Low-Intensity Sweeteners Market Size

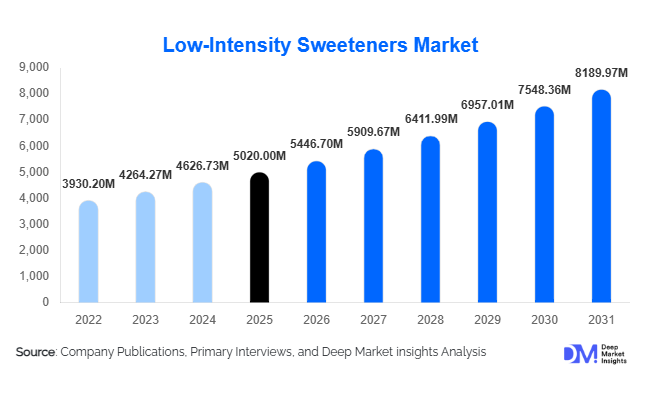

According to Deep Market Insights,the global low-intensity sweeteners market size was valued at USD 5,020 million in 2025 and is projected to grow from USD 5,446.70 million in 2026 to reach USD 8,189.97 million by 2031, expanding at a CAGR of 8.5% during the forecast period (2026–2031). Market growth is primarily driven by rising sugar-reduction mandates, increasing diabetic and obese populations, and the growing demand for bulk sweetening agents that maintain texture and mouthfeel in reformulated food and beverage products.

Key Market Insights

- Polyols dominate the global market, accounting for over 60% share, due to established industrial-scale production and widespread usage in bakery and confectionery.

- Bakery & confectionery remains the largest application segment, contributing more than one-third of total demand.

- North America leads global consumption, supported by strong reformulation initiatives and sugar-tax driven product innovation.

- Asia-Pacific is the fastest-growing region, driven by expanding processed food industries in China and India.

- Rare sugars such as allulose are witnessing rapid commercialization, supported by fermentation-based cost efficiencies.

- Pharmaceutical and nutraceutical applications are accelerating, particularly for low-glycemic syrups and chewable formulations.

What are the latest trends in the low-intensity sweeteners market?

Shift Toward Rare Sugars and Clean-Label Formulations

Food manufacturers are increasingly incorporating rare sugars such as allulose and tagatose into reformulated products due to their near-sucrose taste profile and low caloric value. These ingredients enable sugar reduction without compromising volume or texture. Clean-label positioning is becoming a strategic differentiator, especially in North America and Europe, where consumers prefer plant-derived and minimally processed ingredients. As fermentation technologies improve yield efficiency, rare sugars are becoming more commercially viable across mainstream applications.

Expansion of Sugar-Reduction Reformulation Programs

Global sugar tax policies and voluntary sugar reduction commitments by multinational food brands are accelerating reformulation demand. Low-intensity sweeteners offer bulk functionality absent in high-intensity sweeteners, making them essential in baked goods, dairy, and beverages. Companies are increasingly adopting blended sweetening systems combining polyols and rare sugars to optimize taste, cost, and functionality.

What are the key drivers in the low-intensity sweeteners market?

Rising Global Diabetes and Obesity Rates

With over 500 million individuals globally affected by diabetes, demand for low-glycemic sweetening alternatives is expanding rapidly. Low-intensity sweeteners provide controlled blood glucose impact, making them suitable for diabetic-friendly and keto products.

Sugar Tax Implementation and Regulatory Pressure

More than 40 countries have introduced sugar taxes, encouraging food and beverage manufacturers to reformulate products. Low-intensity sweeteners allow volume replacement while reducing taxable sugar content, strengthening their adoption in processed foods and beverages.

Growth in Functional and Nutraceutical Foods

Sports nutrition, protein bars, meal replacements, and functional beverages increasingly utilize polyols and rare sugars. The nutraceutical sector is growing above 9% CAGR globally, directly supporting ingredient demand.

What are the restraints for the global market?

Digestive Tolerance Limitations

Excessive consumption of certain polyols can cause gastrointestinal discomfort, limiting high inclusion rates in some formulations.

Higher Production Costs of Rare Sugars

Allulose and tagatose remain costlier than conventional sucrose and sorbitol, restricting penetration in price-sensitive developing markets.

What are the key opportunities in the low-intensity sweeteners industry?

Biotechnological Manufacturing Advancements

Fermentation-based production is reducing costs and improving scalability of rare sugars. Investments in bioreactors and enzymatic conversion facilities are expected to lower production costs by 10–15% over the next five years, opening opportunities for wider adoption.

Expansion in Emerging Markets

Rapid urbanization in India, Southeast Asia, and Latin America is driving demand for packaged and reduced-sugar foods. Companies entering these regions with cost-optimized formulations can capture substantial untapped demand.

Pharmaceutical and Oral Care Applications

Polyols such as sorbitol and xylitol are widely used in syrups, chewable tablets, and toothpaste due to non-cariogenic properties. Growth in OTC medicines and oral care products provides stable long-term demand.

Product Type Insights

Polyols dominate the global low-calorie sweetener market, accounting for a 62% share in 2025. The segment’s leadership is primarily driven by its cost efficiency, bulk sweetening capability, and functional properties such as moisture retention, mouthfeel enhancement, and stability under heat processing. Strong production infrastructure in China and the U.S. further strengthens supply chain efficiency and global export capabilities. Sorbitol and maltitol remain the leading bulk sweeteners in confectionery and bakery applications due to their textural functionality, low glycemic response, and compatibility with sugar-free formulations.

Rare sugars, though smaller in overall share, represent the fastest-growing product category, driven by increasing consumer demand for low-calorie, clean-label, and minimally processed alternatives. Rising awareness of metabolic health and obesity management is accelerating adoption in premium food and beverage formulations. Specialty low-calorie syrups are also gaining traction in beverages and dairy applications, particularly in reduced-sugar carbonated drinks, flavored milk, and protein-enriched formulations, where maintaining mouthfeel and sweetness balance is critical.

Application Insights

Bakery & confectionery accounts for 34% of the global market share in 2025, making it the leading application segment. The primary growth driver is the rising demand for sugar-free chocolates, cookies, candies, and reduced-calorie cakes amid growing consumer preference for healthier indulgence products. Manufacturers are increasingly reformulating legacy products to comply with sugar-reduction mandates while maintaining taste parity.

Dairy & frozen desserts represent one of the fastest-expanding application areas, supported by strong demand for low-fat, diabetic-friendly, and high-protein formulations. The growth of functional yogurt, sugar-reduced ice creams, and lactose-free dairy beverages is accelerating polyol and blended sweetener adoption.

The beverages segment is witnessing increasing incorporation of blended low-intensity sweetening systems to reduce total sugar content while preserving mouthfeel and flavor complexity. Reformulated carbonated soft drinks, energy beverages, and flavored waters are key contributors. Pharmaceutical applications represent a high-margin and stable segment, supported by long-term supply contracts for sugar-free medicinal syrups, chewable tablets, lozenges, and pediatric formulations.

End-Use Industry Insights

Food & beverage processing dominates the market with a 68% share in 2025, valued at over USD 3.5 billion in 2026. The leading driver for this segment is large-scale reformulation initiatives across packaged foods, driven by regulatory sugar-reduction mandates, evolving labeling standards, and increasing consumer awareness of diabetes and obesity risks. Major multinational food processors are integrating bulk sweeteners into reformulated SKUs to achieve calorie reduction without compromising sensory attributes.

Pharmaceutical manufacturing is the fastest-growing end-use segment, expanding at nearly 9.5% CAGR. Growth is driven by rising demand for sugar-free medicinal syrups, chewables, and nutraceutical supplements targeting diabetic and pediatric populations. Increased R&D investment in oral dosage formulations further supports segment expansion.

Export-driven demand remains particularly strong in Asia-Pacific, where China serves as a major exporter of sorbitol and maltitol to North America and Europe. Emerging keto, low-carb, and diabetic nutrition brands are increasing procurement volumes, further supporting long-term industry growth.

| By Product Type | By Form | By Source | By Application | By Distribution Channel |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America holds 32% market share in 2025, led by the U.S., which accounts for over 80% of regional consumption. The region is projected to grow at approximately 8% CAGR. Key growth drivers include strong regulatory pressure for sugar reduction, high prevalence of diabetes and obesity, and widespread implementation of front-of-pack labeling initiatives. Major food manufacturers are actively reformulating beverages and packaged snacks to comply with federal dietary guidelines. The growing demand for keto, low-carb, and diabetic-friendly products further accelerates polyol and blended sweetener adoption.

Europe

Europe represents 27% of global market share in 2025, driven by Germany, France, and the U.K. Regional growth is supported by strict regulatory oversight and sugar tax frameworks that incentivize reformulation across beverages and confectionery categories. Strong consumer preference for clean-label and plant-based products is accelerating demand for rare sugars and specialty syrups. Additionally, high penetration of private-label reformulated products across retail chains contributes to stable long-term demand growth.

Asia-Pacific

Asia-Pacific is the fastest-growing region, expanding at a 9.5% CAGR. China dominates global production and export supply due to its established manufacturing infrastructure and cost advantages. India is emerging as a high-growth consumption market, driven by rapid urbanization, rising disposable incomes, and expanding processed food demand. Increasing diabetic population levels and growing awareness of low-calorie diets further stimulate regional demand. Japan and South Korea are also advancing innovation in functional and specialty sweetener formulations.

Latin America

Latin America is experiencing steady growth, led by Brazil and Mexico. Regional expansion is supported by sugar tax implementation, growing packaged food penetration, and rising health awareness among urban populations. Reformulation of carbonated beverages and dairy products remains a primary driver. Increasing investment from multinational food companies is strengthening distribution networks and product availability.

Middle East & Africa

The Middle East & Africa region is witnessing gradual but consistent growth. GCC countries are seeing increased demand for reformulated beverages and low-calorie dairy products, supported by government-led health awareness campaigns. In Africa, South Africa leads consumption due to its relatively advanced food processing industry and expanding retail sector. Rising lifestyle-related health conditions and urbanization trends are expected to sustain long-term market expansion.

The market is moderately consolidated, with the top five companies accounting for approximately 48% of global market share. Leading players maintain competitive advantages through large-scale production capacity, vertical integration in corn processing, and global distribution networks.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Low-Intensity Sweeteners Market

- Cargill Incorporated

- Archer Daniels Midland Company

- Ingredion Incorporated

- Roquette Frères

- Tate & Lyle PLC

- Mitsubishi Corporation Life Sciences

- Tereos Group

- Gulshan Polyols Ltd

- SPI Pharma

- Samyang Corporation

- Shandong Sanyuan Biotechnology

- CJ CheilJedang

- DuPont Nutrition & Biosciences

- Futaste Co., Ltd.

- Baolingbao Biology Co., Ltd.