Lipid Nutrition Market Size

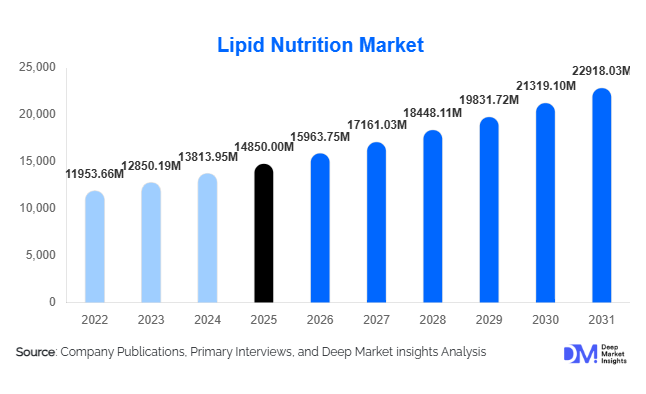

According to Deep Market Insights, the global lipid nutrition market size was valued at USD 14,850 million in 2025 and is projected to grow from USD 15,963.75 million in 2026 to reach USD 22,918.03 million by 2031, expanding at a CAGR of 7.5% during the forecast period (2026–2031). The lipid nutrition market growth is primarily driven by increasing demand for preventive healthcare solutions, rising awareness of cardiovascular and cognitive health, expanding infant nutrition fortification mandates, and the growing adoption of plant-based and algae-derived omega-3 ingredients.

Key Market Insights

- Omega-3 fatty acids dominate the market, accounting for nearly 48% of total revenue in 2025, driven by strong clinical validation in cardiovascular and cognitive health.

- Marine-based lipid sources lead globally, representing approximately 52% of the market, although algae-derived alternatives are expanding at a faster pace.

- Dietary supplements remain the largest application segment, contributing around 46% of total demand due to strong OTC and e-commerce penetration.

- North America holds the largest regional share (32%), supported by high supplement consumption and strong regulatory frameworks.

- Asia-Pacific is the fastest-growing region, expanding at over 8.5% CAGR, driven by rising middle-class populations in China and India.

- Technological advancements in microencapsulation and fermentation-based lipid production are reshaping product stability, bioavailability, and sustainability metrics.

What are the latest trends in the lipid nutrition market?

Shift Toward Algae and Fermentation-Based Omega-3

Sustainability concerns surrounding overfishing and marine ecosystem pressures are accelerating the adoption of algae-derived and microbial fermentation-based omega-3 oils. These alternatives offer consistent quality, reduced contamination risk, and vegan certification, making them highly attractive for infant formula, pharmaceutical-grade applications, and premium supplements. Investment in large-scale fermentation facilities in North America, Europe, and Asia is improving production scalability and reducing long-term cost volatility. The shift is also supported by growing regulatory scrutiny of marine sourcing practices and consumer preference for environmentally responsible products.

Microencapsulation and Functional Food Integration

Advanced microencapsulation technologies are enabling lipid fortification in mainstream food and beverage categories without oxidation or taste compromise. Omega-3 fortified dairy, bakery, RTD beverages, and plant-based foods are gaining traction globally. This trend is expanding lipid nutrition beyond capsules into daily-consumed staples, broadening the addressable market. Improved oxidative stability and shelf life are enhancing product acceptance among food manufacturers, while allowing brands to differentiate through health-focused claims.

What are the key drivers in the lipid nutrition market?

Rising Cardiovascular and Metabolic Health Awareness

The increasing global prevalence of cardiovascular disease, obesity, and metabolic disorders is significantly boosting omega-3 supplement demand. Clinical validation supporting triglyceride reduction and anti-inflammatory benefits has strengthened physician recommendations and pharmaceutical adoption. Aging populations in developed economies further reinforce long-term demand.

Growth in Infant and Clinical Nutrition

DHA and ARA inclusion in infant formula has become standard in many regulated markets. Rising birth rates in emerging economies and regulatory mandates supporting brain development fortification are expanding structured lipid demand. Clinical nutrition products using MCT oils and specialty lipids for hospital and recovery care are also contributing to stable, high-value growth.

What are the restraints for the global market?

Raw Material Price Volatility

Marine oil supply fluctuations due to climate events such as El Niño and fish stock variability create pricing instability. This impacts margins for manufacturers reliant on fish oil inputs and increases procurement risks across the value chain.

Regulatory and Health Claim Restrictions

Strict regulatory frameworks, particularly in Europe and North America, limit permissible health claims and increase compliance costs. Variations in standards across regions complicate product approvals and cross-border expansion strategies.

What are the key opportunities in the lipid nutrition industry?

Expansion in Emerging Markets

Rapid urbanization and growing middle-class populations in India, Southeast Asia, and Latin America are increasing supplement penetration. Localized manufacturing supported by government incentives is creating favorable entry points for new players.

Personalized and Preventive Nutrition Solutions

Integration of lipid nutrition into personalized health plans, supported by digital diagnostics and AI-driven supplementation models, is unlocking premium segments. Tailored omega-3 blends targeting cognitive health, sports recovery, and prenatal care are expanding niche applications.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 14850 Million |

| Market Size in 2026 | USD 15963.75 Million |

| Market Size in 2031 | USD 22918.03 Million |

| CAGR | 7.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Omega-3 fatty acids dominate the global lipid nutrition market, accounting for approximately 48% of total market revenue in 2025. The segment’s leadership is primarily driven by extensive clinical validation supporting cardiovascular, cognitive, prenatal, and anti-inflammatory benefits. Regulatory endorsements for EPA and DHA in heart health management, combined with increasing physician recommendations, have reinforced consumer trust and repeat purchase behavior. The pharmaceutical-grade omega-3 segment, particularly high-concentration EPA/DHA formulations (70%+), is expanding rapidly in developed markets due to rising prescription adoption for triglyceride management. Additionally, infant formula fortification mandates in multiple countries requiring DHA inclusion continue to structurally support long-term demand.

Medium-chain triglycerides (MCTs) represent one of the fastest-growing product categories, supported by increasing consumer adoption of ketogenic diets, sports nutrition products, and metabolic health supplements. The rapid rise of functional beverages and ready-to-mix powders incorporating MCT oil has significantly broadened its commercial footprint. Structured and specialty lipids, including phytosterols, conjugated linoleic acid (CLA), and customized designer lipids, are gaining traction in premium clinical and infant nutrition applications. These lipids command higher margins due to formulation specificity, regulatory-backed functionality, and growing demand for targeted therapeutic nutrition.

Source Insights

Marine-based lipids account for approximately 52% of total market revenue, maintaining dominance due to established global fish oil extraction and refining infrastructure concentrated in Norway, Peru, and Chile. The mature marine supply chain ensures consistent large-scale availability of EPA and DHA concentrates, particularly for pharmaceutical and infant nutrition applications. Strong aquaculture integration and vertically aligned processing facilities further enhance supply reliability.

However, plant-based and microbial sources are expanding at a faster CAGR compared to marine lipids. Sustainability concerns, fluctuating fish harvest volumes due to climate variability, and growing vegan consumer preferences are accelerating investment in algae-derived omega-3 production. Fermentation-based lipid manufacturing offers improved purity control, traceability, and scalability, reducing dependency on marine ecosystems. Significant capital expenditure in North America, Europe, and China toward fermentation facilities is expected to gradually rebalance the source mix over the forecast period.

Application Insights

Dietary supplements lead the application segment with approximately 46% of total demand, supported by a strong consumer shift toward preventive healthcare and self-directed wellness management. The rapid expansion of e-commerce platforms, subscription-based supplement models, and D2C nutraceutical brands has significantly increased accessibility and repeat consumption. Omega-3 capsules and softgels remain the highest-selling format within this category due to dosage precision and convenience.

Functional foods and beverages represent a high-growth segment driven by microencapsulation technologies enabling odor-free fortification. Infant nutrition remains structurally resilient due to DHA inclusion mandates in several countries. Pharmaceutical applications are expanding steadily, particularly in North America and Europe, where prescription omega-3 formulations are used in triglyceride management. Meanwhile, animal nutrition and aquaculture applications contribute significantly in the Asia-Pacific region, where lipid-enriched feed improves livestock productivity and aquaculture yields.

Distribution Channel Insights

B2B ingredient supply accounts for approximately 58% of total market revenue, reflecting the industry’s upstream-driven structure. Major lipid manufacturers primarily generate revenue through bulk refined oil sales to supplement brands, pharmaceutical companies, and infant formula manufacturers. This channel benefits from long-term supply contracts, regulatory compliance requirements, and economies of scale in refining and concentration.

Retail and e-commerce channels are expanding rapidly within the finished supplement category. Online sales growth is particularly strong in the U.S., China, and India, driven by digital health awareness campaigns and influencer-led marketing. Subscription-based wellness platforms and personalized nutrition programs are further accelerating retail channel expansion.

Explore more data points, trends and opportunities Download Free Sample Report

Lipid Nutrition Market Segmentations

By Product Type

- Omega-3 Fatty Acids

- Omega-6 Fatty Acids

- Omega-9 Fatty Acids

- Medium-Chain Triglycerides

- Structured & Specialty Lipids

By Source

- Marine-Based

- Plant-Based

- Microbial & Algae-Based

- Animal-Based

By Application

- Dietary Supplements

- Functional Foods & Beverages

- Infant Nutrition

- Clinical Nutrition

- Pharmaceuticals

- Animal Nutrition & Aquaculture

By Distribution Channel

- B2B Ingredient Supply

- Retail Pharmacies & Supermarkets

- E-commerce & Direct-to-Consumer

Regional Insights

North America

North America holds approximately 32% of the global lipid nutrition market, with the United States alone accounting for nearly 28% of global revenue. Regional growth is driven by high supplement penetration rates, widespread preventive healthcare awareness, and strong physician endorsement of omega-3 formulations. The presence of leading nutraceutical and pharmaceutical manufacturers enhances innovation and high-concentration product availability. Robust FDA regulatory oversight also strengthens consumer confidence in product quality and labeling. Additionally, strong e-commerce infrastructure and high disposable incomes support premium supplement adoption. Canada contributes through advanced omega-3 refining capacity and export-oriented production facilities.

Europe

Europe represents approximately 27% of global market demand, supported by stringent EFSA regulatory frameworks that reinforce product quality and scientific validation. Norway plays a dual role as both a leading fish oil exporter and regional supplier, benefiting from strong marine resource management. Germany, France, and the U.K. are key consumer markets, driven by aging populations and increasing cardiovascular health awareness. The region’s strong preference for sustainable and traceable ingredients is accelerating the adoption of algae-based lipids. Government support for sustainable aquaculture and bio-based manufacturing further strengthens Europe’s long-term growth outlook.

Asia-Pacific

Asia-Pacific accounts for nearly 29% of the global market and is the fastest-growing region, expanding at approximately 8.5% CAGR. China acts as both a major importer and refiner of crude fish oil, serving domestic supplement manufacturing and export markets. Rising middle-class income levels, expanding healthcare awareness, and strong demand for infant nutrition are key growth drivers. India is emerging as the fastest-growing national market, supported by rapid nutraceutical penetration and government initiatives encouraging domestic manufacturing. Japan maintains a strong demand for omega-3-enriched functional foods, supported by an aging population and high health-consciousness. Increasing aquaculture activities across Southeast Asia further stimulate lipid demand for feed applications.

Latin America

Latin America contributes approximately 6% of global revenue, led by Brazil and Mexico. Growth is primarily driven by expanding aquaculture production, increasing dietary supplement awareness, and improving retail distribution networks. Brazil’s strong livestock and aquaculture industries create additional demand for lipid-enriched feed ingredients. Rising middle-class consumption and greater urban health awareness are gradually expanding the human nutrition segment.

Middle East & Africa

The Middle East & Africa account for nearly 6% of global demand. The UAE and Saudi Arabia are leading premium supplement markets due to high per capita income and increasing lifestyle-related health concerns. Government investments in healthcare infrastructure and growing private hospital networks are improving clinical nutrition adoption. South Africa supports regional growth through both supplement consumption and localized production. Expanding retail chains and increasing online supplement penetration across the Gulf Cooperation Council (GCC) countries are further contributing to regional expansion.

Key Players in the Lipid Nutrition Market

- DSM-Firmenich

- BASF SE

- Croda International

- Cargill Inc.

- Aker BioMarine

- KD Pharma Group

- Polaris

- GC Rieber

- Epax

- ADM

- Wilmar International

- Omega Protein

- Kerry Group

- Corbion

- Novotech Nutraceuticals