Lentil Flour Ingredient Market Size

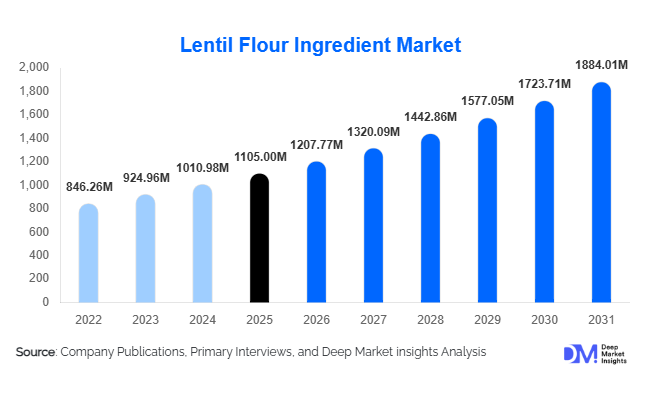

According to Deep Market Insights, the global lentil flour ingredient market size was valued at USD 1,105 million in 2025 and is projected to grow from USD 1207.77 million in 2026 to reach USD 1884.01 million by 2031, expanding at a CAGR of 9.3% during the forecast period (2026–2031). The lentil flour ingredient market growth is primarily driven by rising demand for plant-based protein, expanding gluten-free product penetration, and increasing adoption of clean-label functional ingredients across bakery, snacks, and meat alternatives.

Key Market Insights

- Plant-based protein adoption is accelerating globally, positioning lentil flour as a core ingredient in meat analogues and hybrid protein formulations.

- Gluten-free bakery applications account for the largest revenue share, supported by rising lifestyle-driven gluten-free consumption.

- North America dominates the global market, backed by strong plant-based innovation and large-scale pulse processing infrastructure.

- Asia-Pacific is the fastest-growing region, driven by expanding food processing capacity in India, China, and Australia.

- B2B industrial supply channels account for over 60% of sales, reflecting strong demand from food manufacturers.

- Technological advancements in precision milling and pre-gelatinization are improving texture functionality and expanding application scope.

What are the latest trends in the lentil flour ingredient market?

Rise of Functional & Clean-Label Reformulation

Food manufacturers are increasingly replacing synthetic emulsifiers, binders, and stabilizers with pulse-based alternatives. Lentil flour offers protein enrichment, fiber fortification, and binding capabilities within a single ingredient, making it highly attractive for clean-label reformulations. Shorter ingredient lists and regulatory scrutiny around artificial additives are accelerating this transition. Pre-gelatinized and instantized lentil flour variants are gaining traction in industrial baking and extruded snacks to improve texture consistency and processing stability.

Expansion in Alternative Protein Infrastructure

The rapid expansion of plant-based meat and dairy alternatives is significantly influencing lentil flour demand. Compared to soy and pea protein isolates, lentil flour offers a balanced amino acid profile and lower allergen risks. Hybrid protein systems incorporating lentil flour are increasingly adopted to improve mouthfeel and water-binding capacity. Investments in alternative protein hubs across North America and Europe are further strengthening ingredient-level demand.

What are the key drivers in the lentil flour ingredient market?

Growing Global Demand for Plant-Based Nutrition

The global shift toward vegetarian, vegan, and flexitarian diets is driving ingredient innovation. Lentil flour provides 22–26% protein content along with dietary fiber and micronutrients, making it ideal for fortified foods. Rising consumer awareness regarding sustainable protein sources is accelerating adoption across developed markets.

Gluten-Free Product Expansion

The gluten-free food category continues to expand beyond medical necessity into lifestyle consumption. Lentil flour serves as both a protein fortifier and structural substitute in gluten-free bakery and pasta formulations. Its mild flavor profile and superior blending properties enhance its industrial appeal.

What are the restraints for the global market?

Raw Material Price Volatility

Lentil production is highly dependent on climatic conditions in major producing countries such as Canada and Australia. Crop yield fluctuations can significantly impact pricing stability and processor margins.

Functional Limitations in Elastic Applications

Unlike wheat flour, lentil flour lacks gluten network formation, limiting its use as a standalone ingredient in certain bakery products. Manufacturers often require blending with other functional flours or hydrocolloids.

What are the key opportunities in the lentil flour ingredient industry?

High-Protein Snack & Extrusion Growth

Protein-fortified snacks and extruded products are expanding at double-digit rates globally. Lentil flour is increasingly incorporated into chips, puffs, and ready-to-eat extruded formats, presenting strong volume potential for ingredient suppliers.

Emerging Market Processing Infrastructure

Governments in India, Australia, and the Middle East are investing in pulse-processing clusters. Localization of milling facilities reduces logistics costs and supports export-driven growth, presenting expansion opportunities for both global and regional players.

Product Type Insights

Red lentil flour dominates the global lentil flour market, accounting for approximately 38% of the total market share in 2025. The leading position of red lentil flour is primarily driven by its mild flavor profile, uniform reddish-golden color, high protein retention, and excellent milling yield, making it highly suitable for bakery, snacks, pasta, and plant-based formulations. Its consistent functional performance in extrusion and baking applications further strengthens its adoption among industrial manufacturers.

Green and brown lentil flours collectively represent nearly 34% of the global share. These variants are widely utilized in specialty formulations, ethnic cuisines, and clean-label food products due to their distinctive flavor and higher fiber content. Their application is particularly strong in Mediterranean and Middle Eastern food categories.Yellow lentil flour is witnessing steady growth, particularly in Asian markets. Its expansion is supported by traditional culinary acceptance, compatibility with extruded snack products, and demand for protein-fortified staples. Increasing urbanization and convenience food consumption across Asia are accelerating its adoption.

Processing Type Insights

Conventional lentil flour holds nearly 72% of the global market share in 2025, driven by its cost efficiency, large-scale industrial availability, and strong demand from mass-market food processors. The leading segment driver for conventional processing is bulk procurement by multinational food manufacturers seeking cost-optimized protein enrichment solutions.Organic lentil flour, while comparatively smaller in volume, is expanding at a faster CAGR. Growth is primarily supported by rising demand for certified organic, non-GMO, and clean-label ingredients in North America and Europe. Premium pricing, regulatory certifications, and sustainability-focused branding strategies further enhance the segment’s value growth.

Functionality Insights

Protein enrichment applications account for approximately 41% of global demand, making it the leading functionality segment. The primary driver for this segment is the rapid expansion of plant-based protein products, including meat analogues, protein bars, fortified bakery items, and high-protein snacks. Lentil flour’s naturally high protein content and balanced amino acid profile make it an attractive alternative to soy and wheat proteins.Binding and texturizing functionalities are expanding significantly in plant-based meat systems, where lentil flour enhances moisture retention, emulsification stability, and structural integrity. Its role as a clean-label binder is increasingly preferred over synthetic additives.

End-Use Industry Insights

The Bakery & Confectionery segment leads the market with around 29% share in 2025. The leading driver for this segment is the growing demand for gluten-free, high-protein, and fiber-enriched baked goods. Lentil flour improves nutritional density while maintaining desirable texture in bread, cookies, cakes, and pastries.Plant-based meat and alternative protein applications represent the second-largest segment, supported by the global shift toward flexitarian and vegan diets. Snacks and extruded products are among the fastest-growing categories, fueled by increasing consumer preference for protein-enriched convenience foods.Infant nutrition and clinical nutrition applications are emerging niche segments, particularly in Europe, where lentil flour is incorporated into fortified formulations due to its digestibility and nutrient density.

Distribution Channel Insights

B2B direct supply dominates the distribution landscape with nearly 63% share. The leading driver for this channel is long-term procurement contracts between pulse processors and large-scale food manufacturers, ensuring stable supply chains and pricing efficiency.Ingredient distributors and private-label suppliers account for a significant portion of the remaining share, facilitating regional market penetration. Retail consumer packs, although smaller in comparison, are steadily expanding due to growing household adoption of gluten-free and plant-based cooking ingredients.

Form Insights

Fine-milled lentil flour leads with approximately 54% market share, driven by its superior blendability, smooth texture, and uniform particle size, which are critical for bakery, beverage mixes, and snack applications.Pre-gelatinized and instantized lentil flour forms are gaining traction in ready-to-eat and convenience food applications. Their growth is supported by improved hydration properties, faster processing times, and enhanced functional performance in instant formulations.

| By Product Type | By Processing Type | By Functionality | By End-Use Industry | By Distribution Channel |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America accounts for approximately 34% of the global market share in 2025, with the United States representing nearly 26% of global consumption. Regional dominance is driven by strong plant-based product innovation, advanced pulse processing infrastructure, increasing gluten-free product launches, and rising consumer focus on high-protein diets. Canada plays a strategic role as a major lentil producer and exporter, ensuring supply chain stability and raw material availability for domestic and international processors.

Europe

Europe holds around 27% share, led by Germany, France, and the UK. Regional growth is supported by strict sustainability regulations, carbon reduction goals, strong clean-label awareness, and growing demand for alternative proteins. The expansion of high-protein pasta, fortified baked goods, and meat substitutes is significantly contributing to market development. Government-backed initiatives promoting plant-based diets further accelerate adoption.

Asia-Pacific

Asia-Pacific is the fastest-growing region, expanding at over 11% CAGR. Growth drivers include rapid urbanization, rising middle-class income, increasing demand for protein-enriched snacks, and expanding food processing industries. India and Australia serve as major production hubs, while China and Japan are experiencing rising demand for convenience foods and fortified snack products. Traditional pulse consumption patterns also support long-term market expansion.

Latin America

Brazil and Mexico are emerging markets within the region. Growth is driven by expanding gluten-free food segments, increasing awareness of plant-based nutrition, and improving domestic food processing capabilities. Rising investments in local pulse cultivation and ingredient manufacturing are strengthening regional supply chains.

Middle East & Africa

The UAE and Saudi Arabia are key import-driven markets due to limited local pulse cultivation. Regional growth is supported by increasing health-conscious consumer trends, rising demand for high-protein bakery products, and expanding modern retail infrastructure. Growing expatriate populations and evolving dietary preferences further contribute to lentil flour adoption across the region.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Lentil Flour Ingredient Market

- AGT Food and Ingredients

- Ingredion Incorporated

- Archer Daniels Midland Company

- Bunge Limited

- Roquette Frères

- SunOpta Inc.

- Parrish & Heimbecker

- Vestkorn Milling AS

- Grain Millers Inc.

- Arbel Group

- Molino Rossetto

- Healthy Food Ingredients

- Best Cooking Pulses Inc.

- Anchor Ingredients

- Natural Products Inc.