ready-to-Eat & Frozen Meals

- Food Processing Ingredients

- Snacks & Convenience Foods

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail & Direct-to-Consumer

- Foodservice & Quick Service Restaurants

- Specialty Health & Organic Stores

- Institutional Sales (Airlines, Schools, Hospitals)

By End Use

- Household Consumption

- Foodservice Industry

- Food Processing Manufacturers

- Institutional Catering

Regional Insights

North America

North America accounted for approximately 38% of the global meat substitutes market in 2025, led primarily by the United States, which benefits from advanced food technology ecosystems and strong venture capital investment in alternative proteins. Regional growth is driven by high consumer awareness of health and environmental sustainability, widespread retail penetration, and strong collaboration between alternative protein companies and major restaurant chains. Increasing demand for high-protein and clean-label foods, combined with rising flexitarian adoption, continues to support market expansion. Canada is strengthening regional supply chains through increased domestic cultivation of protein crops such as peas and soybeans, improving raw material availability and cost efficiency while supporting long-term market resilience.

Europe

Europe held nearly 30% market share, supported by stringent sustainability regulations, climate-focused food policies, and widespread adoption of plant-based diets. Regional growth is driven by government initiatives encouraging reduced carbon emissions within the food system, strong vegan and flexitarian populations, and high consumer willingness to pay for sustainable products. Germany, the United Kingdom, and the Netherlands lead regional demand due to advanced retail infrastructure and active product innovation. Expansion of private-label offerings, improved labeling transparency, and increasing investment in alternative protein research are further accelerating regional adoption and market maturity.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, with a CAGR exceeding 17%, driven by demographic expansion, rapid urbanization, and evolving dietary preferences. China’s strategic focus on food security and protein diversification is encouraging investment in alternative protein development, while India’s large vegetarian population provides a strong cultural foundation for adoption. Japan’s innovation-driven food industry is advancing product development through technology integration and premium product positioning. Rising disposable incomes, expanding modern retail networks, and growing awareness of health and sustainability benefits are collectively accelerating regional demand and enabling long-term growth potential.

Latin America

Latin America is emerging as a promising growth region, led by Brazil and Mexico, supported by abundant soy production and expanding processed food industries. Regional growth drivers include increasing health awareness, rising middle-class consumption, and growing export-oriented manufacturing capabilities for plant-based products. Local manufacturers are leveraging agricultural advantages to develop cost-competitive offerings, while retail modernization and international brand entry are improving product accessibility. The gradual shift toward healthier dietary habits and sustainable food consumption is expected to strengthen regional market penetration over the forecast period.

Middle East & Africa

The Middle East & Africa region is witnessing gradual but steady adoption of meat substitutes, driven by rising urbanization, increasing disposable incomes, and growing interest in sustainable food solutions. The Middle East, particularly the UAE and Israel, is experiencing strong demand among high-income consumers seeking premium and innovative food products. Israel is emerging as a global innovation hub for cultivated meat technologies due to strong startup ecosystems and supportive regulatory frameworks. Across Africa, expanding urban retail infrastructure, improving cold-chain logistics, and increasing exposure to international food trends are supporting early-stage adoption, positioning the region for long-term growth as awareness and accessibility continue to improve.

Key Players in the Meat Substitutes Market

- Beyond Meat Inc.

- Impossible Foods Inc.

- Nestlé S.A.

- Conagra Brands Inc.

- Maple Leaf Foods Inc.

- Kellogg Company (MorningStar Farms)

- Unilever PLC

- Tyson Foods Inc.

- Marlow Foods (Quorn Foods)

- Oatly Group AB

- Eat Just Inc.

- Vivera Holding BV

- Sunfed Meats

- VBites Foods Ltd.

- Tofurky Company