Malt Market Size

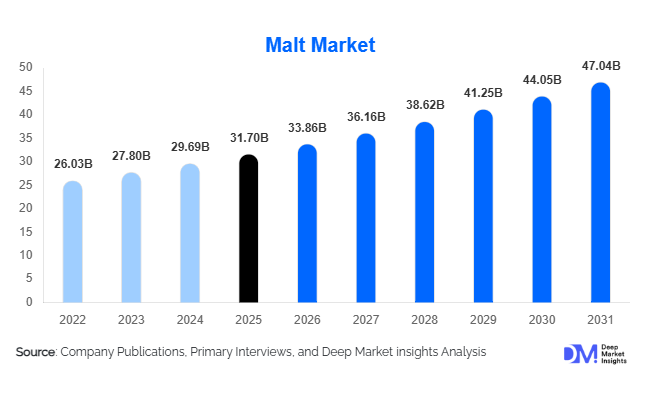

According to Deep Market Insights, the global malt market size was valued at USD 31.7 billion in 2025 and is projected to grow from USD 33.86 billion in 2026 to reach USD 47.04 billion by 2031, expanding at a CAGR of 6.8% during the forecast period (2026–2031). The malt market growth is primarily driven by rising global beer production, increasing demand for craft and premium alcoholic beverages, expanding applications of malt extracts in food and beverage processing, and growing consumer preference for natural and clean-label ingredients.

Key Market Insights

- Specialty malt demand is increasing rapidly, supported by the global expansion of craft breweries and premium beer innovations focused on unique flavor profiles and color differentiation.

- Barley malt continues to dominate the industry, accounting for the majority of global production due to its superior enzymatic activity and brewing efficiency.

- Europe remains the largest malt-producing region, supported by strong barley cultivation, advanced malting infrastructure, and high beer consumption levels.

- Asia-Pacific is the fastest-growing regional market, driven by expanding brewery production, urbanization, and rising disposable incomes in China, India, and Southeast Asia.

- Food and nutritional beverage applications are gaining momentum, as malt extracts are increasingly used in bakery products, dairy beverages, cereals, and functional health drinks.

- Technological modernization in malting operations, including automated germination systems, AI-based quality monitoring, and energy-efficient kilning technologies, is improving operational efficiency and sustainability.

malt market latest trends

Rising Demand for Specialty and Craft Brewing Malt

The global expansion of craft breweries is significantly reshaping the malt market landscape. Breweries are increasingly utilizing specialty malts such as roasted, caramel, smoked, and chocolate malt to create differentiated beer products with unique flavor, aroma, and color profiles. Consumers are shifting toward premium and artisanal alcoholic beverages, encouraging brewers to experiment with customized malt blends. Craft breweries in North America, Europe, and Asia-Pacific are especially contributing to demand for small-batch and premium-quality malt ingredients. This trend is further driving investments in specialty malting facilities and product innovation. Malt manufacturers are also collaborating directly with craft brewers to develop tailored formulations that align with evolving consumer taste preferences and seasonal beer launches.

Expansion of Malt-Based Functional and Nutritional Beverages

Malt ingredients are increasingly being incorporated into health-oriented beverages and nutritional products. Consumers are favoring natural sweeteners and clean-label ingredients, making malt extracts attractive for dairy beverages, malted milk drinks, sports nutrition products, and fortified health beverages. The demand for non-alcoholic malt beverages is also growing rapidly, particularly in the Middle East, Asia, and parts of Africa. Beverage manufacturers are positioning malt-based drinks as natural energy sources enriched with vitamins, minerals, and antioxidants. Additionally, organic and non-GMO malt products are gaining traction among health-conscious consumers, prompting manufacturers to diversify product portfolios. The increasing popularity of low-alcohol and alcohol-free beer categories is further contributing to specialty malt demand globally.

malt market drivers

Growth in Global Beer Consumption

The continuous expansion of the global brewing industry remains the primary driver of the malt market. Beer production volumes are increasing across emerging economies due to rising urbanization, expanding middle-class populations, and evolving social consumption trends. Premiumization within the beer industry is accelerating demand for high-quality and specialty malt products. Craft breweries, microbreweries, and independent brewers are increasingly emphasizing flavor complexity and ingredient authenticity, leading to higher malt consumption per unit of beer produced. Growing demand for flavored beers, dark lagers, and premium ales is also supporting specialty malt utilization across developed and emerging markets.

Increasing Adoption in Food Processing Applications

Malt is increasingly being used in bakery products, breakfast cereals, confectionery, dairy products, and nutritional beverages due to its natural sweetness, flavor-enhancing properties, and functional benefits. Food manufacturers are incorporating malt extracts into clean-label product formulations to replace artificial sweeteners and synthetic additives. Bakery applications remain particularly important, as malt improves crust color, dough fermentation, texture, and shelf life. The expansion of functional foods and fortified beverage categories is further increasing industrial demand for malt ingredients globally.

global market restraints

Volatility in Barley Prices and Agricultural Supply

The malt market is highly dependent on global barley production, making it vulnerable to agricultural disruptions and raw material price volatility. Climate change, drought conditions, unpredictable rainfall patterns, and declining crop yields in major barley-producing regions such as Europe and Australia have created procurement challenges for malt manufacturers. Fluctuations in barley prices directly impact production costs and profit margins, especially for smaller maltsters operating under long-term supply agreements with breweries.

High Energy Consumption in Malting Operations

Malting processes, including germination, drying, and kilning, require significant energy inputs. Rising fuel and electricity costs are increasing operational expenses for manufacturers globally. Environmental regulations related to emissions, water utilization, and industrial waste management are also becoming stricter, particularly in Europe and North America. Smaller producers often face difficulties investing in sustainable infrastructure upgrades, which can limit profitability and expansion opportunities. Additionally, transportation costs and supply chain disruptions continue to affect overall market pricing dynamics.

malt industry key opportunities

Growth of Non-Alcoholic and Low-Alcohol Beverages

The rapid expansion of non-alcoholic and low-alcohol beverage categories presents a major opportunity for malt manufacturers. Consumers are increasingly reducing alcohol intake while still seeking authentic beer flavors and premium beverage experiences. Specialty malt ingredients play a crucial role in maintaining flavor complexity and mouthfeel in alcohol-free beer formulations. Breweries are investing heavily in low-alcohol product development across Europe, the Middle East, and Asia-Pacific, creating sustained demand for high-quality malt ingredients. This trend is expected to generate long-term opportunities for both established malt producers and new entrants focused on functional beverage innovation.

Sustainable and Organic Malt Production

Growing consumer awareness regarding sustainability and environmentally responsible sourcing is encouraging demand for organic and clean-label malt products. Malt manufacturers are increasingly investing in renewable energy systems, low-emission kilning technologies, and sustainable barley sourcing partnerships. Governments across Europe and Asia are also supporting sustainable agriculture initiatives that improve barley productivity while reducing environmental impact. Organic malt is emerging as a premium category in both brewing and food applications, particularly in developed consumer markets where demand for traceable and eco-certified ingredients continues to increase.

Product Type Insights

Base malt continues to dominate the global malt market, holding the largest consumption share owing to its essential role as the primary fermentable base in mainstream beer production. Its strong enzymatic profile and consistency make it indispensable for large-scale brewing operations where efficiency, cost optimization, and flavor stability are critical performance drivers. Pale malt and pilsner malt remain the most widely utilized variants, supported by their high diastatic power and broad applicability across diverse beer styles, from lagers to ales. The dominance of these variants is reinforced by standardized industrial brewing processes and the need for reliable raw material performance at scale.Specialty malt represents the fastest-growing product category, propelled by the global expansion of craft brewing and the intensifying consumer shift toward premium, flavor-rich, and differentiated alcoholic beverages. Growth in this segment is primarily driven by innovation in craft beer formulations, where brewers increasingly rely on caramel, crystal, roasted, smoked, and chocolate malts to develop unique color profiles, aroma complexity, and taste differentiation. Functional malt variants with enhanced enzymatic efficiency are gaining traction in industrial brewing environments focused on improving yield, fermentation control, and operational consistency. Additionally, organic and gluten-free malt categories are expanding steadily, supported by health-conscious consumption patterns and rising demand for clean-label ingredients across both food and beverage applications.

Application Insights

The brewing industry remains the dominant application segment in the global malt market, driven by malt’s indispensable role in fermentation, flavor development, and color formation in beer production. Large-scale breweries continue to generate stable demand due to high-volume production cycles and standardized formulations, while craft breweries act as the primary growth accelerator, fueled by experimentation, premiumization strategies, and rising consumer demand for artisanal and locally produced beer variants. The growth of specialty brewing is further reinforcing demand for diverse malt profiles that enable innovation in product development.Food processing applications are witnessing steady expansion, supported by increasing adoption of malt extracts as natural sweeteners, colorants, and flavor enhancers. The growth driver in this segment is the clean-label movement, where manufacturers are replacing artificial additives with natural ingredients to meet evolving regulatory standards and consumer expectations. Malt is increasingly integrated into bakery products, confectionery formulations, breakfast cereals, and dairy-based beverages due to its nutritional value and functional properties. Nutritional beverage manufacturers are also incorporating malt in energy drinks and health-focused beverages, leveraging its carbohydrate content and perceived natural energy benefits. Meanwhile, non-alcoholic malt beverages continue to gain traction in culturally and regionally significant markets, particularly across parts of Asia and the Middle East, where demand is driven by tradition, affordability, and increasing preference for functional refreshment beverages.

Distribution Channel Insights

Direct B2B sales remain the cornerstone distribution channel in the global malt market, primarily driven by long-term contractual relationships between malt producers and large breweries or food manufacturing companies. This channel is reinforced by the need for supply chain stability, price predictability, and consistent quality assurance in high-volume procurement environments. Large buyers often prioritize integrated supply agreements to secure uninterrupted access to malt amid fluctuating barley production and global commodity price volatility.Ingredient distributors and specialty suppliers play a crucial role in serving small and medium-scale breweries, craft beverage producers, and food processors that require flexible sourcing and smaller batch volumes. The growth of this channel is supported by the fragmentation of the craft brewing industry and the increasing demand for product diversity. Digital procurement platforms are emerging as an additional growth enabler, improving price transparency, simplifying supplier access, and enhancing procurement efficiency for independent producers. In response, malt manufacturers are strengthening digital engagement capabilities and integrating supply chain management systems to improve responsiveness, reduce lead times, and enhance customer retention in a highly competitive sourcing environment.

End-Use Industry Insights

Breweries represent the largest end-use industry for malt globally, with macro breweries accounting for the majority of consumption due to their large-scale production requirements and standardized beer formulations. The key growth driver in this segment is sustained global beer consumption combined with operational scaling in emerging markets. However, craft breweries and microbreweries are emerging as the fastest-growing sub-segment, driven by consumer demand for premium, innovative, and locally differentiated beer products. This shift is encouraging malt suppliers to diversify product portfolios and support small-scale brewers with specialized malt blends.Food processing companies form another significant end-use category, where malt is increasingly used in bakery, confectionery, and functional food applications. Growth in this segment is primarily driven by the clean-label trend and rising demand for natural ingredient substitutes. Beverage manufacturers are expanding malt usage in both functional drinks and non-alcoholic beverages, supported by consumer preference for healthier, energy-boosting, and naturally derived ingredients. Distilleries, particularly whiskey producers, continue to contribute stable demand, with growth driven by premium spirit consumption and aging inventory cycles. Additionally, nutraceutical companies are exploring malt as a base ingredient in fortified foods and dietary supplements, expanding its application scope beyond traditional food and beverage industries.

| By Product Type | By Raw Material | By Application | By Form | By Distribution Channel |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America accounts for a significant share of global malt consumption, driven by a highly developed craft brewing ecosystem and strong demand for specialty beer varieties. The region’s growth is primarily supported by rising consumer preference for premium, low-alcohol, and flavor-diverse beer products, particularly in the United States. Innovation in craft brewing and the expansion of independent breweries are key structural drivers supporting sustained malt demand. Canada further strengthens regional supply dynamics through established barley production and export-oriented malting infrastructure, while increasing investments in sustainable brewing technologies and energy-efficient production processes continue to enhance long-term market competitiveness.

Europe

Europe remains the largest regional malt market, supported by deep-rooted brewing traditions, advanced malting infrastructure, and strong barley cultivation capacity. Germany, France, the United Kingdom, and Belgium collectively anchor regional demand, with Germany playing a dual role as both a major producer and exporter. The primary growth driver in Europe is the premiumization of beer consumption combined with rising demand for craft and organic malt products. Regulatory emphasis on sustainability and carbon-efficient production is accelerating investment in modern malting technologies, while France’s strong barley export ecosystem enhances supply chain stability across the continent.

Asia-Pacific

Asia-Pacific is the fastest-growing regional malt market, driven by rapid urbanization, rising disposable incomes, and expanding beer consumption across emerging economies. China leads regional demand due to its large-scale brewing industry and increasing consumption of premium beer varieties. India represents a high-growth market supported by expanding brewery investments, evolving consumer lifestyles, and increasing Western influence on beverage consumption patterns. Japan, South Korea, Vietnam, and Australia also contribute significantly to demand growth, particularly in specialty beer and non-alcoholic beverage categories. The primary regional driver is the structural shift toward branded, premium alcoholic beverages combined with rapid expansion of the hospitality and retail beverage sectors.

Latin America

Latin America is experiencing steady malt market growth, led by Brazil, Mexico, and Argentina. Brazil dominates regional consumption due to its large beer market and rising preference for premium and craft beer products. Growth is further supported by expanding domestic brewery capacity and increasing investment from global beverage companies. Mexico’s strong export-oriented beer industry acts as a key demand stabilizer for malt, while urbanization and evolving consumer preferences across the region continue to support long-term consumption growth. The overall regional driver is the gradual shift toward premiumization and increasing integration of global beer consumption trends.

Middle East & Africa

The Middle East & Africa region is emerging as a high-potential growth market for malt, driven by increasing demand for non-alcoholic malt beverages and expanding urban beverage consumption. In the Gulf countries, cultural preferences strongly support non-alcoholic malt drinks, with growth further reinforced by rising health-consciousness and demand for functional beverages. South Africa remains the most developed malt-consuming market in Sub-Saharan Africa due to its established brewing sector and expanding production capacity. Meanwhile, countries such as Nigeria, Ethiopia, and Kenya are witnessing rising brewery investments and increasing beer consumption linked to urbanization and demographic growth. The key regional driver is rapid urban population expansion combined with evolving beverage consumption habits and increasing investment in local brewing infrastructure.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Malt Market

- Malteurop Group

- Boortmalt

- Soufflet Malt

- Cargill

- GrainCorp

- Viking Malt

- Crisp Malt

- Muntons

- Bairds Malt

- Maltexco

- Axereal

- Simpsons Malt

- IREKS

- Prairie Malt

- United Malt Group