Lighting Market Size

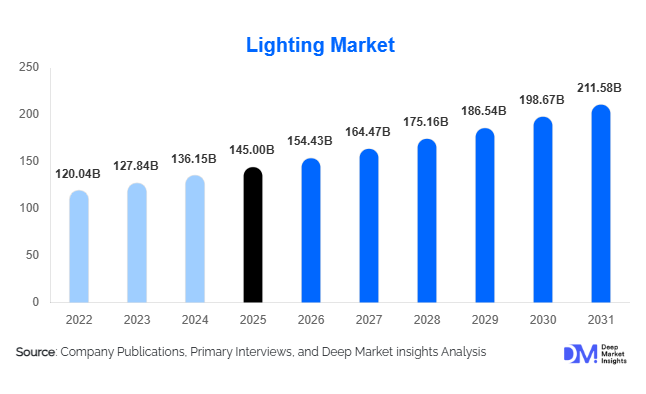

According to Deep Market Insights, the global lighting market size was valued at USD 145 billion in 2025 and is projected to grow from USD 154.43 billion in 2026 to reach USD 211.58 billion by 2031, expanding at a CAGR of 6.5% during the forecast period (2026–2031). The lighting market growth is primarily driven by the rapid transition toward energy-efficient LED technologies, increasing adoption of smart and connected lighting systems, and strong infrastructure development across emerging economies. Rising urbanization, government mandates to phase out inefficient lighting, and growing demand for sustainable solutions are accelerating market expansion globally.

Key Market Insights

- LED lighting dominates the global market, accounting for over 70% share due to superior energy efficiency and declining costs.

- Smart and connected lighting systems are rapidly gaining adoption, particularly in smart homes and urban infrastructure projects.

- Asia-Pacific leads the global market, driven by large-scale manufacturing and infrastructure investments in China and India.

- Retrofit and replacement projects account for the majority of installations, supported by global sustainability initiatives.

- The commercial sector remains the largest end-use segment, driven by demand from offices, retail, and hospitality industries.

- Emerging applications such as horticulture and healthcare lighting are creating new growth opportunities in niche segments.

What are the latest trends in the lighting market?

Smart Lighting and IoT Integration

The integration of IoT technologies into lighting systems is transforming the industry from traditional illumination to intelligent infrastructure. Smart lighting systems enable remote control, automation, energy optimization, and data analytics. Cities are increasingly deploying connected street lighting systems that integrate sensors for traffic monitoring, environmental tracking, and public safety. In residential and commercial spaces, smart lighting solutions are enhancing user experience through voice control, mobile applications, and adaptive lighting settings. This trend is also driving the development of interoperable platforms, although standardization remains a challenge. The growing adoption of wireless technologies such as Zigbee, Bluetooth, and Wi-Fi is further accelerating the deployment of connected lighting systems globally.

Human-Centric and Sustainable Lighting

Human-centric lighting, designed to mimic natural daylight patterns, is gaining traction across workplaces, healthcare facilities, and educational institutions. These systems improve productivity, well-being, and sleep patterns by aligning lighting conditions with human circadian rhythms. At the same time, sustainability remains a core focus, with manufacturers developing energy-efficient products and integrating recyclable materials into lighting systems. Governments and corporations are prioritizing green building certifications, further boosting demand for advanced lighting solutions. Carbon reduction targets and energy efficiency regulations are reinforcing the shift toward environmentally responsible lighting technologies, positioning sustainability as a long-term market driver.

What are the key drivers in the lighting market?

Energy Efficiency Regulations and LED Adoption

Governments worldwide are implementing stringent regulations to phase out inefficient lighting technologies, driving widespread adoption of LED solutions. LEDs offer significant energy savings, longer lifespan, and lower maintenance costs, making them the preferred choice across residential, commercial, and industrial applications. Subsidies, incentive programs, and bulk procurement initiatives are further accelerating the transition, particularly in developing regions.

Growth of Smart Cities and Infrastructure Development

The expansion of smart cities and infrastructure projects is a major driver for the lighting market. Public lighting systems are being upgraded to smart, energy-efficient solutions that enhance urban management and reduce operational costs. Investments in highways, railways, airports, and public utilities are driving demand for advanced lighting systems, particularly in the Asia-Pacific and the Middle East.

What are the restraints for the global market?

High Initial Investment Costs

Despite long-term cost benefits, the high upfront investment required for LED and smart lighting systems remains a key barrier, particularly in price-sensitive markets. Budget constraints in developing regions can delay adoption, especially for large-scale infrastructure projects.

Integration and Interoperability Challenges

The lack of standardization across smart lighting platforms creates integration challenges, limiting seamless deployment. Compatibility issues between different technologies and systems increase complexity and cost, acting as a restraint to widespread adoption of connected lighting solutions.

What are the key opportunities in the lighting industry?

Expansion of Smart and Connected Lighting

The growing adoption of IoT and digital infrastructure presents significant opportunities for smart lighting solutions. Companies can leverage this trend by offering integrated systems that combine lighting with automation, energy management, and data analytics. Smart city initiatives and intelligent building systems are expected to drive large-scale deployments.

Emerging Applications in Horticulture and Healthcare

Specialized lighting applications such as horticulture and healthcare are gaining traction. LED-based grow lights are essential for controlled-environment agriculture, supporting vertical farming and greenhouse operations. In healthcare, human-centric lighting is improving patient outcomes and staff productivity, creating new demand avenues.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 145 Billion |

| Market Size in 2026 | USD 154.43 Billion |

| Market Size in 2031 | USD 211.58 Billion |

| CAGR | 6.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

LED lighting is the dominant product segment, accounting for approximately 72% of the global market in 2025. This leadership position is primarily driven by strong regulatory support across major economies mandating the phase-out of inefficient lighting technologies, coupled with the superior energy efficiency and longer lifecycle of LED products. Governments across North America, Europe, and the Asia-Pacific have introduced subsidy programs, bulk procurement schemes, and minimum energy performance standards, accelerating LED penetration. Additionally, continuous technological advancements such as improved lumen efficiency, miniaturization, and cost reductions in semiconductor components have made LEDs more accessible across both developed and emerging markets. Conventional lighting technologies, including incandescent, halogen, and fluorescent lamps, are witnessing rapid decline due to environmental concerns and regulatory bans. Meanwhile, smart lighting systems are emerging as a high-growth sub-segment within LEDs, driven by increasing demand for connected, sensor-enabled, and automated lighting solutions. The transition toward integrated lighting ecosystems combining hardware, software, and controls is shifting the market from a product-centric to a solution-oriented model, further strengthening LED dominance.

Application Insights

Indoor lighting represents the largest application segment, accounting for nearly 60% of the global market, driven by strong demand from residential and commercial spaces. The leading position of indoor lighting is supported by rapid urbanization, expansion of office spaces, and growth in retail and hospitality sectors globally. Increasing construction of smart buildings and green-certified commercial infrastructure is further accelerating demand for energy-efficient indoor lighting systems. Offices, malls, hotels, and healthcare facilities are adopting advanced lighting solutions to enhance energy savings, occupant comfort, and aesthetics. Outdoor lighting, including street and roadway lighting, is witnessing robust growth due to government investments in infrastructure modernization and smart city projects. Large-scale deployment of LED streetlights in countries such as China and India is a major growth driver. Additionally, architectural and landscape lighting are gaining traction in urban redevelopment and tourism-focused regions, where aesthetic illumination plays a key role in enhancing public spaces. The rising adoption of solar-powered and energy-efficient outdoor lighting systems is also contributing to segment growth.

Distribution Channel Insights

Direct sales dominate the lighting market, accounting for approximately 55% of total revenue, primarily driven by large-scale infrastructure, commercial, and industrial projects. The leadership of this segment is attributed to the project-based nature of lighting demand in sectors such as construction, public utilities, and industrial facilities, where manufacturers engage directly with contractors, governments, and corporate clients. This channel enables customized solutions, bulk pricing, and long-term service agreements, making it the preferred route for high-value transactions. Retail channels continue to play a crucial role in residential lighting sales, particularly in developing markets where physical stores remain a key purchasing point. However, e-commerce platforms are rapidly gaining traction, driven by increasing digital adoption, wider product availability, and competitive pricing. Online channels are particularly popular for smart lighting products, where consumers seek product comparisons and reviews. Manufacturers are increasingly adopting omnichannel strategies, integrating offline and online sales to enhance customer reach and improve overall market penetration.

End-Use Insights

The commercial sector is the largest end-use segment, contributing around 35% of the global market in 2025. Its dominance is driven by high lighting intensity requirements in office buildings, retail outlets, hotels, and institutional facilities, where lighting plays a critical role in energy consumption and customer experience. The growing emphasis on energy efficiency, sustainability certifications (such as LEED), and smart building integration is further driving the adoption of advanced lighting systems in this segment. The residential sector is witnessing steady growth, supported by increasing urban population, rising disposable incomes, and growing adoption of smart home technologies. Consumers are increasingly opting for aesthetically appealing, energy-efficient, and connected lighting solutions. Industrial applications are focused on high-performance lighting systems that enhance operational efficiency, worker safety, and productivity, particularly in manufacturing and warehousing environments. Emerging segments such as horticulture lighting, driven by the expansion of vertical farming and controlled-environment agriculture, and automotive lighting are experiencing rapid growth, supported by technological innovation and expanding application scope.

Explore more data points, trends and opportunities Download Free Sample Report

Lighting Market Segmentations

By Product Type

- LED Lighting

- Conventional Lighting

- Smart Lighting Systems

By Application

- Indoor Lighting

- Outdoor Lighting

By Distribution Channel

- Direct Sales

- Retail Sales

- E-commerce Platforms

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global lighting market with approximately 42% share in 2025, making it the largest and fastest-growing regional market. China leads the region due to its strong manufacturing ecosystem, large-scale production capabilities, and significant domestic demand driven by urbanization and infrastructure expansion. India is emerging as a high-growth market, supported by government initiatives such as large-scale LED distribution programs and rural electrification schemes. Southeast Asian countries, including Indonesia, Vietnam, and Thailand, are also contributing to growth through rapid urban development and increasing electrification rates. Key drivers for regional growth include rising construction activities, favorable government policies promoting energy efficiency, and the presence of low-cost manufacturing hubs that support both domestic consumption and exports.

North America

North America accounts for around 22% of the global market, with the United States being the primary contributor. The region’s growth is driven by strong adoption of smart lighting technologies, extensive retrofit projects, and stringent energy efficiency regulations. Government policies aimed at reducing carbon emissions and improving building efficiency are accelerating the replacement of legacy lighting systems with LEDs. Additionally, the presence of advanced infrastructure, high consumer awareness, and early adoption of IoT-enabled lighting solutions are key growth drivers. Commercial and industrial sectors are major consumers, with increasing investments in smart buildings and automation systems further boosting demand.

Europe

Europe holds approximately 20% share of the market, led by Germany, France, and the UK. The region is characterized by stringent environmental regulations and ambitious sustainability targets, which are driving widespread adoption of energy-efficient lighting solutions. The European Union’s directives on energy performance and carbon reduction are major drivers for LED and smart lighting adoption. Retrofit projects are particularly prominent, as older infrastructure is upgraded to meet modern efficiency standards. Additionally, growing investments in smart city initiatives and green buildings are supporting market expansion. Consumer preference for sustainable and high-quality lighting products further strengthens demand in the region.

Middle East & Africa

The Middle East & Africa region is witnessing rapid growth, particularly in countries such as the UAE and Saudi Arabia. The market is driven by large-scale infrastructure projects, including smart cities, airports, and commercial complexes. Government-led initiatives such as Saudi Vision 2031 and urban development projects in the UAE are significantly boosting demand for advanced lighting systems. In Africa, increasing electrification rates and infrastructure development are creating new opportunities for lighting adoption. Key growth drivers include rising investments in construction, tourism infrastructure, and energy-efficient public lighting systems.

Latin America

Latin America is gradually expanding, with Brazil and Mexico leading the market. The region’s growth is driven by urbanization, infrastructure development, and increasing government focus on energy efficiency. Public lighting upgrade programs and the adoption of LED street lighting are key contributors to market growth. Economic recovery and rising construction activities are also supporting demand. Additionally, increasing awareness about energy savings and declining LED prices are encouraging adoption across residential and commercial sectors, positioning the region for steady long-term growth.

Key Players in the Lighting Market

- Signify N.V.

- Acuity Brands Inc.

- Zumtobel Group AG

- OSRAM GmbH

- Cree Lighting (Wolfspeed Inc.)

- Hubbell Incorporated

- Panasonic Corporation

- Samsung Electronics

- General Electric Company

- Eaton Corporation

- Nichia Corporation

- Sharp Corporation

- Havells India Ltd.

- Opple Lighting Co., Ltd.

- Fagerhult Group