Meat Starter Cultures Market Size

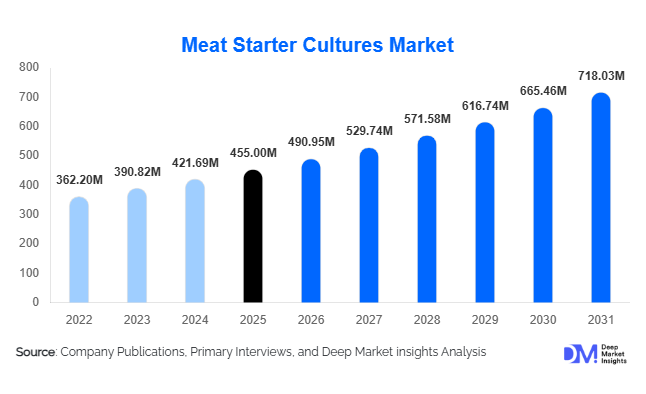

According to Deep Market Insights, the global meat starter cultures market size was valued at USD 455 million in 2025 and is projected to grow from USD 490.95 million in 2026 to reach USD 718.03 million by 2031, expanding at a CAGR of 7.9% during the forecast period (2026–2031). The market growth is primarily driven by the increasing consumption of processed and fermented meat products, rising demand for clean-label food ingredients, and stringent food safety regulations globally.

Key Market Insights

- Lactic acid bacteria dominate the market, accounting for over 50% share due to their critical role in acidification and food safety.

- Freeze-dried cultures are the preferred format, contributing more than 60% of market share owing to ease of storage and extended shelf-life.

- Europe leads the global market, supported by strong consumption of fermented meat products such as salami and dry-cured meats.

- Asia-Pacific is the fastest-growing region, driven by rising processed meat consumption and urbanization.

- Industrial meat processors account for the majority of demand, contributing nearly 70% of total market consumption.

- Technological advancements in microbial strain development are enabling customized cultures for flavor, texture, and shelf-life enhancement.

What are the latest trends in the meat starter cultures market?

Clean-Label and Natural Fermentation Trends

The increasing consumer preference for natural and additive-free food products is driving demand for clean-label meat processing solutions. Starter cultures are being widely adopted as natural preservatives, replacing synthetic chemicals such as nitrites and nitrates. This trend is particularly strong in developed markets where regulatory pressures and consumer awareness are high. Manufacturers are investing in developing cultures that enhance natural fermentation while improving safety and sensory attributes.

Customization and Precision Fermentation

Advancements in biotechnology are enabling the development of highly customized starter cultures tailored to specific meat products. Precision fermentation techniques allow manufacturers to control flavor profiles, texture, and maturation time more effectively. This trend is especially relevant for premium and artisanal meat producers seeking product differentiation. Genomic sequencing and strain optimization are also improving efficiency and consistency in meat processing.

What are the key drivers in the meat starter cultures market?

Growing Processed Meat Consumption

The rising global demand for processed meat products such as sausages, salami, and cured meats is a major driver for the market. Urbanization, busy lifestyles, and the demand for convenience foods are significantly boosting processed meat consumption, thereby increasing the adoption of starter cultures in industrial processing.

Stringent Food Safety Regulations

Governments and regulatory bodies worldwide are implementing strict food safety standards, particularly for meat processing. Starter cultures help inhibit harmful pathogens and ensure consistent fermentation, making them essential for regulatory compliance and quality assurance.

What are the restraints for the global market?

High Cost of Advanced Starter Cultures

Specialized and customized starter cultures involve high production costs due to advanced R&D and processing requirements. This can limit adoption among small-scale producers, particularly in developing regions.

Limited Technical Expertise

The effective use of starter cultures requires technical knowledge and controlled fermentation environments. Lack of expertise in emerging markets can hinder adoption and impact product quality.

What are the key opportunities in the meat starter cultures industry?

Expansion in Emerging Markets

Rapid urbanization and increasing disposable incomes in Asia-Pacific and Latin America are creating strong growth opportunities. Rising demand for processed meat products in countries such as China, India, and Brazil is expected to drive market expansion significantly.

Growth of Artisanal and Premium Meat Products

The increasing popularity of artisanal and premium meat products is opening new avenues for specialized starter cultures. Small-scale producers are adopting these cultures to maintain consistency while preserving traditional flavors, creating a high-margin niche segment.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 455 Million |

| Market Size in 2026 | USD 490.95 Million |

| Market Size in 2031 | USD 718.03 Million |

| CAGR | 7.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Microorganism Type Insights

The microorganism type segment plays a fundamental role in determining product quality, safety, sensory characteristics, and processing efficiency within the meat starter cultures market. Lactic acid bacteria dominate the market with approximately 52% share, primarily due to their critical function in rapid acidification, pathogen inhibition, and shelf-life enhancement. The leading position of this segment is strongly driven by the increasing need for controlled fermentation processes that ensure consistent product quality and compliance with global food safety standards. Lactic acid bacteria enable manufacturers to achieve predictable pH reduction, improved microbial stability, and enhanced texture development, making them indispensable in large-scale industrial meat processing operations. Additionally, growing consumer demand for naturally preserved and clean-label meat products has further strengthened adoption, as these cultures reduce reliance on synthetic preservatives while maintaining product safety.Coagulase-negative cocci are widely utilized for their ability to enhance flavor complexity, color stabilization, and oxidative stability in fermented meat products. Their enzymatic activity contributes significantly to aroma development and cured meat appearance, particularly in premium and traditional European-style products. Meanwhile, yeasts and molds are gaining increasing importance in specialty and dry-cured applications, where they improve surface maturation, aroma formation, and moisture regulation. These microorganisms are increasingly adopted in high-value artisanal and gourmet products as manufacturers seek product differentiation through authentic sensory profiles. Mixed cultures are also witnessing rising adoption, as processors increasingly prefer multifunctional solutions that combine acidification, flavor formation, and preservation benefits within a single culture system, improving operational efficiency and reducing formulation complexity.

Application Insights

Application-based demand highlights the dominance of fermented sausages, which account for the largest share of around 48% of the global market. The leading position of this segment is driven by strong global consumption patterns, wide product variety, and the scalability of fermented sausage production across industrial and artisanal manufacturing environments. Starter cultures are essential in this application to ensure controlled fermentation, uniform taste, and microbial safety, which are critical for meeting regulatory standards and consumer expectations. Increasing consumer preference for protein-rich ready-to-eat foods and traditional preserved meat products continues to accelerate demand within this segment.Dry-cured meat products represent another significant application area, particularly across European markets where long-standing culinary traditions support sustained consumption. The growth of premium and specialty meat categories has encouraged producers to adopt advanced starter cultures that improve consistency while preserving traditional flavor characteristics. Cooked fermented products are gaining traction in emerging economies, supported by urbanization, rising disposable incomes, and expanding retail distribution channels. Additionally, traditional and regional meat products contribute to steady market expansion, as local processors increasingly incorporate starter cultures to modernize production while maintaining authentic regional taste profiles and improving food safety outcomes.

Form Insights

Based on form, freeze-dried cultures lead the market with over 61% share, primarily driven by their superior stability, extended shelf-life, and simplified logistics. The leading growth driver for this segment is the increasing globalization of meat processing supply chains, where manufacturers require cultures that can be transported and stored without complex cold-chain infrastructure. Freeze-dried cultures offer operational convenience, accurate dosing, and reduced contamination risk, making them highly suitable for large-scale industrial production. Their ability to maintain microbial viability over long storage periods further enhances cost efficiency and inventory management for processors.Frozen cultures remain important for high-performance fermentation applications where maximum microbial activity and rapid fermentation initiation are required. These cultures are often preferred by large processors producing premium or highly standardized products. Liquid cultures, while representing a smaller share, continue to serve niche applications and small-scale production environments where immediate culture activation and customized formulations are advantageous. Growth in artisanal processing and localized meat production is expected to sustain gradual demand for liquid culture formats.

End-User Insights

Industrial meat processors dominate the end-user landscape, accounting for approximately 68% of total demand. The leading driver behind this segment’s dominance is the increasing industrialization of meat processing combined with the need for standardized quality, scalability, and regulatory compliance. Large processors rely heavily on starter cultures to ensure batch-to-batch consistency, optimize production timelines, and minimize contamination risks. Automation in meat processing facilities and growing exports of processed meat products have further accelerated adoption among industrial manufacturers.Artisanal producers are emerging as a rapidly expanding segment, particularly within premium and specialty meat categories. These producers increasingly adopt starter cultures to balance traditional craftsmanship with modern safety standards, enabling them to achieve authentic flavors while improving product reliability. Foodservice applications are expanding gradually as restaurants and specialty food providers introduce fermented and cured meat offerings to meet evolving consumer tastes, contributing to incremental demand growth across this segment.

Explore more data points, trends and opportunities Download Free Sample Report

Meat Starter Cultures Market Segmentations

By Microorganism Type

- Lactic Acid Bacteria

- Coagulase-Negative Cocci

- Yeasts

- Molds

- Mixed/Composite Cultures

By Application

- Fermented Sausages

- Dry-Cured Meat Products

- Cooked Fermented Meat Products

- Traditional/Regional Meat Products

By Distribution Channel

- Direct Sales

- Distributors & Ingredient Suppliers

Regional Insights

Europe

Europe holds the largest market share of approximately 38%, supported by deep-rooted consumption traditions for fermented and dry-cured meat products in countries such as Germany, Italy, Spain, and France. Regional growth is strongly driven by the presence of established meat processing industries, advanced fermentation technologies, and stringent food safety regulations that encourage the use of standardized starter cultures. Increasing demand for premium cured meats, geographical indication (GI) products, and clean-label formulations further supports market expansion. Additionally, innovation in culture development and strong collaboration between food research institutions and manufacturers continue to reinforce Europe’s leadership position in the market.

North America

North America accounts for around 28% of the market, led primarily by the United States, where large-scale industrial meat processing operations drive substantial demand for starter cultures. Regional growth is supported by rising consumer awareness regarding food safety, increasing preference for minimally processed and clean-label meat products, and growing consumption of ready-to-eat protein foods. Technological advancements in fermentation control, coupled with strong investments in food innovation and product standardization, are accelerating adoption across both industrial and premium meat segments. Expansion of specialty meat brands and private-label offerings also contributes to sustained regional growth.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, expanding at a CAGR of approximately 9.5%. Growth in this region is driven by rapid urbanization, rising disposable incomes, and shifting dietary patterns toward processed and convenience meat products. Countries such as China, India, and Japan are witnessing strong expansion of organized food processing industries, increasing cold-chain infrastructure, and growing adoption of Western-style fermented meat products. Additionally, improving regulatory frameworks related to food safety and increasing investments by global meat processors are encouraging the adoption of starter cultures to enhance production efficiency and product consistency.

Latin America

Latin America holds around 12% market share, with Brazil and Argentina serving as key growth engines due to their strong meat production and export-oriented industries. Regional market expansion is supported by increasing modernization of meat processing facilities, rising demand for value-added meat products, and growing export requirements that necessitate standardized fermentation practices. The region’s strong livestock base and expanding processed food consumption among urban populations further contribute to sustained demand for starter cultures.

Middle East & Africa

The Middle East & Africa region accounts for approximately 7% of the global market, with growth driven by rapid urbanization, population expansion, and increasing demand for packaged and processed food products. Rising investments in food manufacturing infrastructure, particularly in countries such as the UAE and South Africa, are supporting adoption of advanced processing technologies including starter cultures. Increasing retail penetration, evolving consumer lifestyles, and growing reliance on imported processed meat products are further encouraging regional manufacturers to adopt controlled fermentation solutions to improve product safety, shelf-life, and quality consistency.

Key Players in the Meat Starter Cultures Market

- Chr. Hansen

- DSM-Firmenich

- Kerry Group

- Lallemand Inc.

- Sacco System

- Biochem SRL

- CSK Food Enrichment

- Bioprox

- Dalton Biotechnologies

- Meat Cracks Technologie

- Bactoferm

- LB Bulgaricum

- Mediterranea Biotecnologie

- Aplin & Barrett

- Sacco Srl