Loose Leaf Tea Market Size

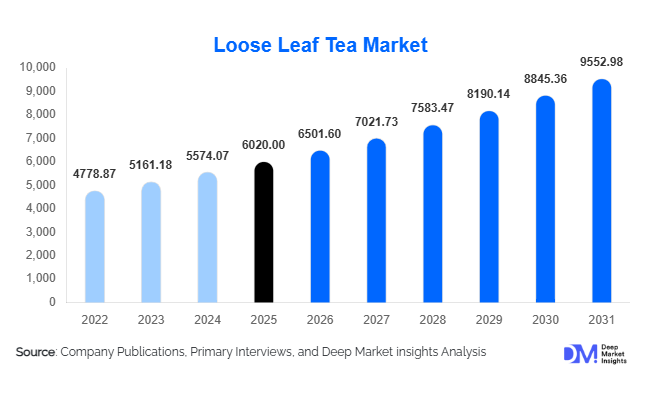

According to Deep Market Insights, the global loose leaf tea market size was valued at USD 6,020 million in 2025 and is projected to grow from USD 6,501.60 million in 2026 to reach USD 9,552.98 million by 2031, expanding at a CAGR of 8.0% during the forecast period (2026–2031). The loose leaf tea market growth is primarily driven by rising consumer preference for premium and minimally processed beverages, increasing health awareness, and growing demand for specialty tea experiences across households and foodservice environments. Premiumization trends, sustainability-focused sourcing practices, and the expansion of online direct-to-consumer tea brands are further accelerating global adoption of loose leaf tea products.

Key Market Insights

- Premium and specialty loose leaf tea consumption is expanding globally, driven by consumer interest in authentic flavors, origin transparency, and artisanal beverage experiences.

- Health and wellness trends are reshaping tea consumption patterns, positioning loose leaf tea as a natural alternative to sugary beverages and processed drinks.

- Asia-Pacific dominates global demand, supported by strong tea-drinking traditions and growing premium consumption in China and India.

- Online retail and subscription-based tea platforms are the fastest-growing distribution channels, enabling direct engagement between brands and consumers.

- Europe and North America are witnessing strong premiumization, with increasing demand for organic, single-origin, and functional tea blends.

- Sustainability and ethical sourcing initiatives are becoming critical purchasing factors influencing brand competitiveness worldwide.

What are the latest trends in the loose leaf tea market?

Premiumization and Origin-Based Tea Consumption

Consumers are increasingly shifting from mass-produced tea bags toward premium loose leaf varieties that emphasize origin authenticity and craftsmanship. Single-estate teas, terroir-based branding, and traceable supply chains are becoming central to product differentiation. Specialty tea retailers and boutique brands are highlighting regional characteristics such as Darjeeling, Assam, Japanese green tea, and Chinese oolong varieties to attract knowledgeable consumers. This trend has significantly increased average selling prices and strengthened the value-driven nature of the market. Premium packaging formats, storytelling-driven marketing, and curated tasting experiences are transforming loose leaf tea into a lifestyle product rather than a daily commodity beverage.

Functional and Wellness Tea Innovations

Functional blends incorporating botanicals, adaptogens, flowers, and natural ingredients are rapidly gaining traction. Consumers increasingly associate tea consumption with immunity support, stress reduction, and digestive health benefits. Wellness-focused blends targeting sleep improvement, relaxation, and metabolism support are expanding shelf presence in both online and specialty wellness stores. Brands are investing in research-backed formulations and clean-label positioning to meet evolving consumer expectations. The integration of herbal infusions alongside traditional tea varieties is broadening market appeal and attracting younger health-conscious demographics globally.

What are the key drivers in the loose leaf tea market?

Growing Health-Conscious Consumer Behavior

Rising awareness regarding preventive healthcare and natural nutrition is a major driver supporting loose leaf tea adoption. Consumers increasingly prefer beverages rich in antioxidants and polyphenols, positioning loose leaf tea as a healthier alternative to carbonated drinks and artificial beverages. The global wellness movement has strengthened demand across both developed and emerging economies, encouraging frequent at-home consumption and experimentation with diverse tea varieties.

Expansion of Specialty Retail and Café Culture

The rapid growth of specialty cafés and tea boutiques has elevated loose leaf tea into an experiential beverage category. Premium tea menus, tasting sessions, and education-driven retail formats are introducing consumers to brewing rituals and flavor appreciation. Hospitality operators are integrating curated tea offerings to diversify beverage menus, creating new demand channels beyond household consumption. Social media exposure and influencer-driven content further accelerate consumer curiosity and adoption.

What are the restraints for the global market?

Preparation Complexity Compared to Tea Bags

Loose leaf tea requires brewing equipment, preparation time, and product knowledge, which can limit adoption among convenience-focused consumers. Despite growing awareness, many consumers continue to favor tea bags and ready-to-drink beverages due to ease of use. Brands are attempting to overcome this restraint through educational marketing, simplified brewing accessories, and pre-measured packaging solutions.

Raw Material Price Volatility and Climate Dependency

Tea cultivation is highly dependent on climatic conditions, making production vulnerable to rainfall variability, temperature fluctuations, and labor shortages. Rising cultivation and compliance costs linked to sustainability standards can increase product pricing and affect profitability. Supply disruptions in major producing countries occasionally create pricing instability across global markets.

What are the key opportunities in the loose leaf tea industry?

Direct-to-Consumer Digital Expansion

E-commerce platforms and subscription-based tea services present strong growth opportunities for market participants. Direct-to-consumer models allow brands to build loyal communities while improving margins by reducing reliance on intermediaries. Personalized recommendations, curated monthly tea boxes, and digital storytelling enhance customer engagement and drive repeat purchases. Emerging brands particularly benefit from digital-first strategies that enable global market access with lower infrastructure investment.

Premium Demand Growth in Emerging Economies

Rising disposable incomes in countries such as India, China, Indonesia, and Gulf nations are shifting consumption toward premium beverage categories. Urban consumers increasingly seek higher-quality tea experiences, encouraging producers to invest in value-added processing and branding. Government export promotion initiatives and growing tea tourism further strengthen opportunities for premium loose leaf tea expansion worldwide.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 6020 Million |

| Market Size in 2026 | USD 6501.60 Million |

| Market Size in 2031 | USD 9552.98 Million |

| CAGR | 8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global loose leaf tea market demonstrates strong product diversification, with black loose leaf tea maintaining its leadership position by accounting for nearly 38% of total revenue share. The dominance of black tea is primarily supported by deeply rooted consumption traditions across South Asia, Europe, and the Middle East, where daily tea drinking remains culturally embedded. Its adaptability across flavor infusions, milk-based preparations, and regional blends allows manufacturers to maintain consistent demand across both premium and mass-market categories. Additionally, established global supply chains originating from major producing nations such as India and Sri Lanka ensure stable availability, reinforcing its commercial strength.Green tea represents the second-largest segment and continues to gain momentum due to growing consumer awareness surrounding preventive healthcare and natural antioxidants. Rising interest in metabolism support, detoxification, and plant-based wellness beverages has positioned green tea as a functional lifestyle product rather than a traditional beverage alone. Strong consumption growth in East Asia remains a foundational driver, while expanding adoption in North America and Europe reflects shifting preferences toward low-calorie and minimally processed drinks.Oolong, white, and pu-erh teas collectively represent premium and specialty segments experiencing accelerated growth. These categories benefit from increasing consumer curiosity toward artisanal beverages, provenance storytelling, and traditional processing techniques. Specialty tea retailers and digital education platforms have improved consumer understanding of flavor complexity and brewing rituals, enabling higher price realization and premiumization opportunities. Limited production volumes and perceived authenticity further elevate their appeal among affluent and enthusiast consumers.Herbal and botanical loose leaf blends are emerging as one of the most dynamic product categories within the market. Growth is largely driven by wellness-oriented consumers seeking caffeine-free alternatives that support relaxation, digestion, immunity, and stress management. Younger demographics are particularly attracted to innovative blends incorporating flowers, spices, and functional botanicals, expanding the category beyond conventional tea drinkers and increasing overall market penetration.

Application Insights

Household consumption remains the leading application segment, contributing approximately 57% of global demand, primarily driven by the rapid expansion of home brewing culture and consumer preference for personalized beverage experiences. Increased time spent at home, rising disposable income, and greater access to premium tea varieties through e-commerce platforms have encouraged consumers to experiment with loose leaf formats that offer superior freshness and flavor customization compared to packaged tea bags. The leading driver for this segment is the growing perception of loose leaf tea as a healthier and more authentic alternative to sugary beverages and processed drinks.The foodservice and hospitality sector is witnessing robust expansion as cafés, boutique tea houses, luxury hotels, and wellness resorts increasingly incorporate curated tea menus into their offerings. Experiential consumption trends, including tea tastings and ceremonial presentations, enhance customer engagement and enable establishments to differentiate their beverage portfolios. Premiumization within the global café culture further supports demand for specialty loose leaf varieties.Institutional consumption is gradually emerging as an additional growth avenue, particularly across corporate offices, coworking environments, and wellness-focused workplaces that promote healthier beverage choices among employees. Meanwhile, functional beverage manufacturers are integrating loose leaf tea extracts into premium ready-to-drink formulations, broadening application scope and enabling cross-category innovation within the global beverage industry.

Distribution Channel Insights

Online retail and direct-to-consumer platforms represent the fastest-growing distribution channel, accounting for nearly 28% of global sales. The leading driver of this segment is digital accessibility combined with consumer demand for education and product transparency. Online platforms allow brands to communicate origin stories, brewing techniques, and health benefits through content-driven marketing strategies, significantly improving consumer engagement and repeat purchases. Subscription models and personalized recommendations further strengthen customer retention while enabling niche brands to compete globally.Specialty tea stores continue to play a critical role in premium category expansion by offering sensory-driven retail experiences where consumers can explore aroma, texture, and flavor before purchase. These stores serve as important brand-building environments that reinforce product authenticity and craftsmanship.Supermarkets and hypermarkets maintain relevance by ensuring widespread accessibility and convenience, particularly in developing markets where organized retail penetration is increasing. At the same time, wellness stores and organic retailers are gaining importance as consumers increasingly prioritize clean-label products, sustainable sourcing practices, and ethically produced beverages aligned with holistic lifestyle choices.

End-Use Insights

Households remain the dominant end-use segment, supported by a global shift toward mindful consumption and wellness-oriented beverage habits. The primary driver for this segment is the increasing adoption of home-based premium beverage rituals, where consumers seek higher-quality ingredients and customizable brewing methods. Loose leaf tea aligns strongly with these preferences due to its perceived authenticity, freshness, and sensory richness.The foodservice sector represents the fastest-growing end-use category, fueled by evolving café concepts, premium dining experiences, and global tourism recovery. Restaurants and hospitality operators increasingly incorporate tea pairings, tasting flights, and ceremonial experiences to elevate customer engagement and enhance brand differentiation. Luxury hospitality brands, in particular, leverage curated tea experiences as part of wellness-focused service offerings.Industrial demand is also expanding through export-driven trade flows, with producing countries such as India and Sri Lanka supplying premium loose leaf varieties to Europe and North America. Growing international appreciation for origin-specific teas supports long-term trade expansion and encourages investments in quality improvement and sustainable cultivation practices.

Explore more data points, trends and opportunities Download Free Sample Report

Loose Leaf Tea Market Segmentations

By Product Type

- Black Loose Leaf Tea

- Green Loose Leaf Tea

- Oolong Loose Leaf Tea

- White Loose Leaf Tea

- Pu-erh Loose Leaf Tea

- Herbal & Botanical Loose Leaf Blends

By Application

- Household Consumption

- Foodservice & Hospitality

- Institutional Consumption

- Functional Beverage Manufacturing

By Distribution Channel

- Online Retail & E-commerce Platforms

- Specialty Tea Stores

- Supermarkets & Hypermarkets

- Wellness & Organic Retail Stores

- Direct-to-Consumer

Regional Insights

Asia-Pacific

Asia-Pacific leads the global loose leaf tea market with approximately 42% market share in 2025, supported by a combination of large-scale production capacity and deeply ingrained tea consumption traditions. China remains the largest producer and consumer, benefiting from centuries-old tea culture and strong domestic demand for green, oolong, and fermented teas. India continues to dominate global black tea exports while simultaneously experiencing premiumization trends among urban consumers seeking specialty and organic varieties. Japan contributes through high-quality green tea production supported by technological cultivation practices and strong domestic appreciation for functional beverages.Regional growth is primarily driven by rising disposable incomes, expanding middle-class populations, and increasing health awareness across emerging Southeast Asian economies. Rapid urbanization and the expansion of modern retail and e-commerce infrastructure further improve accessibility to premium tea products. Additionally, younger consumers are embracing specialty cafés and modern tea formats, blending traditional consumption habits with contemporary lifestyle trends, thereby accelerating market expansion across the region.

Europe

Europe accounts for nearly 26% of global demand, led by established tea-consuming nations including the United Kingdom, Germany, and France. Traditional tea-drinking culture in the UK continues to provide a stable consumption base, while Germany drives market expansion through strong adoption of herbal and wellness-oriented teas. European consumers demonstrate high sensitivity toward product quality, sustainability, and ethical sourcing, encouraging producers to adopt organic certifications and transparent supply chains.Regional growth is supported by increasing demand for premium and specialty beverages, rising interest in plant-based wellness products, and strong regulatory emphasis on sustainable agriculture. Premium packaging innovation and storytelling around origin and craftsmanship further enhance consumer engagement. The expansion of specialty tea boutiques and online premium marketplaces continues to strengthen Europe’s position as a high-value consumption region.

North America

North America represents one of the fastest-growing markets, led by the United States and Canada, where consumer preferences are rapidly shifting toward healthier beverage alternatives. Rising awareness of functional nutrition, combined with declining consumption of carbonated soft drinks, is encouraging adoption of loose leaf tea as a natural and customizable beverage option.Regional growth is strongly driven by e-commerce penetration, subscription-based tea services, and increasing interest in single-origin and artisanal products. Wellness trends, mindfulness practices, and premium lifestyle branding further support demand expansion. The growth of specialty cafés and independent tea brands has also contributed to consumer education, accelerating acceptance of loose leaf formats beyond traditional tea bags.

Latin America

Latin America is emerging as a promising growth region, with Brazil, Argentina, and Chile leading adoption trends. Increasing urbanization and expanding café culture are encouraging experimentation with premium beverages, including specialty teas. While coffee remains dominant across much of the region, rising health consciousness is gradually diversifying consumer beverage preferences.Regional growth is supported by improving retail infrastructure, rising middle-income populations, and growing exposure to global wellness trends through digital media. Younger consumers are increasingly exploring alternative beverages aligned with healthier lifestyles, although price sensitivity continues to shape purchasing decisions and encourages value-oriented product innovation.

Middle East & Africa

The Middle East and Africa region demonstrates a strong cultural affinity for tea consumption, making it an important demand center for loose leaf tea products. Countries such as the UAE, Saudi Arabia, and Morocco exhibit high per-capita tea consumption supported by longstanding social traditions and hospitality customs centered around tea serving.Regional growth is driven by rising disposable incomes, expanding luxury hospitality sectors, and increasing tourism activities that elevate demand for premium imported teas. The rapid development of high-end hotels and experiential dining concepts encourages adoption of specialty tea offerings. Additionally, strong intra-regional trade networks and growing consumer interest in premium and wellness beverages continue to support long-term market expansion across both urban Middle Eastern markets and developing African economies.

Key Players in the Loose Leaf Tea Market

- Tata Consumer Products Ltd.

- Unilever PLC

- Twinings (Associated British Foods plc)

- Dilmah Ceylon Tea Company PLC

- Harney & Sons Fine Teas

- DAVIDsTEA Inc.

- Teavana

- Kusmi Tea

- Mariage Frères

- Fortnum & Mason

- Ahmad Tea Ltd.

- Numi Organic Tea

- The Republic of Tea

- Rishi Tea & Botanicals

- Vahdam India