Marine Collagen Market Size

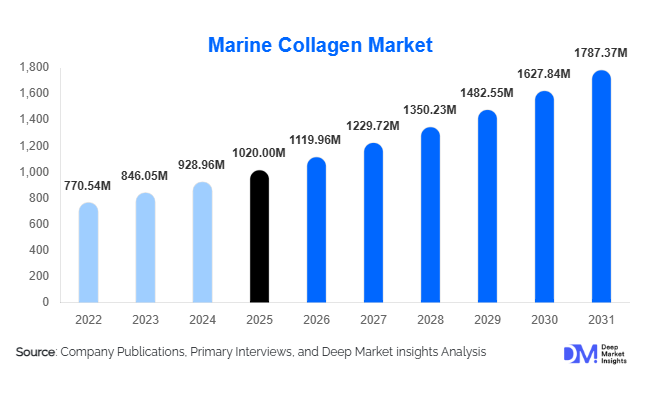

According to Deep Market Insights, the global marine collagen market size was valued at USD 1,020 million in 2025 and is projected to grow from USD 1,119.96 million in 2026 to reach USD 1,787.37 million by 2031, expanding at a CAGR of 9.8% during the forecast period (2026–2031). The marine collagen market growth is primarily driven by rising demand for bioavailable protein supplements, expanding nutricosmetics consumption, and increasing adoption of clean-label and pescatarian-friendly ingredients across food, beauty, and healthcare industries.

Key Market Insights

- Marine collagen peptides dominate product demand, accounting for over 70% of total market revenue due to superior bioavailability and solubility.

- Asia-Pacific leads global production and consumption, supported by strong seafood processing industries and high collagen beverage consumption in Japan and China.

- Nutraceuticals remain the largest application segment, contributing nearly 46% of global revenue in 2025.

- Fish skin-derived collagen holds the highest source share, driven by higher yield and purity compared to scales and bones.

- North America represents the largest consumption hub, led by U.S. dietary supplement demand.

- Sustainability and circular economy positioning are increasingly shaping procurement decisions and premium pricing strategies.

What are the latest trends in the marine collagen market?

Rise of Ingestible Beauty and Nutricosmetics

Marine collagen is increasingly positioned as a “beauty-from-within” ingredient, particularly in powders, capsules, and ready-to-drink (RTD) beauty beverages. Consumers are shifting from topical skincare to ingestible solutions targeting skin elasticity, hydration, and anti-aging benefits. This has accelerated the growth of collagen-infused drinks in Japan, South Korea, the U.S., and Germany. Brands are investing in clinically backed claims, vitamin C–enriched blends, and multi-collagen formulations to enhance differentiation in a competitive nutraceutical environment.

Premiumization and Sustainable Sourcing

Manufacturers are leveraging marine collagen’s origin from fish processing by-products to promote sustainability and circular economy narratives. Certifications related to marine stewardship, traceable sourcing, and low-carbon extraction processes are becoming key competitive differentiators. European and Japanese buyers increasingly demand documented sustainable supply chains, enabling premium pricing of 15–25% above conventional collagen products. Sustainable branding is strengthening marine collagen’s positioning over bovine and porcine alternatives.

What are the key drivers in the marine collagen market?

Growing Health & Wellness Industry

The global health and wellness industry, valued at over USD 5 trillion, continues to expand, directly influencing marine collagen demand. Dietary supplements, growing at double-digit rates globally, are the primary revenue contributor. Increasing awareness regarding joint health, sports recovery, and protein supplementation is reinforcing collagen’s mainstream adoption. Aging populations in Japan, Europe, and North America are further accelerating demand for bone and skin health solutions.

Higher Bioavailability Compared to Bovine Collagen

Marine collagen peptides typically have lower molecular weights (2–5 kDa), enhancing absorption and faster bioactivity. This scientific advantage has driven substitution from bovine collagen in premium supplement categories. Additionally, marine collagen avoids BSE concerns and is inherently halal-compliant, strengthening acceptance across Asia and the Middle East.

What are the restraints for the global market?

High Production and Raw Material Costs

Marine collagen remains 20–40% more expensive than bovine collagen due to limited raw material supply and specialized enzymatic hydrolysis processes. Seasonal fish supply fluctuations can affect pricing stability, impacting manufacturer margins.

Supply Chain Concentration Risks

Production is concentrated in Asia-Pacific, particularly China, Japan, and Vietnam. Dependence on seafood processing industries exposes the market to raw material volatility, regulatory changes, and export restrictions, potentially constraining growth.

What are the key opportunities in the marine collagen industry?

Biomedical and Regenerative Medicine Applications

Marine collagen’s biocompatibility and low immunogenicity make it suitable for wound dressings, tissue engineering scaffolds, and regenerative implants. With increasing healthcare investments globally, clinical-grade marine collagen represents a high-margin opportunity for manufacturers investing in pharmaceutical-grade production facilities.

Collagen-Infused Functional Beverages

The rapid expansion of functional RTD beverages presents a major opportunity. Marine collagen’s neutral taste and solubility allow integration into protein waters, flavored drinks, and fortified juices. Younger consumers favor convenient formats, making RTD beverages one of the fastest-growing product categories within the collagen ecosystem.

Product Type Insights

Marine collagen peptides continue to dominate the market, accounting for approximately 72% of the 2025 market share. This dominance is driven by their high bioavailability, low molecular weight, and extensive use in dietary supplements and functional foods, where digestibility and rapid absorption are key factors. Marine gelatin represents around 20% of the market, primarily utilized in confectionery, pharmaceutical capsules, and gel-based formulations, benefiting from its gelling and stabilizing properties. Native (undenatured) marine collagen, while a smaller segment, is experiencing robust growth due to its intact protein structures, which are preferred in biomedical applications, wound healing products, and certain high-end cosmetic formulations. Overall, peptide formats lead due to their versatile formulation compatibility, ease of incorporation into powders, beverages, and capsules, and growing consumer preference for fast-acting health and beauty solutions.

Application Insights

Nutraceuticals and dietary supplements remain the largest application segment, contributing nearly 46% of total market revenue in 2025. This is largely driven by increasing consumer awareness of joint health, skin aging, and overall wellness, combined with strong adoption in protein powders, capsules, and functional beverages. Cosmetics and personal care applications account for roughly 22%, supported by the growing “beauty-from-within” trend and collagen-infused skin care products. Food and beverage fortification holds approximately 18% of the market, with fortified beverages, protein bars, and functional snacks driving growth. Pharmaceutical and biomedical applications represent about 9%, reflecting rising use in tissue engineering, wound care, and regenerative medicine. Animal nutrition and pet supplements make up the remaining share, growing steadily due to demand for joint health and mobility-enhancing products for pets. The nutraceutical segment’s growth continues to be the primary driver for overall marine collagen market expansion, supported by peptide-dominant product formulations.

Distribution Channel Insights

Direct B2B industrial supply dominates with nearly 58% of total revenue, as manufacturers and formulators procure bulk marine collagen for supplements, functional foods, and pharmaceutical applications. Contract manufacturing and private label account for roughly 25%, reflecting the trend of outsourcing production by emerging supplement and cosmetic brands seeking to reduce capital expenditure. Retail and e-commerce channels represent about 17%, driven by branded collagen powders, capsules, and RTD beverages sold through platforms in the U.S., China, Japan, and Europe. The rapid growth of online channels is fueled by younger consumers’ preference for convenient, direct-to-consumer purchase options and increased digital marketing initiatives from premium marine collagen brands.

End-Use Industry Insights

The health and wellness industry accounts for approximately 44% of marine collagen demand, primarily due to dietary supplements experiencing double-digit growth globally. The beauty and personal care industry, valued at over USD 500 billion, continues integrating marine collagen into ingestible products targeting skin hydration, elasticity, and anti-aging benefits. Pharmaceutical and medical device applications are emerging high-growth areas, driven by demand for bioresorbable materials, wound healing scaffolds, and regenerative medicine products. Export-driven demand is significant in markets such as Japan, Germany, and the U.S., where premium marine collagen is imported for formulation into high-value functional foods, nutraceuticals, and cosmeceuticals.

| By Product Type | By Application | By Distribution Channel | By End-Use Industry |

|---|---|---|---|

|

|

|

|

Regional Insights

Asia-Pacific

Asia-Pacific holds approximately 38% of the global marine collagen market share in 2025. Japan alone contributes nearly 14% of global revenue, fueled by strong cultural acceptance of collagen beverages, functional foods, and anti-aging supplements. China is the fastest-growing country in the region, expanding at over 12% CAGR, supported by domestic production leadership, growing middle-class affluence, and rising export demand for collagen peptides. South Korea also represents a high-growth market, driven by the nutricosmetics trend and increased online sales of beauty-focused collagen products. The primary drivers for the region include rising disposable incomes, the popularity of beauty and wellness supplements, and government support for the marine biotechnology and functional food industries.

North America

North America accounts for approximately 29% of the global market, with the U.S. representing nearly 24% of worldwide demand. Growth is driven by high consumer awareness of health, wellness, and sports nutrition, strong adoption of clinically backed supplement formulations, and the expansion of e-commerce and retail platforms for direct-to-consumer sales. The region emphasizes premium marine collagen peptides in powders, capsules, and beverages, supported by advanced clinical validation and regulatory compliance. Key drivers include rising aging populations seeking joint and skin health solutions, widespread digital adoption for supplement purchasing, and increasing investment in functional nutrition by leading brands.

Europe

Europe holds around 22% of the global marine collagen market share, led by Germany, France, and the U.K. Growth is supported by rising demand for clean-label products, sustainability certifications, and EFSA-approved functional foods. The nutraceutical and cosmeceutical sectors in Europe favor marine collagen due to its high bioavailability and premium positioning. Drivers of regional growth include strong consumer preference for anti-aging and health supplements, government initiatives promoting marine-derived nutraceuticals, and a highly regulated market that ensures product efficacy and safety, reinforcing consumer trust in marine collagen products.

Latin America

Latin America represents roughly 6% of global demand, with Brazil as the leading market. Rising middle-class incomes, urbanization, and growing health-conscious behavior are driving moderate growth in dietary supplements and beauty-focused marine collagen products. The primary growth drivers are increasing consumer education on wellness, adoption of functional foods, and expanding e-commerce platforms targeting younger demographics seeking premium and convenient collagen products.

Middle East & Africa

MEA accounts for about 5% of global revenue. Growth is driven by rising health awareness, halal-compliant product demand, and increasing disposable incomes in the UAE, Saudi Arabia, and Qatar. Premium supplement adoption is on the rise due to urbanization and wellness-oriented lifestyles. Regional drivers include religious compliance favoring marine over bovine collagen, strong retail and e-commerce expansion in GCC countries, and rising investment in health and wellness infrastructure supporting nutraceutical and beauty product adoption.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Marine Collagen Market

- Rousselot

- Nitta Gelatin

- Weishardt

- GELITA AG

- Vital Proteins

- Amicogen

- Darling Ingredients

- Tessenderlo Group

- Titan Biotech

- Hangzhou Nutrition Biotechnology

- Seagarden

- Connoils

- Juncà Gelatines

- Norland Products

- Lapi Gelatine