Luncheon Meat Market Size

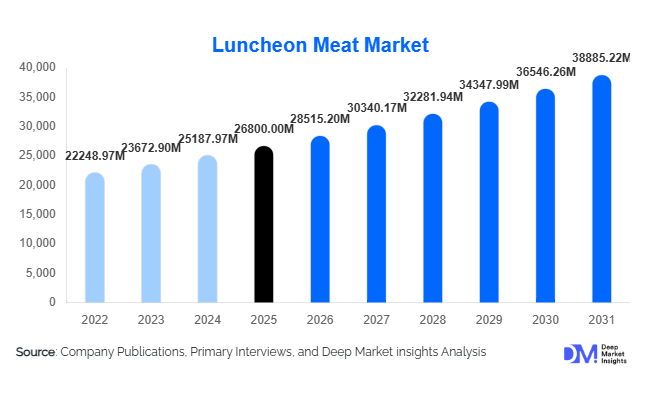

According to Deep Market Insights, the global luncheon meat market size was valued at USD 26,800 million in 2025 and is projected to grow from USD 28,515.20 million in 2026 to reach USD 38,885.22 million by 2031, expanding at a CAGR of 6.4% during the forecast period (2026–2031). The luncheon meat market growth is primarily driven by rising demand for convenient, ready-to-eat protein sources, increasing urbanization, and the expansion of organized retail and foodservice sectors globally. The growing popularity of processed meat products across emerging economies, coupled with advancements in packaging technologies and product innovation such as low-sodium and plant-based variants, is further accelerating market expansion.

Key Market Insights

- Luncheon meat consumption is shifting toward convenience-driven eating habits, particularly in urban populations with busy lifestyles.

- Asia-Pacific dominates the global market, driven by strong consumption in China, Japan, and Southeast Asia.

- Plant-based luncheon meat alternatives are gaining traction, especially in North America and Europe.

- Canned products remain the leading packaging format, supported by long shelf life and export suitability.

- Mid-range products hold the largest market share, balancing affordability and quality.

- Technological advancements in packaging and processing are enhancing product safety, shelf life, and consumer appeal.

What are the latest trends in the luncheon meat market?

Shift Toward Healthier and Clean-Label Products

Consumers are increasingly demanding healthier processed meat options, leading manufacturers to introduce low-sodium, nitrate-free, and preservative-free luncheon meat products. Clean-label trends are particularly strong in developed markets such as North America and Europe, where consumers are scrutinizing ingredient lists more closely. This shift is pushing companies to reformulate products without compromising taste or shelf life. Organic and antibiotic-free meat sourcing is also gaining popularity, aligning with broader health and wellness trends.

Growth of Plant-Based and Alternative Proteins

The emergence of plant-based luncheon meat is transforming the competitive landscape. With rising vegan and flexitarian populations, manufacturers are investing in plant protein technologies to replicate the taste and texture of traditional meat. These products are gaining shelf space in supermarkets and online platforms, particularly in Western markets. Innovation in soy, pea, and wheat protein formulations is enabling improved product quality, opening new high-margin opportunities for producers.

What are the key drivers in the luncheon meat market?

Rising Demand for Ready-to-Eat Foods

The increasing pace of urban lifestyles is driving demand for convenient, ready-to-eat food options. Luncheon meat fits seamlessly into this trend due to its versatility, long shelf life, and ease of preparation. It is widely used in sandwiches, salads, and quick meals, making it a staple for working professionals and students. The growth of dual-income households and time-constrained consumers is further boosting demand.

Expansion of Retail and Cold Chain Infrastructure

The rapid expansion of supermarkets, hypermarkets, and convenience stores, especially in emerging economies, is enhancing product accessibility. Improved cold chain infrastructure is enabling the distribution of refrigerated and frozen variants, expanding the market beyond traditional canned products. E-commerce platforms are also playing a critical role in reaching new consumer segments and driving sales growth.

What are the restraints for the global market?

Health Concerns Related to Processed Meat

Increasing awareness about the potential health risks associated with processed meat consumption, including high sodium and preservative content, is restraining market growth. Regulatory bodies in several countries are implementing stricter labeling requirements and encouraging reduced consumption, which may impact demand in developed markets.

Volatility in Raw Material Prices

Fluctuations in the prices of key raw materials such as pork, beef, and poultry pose a significant challenge for manufacturers. Supply disruptions caused by livestock diseases or environmental factors can lead to increased production costs, affecting profit margins and pricing strategies.

What are the key opportunities in the luncheon meat industry?

Expansion in Emerging Markets

Emerging economies in Asia-Pacific, Africa, and Latin America present significant growth opportunities due to rising disposable incomes, urbanization, and changing dietary patterns. Governments are supporting food processing industries through favorable policies and infrastructure investments, creating a conducive environment for market expansion.

Packaging Innovation and Premiumization

Advancements in packaging technologies, such as modified atmosphere packaging (MAP) and vacuum sealing, are enhancing product shelf life and convenience. Premium product offerings, including organic, gourmet, and specialty flavors, are attracting higher-income consumers and improving profit margins for manufacturers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 26800.00 Million |

| Market Size in 2026 | USD 28515.20 Million |

| Market Size in 2031 | USD 38885.22 Million |

| CAGR | 6.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global luncheon meat market demonstrates a clearly structured product segmentation, with pork-based luncheon meat maintaining its dominant position, accounting for approximately 42% of the market share in 2025. This dominance is primarily driven by its cost efficiency, long-standing culinary acceptance across multiple cultures, and its adaptability across a wide range of processed food applications. Pork-based variants benefit significantly from established supply chains and large-scale production efficiencies, which allow manufacturers to maintain competitive pricing while ensuring consistent quality. In addition, the versatility of pork in flavor absorption and processing stability continues to make it the preferred raw material for canned and packaged meat products across both developed and emerging markets.Chicken-based luncheon meat is steadily gaining momentum, particularly in regions where cultural or religious dietary restrictions limit pork consumption. This segment benefits from the growing global preference for leaner protein sources, as consumers increasingly associate poultry with healthier dietary choices. The expansion of fast-food chains and ready-to-eat meal solutions has also accelerated adoption, as chicken-based variants are widely perceived as more versatile and health-aligned.Plant-based luncheon meat alternatives represent one of the fastest-growing niche segments, driven by rising veganism, flexitarian diets, and increasing awareness of environmental sustainability. Although currently smaller in share, this category is supported by strong innovation in plant protein technology, enabling manufacturers to replicate texture and flavor profiles more effectively. Mixed meat variants, which combine different protein sources, are also expanding as they cater to consumers seeking enhanced taste complexity and premium product experiences. Overall, diversification in product types is being shaped by evolving dietary preferences, health consciousness, and sustainability concerns.

Application Insights

In terms of application, household consumption continues to dominate the global luncheon meat market, accounting for nearly 48% of the total market share. This leadership is primarily driven by the convenience factor, as luncheon meat serves as a ready-to-eat protein source suitable for quick meal preparation. Increasing urbanization, busier lifestyles, and the growing demand for shelf-stable food products have further strengthened household adoption. The segment’s leading driver is convenience combined with affordability, making it an essential pantry item in both developed and emerging economies.The foodservice segment represents the fastest-growing application category, fueled by the rapid expansion of quick-service restaurants, sandwich chains, cafés, and institutional catering services. Luncheon meat is widely used in sandwiches, burgers, and fusion dishes due to its ease of preparation and consistent taste profile. The growth of this segment is strongly influenced by rising out-of-home food consumption, increasing tourism activity, and the global proliferation of standardized fast-food menus. Additionally, foodservice providers benefit from the product’s long shelf life and minimal preparation requirements, reducing operational complexity and food waste.Institutional applications, including military, healthcare facilities, and educational institutions, provide a stable and consistent demand base. The key driver in this segment is the product’s extended shelf life, nutritional reliability, and ease of bulk storage. Governments and institutional buyers prioritize processed meat products like luncheon meat for emergency food reserves and large-scale meal provisioning due to their logistical advantages. As a result, while this segment grows at a steadier pace compared to foodservice, it remains essential for market stability and long-term demand consistency.

Distribution Channel Insights

Supermarkets and hypermarkets dominate the distribution landscape, accounting for approximately 40% of global market share. This dominance is supported by their wide product assortment, strong brand visibility, and the high level of consumer trust associated with organized retail environments. These channels allow consumers to physically evaluate product packaging, pricing, and brand reputation, which significantly influences purchase decisions. The leading driver in this segment is accessibility combined with promotional pricing strategies, which encourage bulk purchases and brand switching.Convenience stores play a critical role in urban and semi-urban areas, particularly for impulse purchases and small-scale consumption needs. Their proximity to residential zones and extended operating hours make them a vital distribution channel for ready-to-eat products like luncheon meat. Meanwhile, specialty meat stores cater to premium and niche consumer segments, offering customized, organic, and gourmet variations that appeal to quality-focused buyers.Online retail is the fastest-growing distribution channel, driven by rapid digital transformation, increasing smartphone penetration, and the expansion of e-commerce grocery platforms. The convenience of home delivery, combined with attractive discounts and subscription models, is significantly reshaping consumer buying behavior. The key driver in this segment is digital accessibility and evolving consumer preference for contactless shopping experiences. Furthermore, improved cold-chain logistics have enhanced the feasibility of selling perishable meat products online, supporting sustained growth in this channel.

Pricing Insights

The mid-range pricing segment leads the global luncheon meat market with approximately 50% market share, reflecting a strong balance between affordability and perceived product quality. This segment appeals to a broad consumer base, particularly middle-income households that prioritize value for money without compromising on taste and nutritional consistency. The primary driver of this segment is its ability to cater to mass-market demand while maintaining consistent product quality standards across regions.Economy-priced luncheon meat products maintain strong demand in developing regions where price sensitivity is high and processed meat consumption is expanding due to urbanization and rising population density. These products focus on affordability and accessibility, often leveraging cost-efficient production methods and simplified packaging formats.Premium and gourmet segments are witnessing increasing traction in developed markets, driven by rising disposable incomes, evolving consumer tastes, and demand for high-quality, organic, and clean-label products. These offerings often include reduced preservatives, higher meat content, and specialty flavoring. The key driver for the premium segment is health consciousness combined with lifestyle-oriented consumption patterns, where consumers are willing to pay more for perceived quality, transparency, and sustainability.

Explore more data points, trends and opportunities Download Free Sample Report

Luncheon Meat Market Segmentations

By Product Type

- Pork-Based Luncheon Meat

- Chicken-Based Luncheon Meat

- Beef-Based Luncheon Meat

- Mixed Meat Luncheon Meat

- Plant-Based Luncheon Meat

By Application

- Household Consumption

- Foodservice

- Institutional Use

- Industrial Use

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail / E-commerce

- Specialty Meat Stores

- Foodservice / HoReCa Supply

Regional Insights

Asia-Pacific

Asia-Pacific holds the largest share of the global luncheon meat market, accounting for approximately 38% in 2025. This dominance is strongly driven by high population density, rapid urbanization, and deeply rooted consumption of processed pork products, particularly in China. China remains the largest national market due to its established processed meat industry, strong domestic demand, and widespread retail penetration. Japan and South Korea also contribute significantly, supported by high per capita consumption of convenience food products.The key drivers of regional growth include expanding middle-class populations, increasing disposable incomes, and shifting dietary habits toward convenience-oriented food products. Southeast Asian countries are witnessing accelerated growth due to modernization of retail infrastructure, rising fast-food penetration, and growing working-class populations seeking affordable ready-to-eat meals. India and Indonesia are emerging high-growth markets where changing lifestyles, urban migration, and exposure to global food culture are reshaping consumption patterns. Overall, Asia-Pacific growth is anchored in demographic expansion, dietary transition, and strong retail ecosystem development.

North America

North America accounts for around 24% of the global market, with the United States leading consumption due to its well-established processed food industry and high demand for convenience-based protein sources. The region is characterized by strong innovation in product formulation, particularly in premium, organic, nitrate-free, and low-sodium luncheon meat variants.The primary driver of growth in North America is the rising consumer preference for healthier and clean-label products, combined with strong retail penetration and advanced food processing technologies. Additionally, busy lifestyles and high demand for ready-to-eat meals continue to support steady consumption. The region also benefits from strong brand presence and continuous product innovation by major food manufacturers, ensuring sustained market maturity and premiumization trends.

Europe

Europe represents approximately 20% of the global market, led by key countries such as Germany, the United Kingdom, and France. The region is highly regulated, with strict food safety standards and labeling requirements shaping product development and marketing strategies. Consumer awareness regarding health, sustainability, and ethical sourcing is particularly high, influencing purchasing decisions.The leading driver in Europe is the increasing demand for organic, sustainably sourced, and clean-label meat products. Consumers are highly responsive to transparency in production processes, encouraging manufacturers to invest in traceability and certification systems. Additionally, the growing trend of premiumization and gourmet processed foods supports steady market expansion despite relatively moderate consumption growth compared to Asia-Pacific.

Latin America

Latin America accounts for around 10% of the global market, with Brazil and Mexico serving as the primary contributors due to their strong meat production industries and expanding domestic consumption. The region benefits from abundant livestock resources and established food processing capabilities, which support both local consumption and export-oriented production.The key driver of growth in Latin America is increasing urbanization combined with rising demand for affordable protein sources. As more consumers migrate to urban centers, the demand for convenient, shelf-stable food products continues to rise. Additionally, improvements in retail infrastructure and expanding supermarket penetration are enhancing product accessibility, further supporting market expansion.

Middle East & Africa

The Middle East & Africa region accounts for approximately 8% of the global market, with growth primarily driven by urbanization, rising disposable incomes, and increasing demand for halal-certified processed meat products. Countries such as the UAE and Saudi Arabia are major importers, supported by strong retail development and tourism-driven foodservice demand.The key driver in this region is the expansion of halal-certified food supply chains, ensuring compliance with religious dietary requirements while meeting growing demand for convenience foods. Africa, while still in a developing stage, is experiencing gradual growth supported by urban population expansion, improving cold-chain logistics, and increasing exposure to packaged food products. Overall, the region presents long-term growth potential driven by demographic shifts and retail modernization.

Key Players in the Luncheon Meat Market

- Hormel Foods Corporation

- WH Group Limited

- Nestlé S.A.

- Tyson Foods Inc.

- JBS S.A.

- Conagra Brands Inc.

- Maple Leaf Foods Inc.

- BRF S.A.

- Danish Crown A/S

- Smithfield Foods Inc.

- Marfrig Global Foods S.A.

- Perdue Farms Inc.

- Cargill Incorporated

- Itoham Yonekyu Holdings Inc.

- Tulip Food Company