Low-Calorie Bulk Sweetener Market Size

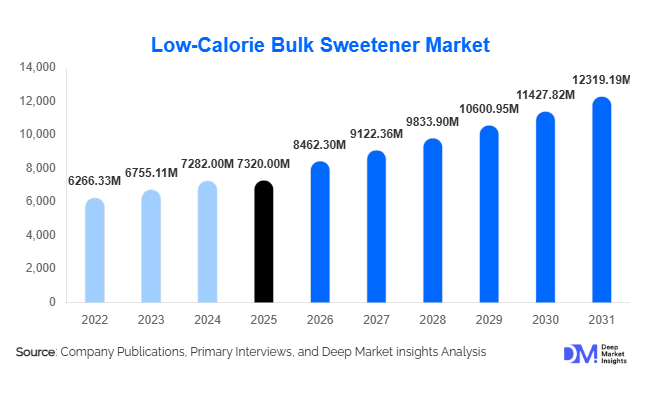

According to Deep Market Insights, the global low-calorie bulk sweetener market size was valued at USD 7,320 million in 2025 and is projected to grow from USD 8462.30 million in 2026 to reach USD 12319.19 million by 2031, expanding at a CAGR of 7.8% during the forecast period (2026–2031). Market growth is primarily driven by rising sugar-reduction regulations, increasing global diabetes prevalence, and strong demand for functional sugar substitutes across bakery, confectionery, beverages, pharmaceuticals, and nutraceuticals. Low-calorie bulk sweeteners, including polyols and rare sugars, provide sweetness along with critical bulking properties, making them essential in reformulation strategies where both texture and taste must be preserved.

Key Market Insights

- Sugar alcohols dominate the market, accounting for nearly 58% of the 2025 market share, driven by widespread use in confectionery, chewing gum, and baked goods.

- Rare sugars such as allulose are the fastest-growing segment, supported by keto and diabetic-friendly product innovation.

- North America leads global demand, contributing approximately 29% of the 2025 market value due to sugar taxation policies and strong functional food adoption.

- Asia-Pacific is the fastest-growing region, expanding at over 9% CAGR, led by China and India.

- Bakery & confectionery applications account for the largest share, representing nearly 34% of total demand.

- Direct industrial sales dominate distribution, comprising more than 70% of total transactions.

What are the latest trends in the low-calorie bulk sweetener market?

Rapid Commercialization of Rare Sugars

Rare sugars such as allulose and tagatose are transitioning from niche functional ingredients to mainstream sugar substitutes. Improved enzymatic conversion and fermentation technologies have reduced production costs, enabling broader commercial applications. Food manufacturers are increasingly incorporating rare sugars into reduced-sugar beverages, protein bars, and frozen desserts due to their near-sucrose taste profile and minimal glycemic impact. As clean-label demand strengthens, rare sugars are being positioned as premium, naturally derived alternatives to traditional polyols.

Expansion of Fermentation-Based Production Technologies

Technological advancements in microbial fermentation have enhanced erythritol and allulose yield efficiency, lowering production costs by 15–20% over the past five years. Investment in large-scale fermentation facilities, particularly in China and the United States, has significantly expanded global supply capacity. Manufacturers are also integrating carbon-neutral production processes and renewable energy sources to align with sustainability commitments, improving competitive positioning among multinational food brands.

What are the key drivers in the low-calorie bulk sweetener market?

Global Sugar Reduction Regulations

Governments worldwide are implementing sugar taxes and front-of-pack labeling regulations, compelling food and beverage manufacturers to reformulate products. These regulatory shifts have accelerated the replacement of sucrose with functional bulk sweeteners capable of maintaining product structure and taste. Beverage reformulation alone has significantly increased demand for erythritol and maltitol in North America and Europe.

Rising Diabetes and Obesity Prevalence

With more than 500 million adults globally living with diabetes, demand for low-glycemic and diabetic-friendly products continues to expand. Bulk sweeteners provide functional benefits without elevating blood glucose levels, making them ideal for medical nutrition, nutraceuticals, and specialty food categories. The growing popularity of ketogenic and low-carb diets further reinforces demand.

What are the restraints for the global market?

Gastrointestinal Tolerance Concerns

Excessive consumption of certain polyols can cause digestive discomfort, leading to mandatory labeling requirements in several regions. Such regulatory disclosures may influence consumer perception and limit usage levels in certain applications.

Raw Material and Energy Price Volatility

Fluctuating corn, wheat, and sugarcane prices directly impact production costs. Hydrogenation and fermentation processes are energy-intensive, and volatility in energy markets can compress manufacturer margins.

What are the key opportunities in the low-calorie bulk sweetener industry?

Expansion into Emerging Asian and Middle Eastern Markets

Rising urbanization and processed food consumption in India, Indonesia, Saudi Arabia, and the UAE are generating new demand pockets. Early investment in localized production facilities can provide long-term competitive advantages.

Integration with Functional and Nutraceutical Applications

The intersection of bulk sweeteners with gut-health products, protein supplements, and diabetic nutrition presents strong growth potential. Polyol-prebiotic blends and fiber-enriched sweetener systems are gaining commercial traction in premium food formulations.

Product Type Insights

Sugar alcohols dominate the market, accounting for 58% of the 2025 market share. The segment’s leadership is primarily driven by the growing demand for low-calorie bulk sweetening agents that closely replicate the functional properties of sucrose, including texture, mouthfeel, and moisture retention. Among sugar alcohols, erythritol leads due to its zero glycemic index, digestive tolerance advantages, and compatibility with keto, diabetic-friendly, and reduced-calorie formulations. Its ability to provide sweetness without blood glucose spikes makes it particularly attractive for health-focused product innovation.

Rare sugars represent a smaller but rapidly expanding segment, projected to witness double-digit growth. The leading growth driver for this segment is increasing clean-label adoption combined with rising consumer preference for naturally derived, minimally processed sweetening solutions. Improved production efficiencies and expanding commercialization are gradually enhancing cost competitiveness, supporting broader application adoption.

Bulk blends combining polyols and high-intensity sweeteners are gaining traction as manufacturers prioritize cost-effective reformulation strategies. These blends enable optimized sweetness profiles, caloric reduction, and improved taste masking, making them especially valuable for large-scale beverage and bakery reformulations responding to sugar reduction mandates.

Form Insights

Powdered and crystalline formats account for approximately 65% of the total market, supported by ease of storage, blending flexibility, transport efficiency, and extended shelf stability. The leading driver for this segment is its compatibility with large-scale industrial dry-mix processing systems, particularly in bakery, confectionery, and nutraceutical manufacturing. Powdered formats allow precise dosage control and consistent dispersion, making them the preferred choice for industrial buyers.

Liquid syrups are primarily used in beverage and pharmaceutical applications, where solubility and rapid incorporation are critical. These formats support ready-to-drink beverage reformulation and functional syrup-based applications. Granular and compressed formats serve specialty confectionery, table-top sweeteners, and controlled-dose applications, where portion convenience and consumer usability are key drivers.

Application Insights

Bakery & confectionery applications lead with 34% of total demand in 2025. The leading driver for this segment is the large-scale sugar replacement requirement in chocolates, chewing gums, candies, and baked goods, where maintaining bulk, sweetness, and texture is essential. Manufacturers increasingly rely on sugar alcohols to achieve reduced-calorie formulations without compromising product structure or sensory appeal.Beverages represent a high-growth segment, expanding at over 8% CAGR. Growth is primarily fueled by regulatory sugar reduction mandates, sugar taxes, and front-of-pack labeling regulations that compel beverage manufacturers to reformulate. The demand for zero-sugar carbonated drinks, flavored waters, and functional beverages continues to accelerate adoption.Pharmaceutical and nutraceutical uses are steadily gaining share, particularly in chewable tablets, syrups, lozenges, and gummy supplements. The key driver here is the need for non-cariogenic, low-glycemic excipients that enhance palatability while supporting patient compliance, especially in pediatric and diabetic-friendly formulations.

Distribution Channel Insights

Direct industrial sales dominate, accounting for nearly 72% of market transactions, as multinational food and beverage manufacturers prefer long-term supply contracts to secure pricing stability and consistent quality. The leading driver for this channel is the scale of procurement required for continuous reformulation initiatives across global product portfolios.Ingredient distributors play a critical role in serving mid-sized and regional manufacturers by offering technical support, flexible order volumes, and customized blending services. Contract manufacturing partnerships are emerging in developing regions, enabling local brands to access advanced sugar-reduction technologies without heavy capital investment.

| By Product Type | By Form | By Source/Feedstock | By Application | By Distribution Channel |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America holds approximately 29% of the 2025 global market share, led by the United States, which contributes nearly 80% of regional demand. Regional growth is primarily driven by strong sugar taxation policies, front-of-pack labeling initiatives, and widespread adoption of keto, low-carb, and diabetic-friendly diets. The presence of major multinational food manufacturers actively reformulating legacy brands further accelerates demand. Canada shows steady growth supported by health-conscious consumers, regulatory alignment with U.S. standards, and expanding nutraceutical production.

Europe

Europe accounts for nearly 26% of the global market. Regional growth is driven by stringent sugar reduction frameworks, public health initiatives targeting obesity, and structured sugar levies across multiple countries. The UK sugar levy has significantly accelerated beverage reformulation, while Germany and France lead industrial demand due to their advanced confectionery and processed food sectors. Eastern Europe is emerging as a competitive production hub, supported by lower manufacturing costs and increasing foreign direct investment in food processing infrastructure.

Asia-Pacific

Asia-Pacific is the fastest-growing region, expanding at over 9.2% CAGR. Growth is fueled by rising diabetes prevalence, rapid urbanization, expanding middle-class populations, and accelerating processed food consumption. China dominates both production and consumption, contributing more than 40% of regional demand, supported by large-scale polyol manufacturing capacity and export competitiveness. India is witnessing rapid growth due to expanding diabetic populations, increased health awareness, and significant expansion in domestic food processing and pharmaceutical manufacturing industries. Southeast Asia is also emerging as a reformulation hotspot due to growing beverage sector investments.

Latin America

Brazil and Mexico drive regional demand, supported by sugar taxation policies, front-of-pack warning labels, and increasing processed food exports. Mexico’s beverage reformulation initiatives have structurally increased polyol demand, particularly in carbonated drinks and flavored beverages. Brazil benefits from a large domestic food manufacturing base and growing demand for reduced-calorie confectionery products. Regional growth is further supported by improving retail penetration and rising consumer awareness regarding obesity and diabetes management.

Middle East & Africa

Saudi Arabia and the UAE represent major import markets due to rising obesity awareness, sugar reduction policies, and strong premium food demand. Regional growth is supported by government-led public health campaigns and increasing investments in domestic food processing infrastructure. Intra-regional consumption is gradually expanding as multinational brands localize production and introduce low-sugar product lines tailored to regional taste preferences. Africa shows early-stage growth potential, particularly in urban centers experiencing rapid dietary transitions.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Low-Calorie Bulk Sweetener Market

- Cargill Incorporated

- Archer Daniels Midland Company

- Ingredion Incorporated

- Tate & Lyle PLC

- Roquette Frères

- Mitsubishi Corporation Life Sciences

- Jungbunzlauer Suisse AG

- Tereos Group

- Gulshan Polyols Ltd

- Shandong Sanyuan Biotechnology Co.

- CJ CheilJedang Corporation

- Futaste Co., Ltd

- SPI Pharma

- BENEO GmbH

- Wilmar International Limited