Meat Products Market Size

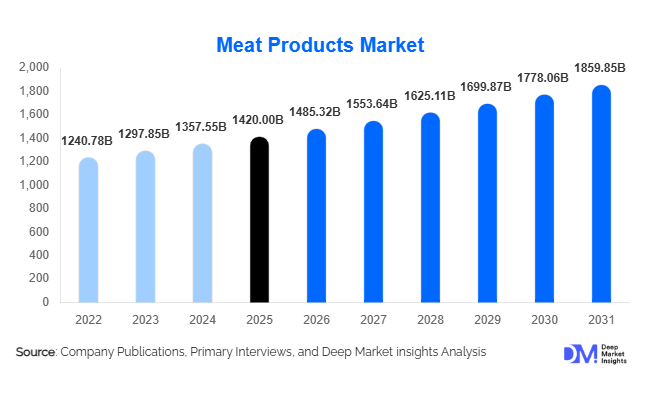

According to Deep Market Insights, the global meat products market size was valued at USD 1,420 billion in 2025 and is projected to grow from USD 1485.32 billion in 2026 to reach USD 1,859.85 billion by 2031, expanding at a CAGR of 4.6% during the forecast period (2026–2031). The meat products market growth is primarily driven by rising global protein consumption, rapid urbanization in emerging economies, expansion of modern retail and cold chain infrastructure, and increasing demand for processed and ready-to-eat meat products. Poultry continues to gain share due to affordability and favorable consumer perception, while processed meat categories are witnessing strong demand in developed economies driven by convenience-oriented lifestyles.

Key Market Insights

- Fresh meat accounts for nearly 48% of total market revenue, supported by high daily consumption in the Asia-Pacific and Africa.

- Poultry leads by animal type with approximately 36% market share, driven by lower production costs and fewer cultural restrictions.

- Asia-Pacific dominates with around 39% of global demand in 2025, led by China and India.

- Foodservice is the fastest-growing end-use segment, expanding at over 6% CAGR due to QSR proliferation.

- Modern retail channels hold about 42% share, reflecting structured supply chains and food safety compliance.

- Top five companies collectively control nearly 23% of the market, indicating moderate fragmentation.

What are the latest trends in the meat products market?

Premiumization and Clean-Label Meat Products

Consumers are increasingly seeking antibiotic-free, hormone-free, grass-fed, and organic-certified meat products. Clean-label positioning, traceability systems, and animal welfare certifications are reshaping purchasing behavior, particularly in North America and Europe. Producers are investing in blockchain-enabled traceability and transparent sourcing models to differentiate their offerings. Premium meat products typically command 10–20% higher margins than conventional alternatives, encouraging companies to expand into value-added and specialty segments.

Technology-Driven Processing and Automation

Automation in slaughterhouses and meat processing facilities is improving yield optimization, hygiene standards, and labor efficiency. AI-powered quality inspection systems, robotic deboning, and smart packaging technologies such as modified atmosphere packaging (MAP) are enhancing shelf life and export viability. Digital supply chain management is reducing waste and improving inventory forecasting, especially in high-volume poultry and pork operations.

What are the key drivers in the meat products market?

Rising Global Protein Consumption

Growing populations and increasing disposable incomes in developing regions are fueling higher per capita meat intake. Emerging economies in Southeast Asia and Africa are experiencing steady increases in poultry and pork demand. Dietary westernization and expanding middle-class households are structurally supporting long-term consumption growth.

Expansion of Quick-Service Restaurants (QSRs)

The global expansion of chains such as McDonald's and KFC has significantly increased demand for standardized beef and poultry supplies. Bulk procurement contracts and vertically integrated supply chains are strengthening industrial-scale processing. The foodservice sector’s growth is particularly strong in Asia-Pacific and Latin America, positively impacting meat processing volumes.

What are the restraints for the global market?

Feed Price Volatility

Fluctuations in corn and soybean prices significantly influence livestock production costs. Feed expenses account for nearly 60–70% of total production costs in poultry and pork farming. Sudden price spikes compress margins and create supply chain instability.

Regulatory and Health Concerns

Increasing regulatory scrutiny on food safety, carbon emissions, and processed meat health impacts presents compliance challenges. Stringent environmental regulations in Europe and rising sustainability pressures globally may moderate long-term growth unless mitigated through technological innovation.

What are the key opportunities in the meat products industry?

Emerging Market Protein Gap

Countries such as China, India, Indonesia, and Vietnam are experiencing rising protein demand. Investments in domestic livestock production and cold chain infrastructure present expansion opportunities for global processors through joint ventures and localized facilities.

Export-Oriented Production Expansion

Brazil and the United States remain dominant exporters of beef and poultry. Expanding processing capacity for halal-certified and region-specific meat products can unlock demand in Middle Eastern and African markets, which are heavily import-dependent.

Product Type Insights

Fresh meat remains the dominant segment, accounting for approximately 48% of the global market share in 2025. The leadership of this segment is primarily driven by high daily household consumption, particularly across Asia-Pacific and parts of Africa, where fresh meat purchases through wet markets and traditional retail remain culturally embedded. In countries such as China and India, consumers prefer freshly slaughtered or minimally processed meat due to perceptions of quality, taste, and safety. Additionally, fresh poultry and pork benefit from shorter supply chains and lower processing costs, enabling competitive pricing. Rising urbanization has also supported the expansion of packaged fresh meat in supermarkets, further strengthening this segment’s global dominance.

Processed meat accounts for nearly 35% of global revenue, supported by growing demand for convenience foods in North America and Europe. Urban lifestyles, rising female workforce participation, and time-constrained consumers are driving sales of sausages, cured meats, deli cuts, and frozen meat products. Food safety compliance and standardized packaging have enhanced consumer trust, while technological innovations such as modified atmosphere packaging (MAP) extend shelf life and enable international trade. Value-added ready-to-eat (RTE) meat products represent a rapidly expanding niche, benefiting from the growth of dual-income households and ready-meal consumption. Snack meat products such as jerky and meat bars are gaining strong traction among younger consumers, fitness-oriented demographics, and on-the-go professionals in North America and Europe, contributing to higher per-unit margins compared to conventional fresh meat.

Animal Type Insights

Poultry leads globally with approximately 36% market share in 2025, making it the most consumed animal protein category worldwide. Its dominance is driven by affordability, shorter production cycles, lower feed conversion ratios, and fewer religious or cultural restrictions compared to pork or beef. Poultry production is also less resource-intensive, enabling scalability in emerging economies. Rising health consciousness has further positioned chicken as a leaner alternative to red meat, particularly in urban markets.

Pork remains dominant in China and several European countries, supported by strong cultural dietary preferences and well-established domestic production systems. Beef consumption is particularly strong in North America and Latin America, where large-scale cattle ranching and export infrastructure support supply. Lamb and specialty meats occupy smaller but premium niches, especially in Middle Eastern markets where halal-certified lamb products command higher margins.

Distribution Channel Insights

Modern retail channels account for around 42% of global meat product sales, making them the leading distribution segment. Growth is driven by increasing consumer preference for hygienically packaged, quality-certified, and traceable meat products. Supermarkets and hypermarkets offer standardized cold chain management and bulk procurement efficiencies, ensuring consistent supply and food safety compliance. Expansion of organized retail networks in Asia-Pacific and Latin America is further strengthening this segment.

Traditional retail and wet markets remain highly relevant in Asia and Africa due to cultural buying habits and proximity to consumers. However, online retail and direct-to-consumer (D2C) platforms are emerging as high-growth channels, particularly in urban centers with advanced cold storage and last-mile logistics. Digital platforms are leveraging subscription models, farm-to-home branding, and premium meat offerings to attract higher-income consumers.

End-Use Insights

Household consumption accounts for approximately 55% of total global demand, maintaining its position as the largest end-use segment. Daily protein intake requirements, population growth, and rising disposable incomes in emerging economies continue to drive steady household purchases. The foodservice segment is the fastest-growing end-use category, expanding at over 6% CAGR. The proliferation of quick-service restaurants (QSRs), casual dining chains, and institutional catering services is significantly increasing demand for standardized beef, poultry, and processed meat products. Industrial food processors represent a substantial share of consumption, particularly for frozen meals, ready snacks, and bakery fillings. Export-driven demand from Brazil and the United States contributes significantly to global trade volumes exceeding 40 million metric tons annually, reinforcing industrial-scale meat processing growth.

| By Product Type | By Animal Type | By Distribution Channel | By End-Use |

|---|---|---|---|

|

|

|

|

Regional Insights

Asia-Pacific

Asia-Pacific leads the global meat products market with approximately 39% share in 2025. The region’s dominance is driven by large population bases, rising middle-class incomes, and increasing urbanization. China alone represents over 20% of global meat consumption, particularly in pork, supported by strong domestic demand and government-backed livestock modernization programs. India is witnessing rapid poultry growth due to affordability and expanding cold chain infrastructure. Japan and South Korea rely heavily on imports to meet domestic consumption, creating stable trade flows. Southeast Asia is the fastest-growing sub-region, expanding at nearly 6–7% CAGR, driven by rising protein consumption and expansion of organized retail and foodservice sectors.

North America

North America accounts for roughly 24% of global revenue, supported by high per capita meat consumption and advanced industrial processing capabilities. The United States remains one of the largest producers and exporters of beef and poultry, benefiting from automation, large-scale feed production, and integrated supply chains. Growth drivers include strong foodservice demand, expansion of value-added processed meat products, and rising exports to Asia and the Middle East. Technological adoption in slaughterhouses and packaging facilities further enhances competitiveness.

Europe

Europe holds approximately 20% market share, led by Germany, France, and Spain. The region is characterized by high processed meat consumption and well-established cold chain networks. Growth is driven by premiumization trends, demand for organic and animal welfare-certified meat, and export opportunities to Asia. However, stringent environmental regulations and health concerns related to processed meat moderate overall growth rates. Investments in sustainable livestock farming and methane-reduction technologies are shaping long-term regional competitiveness.

Latin America

Latin America is largely export-driven, with Brazil serving as a global leader in beef and poultry exports. Abundant feed resources, favorable climate conditions, and competitive production costs support large-scale livestock farming. Domestic consumption is gradually increasing due to urbanization and rising incomes. Expansion of trade agreements and halal-certified meat production strengthens export opportunities to the Middle East and Asia, acting as key regional growth drivers.

Middle East & Africa

The Middle East relies heavily on imports to meet domestic demand due to limited livestock production capacity and water constraints. Halal-certified meat trade is a major growth driver, supported by strong demand from Saudi Arabia, the UAE, and other Gulf countries. In Africa, rising population growth, urbanization, and gradual improvements in cold storage infrastructure are increasing meat consumption levels. Import dependence combined with infrastructure development and retail modernization is expected to steadily boost regional market expansion.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Meat Products Market

- JBS S.A.

- Tyson Foods

- WH Group

- Cargill

- Marfrig

- BRF S.A.

- Hormel Foods

- Danish Crown

- Smithfield Foods

- Perdue Farms

- Charoen Pokphand Foods

- Vion Food Group

- Minerva Foods

- NH Foods

- OSI Group