Leafy Vegetable Market Size

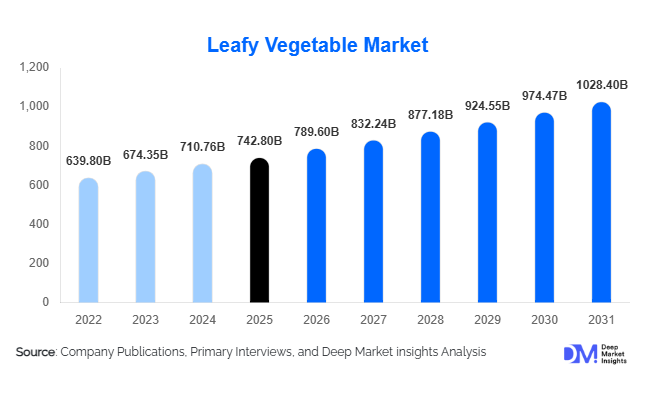

According to Deep Market Insights, the global leafy vegetable market size was valued at USD 742.8 billion in 2025 and is projected to grow from USD 789.6 billion in 2026 to reach USD 1,028.4 billion by 2031, expanding at a CAGR of 5.4% during the forecast period (2026–2031). Market expansion is primarily driven by rising health consciousness, increasing adoption of plant-based diets, urban demand for fresh and minimally processed foods, and rapid expansion of controlled-environment agriculture. Leafy vegetables—including lettuce, spinach, cabbage, kale, arugula, and indigenous greens—form a foundational component of global nutrition systems, benefiting from both staple consumption in developing economies and premium organic demand in developed markets.

The market demonstrates strong resilience due to daily consumption patterns and short production cycles that allow rapid supply adjustments. Growth is supported by expanding modern retail chains, improved cold-chain logistics, and digital agriculture technologies improving yield predictability. Emerging economies across Asia-Pacific and Africa are witnessing rising consumption due to population growth and dietary diversification, while North America and Europe are driving premiumization through organic, hydroponic, and pesticide-free produce. Foodservice recovery, growing salad culture, and demand from ready-to-eat meal industries further reinforce steady expansion. Additionally, sustainability-focused farming practices and urban vertical farming investments are reshaping supply chains, positioning leafy vegetables as a critical category within the global fresh produce ecosystem.

Key Market Insights

- Fresh leafy vegetables dominate consumption globally, supported by daily household usage and strong retail turnover cycles.

- Organic and hydroponically grown greens are expanding rapidly due to pesticide concerns and premium health positioning.

- Asia-Pacific leads global production and consumption, driven by China and India’s large agricultural base.

- Urban vertical farming adoption is accelerating, particularly in North America, Japan, and the Middle East.

- Foodservice and ready-to-eat salad industries are emerging as high-growth demand centers.

- Cold-chain modernization and export trade are enabling year-round global availability.

What are the latest trends in the leafy vegetable market?

Rise of Controlled Environment Agriculture (CEA)

Indoor farming, hydroponics, aeroponics, and vertical farming are transforming leafy vegetable production. Controlled environment agriculture enables year-round cultivation independent of weather variability while improving water efficiency by up to 90%. Retailers increasingly prefer consistent supply and standardized quality offered by indoor farms. Countries with limited arable land such as the UAE, Singapore, and Japan are investing heavily in vertical farming infrastructure, while North American startups are scaling automated greenhouse operations. These systems reduce pesticide use and shorten farm-to-consumer timelines, aligning with sustainability goals and urban food security initiatives.

Premiumization Through Organic and Functional Greens

Consumers are shifting toward nutrient-dense greens such as kale, arugula, microgreens, and spinach due to increased awareness of immunity and wellness. Organic certification and clean-label positioning allow producers to command premium pricing margins of 20–40% compared to conventional produce. Functional positioning—highlighting antioxidants, iron content, and digestive health benefits—is influencing purchasing decisions globally. Supermarkets are expanding packaged salad kits and mixed greens offerings, reflecting evolving urban lifestyles favoring convenience without compromising nutrition.

What are the key drivers in the leafy vegetable market?

Growing Health and Plant-Based Diet Adoption

Rising prevalence of lifestyle diseases has encouraged consumers to increase vegetable intake, particularly leafy greens known for micronutrients and fiber. Governments and health organizations worldwide promote vegetable-rich diets, boosting long-term demand. Vegan and flexitarian dietary trends are accelerating consumption across developed markets, while emerging economies see higher vegetable inclusion as incomes rise.

Expansion of Modern Retail and Cold Chains

Supermarkets, hypermarkets, and online grocery platforms are improving availability and freshness standards. Investments in refrigerated logistics reduce post-harvest losses—historically exceeding 25% in developing markets—thereby improving supply reliability and market scalability. Retail branding of packaged leafy vegetables further enhances consumer trust and encourages repeat purchases.

Technological Advancements in Farming

Precision agriculture tools including IoT sensors, AI-based irrigation systems, and climate-controlled greenhouses are improving yields and reducing production risks. These technologies enable consistent quality and predictable output, making leafy vegetables increasingly attractive for large-scale commercial farming operations.

What are the restraints for the global market?

High Post-Harvest Losses and Shelf-Life Constraints

Leafy vegetables are highly perishable, leading to significant wastage during transportation and storage. Limited cold infrastructure in developing regions increases operational costs and reduces farmer profitability.

Climate Variability and Water Dependency

Open-field cultivation remains vulnerable to extreme weather, droughts, and changing rainfall patterns. Water scarcity and rising irrigation costs present long-term challenges, especially in regions dependent on seasonal agriculture.

What are the key opportunities in the leafy vegetable industry?

Urban Farming and Localized Production

Urban vertical farms near consumption centers reduce logistics costs and carbon emissions. Governments promoting food security are incentivizing localized agriculture, creating opportunities for technology providers and agritech investors.

Export Expansion and Premium International Trade

Demand for fresh greens in Europe and the Middle East is increasing imports from Africa and Asia. Export-oriented farming supported by improved packaging and air freight logistics allows producers to access high-margin international markets.

Value-Added Processing and Ready-to-Eat Products

Pre-washed, chopped, and packaged salad mixes are witnessing strong growth. Food processors integrating leafy vegetables into smoothies, meal kits, and functional foods are creating new revenue streams beyond traditional fresh produce sales.

Product Type Insights

The global leafy vegetable market demonstrates strong diversification across product categories; however, lettuce varieties continue to dominate overall consumption patterns and commercial cultivation. Lettuce accounts for approximately 28% of total market share in 2025, supported by its versatility, short cultivation cycle, and widespread adoption across both household and foodservice applications. Its mild flavor profile and adaptability to multiple cuisines make lettuce a foundational ingredient in salads, sandwiches, wraps, burgers, and ready-to-eat meal kits. The rapid expansion of quick-service restaurant chains, urban cafés, and health-oriented dining concepts has further reinforced lettuce demand globally. Additionally, technological improvements in post-harvest handling and packaging have extended shelf life, enabling large-scale distribution through modern retail channels and international exports.Spinach represents one of the fastest-growing segments within the leafy vegetable category, driven primarily by rising consumer awareness regarding nutritional density and functional health benefits. Spinach is widely perceived as a superfood due to its high iron, vitamin K, folate, and antioxidant content, making it increasingly popular among health-conscious consumers, athletes, and plant-based diet adopters. Food manufacturers are integrating spinach into smoothies, frozen meals, soups, snacks, and fortified food products, expanding its application beyond traditional cooking. The growth of clean-label food trends and increasing demand for nutrient-rich ingredients in processed foods are accelerating spinach cultivation globally.Cabbage maintains a strong and stable market presence, particularly across Asia-Pacific and Eastern Europe, where it serves as a dietary staple. Its longer shelf life compared to delicate leafy greens provides logistical advantages for transportation and storage, making it highly suitable for export markets and regions with limited cold-chain infrastructure. Fermented cabbage products such as kimchi and sauerkraut continue to contribute to steady demand, supported by growing global interest in probiotic foods and gut health. The affordability of cabbage also ensures consistent demand among price-sensitive consumers and emerging economies.Kale, arugula, romaine blends, and specialty greens represent premium and rapidly expanding segments. These vegetables are strongly associated with wellness lifestyles, plant-based nutrition, and gourmet culinary experiences. Developed markets in North America and Europe have witnessed significant adoption of specialty greens due to consumer experimentation, rising disposable income, and the influence of social media-driven food trends. Retailers increasingly offer mixed salad packs and pre-washed greens, enhancing convenience and encouraging frequent consumption. The leading driver for specialty greens remains the growing consumer preference for nutrient-dense, minimally processed foods aligned with preventive healthcare trends.

Category Insights

Conventional leafy vegetables continue to dominate the global market, accounting for nearly 72% market share in 2025. Their leadership is primarily driven by affordability, large-scale agricultural productivity, and well-established supply chains that support consistent year-round availability. Conventional farming benefits from economies of scale, mechanized harvesting, and widespread adoption across developing economies where price sensitivity remains a key purchasing factor. Governments in major producing nations support conventional agriculture through subsidies, irrigation infrastructure, and rural development initiatives, ensuring stable production volumes.Despite the dominance of conventional produce, organic leafy vegetables represent the fastest-growing category globally. The primary driver behind this growth is rising consumer concern regarding pesticide residues, food safety, and environmental sustainability. Organic certification provides assurance of chemical-free cultivation practices, which appeals strongly to urban populations and higher-income consumer groups. Retailers are increasingly allocating premium shelf space to organic produce, while e-commerce grocery platforms enable direct-to-consumer distribution of certified organic greens.North America and Europe remain leading adopters of organic leafy vegetables due to strong regulatory frameworks and high consumer awareness regarding sustainable agriculture. Consumers in these regions demonstrate willingness to pay price premiums for traceability, ethical farming practices, and environmentally responsible production. Additionally, institutional buyers such as schools, hospitals, and corporate cafeterias are increasingly incorporating organic produce into procurement policies, further supporting market expansion. The leading growth driver for the organic segment is the convergence of health consciousness, environmental awareness, and premium retail positioning.

Farming Method Insights

Open-field farming dominates leafy vegetable production globally, contributing approximately 76% market share. This dominance stems from lower capital investment requirements, availability of agricultural land in major producing regions, and long-established farming expertise. Countries across Asia-Pacific, Latin America, and parts of Africa rely heavily on open-field cultivation due to favorable climatic conditions and cost-effective labor availability. The leading driver for this segment is production scalability, enabling growers to meet mass-market demand at competitive prices.However, controlled-environment agriculture, including greenhouse and hydroponic farming, is rapidly transforming the industry landscape. Urbanization, climate variability, and water scarcity are encouraging producers to adopt technologically advanced cultivation systems capable of delivering consistent yields independent of seasonal fluctuations. Hydroponic farming allows precise nutrient management, faster growth cycles, and significantly higher productivity per square meter compared to traditional farming methods.Greenhouse cultivation is expanding particularly in regions with extreme climates, where outdoor farming faces limitations. These systems reduce pesticide usage, improve quality consistency, and support year-round production, making them attractive to retailers demanding standardized supply. Investments in vertical farming and smart agriculture technologies are accelerating adoption in metropolitan areas, where proximity to consumers reduces transportation costs and post-harvest losses. The leading growth driver for controlled-environment farming is the need for climate-resilient, resource-efficient food production systems.

Distribution Channel Insights

Supermarkets and hypermarkets remain the dominant distribution channel, accounting for nearly 44% of global sales. Their leadership is supported by advanced cold storage infrastructure, centralized procurement systems, and long-term contracts with commercial growers. Large retail chains ensure consistent product availability, standardized packaging, and food safety compliance, which strengthens consumer trust. Promotional strategies, private-label brands, and ready-to-eat salad offerings further increase sales volumes within modern retail environments.Online grocery platforms represent the fastest-growing distribution channel, fundamentally reshaping fresh produce purchasing behavior. Digital retail adoption accelerated significantly with the rise of home delivery services and subscription-based fresh produce models. Consumers increasingly value convenience, doorstep delivery, and the ability to access farm-fresh vegetables through mobile applications. E-commerce platforms also enable direct farmer-to-consumer supply chains, improving producer margins while offering fresher products to buyers.Specialty stores and local markets continue to play an important role in emerging economies, where consumers prioritize freshness and daily purchasing habits. However, modernization of retail infrastructure and expansion of organized grocery chains are gradually shifting purchasing patterns toward structured distribution networks. The leading driver for distribution channel evolution is digital transformation combined with consumer demand for convenience and product traceability.

End-Use Insights

Household consumption dominates the leafy vegetable market, contributing approximately 63% of total market usage. Increasing awareness regarding balanced diets, preventive healthcare, and plant-based nutrition encourages daily consumption of leafy greens across households worldwide. Rising urban populations and growing middle-class income levels are further driving demand for fresh vegetables as part of routine meal preparation. The leading driver for household consumption is heightened health awareness supported by public nutrition campaigns and lifestyle shifts toward healthier eating habits.The foodservice sector represents the fastest-growing end-use segment, supported by rapid expansion of quick-service restaurants, casual dining chains, and healthy meal concepts. Restaurants increasingly feature salads, wraps, vegan dishes, and customizable bowls that rely heavily on fresh leafy vegetables. Globalization of culinary trends and increased dining-out frequency among urban consumers continue to expand commercial demand.Ready-to-eat meal manufacturers are emerging as significant buyers, integrating leafy greens into packaged salads, microwave meals, and convenience foods. Busy lifestyles and rising workforce participation rates have increased reliance on prepared meals that combine convenience with nutritional value. Export demand is also rising steadily, particularly from Gulf countries that depend on imported fresh produce due to limited arable land and water scarcity. Export-oriented cultivation provides new revenue streams for producers in Asia and Africa.

| By Product Type | By Category | By Farming Method | By Distribution Channel | By End Use |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

Asia-Pacific

Asia-Pacific accounts for nearly 46% of global market share in 2025, making it the largest regional market for leafy vegetables. The region’s dominance is primarily driven by high population density, vegetable-centric dietary traditions, and extensive agricultural production capacity. China leads both production and consumption due to its large farming base, strong domestic demand, and government initiatives supporting agricultural modernization. Leafy vegetables form an essential component of daily meals across Chinese cuisine, ensuring consistent consumption volumes.India represents one of the fastest-growing markets within the region, supported by rapid urbanization, expansion of organized retail chains, and increasing awareness of nutrition and wellness. Growth in supermarkets, online grocery platforms, and cold-chain logistics has improved accessibility to fresh greens in metropolitan areas. Rising disposable incomes and adoption of healthier lifestyles among younger consumers are further accelerating demand.Japan and South Korea contribute significantly to premium market growth through demand for packaged salads, specialty greens, and high-quality produce. Aging populations in these countries prioritize functional foods that support long-term health, driving consumption of nutrient-rich leafy vegetables. Regional growth is further supported by technological adoption, including smart farming and indoor cultivation systems designed to ensure consistent supply despite limited agricultural land. The primary regional growth driver in Asia-Pacific is the combination of population-driven demand and modernization of agricultural and retail infrastructure.

North America

North America holds approximately 18% market share, led by the United States and supported by strong consumer demand for fresh salads and organic produce. Health-conscious lifestyles, widespread adoption of plant-based diets, and increasing awareness of nutrition continue to drive leafy vegetable consumption across the region. Consumers increasingly prioritize fresh, locally sourced produce, encouraging investments in domestic cultivation systems.Controlled-environment agriculture is expanding rapidly across North America, with significant investments in greenhouse and vertical farming technologies. These systems enable year-round production, reduce dependency on imports, and improve supply chain stability. Retailers emphasize traceability and sustainability, encouraging growers to adopt environmentally responsible farming practices. The leading regional growth driver is innovation in agricultural technology combined with strong demand for organic and convenience-oriented fresh foods.

Europe

Europe represents approximately 20% of global market share, driven by strong consumer awareness regarding sustainability, food safety, and organic certification standards. Countries such as Germany, France, Italy, and the Netherlands lead consumption and production, supported by well-developed retail networks and stringent quality regulations. European consumers increasingly prefer locally grown produce with transparent sourcing, encouraging regional agricultural investments.The Netherlands serves as a global leader in greenhouse farming and acts as a major export hub for leafy vegetables across Europe. Advanced cultivation technologies allow efficient production despite limited land availability. Sustainability initiatives, including reduced pesticide usage and carbon footprint reduction targets, strongly influence purchasing decisions. The leading driver for European market growth is regulatory support for sustainable agriculture combined with rising organic consumption.

Middle East & Africa

The Middle East & Africa region is the fastest-growing leafy vegetable market globally, supported by increasing food import dependency and government-led agricultural diversification programs. Countries such as the United Arab Emirates and Saudi Arabia are investing heavily in hydroponic and indoor farming projects to enhance food security and reduce reliance on imports. Harsh climatic conditions and limited freshwater resources are accelerating adoption of controlled-environment agriculture.African nations including South Africa and Kenya play a crucial role as export-oriented producers supplying European and Middle Eastern markets. Favorable climates and competitive labor costs enable year-round cultivation of leafy greens for international trade. Rapid urban population growth and expansion of modern retail infrastructure are also increasing domestic consumption. The leading regional growth driver is food security initiatives combined with investment in water-efficient farming technologies.

Latin America

Latin America demonstrates steady market expansion, with Brazil and Mexico dominating regional demand. Urbanization, rising middle-class populations, and improving retail infrastructure are driving increased consumption of fresh vegetables. Traditional diets rich in vegetables support baseline demand, while growing health awareness is encouraging higher intake of leafy greens among younger consumers.Agricultural advantages such as favorable climates and abundant farmland support large-scale production, enabling both domestic supply and export opportunities. Investments in cold-chain logistics and supermarket expansion are improving distribution efficiency across the region. The leading driver for Latin American growth is expanding urban consumption supported by retail modernization and agricultural productivity improvements.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Leafy Vegetable Market

- Dole Food Company

- Fresh Del Monte Produce Inc.

- Taylor Farms

- Bonduelle Group

- Earthbound Farm

- Mann Packing Co.

- Greenyard NV

- Vegpro Group

- Church Brothers Farms

- Gotham Greens

- AeroFarms

- BrightFarms

- Driscoll’s (Fresh Greens Division)

- Mirak Group

- Costa Group Holdings