Low-Calorie Meal Replacements Market Size

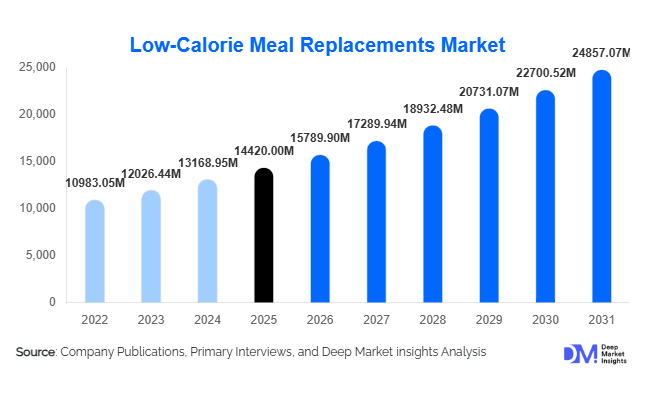

According to Deep Market Insights,the global low-calorie meal replacements market size was valued at USD 14,420 million in 2025 and is projected to grow from USD 15,789.90 million in 2026 to reach USD 24,857.07 million by 2031, expanding at a CAGR of 9.5% during the forecast period (2026–2031). The low-calorie meal replacements market growth is primarily driven by rising global obesity rates, increasing prevalence of diabetes and metabolic disorders, growing adoption of structured weight management programs, and strong consumer demand for convenient, portion-controlled nutrition solutions. The market has transitioned from traditional powdered dieting products to diversified ready-to-drink, plant-based, high-protein, and clinically supervised formulations, supported by digital health ecosystems and direct-to-consumer subscription models.

Key Market Insights

- Ready-to-drink (RTD) meal replacement shakes dominate the market, accounting for nearly 38% of total revenue in 2025 due to portability and improved taste profiles.

- Weight management consumers represent the largest target group, contributing approximately 46% of global demand.

- Plant-based formulations are the fastest-growing ingredient segment, holding nearly 29% of the 2025 market share.

- North America leads the global market, contributing about 36% of total revenue in 2025.

- Asia-Pacific is the fastest-growing region, expanding at over 11% CAGR through 2031.

- Online retail and direct-to-consumer channels account for over 32% of sales, driven by subscription-based nutrition models.

What are the latest trends in the low-calorie meal replacements market?

Shift Toward Plant-Based and Clean-Label Formulations

Consumers are increasingly demanding plant-based, dairy-free, and clean-label meal replacement products. Manufacturers are reformulating products using pea protein, soy isolates, oat blends, and rice protein to cater to vegan and lactose-intolerant populations. Clean-label positioning, minimal additives, and transparent ingredient sourcing are becoming critical differentiators. Organic-certified and non-GMO variants are gaining traction, particularly in North America and Europe. This shift is not only driven by dietary preferences but also by environmental sustainability concerns, encouraging companies to invest in plant-protein extraction and sustainable packaging solutions.

Digital Integration and Subscription Nutrition Models

Technology-enabled nutrition ecosystems are reshaping the competitive landscape. Companies are integrating AI-powered calorie calculators, metabolic tracking apps, and wearable-compatible platforms to personalize meal replacement plans. Subscription-based delivery models are increasing customer retention and lifetime value while reducing reliance on retail intermediaries. Direct-to-consumer brands are leveraging data analytics to optimize product bundling, dynamic pricing, and flavor innovation, creating recurring revenue streams and improving margin stability.

What are the key drivers in the low-calorie meal replacements market?

Rising Obesity and Metabolic Disorders

The global rise in obesity and type 2 diabetes is a primary structural driver of the market. Healthcare providers increasingly recommend calorie-controlled meal programs to manage weight and metabolic risk. Government-led awareness programs promoting calorie monitoring and portion control further support adoption. The growing medicalization of obesity treatment has expanded meal replacements beyond cosmetic dieting into structured therapeutic nutrition.

Convenience-Oriented Urban Lifestyles

Urbanization and time-constrained work patterns have accelerated demand for nutritionally balanced yet convenient food solutions. Ready-to-drink shakes and bars provide standardized calorie intake without meal preparation, making them attractive to working professionals, students, and fitness enthusiasts. Rising female workforce participation and dual-income households are further contributing to demand growth globally.

What are the restraints for the global market?

Perception of Processed Nutrition

Some consumers perceive meal replacements as overly processed or artificial, which limits adoption among health-conscious groups preferring whole foods. Manufacturers must address this challenge through transparent labeling, natural sweeteners, and clean-label reformulations.

Premium Pricing in Emerging Markets

High per-serving costs, particularly in premium and plant-based segments, restrict penetration in price-sensitive regions such as parts of Asia, Africa, and Latin America. Localized production and affordable SKU strategies are essential to improve accessibility.

What are the key opportunities in the low-calorie meal replacements industry?

Clinical and Medical Nutrition Expansion

Hospitals and medically supervised weight management programs increasingly incorporate low-calorie meal replacements for obesity treatment and bariatric surgery preparation. This segment offers higher margins and long-term institutional contracts. Insurance-backed wellness programs in developed markets are also integrating structured meal plans, creating predictable demand streams.

Emerging Market Penetration

Rapid urbanization in India, China, Indonesia, UAE, and Saudi Arabia presents strong growth potential. Rising middle-class income and increasing diabetes prevalence are creating new demand pockets. Establishing regional manufacturing facilities and culturally adapted flavor portfolios can unlock scalable growth opportunities.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 14420 Million |

| Market Size in 2026 | USD 15789.90 Million |

| Market Size in 2031 | USD 24857.07 Million |

| CAGR | 9.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Ready-to-drink (RTD) liquid shakes dominate the global market, accounting for approximately 38% of total revenue in 2025. The segment’s leadership is primarily driven by rising demand for convenience-oriented nutrition, particularly among urban professionals and time-constrained consumers seeking portion-controlled meal solutions. Advances in aseptic processing, Tetra Pak-style shelf-stable packaging, and improved flavor masking technologies have enhanced product palatability and extended distribution reach without refrigeration. Additionally, RTD formats benefit from strong visibility across supermarkets, fitness centers, and e-commerce platforms, reinforcing impulse purchases and subscription-based repeat buying.

Powdered meal replacements maintain a substantial market presence due to their affordability, customizable serving sizes, and multi-serve packaging formats that appeal to cost-sensitive consumers and households. The flexibility to adjust macronutrient density through blending with milk alternatives, fruits, or supplements further strengthens demand among fitness enthusiasts. Meal replacement bars are witnessing steady expansion, supported by crossover demand from sports nutrition and functional snacking categories. Their portability and long shelf life make them particularly attractive in travel retail and convenience channels. Meanwhile, savory soups and oatmeal-based meal replacements represent emerging niche segments, gaining traction among consumers seeking flavor diversity beyond sweet profiles and culturally adaptable meal formats.

Ingredient Composition Insights

Plant-based formulations represent nearly 29% of global market revenue in 2025 and are the fastest-growing segment, primarily driven by increasing vegan and flexitarian adoption, lactose intolerance prevalence, and sustainability-conscious purchasing behavior. Manufacturers are investing in pea, soy, oat, and rice protein blends to improve amino acid profiles and mouthfeel while reducing allergen concerns. Clean-label positioning and non-GMO certifications further strengthen consumer trust in this segment.

Dairy-based protein products continue to command a significant share owing to high protein bioavailability, complete amino acid composition, and long-standing consumer familiarity with whey and casein proteins. These formulations are particularly preferred in performance nutrition and medically supervised weight management programs. Keto-friendly and low-carbohydrate blends are expanding rapidly among metabolically focused consumers aiming to manage insulin response and promote fat oxidation. Simultaneously, fiber-enriched and probiotic-infused variants are increasingly marketed for digestive health benefits, satiety enhancement, and glycemic control, aligning with preventive healthcare trends.

Distribution Channel Insights

Online retail and direct-to-consumer platforms account for over 32% of total market revenue in 2025, emerging as the leading distribution channel due to subscription-based purchasing models, personalized nutrition algorithms, influencer-driven marketing campaigns, and targeted digital advertising. The ability to bundle products, offer auto-refill services, and collect consumer data for product optimization provides brands with a strong competitive advantage in this channel.

Supermarkets and hypermarkets remain critical for broad consumer reach and mass-market penetration, particularly across developed economies where organized retail infrastructure is mature. These outlets enable strong brand comparison, promotional bundling, and in-store sampling initiatives. Pharmacies and drug stores play an essential role in distributing clinically positioned and medically recommended formulations, particularly for diabetic and weight management consumers. Specialty nutrition stores and fitness centers continue to serve performance-driven buyers seeking high-protein, functional, or sports-specific meal replacements.

Target Consumer Insights

Weight management consumers dominate the global market with approximately 46% share in 2025, making this the leading demand segment. Growth is primarily fueled by rising obesity rates, increasing awareness of calorie-controlled diets, physician-supervised nutrition programs, and structured meal plans designed for sustainable weight reduction. The integration of meal replacements into intermittent fasting and portion-control strategies further supports segment expansion.

Sports and fitness users represent a rapidly growing secondary segment as consumers incorporate low-calorie, high-protein meal solutions into body recomposition, endurance training, and muscle recovery routines. Diabetic and pre-diabetic consumers are emerging as a high-growth demographic, driven by increasing global diabetes prevalence and greater emphasis on low-glycemic, balanced macronutrient dietary interventions recommended by healthcare professionals.

Explore more data points, trends and opportunities Download Free Sample Report

Low-Calorie Meal Replacements Market Segmentations

By Product Type

- Ready-to-Drink (RTD) Liquid Shakes

- Powdered Meal Replacement Shakes

- Meal Replacement Bars

- Low-Calorie Soups & Savory Meals

- Oatmeal & Porridge-Based Meal Replacements

By Calorie Band (Per Serving)

- Below 150 kcal

- 150–200 kcal

- 200–250 kcal

- Above 250 kcal (Structured Low-Calorie Meals)

By Ingredient Composition

- Dairy-Based Protein Formulations

- Plant-Based (Soy, Pea, Rice, Oat)

- Keto-Friendly / Low-Carb Blends

- High-Protein Functional Blends

- Fiber-Enriched & Digestive Support Formulations

By Target Consumer Group

- Weight Management Consumers

- Sports & Fitness Consumers

- Diabetic / Pre-Diabetic Consumers

- Busy Professionals / On-the-Go Consumers

- Senior Nutrition Segment

By Distribution Channel

- Online Retail & Direct-to-Consumer

- Supermarkets & Hypermarkets

- Pharmacies & Drug Stores

- Specialty Nutrition Stores

- Institutional & Clinical Sales

Regional Insights

North America

North America accounts for approximately 36% of the global market in 2025, with the United States contributing nearly 82% of regional revenue. Regional growth is driven by high obesity prevalence, strong diet culture adoption, widespread availability of structured commercial weight-loss programs, and advanced retail infrastructure. The strong presence of established nutrition brands, high disposable income, and rapid adoption of subscription-based online nutrition services further accelerate market expansion. Canada demonstrates steady growth supported by clean-label demand, plant-based product adoption, and increasing government initiatives promoting healthier eating habits.

Europe

Europe holds around 28% of global market share, led by Germany, the United Kingdom, and France. Regional growth is supported by stringent nutritional labeling regulations that enhance product transparency and consumer confidence. Demand for organic-certified, non-GMO, and sustainably sourced ingredients is driving premiumization across Western Europe. Rising geriatric populations seeking convenient nutrition solutions, along with growing awareness of preventive healthcare, further contribute to market expansion. While Western Europe remains the primary revenue generator, Eastern Europe is gradually emerging due to expanding retail networks and improving disposable income levels.

Asia-Pacific

Asia-Pacific represents roughly 24% of global demand in 2025 and is the fastest-growing region, registering a CAGR of over 11%. China leads regional consumption, followed by Japan, India, and Australia. Growth is primarily driven by rapid urbanization, rising middle-class income levels, increasing lifestyle-related diseases such as obesity and diabetes, and expanding digital commerce ecosystems. The proliferation of e-commerce platforms and mobile payment systems has significantly improved product accessibility. Additionally, growing adoption of Western dietary patterns and increasing participation in fitness activities are accelerating demand across metropolitan areas.

Latin America

Latin America accounts for nearly 5% of the global market, with Brazil and Mexico serving as the primary contributors. Regional growth is supported by expanding middle-class demographics, increasing health awareness campaigns, and rising obesity rates that encourage structured dieting practices. Improvements in modern retail penetration and cross-border e-commerce are enhancing product availability. However, price sensitivity remains a moderating factor, encouraging demand for affordable powdered formats.

Middle East & Africa

The Middle East & Africa region contributes approximately 7% of global demand. The United Arab Emirates and Saudi Arabia lead growth due to high diabetes prevalence, premium product demand, and expanding fitness culture supported by government-led wellness initiatives. In Africa, South Africa represents the largest and most developed market, benefiting from modern retail infrastructure and growing urban health awareness. Increasing expatriate populations and rising disposable incomes in Gulf Cooperation Council countries further strengthen regional market prospects.

Key Players in the Low-Calorie Meal Replacements Market

- Abbott Laboratories

- Herbalife Ltd.

- Nestlé S.A.

- Glanbia Plc

- Amway Corp.

- WW International Inc.

- Huel Ltd.

- SlimFast

- The Kraft Heinz Company

- Arla Foods

- Unilever

- GNC Holdings

- Orgain Inc.

- Nature’s Bounty

- Bayer AG