Low Fat Cheese Market Size

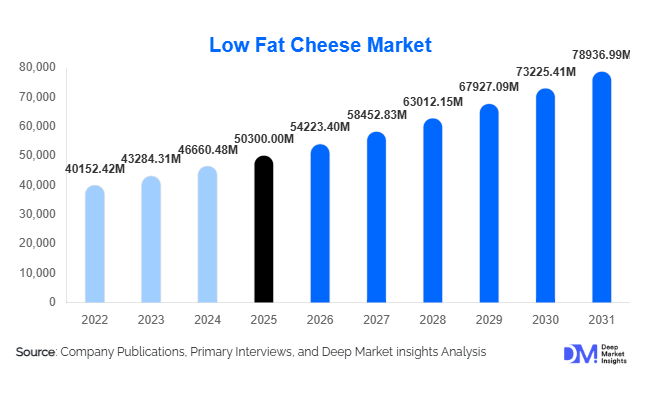

According to Deep Market Insights, the global low fat cheese market size was valued at USD 50,300 million in 2025 and is projected to grow from USD 54,223.40 million in 2026 to reach USD 78,936.99 million by 2031, expanding at a CAGR of 7.8% during the forecast period (2026–2031). Market growth is primarily driven by increasing global health awareness, rising adoption of reduced-fat dairy products, and growing demand from foodservice operators seeking healthier ingredient alternatives without compromising taste and texture. The expansion of protein-focused diets, urbanization, and innovation in dairy processing technologies are further accelerating adoption across both developed and emerging economies.

Key Market Insights

- Health-conscious consumption trends are transforming dairy purchasing behavior, with consumers shifting toward reduced-fat alternatives to manage calorie and cholesterol intake.

- Quick-service restaurants (QSRs) and processed food manufacturers are major demand drivers, particularly for low fat mozzarella and processed cheese formats.

- North America dominates global consumption, supported by mature dairy infrastructure and strong demand for functional dairy products.

- Asia-Pacific represents the fastest-growing regional market, driven by westernized diets and expanding retail penetration in China and India.

- Product innovation focusing on protein fortification and clean-label formulations is reshaping competitive differentiation.

- E-commerce grocery platforms are emerging as a key distribution channel, enabling premium product accessibility and direct-to-consumer dairy sales.

What are the latest trends in the low fat cheese market?

Functional and High-Protein Dairy Innovation

Low fat cheese is increasingly positioned as a functional food rather than merely a reduced-calorie alternative. Manufacturers are introducing protein-enriched, probiotic-enhanced, and calcium-fortified cheese variants targeting fitness-conscious consumers and aging populations. These innovations align with growing global demand for nutrient-dense foods that support weight management, muscle health, and digestive wellness. Clean-label trends are also influencing product development, with brands minimizing artificial stabilizers and emphasizing natural processing techniques. Functional positioning allows manufacturers to command premium pricing while expanding adoption beyond traditional diet-focused consumers.

Expansion of Convenience-Oriented Cheese Formats

Consumer preference for convenience is accelerating demand for shredded, sliced, and snack-sized low fat cheese formats. Ready-to-use cheese products are increasingly integrated into home cooking, meal kits, and ready-to-eat meals. Retailers are expanding refrigerated shelf space for portion-controlled packs targeting busy urban households. Food manufacturers are also incorporating low fat cheese into frozen meals and packaged snacks, supporting sustained volume growth. Packaging innovation, including resealable and single-serve formats, is improving product shelf life and usability, further enhancing consumer adoption.

What are the key drivers in the low fat cheese market?

Rising Health and Lifestyle Awareness

The growing prevalence of obesity and cardiovascular diseases has significantly influenced dietary choices worldwide. Consumers are actively reducing saturated fat intake while maintaining protein consumption, making low fat cheese an attractive alternative to conventional cheese products. Public health campaigns and nutritional labeling regulations are reinforcing consumer awareness, accelerating adoption across retail and institutional food channels.

Growth of Foodservice and Quick-Service Restaurants

The rapid expansion of global QSR chains has increased demand for low fat cheese varieties used in pizzas, sandwiches, and ready meals. Restaurants are reformulating menus to align with calorie transparency regulations and healthier menu positioning. Low fat mozzarella, in particular, enables foodservice operators to reduce fat content while maintaining meltability and flavor consistency, making it a preferred ingredient across large-scale food production.

What are the restraints for the global market?

Texture and Taste Perception Challenges

Despite technological advancements, some consumers still perceive low fat cheese as inferior in taste and mouthfeel compared to full-fat alternatives. Achieving optimal meltability and creaminess remains technically challenging, requiring ongoing investment in formulation and processing technologies.

Volatility in Dairy Raw Material Prices

Fluctuations in milk prices significantly impact production costs and profit margins. Additional processing required to reduce fat content increases operational complexity, placing cost pressure on manufacturers and limiting price competitiveness in certain markets.

What are the key opportunities in the low fat cheese industry?

Emerging Market Expansion

Rapid urbanization and western dietary adoption in Asia-Pacific and Middle Eastern countries present substantial growth opportunities. Rising disposable incomes and expanding cold-chain infrastructure are enabling greater penetration of cheese products in traditionally low-consumption regions. Early market entry and localized product development are expected to provide competitive advantages.

Foodservice Reformulation Partnerships

Collaborations between dairy producers and restaurant chains represent a significant opportunity. Customized low fat cheese formulations designed for specific culinary applications can secure long-term supply contracts and stable revenue streams. Institutional catering and ready-meal manufacturers are increasingly seeking healthier ingredient sourcing, expanding industrial demand.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 50300 Million |

| Market Size in 2026 | USD 54223.40 Million |

| Market Size in 2031 | USD 78936.99 Million |

| CAGR | 7.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Low fat mozzarella continues to dominate the global low fat cheese market, accounting for nearly 28% of total market share in 2025. Its leadership position is primarily supported by extensive utilization across commercial pizza production, quick-service restaurant chains, and industrial food processing applications. The cheese’s superior melting characteristics, balanced flavor profile, and compatibility with calorie-conscious menu reformulations make it the preferred ingredient for manufacturers seeking healthier alternatives without compromising texture or taste. Growing consumer preference for reduced-fat versions of traditionally indulgent foods has further accelerated adoption, particularly within frozen pizza and ready-meal categories where nutritional reformulation remains a key innovation strategy.Reduced-fat cheddar and processed cheese slices represent significant secondary product categories due to their versatility across sandwiches, burgers, snacks, and packaged convenience foods. Manufacturers increasingly focus on maintaining flavor retention and functional performance while reducing fat content, supported by advancements in dairy processing technologies and enzyme optimization. Meanwhile, cottage cheese is experiencing strong growth momentum as health-conscious consumers prioritize high-protein, low-calorie dietary options aligned with fitness, weight management, and active lifestyle trends. Its inclusion in breakfast meals, protein bowls, and diet-focused meal plans continues to expand retail demand globally.Specialty functional cheeses, including fortified, probiotic-enhanced, lactose-modified, and micronutrient-enriched varieties, represent the fastest-growing product segment. This growth is driven by rising consumer awareness regarding gut health, immunity support, and functional nutrition. Dairy producers are increasingly investing in product innovation to address evolving dietary preferences, including clean-label formulations and functional dairy solutions targeting aging populations and wellness-focused consumers. The shift toward value-added dairy offerings is expected to strengthen premiumization trends within the market over the forecast period.

Application Insights

Foodservice applications account for approximately 39% of global demand, making them one of the most influential consumption segments within the low fat cheese market. The rapid expansion of quick-service restaurants, fast-casual dining formats, and international pizza chains has significantly increased bulk procurement of reduced-fat cheese variants. Operators are actively reformulating menus to meet consumer demand for healthier dining options while maintaining familiar taste profiles, positioning low fat cheese as a critical ingredient across pizzas, pasta dishes, sandwiches, and baked menu items. The continued globalization of western-style dining habits further strengthens long-term demand within this segment.Household consumption remains dominant in overall volume terms, supported by rising at-home cooking trends, expanding retail availability, and growing nutritional awareness among consumers. Increased adoption of healthier meal preparation practices, particularly after shifts in consumer eating habits toward home-based dining, has encouraged greater use of reduced-fat dairy ingredients in daily cooking. Retail packaging innovations, portion-controlled formats, and improved shelf-life technologies are also enhancing accessibility for household buyers.The bakery and processed food industries are rapidly integrating low fat cheese into snacks, frozen foods, savory baked goods, and convenience meal solutions. Manufacturers increasingly incorporate reduced-fat ingredients to comply with evolving nutritional standards and clean-label expectations. Additionally, nutritional food producers are utilizing low fat cheese in protein-rich diets, meal replacement products, and functional nutrition offerings targeting athletes, aging populations, and weight-management consumers. This diversification of applications significantly broadens the addressable market across both traditional and emerging food categories.

Distribution Channel Insights

Supermarkets and hypermarkets dominate distribution channels, collectively accounting for nearly 48% market share, driven by strong cold-chain logistics, extensive product visibility, and expansion of private-label dairy offerings. Large retail formats provide consumers with wide product variety, competitive pricing, and convenient access to both mainstream and premium reduced-fat cheese products. Retailers are also allocating increased shelf space to healthier dairy alternatives in response to shifting consumer purchasing behavior toward nutritional transparency.Online retail represents the fastest-growing distribution channel as digital grocery adoption accelerates globally. Improvements in refrigerated logistics, last-mile delivery infrastructure, and subscription-based grocery services are enabling consumers to purchase perishable dairy products with greater confidence. E-commerce platforms are also supporting niche product discovery, allowing emerging functional and specialty cheese brands to reach health-focused consumers directly.Specialty dairy stores continue to play an important role in serving premium, artisanal, and health-focused segments by offering curated selections and personalized customer engagement. Meanwhile, foodservice distribution networks remain essential for large-scale procurement by restaurants, catering companies, and institutional buyers, ensuring consistent supply and standardized quality across commercial operations.

End-Use Industry Insights

The retail consumer segment represents the largest end-use industry, supported by growing awareness of balanced nutrition, calorie reduction, and preventive health management. Consumers increasingly seek dairy products that align with wellness goals without sacrificing flavor or convenience, encouraging manufacturers to expand product lines across multiple fat-reduction levels and functional formulations. Marketing strategies emphasizing protein content, clean ingredients, and lifestyle compatibility further reinforce retail demand growth.The foodservice industry is emerging as the fastest-growing end-use segment, expanding at an annual rate exceeding 8%, driven by global fast-food expansion and menu reformulation initiatives focused on healthier offerings. Restaurant operators are adopting reduced-fat ingredients to meet regulatory pressure and evolving consumer expectations regarding nutritional transparency, particularly in urban markets with rising health consciousness.Processed food manufacturers are becoming increasingly important buyers as frozen meals, ready-to-eat foods, and convenience snack categories expand worldwide. Low fat cheese enables manufacturers to improve nutritional labeling profiles while maintaining sensory quality, making it an essential component in product innovation pipelines. Additionally, export-oriented dairy processors in Europe and Oceania are scaling production capacity to address growing international demand for reduced-fat dairy products, strengthening global supply chains and cross-border trade dynamics.

Explore more data points, trends and opportunities Download Free Sample Report

Low Fat Cheese Market Segmentations

By Product Type

- Low Fat Mozzarella Cheese

- Low Fat Cheddar Cheese

- Low Fat Cottage Cheese

- Low Fat Processed Cheese

- Low Fat Cream Cheese

- Low Fat Specialty Functional Cheese

By Application

- Foodservice

- Household/Retail Consumption

- Processed Packaged Food Manufacturing

- Bakery Ready-to-Eat Meals

- Nutritional Functional Foods

By Distribution Channel

- Supermarkets Hypermarkets

- Convenience Stores

- Online Retail E-commerce Grocery

- Specialty Dairy Stores

- Foodservice Institutional Supply

By End Use

- Retail Consumers

- Foodservice Industry

- Food Processing Manufacturers

- Institutional Catering

Regional Insights

North America

North America accounts for approximately 34% of the global market share in 2025, led primarily by the United States and Canada. Regional growth is strongly supported by high consumer awareness regarding obesity management, cardiovascular health, and calorie-controlled diets, which has accelerated adoption of reduced-fat dairy alternatives. Advanced dairy processing infrastructure enables large-scale production of technologically optimized low fat cheese with improved texture and flavor retention. The widespread penetration of quick-service restaurants and strong consumption of pizza, sandwiches, and convenience foods further reinforces consistent demand. In addition, private-label expansion by major retail chains and strong innovation investments by dairy companies contribute to sustained market maturity and product diversification across the region.

Europe

Europe holds nearly 30% market share, supported by established dairy traditions and strong regulatory frameworks promoting nutritional transparency. Countries such as Germany, France, Italy, and the United Kingdom represent major consumption hubs where consumers increasingly prefer healthier variations of traditional cheese products. Regulatory emphasis on front-of-pack labeling, fat reduction initiatives, and public health campaigns encouraging balanced diets drives manufacturers to reformulate products and expand reduced-fat portfolios. The region also benefits from a highly export-oriented dairy sector, allowing European producers to supply premium low fat cheese to global markets while maintaining stable domestic demand supported by mature retail networks.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, driven by rapid urbanization, westernization of dietary habits, and expanding modern retail infrastructure. China and India are witnessing substantial increases in cheese consumption as younger populations adopt international cuisines and convenience foods. Rising disposable incomes and growing middle-class populations are encouraging experimentation with dairy-based products previously considered niche. Japan and South Korea contribute through strong demand for premium and functional dairy products, including protein-enriched and probiotic cheese varieties. Expansion of cold-chain logistics, growth of e-commerce grocery platforms, and increasing presence of international foodservice brands collectively accelerate regional adoption of low fat cheese products.

Latin America

Latin America demonstrates steady growth led by Brazil and Mexico, where expanding urban populations and rising participation of women in the workforce are increasing demand for convenient and healthier food options. Growth of the processed food sector and expansion of fast-food chains are encouraging incorporation of reduced-fat cheese into packaged meals and snacks. Increasing exposure to western cuisines through media influence and international restaurant chains is gradually shifting consumer preferences toward cheese-based dishes, while improving retail infrastructure supports broader product accessibility across metropolitan areas.

Middle East & Africa

The Middle East & Africa region is experiencing gradual but consistent market expansion, with Saudi Arabia and the United Arab Emirates serving as primary growth centers. Strong reliance on dairy imports, combined with rapidly expanding hospitality and tourism industries, drives demand for low fat cheese within foodservice channels. Urbanization, population growth, and rising health awareness are encouraging consumers to adopt reduced-fat dairy products as part of balanced diets. Investments in modern retail development, increasing expatriate populations, and growing international restaurant presence further contribute to market growth, positioning the region as an emerging opportunity for global dairy exporters.

Key Players in the Low Fat Cheese Market

- Nestlé S.A.

- Danone S.A.

- Lactalis Group

- Arla Foods

- Fonterra Co-operative Group

- Saputo Inc.

- FrieslandCampina

- Dairy Farmers of America

- Bel Group

- Kraft Heinz Company

- Savencia Fromage & Dairy

- Amul (GCMMF)

- Meiji Holdings Co., Ltd.

- Yili Group

- Mengniu Dairy