Maltodextrin Market Size

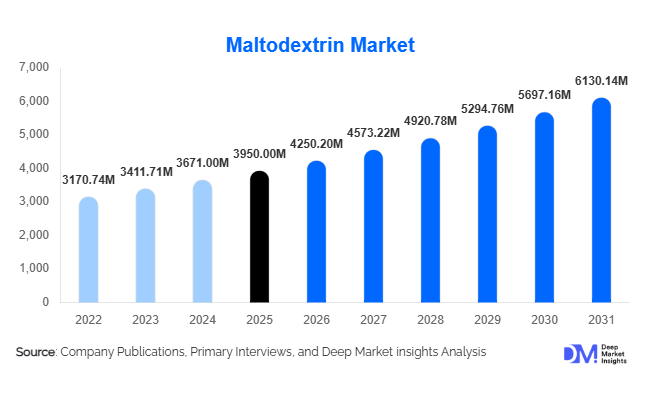

According to Deep Market Insights, the global maltodextrin market size was valued at USD 3,950 million in 2025 and is projected to grow from USD 4,250.20 million in 2026 to reach USD 6,130.14 million by 2031, expanding at a CAGR of 7.6% during the forecast period (2026–2031). The maltodextrin market growth is primarily driven by rising demand from the processed food industry, increasing adoption in sports nutrition products, and expanding pharmaceutical applications. Its multifunctional properties such as thickening, stabilizing, and bulking, along with cost-effectiveness and neutral taste, make it a widely preferred ingredient across industries.

Key Market Insights

- Food & beverages dominate the market, accounting for over 65% of global demand due to increasing consumption of processed and convenience foods.

- Asia-Pacific leads global production and consumption, supported by abundant raw material availability and expanding food processing industries.

- Corn-based maltodextrin remains the primary segment, contributing nearly 55% of the total market share.

- Sports nutrition and nutraceutical applications are the fastest growing, driven by rising health awareness and fitness trends.

- Powder form dominates, capturing around 70% share due to ease of storage and longer shelf life.

- Technological advancements in enzymatic processing are enabling customized maltodextrin solutions for specialized applications.

What are the latest trends in the maltodextrin market?

Shift Toward Clean-Label and Plant-Based Ingredients

The demand for clean-label ingredients is significantly influencing the maltodextrin market. Consumers are increasingly seeking transparency and natural sourcing, prompting manufacturers to develop maltodextrin derived from non-GMO and plant-based sources such as tapioca and rice. This trend is particularly strong in North America and Europe, where regulatory frameworks and consumer awareness around food ingredients are more stringent. Companies are investing in organic certifications and traceability systems to enhance product credibility. Additionally, clean-label maltodextrin is being incorporated into premium food and beverage products, enabling manufacturers to command higher margins while addressing evolving consumer preferences.

Expansion of Functional Foods and Sports Nutrition

The growing popularity of functional foods and sports nutrition products is driving demand for maltodextrin as a rapid energy source. It is widely used in energy drinks, protein powders, and endurance supplements due to its quick digestibility and ability to enhance performance. This trend is particularly pronounced in emerging markets such as India, China, and Brazil, where fitness culture is rapidly expanding. Manufacturers are increasingly developing specialized formulations with targeted dextrose equivalent (DE) levels to cater to specific performance and dietary requirements, further boosting innovation in this segment.

What are the key drivers in the maltodextrin market?

Growth of Processed and Convenience Food Industry

The rapid expansion of the global processed food sector is a key driver for the maltodextrin market. Urbanization, busy lifestyles, and increasing disposable incomes have led to higher consumption of ready-to-eat and packaged foods. Maltodextrin plays a critical role in enhancing texture, stability, and shelf life in these products, making it indispensable for food manufacturers. The steady growth of the global food processing industry continues to provide a strong demand base for maltodextrin.

Rising Demand in Pharmaceutical Applications

Maltodextrin is widely used as an excipient in pharmaceutical formulations due to its binding and stabilizing properties. With global healthcare spending on the rise and increasing production of generic drugs, the demand for maltodextrin in the pharmaceutical industry is growing steadily. Its compatibility with various active pharmaceutical ingredients makes it a preferred choice for manufacturers.

Increasing Adoption in Nutraceuticals

The expanding nutraceutical sector, driven by health-conscious consumers, is further boosting demand. Maltodextrin is used as a carrier and energy source in dietary supplements, particularly in sports and wellness products. The global shift toward preventive healthcare and fitness is accelerating growth in this segment.

What are the restraints for the global market?

Health Concerns Related to High Glycemic Index

Maltodextrin has a high glycemic index, which can lead to rapid spikes in blood sugar levels. This has raised concerns among health-conscious consumers and individuals with diabetes, potentially limiting its use in certain food applications. Manufacturers are increasingly exploring low-GI alternatives and reformulating products to address these concerns.

Volatility in Raw Material Prices

The market is highly dependent on raw materials such as corn, wheat, and tapioca. Fluctuations in agricultural output due to climate change, geopolitical tensions, and supply chain disruptions can lead to price volatility. This directly impacts production costs and profit margins, posing a challenge for manufacturers.

What are the key opportunities in the maltodextrin industry?

Growth in Emerging Markets

Emerging economies such as India, China, and Southeast Asian countries present significant growth opportunities due to rising urbanization and expanding food processing industries. Government initiatives supporting industrial development and food manufacturing are further enhancing market potential in these regions.

Technological Advancements in Processing

Advancements in enzymatic hydrolysis and processing technologies are enabling the production of customized maltodextrin with specific functional properties. This allows manufacturers to cater to niche applications in pharmaceuticals, infant nutrition, and specialty foods, opening new revenue streams.

Expansion in Sports Nutrition and Functional Beverages

The rapid growth of the global sports nutrition market offers substantial opportunities for maltodextrin manufacturers. Increasing consumer focus on fitness and performance is driving demand for energy-boosting ingredients, particularly in emerging markets where awareness is growing rapidly.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3950.00 Million |

| Market Size in 2026 | USD 4250.20 Million |

| Market Size in 2031 | USD 6130.14 Million |

| CAGR | 7.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Source Insights

The source of raw material plays a critical role in determining the cost structure, functional properties, and overall market positioning of maltodextrin products. Among all sources, corn-based maltodextrin continues to dominate the global market, accounting for approximately 55% of the total share in 2025. This dominance is largely attributed to the extensive availability of corn across major producing regions, particularly in North America and Asia-Pacific, combined with well-established processing infrastructure. Corn offers a highly efficient conversion rate into starch, making it the most cost-effective raw material for large-scale production. Additionally, the global supply chain for corn is highly mature, enabling manufacturers to maintain consistent production volumes and stable pricing, which further strengthens its market leadership.Rice-based maltodextrin is also emerging as a niche but rapidly expanding segment, particularly in infant nutrition, clinical nutrition, and specialized dietary products. Its hypoallergenic properties and easy digestibility make it suitable for sensitive consumer groups, including infants and elderly populations. The growing demand for allergen-free and organic ingredients is expected to further support the adoption of rice-based variants. Overall, while corn remains the dominant source due to its economic advantages, the market is gradually shifting toward diversification, driven by evolving consumer preferences, regulatory requirements, and the rising importance of clean-label and specialty ingredients.

Dextrose Equivalent (DE) Insights

Dextrose Equivalent (DE) is a key parameter that determines the sweetness, solubility, and functional characteristics of maltodextrin, making it a critical factor in product selection across industries. Medium DE maltodextrin, typically ranging between 11 and 20, holds the largest market share of approximately 48% in 2025. This segment’s dominance is driven by its balanced functional profile, offering moderate sweetness while maintaining excellent bulking, thickening, and stabilizing properties. These characteristics make medium DE maltodextrin highly versatile, enabling its widespread use across food, beverage, pharmaceutical, and nutraceutical applications.Low DE maltodextrin, typically below 10, is primarily used in applications requiring thickening and bulking without adding significant sweetness. It is commonly utilized in sauces, soups, and bakery products, where structural integrity and viscosity are essential. On the other hand, high DE maltodextrin, with values above 20, is favored in applications requiring higher sweetness and rapid solubility, such as confectionery products, energy drinks, and certain pharmaceutical formulations. Despite their specific applications, both low and high DE segments remain comparatively smaller due to their limited versatility.The continued dominance of medium DE maltodextrin is expected to persist, supported by its adaptability across diverse applications and its ability to meet evolving consumer demands for taste, texture, and functionality. As product innovation continues across industries, manufacturers are likely to further leverage medium DE variants to achieve optimal formulation performance.

Form Insights

The form in which maltodextrin is available significantly influences its usability, storage, transportation, and application efficiency. Powdered maltodextrin dominates the market, accounting for nearly 70% of the total share. This strong dominance is primarily driven by its superior handling convenience, extended shelf life, and ease of incorporation into dry formulations. Powder form is particularly advantageous for manufacturers involved in large-scale production of bakery mixes, instant beverages, powdered soups, and nutritional supplements, where precise dosing and uniform blending are essential.Another key factor supporting the dominance of powdered maltodextrin is its cost-effectiveness in logistics and storage. Unlike liquid forms, powders require less specialized storage conditions and are less susceptible to microbial contamination, making them more suitable for global trade and long-term storage. Additionally, advancements in spray-drying technologies have enhanced the quality and consistency of powdered maltodextrin, further strengthening its market position.Liquid maltodextrin, although accounting for a smaller share of the market, plays a crucial role in specific industrial and beverage applications. Its primary advantage lies in its rapid solubility and ease of integration into liquid formulations, eliminating the need for additional dissolution steps. This makes it particularly suitable for ready-to-drink beverages, syrups, and certain pharmaceutical applications where consistency and processing efficiency are critical. However, challenges related to storage, transportation, and shorter shelf life limit its widespread adoption compared to powdered forms.Overall, the powdered segment is expected to maintain its dominance due to its versatility, cost efficiency, and compatibility with a wide range of applications. Meanwhile, liquid maltodextrin will continue to serve niche markets where its specific functional advantages are required.

Application Insights

The application landscape of maltodextrin is diverse, with the food and beverage segment emerging as the dominant contributor, accounting for over 65% of the global market share. This dominance is driven by the extensive use of maltodextrin as a multifunctional ingredient that enhances texture, improves shelf life, and acts as a bulking agent in a wide range of products. In bakery and confectionery applications, it helps maintain moisture and improve product consistency, while in dairy and beverages, it enhances mouthfeel and stability.The growing demand for processed and convenience foods, particularly in urban areas, is a major driver for this segment. As consumer lifestyles become increasingly fast-paced, the demand for ready-to-eat and easy-to-prepare food products continues to rise, directly boosting the consumption of maltodextrin. Additionally, the increasing popularity of functional foods and fortified beverages has further expanded its application scope.The pharmaceutical sector represents another important application area, experiencing steady growth due to the expanding global healthcare industry. Maltodextrin is widely used as an excipient in drug formulations, where it serves as a binder, filler, and stabilizer. Its compatibility with active pharmaceutical ingredients and its ability to improve drug delivery efficiency make it a valuable component in pharmaceutical manufacturing. The rising prevalence of chronic diseases and increasing investments in healthcare infrastructure, particularly in emerging economies, are expected to further drive demand in this segment.In the personal care and cosmetics industry, maltodextrin is gaining traction as a stabilizing and texturizing agent. Although currently a niche segment, its use in formulations such as creams, lotions, and powders is increasing, driven by the growing demand for natural and multifunctional ingredients. Overall, the food and beverage segment will continue to lead, supported by strong consumer demand and ongoing product innovation.

Distribution Channel Insights

The distribution landscape of the maltodextrin market is characterized by the dominance of direct business-to-business (B2B) sales, which account for approximately 60% of the total market. Large-scale manufacturers prefer direct procurement from producers to ensure consistent supply, maintain quality standards, and achieve cost efficiencies. Direct sourcing also allows companies to establish long-term contracts, reducing supply chain uncertainties and enabling better price negotiations.Distributors and wholesalers play a vital role in bridging the gap between manufacturers and small to medium-sized enterprises. These intermediaries provide flexibility in order quantities and offer a diverse range of products, making them essential for businesses that do not have the capacity for bulk procurement. Their presence is particularly significant in emerging markets, where fragmented industrial structures necessitate efficient distribution networks.Online distribution channels are gradually gaining traction, driven by the digitalization of procurement processes and the growing popularity of e-commerce platforms. While currently representing a smaller share, online channels offer convenience, transparency, and access to a wider range of specialty products. This trend is expected to accelerate as more businesses adopt digital solutions for supply chain management.The continued dominance of direct B2B sales is expected, supported by the need for reliability and cost efficiency. However, the role of distributors and online platforms will expand, particularly in catering to evolving market dynamics and smaller industry players.

End-Use Industry Insights

The food processing industry remains the largest end-use segment, contributing nearly 58% of the global maltodextrin market. This dominance is driven by the ingredient’s widespread use in enhancing texture, stability, and shelf life across a variety of food products. The rapid expansion of the global food processing sector, fueled by urbanization and changing dietary habits, continues to drive demand for maltodextrin.Nutraceuticals and sports nutrition represent the fastest-growing end-use segments, driven by increasing health awareness and the rising popularity of fitness-oriented lifestyles. Maltodextrin is widely used in energy drinks, protein powders, and dietary supplements due to its ability to provide quick energy and improve product consistency. The growing focus on preventive healthcare and wellness is expected to further accelerate growth in this segment.The pharmaceutical industry is also expanding its use of maltodextrin, particularly in emerging markets where healthcare infrastructure is rapidly developing. Its role as a versatile excipient makes it indispensable in modern drug formulations. As global healthcare demand continues to rise, the pharmaceutical segment is expected to witness sustained growth.

Explore more data points, trends and opportunities Download Free Sample Report

Maltodextrin Market Segmentations

By Source

- Corn-Based Maltodextrin

- Wheat-Based Maltodextrin

- Potato-Based Maltodextrin

- Tapioca-Based Maltodextrin

- Rice-Based Maltodextrin

By Form

- Powder Maltodextrin

- Liquid/Syrup Maltodextrin

By Application

- Food & Beverages

- Pharmaceuticals

- Personal Care & Cosmetics

- Industrial Applications

By Functionality

- Bulking Agents

- Thickening Agents

- Stabilizers

- Emulsifiers

- Film Formers

- Sweeteners

By Distribution Channel

- Direct B2B Sales

- Distributors & Wholesalers

- Online Channels

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global maltodextrin market, accounting for approximately 38% of the total share in 2025. The region’s leadership is primarily driven by large-scale production capabilities, abundant raw material availability, and rapidly expanding end-use industries. China plays a central role as the largest producer, supported by its extensive corn processing industry and well-established manufacturing infrastructure. The country’s ability to produce maltodextrin at competitive costs has positioned it as a key exporter in the global market.India is emerging as a significant growth engine within the region, fueled by the rapid expansion of its food processing industry and increasing consumer demand for packaged and convenience foods. Government initiatives aimed at promoting industrial development and food processing are further supporting market growth. Additionally, rising urbanization, increasing disposable incomes, and changing dietary preferences are driving demand for processed and functional foods, thereby boosting maltodextrin consumption.Southeast Asian countries are also contributing to regional growth, supported by the availability of alternative starch sources such as tapioca. The growing focus on clean-label and natural ingredients is encouraging the adoption of tapioca-based maltodextrin in these markets. Overall, strong industrial growth, favorable government policies, and increasing consumer demand make Asia-Pacific the most dynamic and fastest-growing region.

North America

North America accounts for around 28% of the global maltodextrin market, with the United States being the largest contributor. The region benefits from abundant availability of corn, advanced processing technologies, and a highly developed food and pharmaceutical industry. The presence of major industry players and strong research and development capabilities further support market growth.The increasing demand for processed and convenience foods, along with the growing popularity of functional and fortified products, is driving the consumption of maltodextrin in the region. Additionally, the expanding pharmaceutical sector, supported by significant investments in healthcare and drug development, is contributing to steady demand. The trend toward clean-label and non-GMO products is also influencing product innovation, encouraging manufacturers to explore alternative starch sources.Overall, North America’s mature market structure, combined with continuous innovation and strong end-use demand, ensures stable and sustained growth in the region.

Europe

Europe holds approximately 22% of the global maltodextrin market, driven by strong demand from countries such as Germany, France, and the United Kingdom. The region is characterized by a high emphasis on product quality, safety, and sustainability, which significantly influences market dynamics. Strict regulatory standards and increasing consumer awareness are encouraging the adoption of clean-label and organic ingredients.The growing demand for alternative starch sources, such as wheat and tapioca, is a notable trend in the European market. Manufacturers are focusing on developing innovative products that align with consumer preferences for natural and minimally processed ingredients. Additionally, the region’s well-established food and beverage industry, combined with a strong pharmaceutical sector, supports consistent demand for maltodextrin.Innovation remains a key growth driver in Europe, with companies investing in research and development to enhance product functionality and meet evolving consumer expectations. This focus on quality and innovation is expected to sustain market growth in the region.

Latin America

Latin America contributes around 7% of the global maltodextrin market, with Brazil and Mexico leading regional demand. The region benefits from strong agricultural output, particularly in corn and cassava production, which supports local manufacturing capabilities. The expanding food and beverage industry, driven by increasing urbanization and changing consumer lifestyles, is a key growth driver.The growing export of processed foods from the region is also contributing to increased demand for maltodextrin, as manufacturers seek to enhance product quality and shelf life. Additionally, improving economic conditions and rising disposable incomes are supporting the consumption of packaged and convenience foods. While the market is relatively smaller compared to other regions, it offers significant growth potential due to its evolving industrial landscape.

Middle East & Africa

The Middle East & Africa region accounts for approximately 5% of the global maltodextrin market. Growth in this region is primarily driven by increasing urbanization, rising population, and a growing reliance on imported food products. Countries such as the United Arab Emirates and South Africa are key markets, supported by expanding food processing and retail sectors.The increasing demand for packaged and convenience foods, coupled with the development of modern retail infrastructure, is driving maltodextrin consumption. Additionally, the gradual expansion of the pharmaceutical industry and improving healthcare access are contributing to market growth. Although the region currently represents a smaller share, ongoing economic development and infrastructure investments are expected to create new growth opportunities in the coming years.

Key Players in the Maltodextrin Market

- Cargill Inc.

- Archer Daniels Midland Company (ADM)

- Ingredion Incorporated

- Tate & Lyle PLC

- Roquette Frères

- Tereos Group

- Grain Processing Corporation

- AGRANA Beteiligungs-AG

- Avebe U.A.

- Zhucheng Dongxiao Biotechnology

- Shandong Tianli Pharmaceutical

- Xiwang Group

- Gulshan Polyols Ltd.

- Sayaji Industries Ltd.

- Global Sweeteners Holdings Ltd.