Mead Beverages Market Size

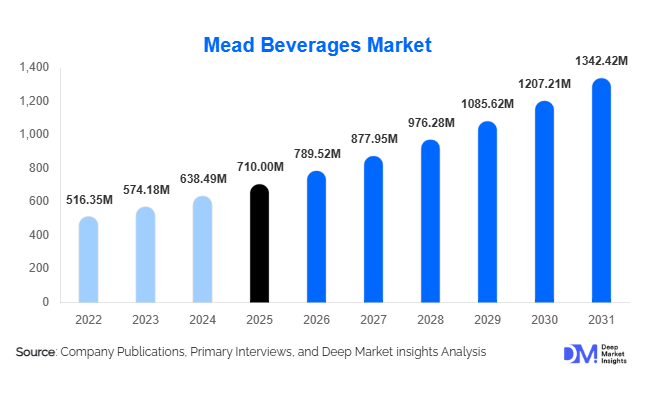

According to Deep Market Insights, the global mead beverages market size was valued at USD 710 million in 2025 and is projected to grow from USD 789.52 million in 2026 to reach USD 1,342.42 million by 2031, expanding at a CAGR of 11.2% during the forecast period (2026–2031). The mead beverages market growth is primarily driven by the rising popularity of craft alcoholic drinks, increasing consumer preference for natural and gluten-free beverages, and the growing influence of premiumization trends across global alcohol consumption patterns.

Key Market Insights

- Mead is transitioning from a niche heritage drink to a mainstream craft beverage, supported by increasing consumer curiosity and experimentation.

- Premium and craft mead segments dominate market revenue, driven by high margins and strong brand storytelling.

- North America leads global consumption, accounting for the largest share due to a strong craft beverage ecosystem.

- Asia-Pacific is the fastest-growing region, fueled by rising disposable incomes and evolving drinking preferences.

- Flavor innovation, including fruit-infused and spiced meads, is expanding consumer appeal globally.

- E-commerce and direct-to-consumer channels are reshaping distribution, especially for small-scale producers.

What are the latest trends in the mead beverages market?

Flavor Innovation and Product Diversification

The mead beverages market is witnessing significant innovation in flavor profiles, with melomel (fruit-infused), metheglin (spiced), and sparkling variants gaining traction. These innovations are helping producers appeal to a broader audience beyond traditional consumers. Fruit-forward meads, in particular, are driving adoption among younger consumers who prefer lighter and more approachable alcoholic beverages. Seasonal and limited-edition flavors are also emerging as a strategy to boost repeat purchases and brand engagement.

Shift Toward Canned and Ready-to-Drink Formats

Packaging innovation is playing a crucial role in expanding the mead market. The introduction of canned mead and ready-to-drink (RTD) formats is improving accessibility and convenience, making mead more suitable for casual and outdoor consumption. This trend is aligning mead with broader RTD alcoholic beverage trends, enabling it to compete with beer, cider, and hard seltzers in social drinking occasions.

What are the key drivers in the mead beverages market?

Rising Demand for Craft and Artisanal Beverages

The global shift toward craft beverages is a primary driver for mead market growth. Consumers are increasingly seeking unique, locally produced, and small-batch alcoholic drinks with authentic stories. Mead fits well within this trend due to its historical roots and customizable production processes, making it highly appealing to premium consumers.

Growing Preference for Natural and Gluten-Free Alcohol

Mead’s natural composition—primarily honey, water, and yeast—positions it as a clean-label and gluten-free alternative to traditional alcoholic beverages. This has significantly expanded its consumer base, particularly among health-conscious individuals and those with dietary restrictions.

What are the restraints for the global market?

High Cost of Production

The cost of honey, the primary raw material, remains significantly higher and more volatile than grains or grapes used in other alcoholic beverages. This leads to higher production costs and retail pricing, limiting mass-market adoption and price competitiveness.

Limited Consumer Awareness in Emerging Markets

Despite its long history, mead remains relatively unknown in many emerging markets. Lack of awareness, combined with limited distribution networks, restricts market penetration in regions such as Asia-Pacific and Latin America, where consumer education is still developing.

What are the key opportunities in the mead beverages industry?

Expansion into Emerging Markets

Emerging economies such as India, China, and Southeast Asian countries present significant growth opportunities. Rising disposable incomes and increasing openness to new alcoholic beverages are driving demand. Localized flavors and culturally relevant branding strategies can further accelerate market penetration in these regions.

Premiumization and Experiential Consumption

Consumers are increasingly willing to pay premium prices for high-quality, artisanal beverages. Mead producers can leverage this trend by offering aged, barrel-fermented, or exotic ingredient-based products. Additionally, experiential offerings such as tasting rooms, brewery tours, and festival participation are enhancing brand engagement and driving direct-to-consumer sales.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 710 Million |

| Market Size in 2026 | USD 789.52 Million |

| Market Size in 2031 | USD 1342.42 Million |

| CAGR | 11.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global mead beverages market is experiencing notable diversification across product types, with melomel (fruit-infused mead) firmly establishing itself as the dominant segment, accounting for approximately 32% of the global market share in 2025. This leadership position is largely attributed to melomel’s broad flavor spectrum, which aligns well with evolving consumer preferences for innovative and approachable alcoholic beverages. By incorporating fruits such as berries, citrus, and tropical varieties, melomel offers a sensory profile that bridges the gap between traditional mead and modern flavored alcoholic drinks. This accessibility plays a critical role in attracting first-time consumers who may otherwise perceive mead as niche or overly traditional. Furthermore, the increasing experimentation by craft producers in blending exotic fruits and botanicals is enhancing product differentiation and driving repeat consumption.Traditional mead continues to maintain a significant presence within the market, particularly among seasoned consumers who value authenticity, heritage, and artisanal production methods. This segment benefits from the growing consumer inclination toward historical and culturally rooted beverages, often associated with premium positioning and storytelling. Meanwhile, metheglin, which incorporates herbs and spices, along with other specialty variants, is witnessing steady growth due to the rising demand for complex and unique flavor profiles. Consumers seeking novelty and premium experiences are increasingly drawn to these offerings, especially within urban and high-income demographics. Additionally, session meads are emerging as one of the fastest-growing categories, driven by their lower alcohol content and enhanced drinkability. These products cater to modern drinking occasions where moderation, socialization, and extended consumption are key factors, thereby expanding the market’s appeal to younger and health-conscious consumers.

Alcohol Content Insights

In terms of alcohol content segmentation, standard alcohol mead, typically ranging between 5% and 12% ABV, dominates the global market with an estimated 54% share. This segment’s leadership is primarily driven by its optimal balance between alcohol strength and drinkability, making it suitable for a wide range of consumption occasions. Standard meads appeal to both casual drinkers and premium consumers, offering versatility that aligns with evolving consumption patterns. The segment also benefits from its compatibility with food pairing and social drinking environments, further reinforcing its widespread acceptance.Low-alcohol meads are gaining significant traction, particularly among health-conscious consumers and those seeking mindful drinking options. The global shift toward wellness-oriented lifestyles has influenced alcohol consumption habits, leading to increased demand for beverages that offer reduced alcohol content without compromising on flavor. This trend is especially prominent among millennials and Gen Z consumers, who prioritize moderation and balanced lifestyles. On the other hand, high-alcohol meads, often exceeding 12% ABV, cater to a niche yet lucrative premium segment. These products are typically positioned as luxury or specialty offerings, appealing to connoisseurs who appreciate bold flavors, higher complexity, and aging potential. The growth of this segment is supported by the increasing popularity of craft and artisanal alcoholic beverages, where quality and uniqueness outweigh volume consumption.

Packaging Insights

Packaging plays a crucial role in shaping consumer perception and purchase decisions within the mead beverages market. Glass bottles remain the dominant packaging format, accounting for approximately 48% of the market share. This dominance is largely driven by the traditional and premium image associated with glass packaging, which aligns with mead’s historical roots and artisanal appeal. Glass bottles are particularly favored in premium and craft segments, where branding, aesthetics, and product integrity are critical factors. Additionally, glass packaging is perceived as environmentally sustainable and capable of preserving the beverage’s quality, further reinforcing its preference among both producers and consumers.However, the market is witnessing a notable shift toward alternative packaging formats, particularly cans, which are emerging as the fastest-growing segment. The increasing popularity of canned mead is driven by its convenience, portability, and suitability for outdoor and casual consumption scenarios such as festivals, picnics, and social gatherings. Cans also offer advantages in terms of lightweight transportation and reduced carbon footprint, aligning with sustainability trends. Furthermore, the rise of ready-to-drink (RTD) alcoholic beverages has contributed to the growing acceptance of cans, especially among younger consumers who prioritize convenience and modern packaging formats. This evolving packaging landscape reflects the industry’s efforts to balance tradition with innovation, catering to diverse consumer preferences.

Distribution Channel Insights

The distribution landscape of the mead beverages market is predominantly led by off-trade channels, which account for approximately 61% of the total market share. This segment includes retail outlets such as specialty liquor stores, supermarkets, and online platforms, which provide consumers with easy access to a wide variety of mead products. The growth of off-trade channels is significantly supported by the expansion of e-commerce and digital retailing, enabling consumers to explore and purchase niche and craft beverages from the comfort of their homes. Online platforms, in particular, play a crucial role in educating consumers, offering detailed product descriptions, reviews, and recommendations that enhance the overall purchasing experience.On-trade channels, including bars, restaurants, and hospitality venues, are also experiencing steady growth as mead gains acceptance within social and experiential drinking environments. The increasing inclusion of mead in curated beverage menus, tasting events, and craft beverage festivals is contributing to its rising visibility and consumer awareness. Additionally, collaborations between mead producers and hospitality establishments are fostering innovation in serving styles and pairings, further enhancing the beverage’s appeal. The growth of on-trade channels is particularly evident in urban areas, where consumers seek unique and premium drinking experiences. This dual-channel expansion underscores the market’s ability to cater to both convenience-driven and experience-oriented consumption patterns.

Price Segment Insights

The price segmentation of the mead beverages market is characterized by a strong dominance of premium and craft products, which collectively account for approximately 46% of the market share. This dominance is driven by a growing consumer willingness to pay for quality, authenticity, and distinctive flavor profiles. Premium meads often emphasize artisanal production methods, high-quality ingredients, and innovative formulations, which resonate with consumers seeking unique and memorable drinking experiences. The increasing popularity of craft beverages across the broader alcoholic drinks industry has further reinforced the demand for premium mead offerings.Mid-range products serve as a bridge between premium and economy segments, catering to mainstream consumers who seek a balance between affordability and quality. These products are essential for expanding the market’s reach and attracting new consumers who may eventually transition to premium offerings. Meanwhile, the economy segment remains relatively small, primarily due to the inherently high production costs associated with mead, including the use of honey as a key ingredient. Despite its limited share, the economy segment plays a role in introducing price-sensitive consumers to the category, particularly in emerging markets where affordability is a key consideration. Overall, the pricing dynamics of the market reflect a strong emphasis on value, quality, and consumer experience.

Explore more data points, trends and opportunities Download Free Sample Report

Mead Beverages Market Segmentations

By Product Type

- Traditional Mead

- Melomel

- Metheglin

- Cyser

- Pyment

- Braggot

- Session

- Low-Alcohol Mead

By Alcohol Content

- Low Alcohol

- Standard Alcohol

- High Alcohol

By Packaging Type

- Glass Bottles

- Cans

- Kegs/Draught

- Premium/Decorative Packaging

By Distribution Channel

- On-Trade

- Off-Trade

By Price Segment

- Economy Mead

- Mid-Range Mead

- Premium & Craft Mead

Regional Insights

North America

North America leads the global mead beverages market, accounting for approximately 38% of the total market share in 2025. The United States is the primary driver of regional demand, contributing over 80% of consumption. This dominance is underpinned by a well-established craft beverage culture, which has fostered innovation and experimentation within the mead segment. The proliferation of craft breweries and meaderies has significantly enhanced product availability and consumer awareness, while also encouraging the development of diverse and high-quality offerings. Additionally, the region benefits from a strong distribution network, including both off-trade and on-trade channels, which ensures widespread accessibility.Another key growth driver in North America is the increasing consumer preference for locally produced and artisanal beverages. This trend aligns with broader movements toward sustainability, authenticity, and community support. The rising popularity of experiential consumption, including tasting events and brewery tours, further contributes to market growth. In Canada, the market is witnessing steady expansion, supported by a growing interest in craft beverages and premium consumption trends. Favorable regulatory frameworks and the availability of high-quality raw materials also play a crucial role in supporting regional growth. Overall, North America’s leadership position is reinforced by its mature market ecosystem, strong consumer base, and continuous innovation.

Europe

Europe represents a significant portion of the global mead beverages market, accounting for approximately 34% of the total share. The region’s growth is deeply rooted in its historical association with mead, particularly in countries such as Poland, the United Kingdom, and Germany. Poland remains a traditional stronghold for mead production, with a rich heritage that continues to influence contemporary consumption patterns. The United Kingdom, on the other hand, is at the forefront of innovation, with a vibrant craft mead industry that emphasizes creativity and product differentiation.One of the primary drivers of growth in Europe is the strong cultural and historical connection to mead, which fosters consumer familiarity and acceptance. Additionally, the region benefits from a well-developed craft beverage industry, which encourages experimentation and the introduction of new flavors and formats. The increasing popularity of premium and artisanal products is also contributing to market expansion, as consumers seek high-quality and authentic experiences. Furthermore, supportive regulatory frameworks and the presence of established distribution networks facilitate market growth. The growing trend of food and beverage tourism in Europe, where traditional and locally produced beverages are a key attraction, further enhances the visibility and demand for mead.

Asia-Pacific

The Asia-Pacific region is emerging as the fastest-growing market for mead beverages, with an expected CAGR of 13–15% over the forecast period. Countries such as China, India, Japan, and Australia are driving this growth, supported by rising disposable incomes and increasing urbanization. The expanding middle class in these countries is increasingly seeking premium and imported alcoholic beverages, creating significant opportunities for mead producers. Additionally, the growing influence of Western drinking culture is contributing to the adoption of mead, particularly among younger consumers.India, in particular, is emerging as a high-potential market, driven by the rise of local meaderies and increasing consumer awareness. The country’s large and youthful population, coupled with a growing preference for craft and artisanal products, is creating a favorable environment for market expansion. In China, the demand for premium alcoholic beverages is on the rise, supported by increasing affluence and changing consumption patterns. Japan and Australia also present strong growth prospects, driven by their established craft beverage industries and high consumer spending on premium products. The region’s growth is further supported by the expansion of e-commerce platforms, which enhance product accessibility and consumer engagement.

Latin America

Latin America accounts for approximately 8% of the global mead beverages market, with Brazil and Mexico leading regional growth. The market in this region is gradually gaining traction, driven by increasing exposure to international craft beverage trends and the rising popularity of premium alcoholic drinks. The growing middle-class population and improving economic conditions are also contributing to increased consumer spending on non-traditional beverages.Key growth drivers in Latin America include the expansion of urban centers, which serve as hubs for innovation and consumption, as well as the increasing presence of craft breweries and specialty beverage producers. Additionally, the region’s favorable climate for honey production provides a strong foundation for local mead production. Cultural openness to new and diverse flavors further supports market growth, as consumers become more willing to experiment with unique alcoholic beverages. While the market remains relatively small compared to other regions, its growth potential is significant, particularly as awareness and accessibility continue to improve.

Middle East & Africa

The Middle East & Africa region holds approximately 6% of the global market share, with key markets including South Africa and the United Arab Emirates. Growth in this region is relatively moderate, primarily due to regulatory constraints and cultural factors that influence alcohol consumption. However, the market is supported by the expansion of the premium hospitality sector, particularly in tourist destinations where demand for unique and high-quality beverages is strong.In South Africa, the growing craft beverage industry is contributing to the development of the mead market, supported by local production and increasing consumer interest. The United Arab Emirates, with its thriving tourism and hospitality sectors, presents opportunities for premium mead offerings in high-end establishments. Additionally, the region’s increasing focus on diversification of its food and beverage industry is creating new avenues for growth. The presence of expatriate populations and international tourists further supports demand, as these groups are more familiar with and receptive to mead. Despite existing challenges, the region offers niche opportunities for premium and specialty products, particularly within the hospitality and tourism sectors.

Key Players in the Mead Beverages Market

- Dansk Mjød

- Redstone Meadery

- B. Nektar Meadery

- Schramm’s Mead

- Superstition Meadery

- Moonlight Meadery

- Brothers Drake Meadery

- Charm City Meadworks

- Viking Alchemist Meadery

- Nidhoggr Mead Co.

- BeeHaven Mead & Cider

- Gosnells of London

- Batch Mead

- Tallgrass Mead

- Apis Meadery