Meat Speciation Testing Market Size

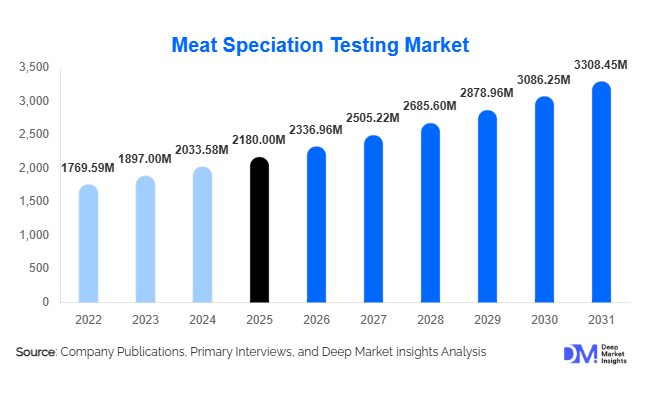

According to Deep Market Insights, the global meat speciation testing market size was valued at USD 2,180 million in 2025 and is projected to grow from USD 2,336.96 million in 2026 to reach USD 3,308.45 million by 2031, expanding at a CAGR of 7.2% during the forecast period (2026–2031). Market growth is primarily driven by rising food fraud incidents, stringent regulatory mandates on labeling and traceability, expanding global meat trade, and increasing consumer demand for transparency in processed meat products.

Key Market Insights

- PCR-based testing dominates the market, accounting for over 50% of total revenues due to high sensitivity, regulatory acceptance, and rapid turnaround times.

- Adulteration detection remains the leading testing objective, contributing nearly half of total testing volumes globally.

- North America leads the global market, supported by strict USDA and FDA enforcement and high processed meat consumption.

- Asia-Pacific is the fastest-growing region, driven by expanding meat exports, tightening food safety regulations, and rising halal certification requirements.

- Independent food testing laboratories represent the largest end-use segment, owing to accreditation requirements for export certification.

- Halal and kosher authentication demand is accelerating, particularly in Southeast Asia, the Middle East, and export-oriented economies.

What are the latest trends in the meat speciation testing market?

Shift Toward High-Throughput and Multiplex PCR Platforms

Laboratories are increasingly adopting multiplex real-time PCR systems capable of detecting multiple species within a single assay. This significantly reduces per-sample testing costs while improving throughput efficiency. Automation and robotic sample preparation are also gaining traction, especially in large independent labs handling export certifications. The integration of digital reporting systems with laboratory information management systems (LIMS) is further streamlining compliance documentation and traceability, improving operational efficiency.

Rising Demand for Halal and Religious Compliance Testing

Global halal meat trade expansion is significantly influencing testing volumes. Countries such as Malaysia, Indonesia, Saudi Arabia, and the UAE are strengthening halal certification requirements, increasing routine pork detection testing in meat products. Exporters from Brazil, Australia, and India are expanding batch-level verification processes to maintain access to Muslim-majority markets. This trend is expected to sustain long-term demand growth, particularly for rapid and highly sensitive PCR-based solutions.

What are the key drivers in the meat speciation testing market?

Stringent Regulatory Enforcement

Governments across North America and Europe have implemented strict species identification and labeling regulations following global food fraud scandals. Mandatory inspection frameworks and random sampling programs have institutionalized routine meat testing, transforming it from reactive investigation to proactive compliance. Import-export screening requirements are further expanding test volumes.

Expansion of Processed and Ready-to-Eat Meat Consumption

The rapid growth of processed meat products, including sausages, frozen meals, and ready-to-cook items, has increased the risk of cross-contamination and adulteration. With the global processed meat industry exceeding USD 900 billion in 2025, testing demand is closely tied to production expansion. Emerging markets in the Asia-Pacific are particularly contributing to higher sample testing volumes.

What are the restraints for the global market?

High Equipment and Operational Costs

Advanced PCR and sequencing platforms require significant capital investment, limiting in-house adoption among small and medium-sized meat processors. Many rely on third-party laboratories, which can increase turnaround times and operational complexity.

Complexity in Testing Highly Processed Products

DNA degradation in heat-treated or heavily processed products can affect test sensitivity. Variability in international standards and cross-reactivity challenges can complicate validation processes, particularly for exporters operating across multiple regulatory jurisdictions.

What are the key opportunities in the meat speciation testing industry?

Emerging Market Export Expansion

Countries such as Brazil, Argentina, Thailand, and Vietnam are expanding processed meat exports. Compliance with EU and U.S. standards requires accredited laboratory testing, creating recurring revenue streams for service providers. Establishing regional labs and forming public-private partnerships with export inspection authorities represent strong growth avenues.

Portable and On-Site Testing Solutions

Compact PCR devices and isothermal amplification technologies are enabling on-site verification within processing plants. This reduces dependency on external labs and shortens supply chain response times. Companies developing user-friendly, automated platforms are well-positioned to capture mid-sized processor demand globally.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2180 Million |

| Market Size in 2026 | USD 2336.96 Million |

| Market Size in 2031 | USD 3308.45 Million |

| CAGR | 7.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Technology Insights

PCR-based testing holds approximately 52% of the 2025 global market share, maintaining its leadership position due to superior analytical sensitivity, rapid turnaround time, regulatory acceptance, and scalability for high-throughput laboratory operations. The dominance of PCR is fundamentally driven by increasing regulatory mandates requiring validated DNA-based confirmation methods for species identification, particularly in processed and heat-treated meat products, where protein-based methods may lack precision. Multiplex real-time PCR represents the leading sub-segment, as it allows simultaneous detection of multiple species within a single reaction, significantly reducing per-sample costs and improving laboratory efficiency. This efficiency is critical in export-oriented markets where batch-level testing volumes are high.

Immunoassay-based testing continues to play a supporting role, particularly for rapid on-site screening and preliminary quality checks within processing facilities. However, its relatively lower specificity compared to DNA-based methods limits its application in formal regulatory reporting. DNA sequencing technologies, including next-generation sequencing (NGS), are increasingly adopted in complex adulteration investigations, forensic audits, and high-value export disputes where deeper genomic resolution is required. Mass spectrometry-based testing is gaining traction for confirmatory analysis in highly processed matrices. The growing need for automation, laboratory accreditation compliance, and digital traceability integration further reinforces PCR’s structural dominance across global markets.

Testing Objective Insights

Adulteration detection represents approximately 49% of total global revenues in 2025, making it the largest testing objective segment. Its leadership is primarily driven by persistent economic adulteration risks in global meat supply chains, especially in processed and multi-ingredient products. Regulatory authorities in North America and Europe have institutionalized routine sampling programs following past food fraud incidents, creating sustained structural demand for species verification testing.

Label verification and regulatory compliance testing constitute the second-largest objective segment, particularly in export-driven economies where incorrect labeling can result in shipment rejections, financial penalties, and reputational damage. This is especially relevant for exporters supplying the European Union and North American markets, where documentation and batch-level traceability are mandatory. Halal and kosher authentication testing is the fastest-growing objective sub-segment, supported by expanding Muslim consumer populations, increasing halal-certified exports from Brazil, India, and Australia, and stricter certification frameworks across Southeast Asia and the Middle East. Religious compliance testing is increasingly transitioning from periodic audits to systematic verification protocols, thereby expanding recurring testing volumes.

End-Use Insights

Food testing laboratories account for approximately 38% of global market revenues in 2025, positioning them as the leading end-use segment. Their dominance is driven by ISO/IEC 17025 accreditation requirements, which are mandatory for export certification and regulatory reporting in many countries. Independent laboratories offer higher credibility for compliance validation, making them preferred partners for exporters and multinational food processors. The consolidation of testing laboratories through mergers and acquisitions has further expanded geographic coverage and enhanced technical capabilities, reinforcing this segment’s leadership.

Food and beverage manufacturers represent a substantial share of demand due to the increasing integration of in-house quality assurance programs. Large processors are investing in internal PCR platforms to reduce turnaround times and minimize supply chain disruptions. Meanwhile, the pet food manufacturing segment is emerging as one of the fastest-growing end-use categories. Stricter labeling regulations in the United States and Europe, coupled with premiumization trends in pet nutrition, are driving higher testing frequency to ensure species authenticity and prevent cross-contamination. Growth in private-label retail brands is also contributing to increased supplier-level verification requirements.

Explore more data points, trends and opportunities Download Free Sample Report

Meat Speciation Testing Market Segmentations

By Technology Platform

- PCR-Based Testing

- Immunoassay-Based Testing

- DNA Sequencing

- Mass Spectrometry-Based Testing

- Isothermal Amplification Techniques

By Testing Objective

- Adulteration Detection

- Label Verification & Regulatory Compliance

- Halal & Kosher Authentication

- Allergen & Cross-Contamination Detection

- Fraud Investigation & Forensic Analysis

By End-Use Industry

- Food Testing Laboratories

- Food & Beverage Manufacturers

- Regulatory & Government Authorities

- Retail & Private Label Brands

- Pet Food Manufacturers

Regional Insights

North America

North America holds approximately 32% of the 2025 global market share, with the United States representing the largest national contributor. Regional growth is primarily driven by stringent oversight from regulatory bodies such as the U.S. Department of Agriculture (USDA) and the Food and Drug Administration (FDA), which mandate routine species verification and labeling compliance. The region’s large processed meat industry, high per capita meat consumption, and well-established laboratory infrastructure further support testing volumes. Canada contributes significantly through export-oriented compliance testing, particularly for shipments to the European Union and Asia-Pacific markets. Increased scrutiny on pet food labeling and private-label retail brands is also accelerating demand across North America.

Europe

Europe accounts for roughly 30% of global revenues in 2025, supported by one of the most stringent food authenticity regulatory frameworks globally. The European Union’s strict traceability regulations and coordinated cross-border inspection mechanisms drive consistent demand for routine meat speciation testing. Germany, France, the United Kingdom, Italy, and Spain serve as major testing hubs due to their large meat processing sectors and intra-EU trade flows. Regional growth is further supported by high consumer awareness regarding food transparency, strong enforcement following past food fraud incidents, and robust accreditation systems. Additionally, Europe’s significant meat import volumes necessitate continuous import screening, reinforcing laboratory demand.

Asia-Pacific

Asia-Pacific holds approximately 24% of the global market share in 2025 and is the fastest-growing region, with an estimated CAGR of nearly 9%. Growth is primarily driven by tightening food safety regulations in China, the expansion of halal-certified exports from India and Southeast Asia, and rising processed meat consumption across urban centers. China’s regulatory modernization programs have expanded domestic laboratory infrastructure, increasing internal testing volumes. India’s growing role as a buffalo meat exporter has intensified batch-level compliance testing. Meanwhile, Japan and Australia represent mature but stable markets, supported by high-quality export standards and advanced laboratory capabilities. Rapid urbanization, expanding middle-class populations, and export diversification strategies continue to accelerate regional growth.

Latin America

Latin America contributes approximately 8% of global demand in 2025, with Brazil and Argentina serving as the primary growth engines. Regional demand is strongly export-driven, as both countries are among the world’s largest beef and poultry exporters. Compliance with European, Middle Eastern, and Asian import regulations necessitates systematic species verification. Investments in accredited laboratory infrastructure and government-backed export inspection programs are further strengthening regional capabilities. Growing trade agreements and diversification into value-added processed meat exports are expected to sustain testing growth.

Middle East & Africa

The Middle East & Africa region holds roughly 6% of global market share in 2025, with Saudi Arabia, the UAE, and South Africa leading demand. The primary regional growth driver is halal compliance enforcement, as pork contamination testing is mandatory for certified imports and domestic distribution. Increasing meat import dependence in Gulf countries necessitates rigorous screening protocols. In Africa, South Africa’s relatively advanced food safety infrastructure supports steady demand, while emerging economies are gradually expanding laboratory investments. Rising population growth, urbanization, and increasing packaged food consumption across the region are expected to gradually enhance long-term market potential.

Key Players in the Meat Speciation Testing Market

- Eurofins Scientific

- SGS SA

- Intertek Group plc

- Bureau Veritas

- ALS Limited

- Thermo Fisher Scientific

- Merieux NutriSciences

- Neogen Corporation

- Romer Labs

- Bio-Rad Laboratories

- Agilent Technologies

- PerkinElmer

- Qiagen

- LGC Limited

- TUV SUD