Larvicides Market Size

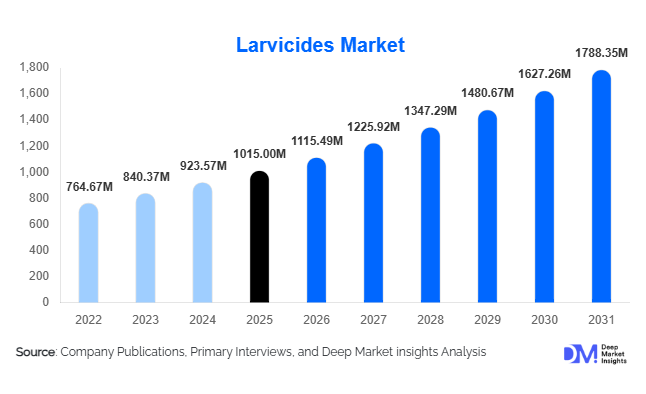

According to Deep Market Insights, the global larvicides market size was valued at USD 1,015 million in 2025 and is projected to grow from USD 1,115.49 million in 2026 to reach USD 1,788.35 million by 2031, expanding at a CAGR of 9.9% during the forecast period (2026–2031). Market growth is primarily driven by increasing incidences of vector-borne diseases, rising government investments in preventive public health programs, and growing adoption of environmentally safe biological larvicides. As climate change expands mosquito breeding habitats and urbanization increases stagnant water environments, larvicides are becoming a critical component of integrated vector management strategies worldwide.

Key Market Insights

- Biological larvicides are rapidly replacing conventional chemical solutions due to stricter environmental regulations and rising ecological awareness.

- Government procurement programs dominate global demand, accounting for the majority of larvicide purchases through public health tenders.

- Asia-Pacific leads global consumption, supported by large-scale mosquito control initiatives across India, China, and Southeast Asia.

- Africa represents the fastest-growing demand hub owing to malaria elimination programs funded by international health organizations.

- Technological advancements such as drone spraying and GIS-based surveillance are improving precision larvicide deployment.

- Slow-release formulations and microbial innovations are enabling longer treatment cycles and improved operational efficiency.

What are the latest trends in the larvicides market?

Shift Toward Biological and Eco-Friendly Larvicides

The global larvicides market is witnessing a structural transition toward biological formulations such as Bacillus-based microbial products and insect growth regulators. Regulatory restrictions on toxic pesticides and increasing environmental scrutiny have accelerated adoption of eco-safe alternatives. Municipal authorities increasingly prefer biological larvicides because they selectively target larvae while minimizing ecological impact on aquatic ecosystems. Manufacturers are investing heavily in fermentation technologies and biodegradable carriers to improve product efficacy and sustainability credentials. This trend is particularly strong in Europe and North America, where environmental compliance standards influence procurement decisions and favor low-toxicity solutions.

Precision Vector Control Through Technology Integration

Technology adoption is reshaping larvicide application practices. Drone-assisted spraying, satellite mapping, and AI-driven mosquito surveillance systems are enabling targeted treatment of breeding habitats. Smart monitoring platforms allow authorities to identify high-risk zones, reducing chemical usage and operational costs. Automated dosing systems and IoT-enabled water monitoring solutions are also gaining traction in urban infrastructure and industrial facilities. These innovations enhance treatment efficiency while supporting data-driven public health planning, creating new service-based business models where larvicide supply is integrated with monitoring and analytics solutions.

What are the key drivers in the larvicides market?

Rising Incidence of Vector-Borne Diseases

The increasing prevalence of dengue, malaria, chikungunya, and West Nile virus has significantly strengthened demand for preventive vector control measures. Governments are prioritizing larval-stage intervention as it offers cost-effective long-term disease mitigation compared to adult insecticide spraying. Expanding urban populations and changing climate patterns have amplified mosquito breeding conditions, reinforcing the need for consistent larvicide deployment programs worldwide.

Expansion of Integrated Vector Management Programs

Global health organizations advocate integrated vector management strategies combining environmental control, biological solutions, and surveillance technologies. Larvicides play a central role in these programs by disrupting insect life cycles early. Municipal authorities increasingly allocate dedicated budgets to larval control programs, ensuring recurring demand and long-term supply contracts for manufacturers.

What are the restraints for the global market?

Resistance Development Among Target Species

Prolonged use of certain chemical larvicides has resulted in resistance among mosquito populations in several regions. This reduces treatment effectiveness and requires continuous innovation in formulation chemistry. Companies must invest heavily in research and resistance management strategies, increasing development costs and regulatory complexity.

Funding Volatility in Developing Economies

Although disease burden is highest in emerging regions, procurement cycles often depend on international funding and donor-supported health programs. Budget delays or policy changes may temporarily slow larvicide adoption, creating demand variability across low-income markets.

What are the key opportunities in the larvicides industry?

Government-Led Preventive Healthcare Expansion

Countries worldwide are shifting from reactive outbreak management toward preventive public health systems. National mosquito control programs and urban sanitation initiatives are creating large-scale procurement opportunities for larvicide manufacturers. Multilateral health funding and disease elimination campaigns provide stable long-term demand pipelines.

Innovation in Biological and Slow-Release Formulations

Advancements in microbial technologies and controlled-release delivery systems are enabling longer treatment cycles and reduced application frequency. These innovations improve operational efficiency for municipalities and allow suppliers to command premium pricing. Companies investing in sustainable solutions are gaining competitive advantages as regulatory frameworks increasingly favor environmentally compliant products.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1015 Million |

| Market Size in 2026 | USD 1115.49 Million |

| Market Size in 2031 | USD 1788.35 Million |

| CAGR | 9.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global larvicides market is primarily led by biological larvicides, which account for nearly 48% of total market share in 2025. The dominance of this segment is driven by increasing regulatory restrictions on chemical pesticides, growing environmental awareness, and the need for sustainable vector control solutions. Biological larvicides, particularly Bacillus-based formulations such as Bacillus thuringiensis israelensis (Bti) and Bacillus sphaericus, are widely adopted in public health programs due to their species-specific targeting, minimal ecological impact, and safety for non-target organisms. Governments and international health organizations increasingly prioritize biologically derived solutions to align with integrated pest management (IPM) frameworks. Advancements in microbial fermentation technologies, improved shelf-life formulations, and expanded research investments are further strengthening this segment’s leadership position. Chemical larvicides continue to play a critical supporting role, especially in emergency outbreak situations requiring rapid knockdown effects, particularly across developing economies with high disease burdens. Meanwhile, botanical larvicides are emerging as an innovative niche category supported by growing consumer preference for plant-derived pest management solutions and ongoing innovation in natural extract stabilization technologies.

Application Insights

Mosquito larval control remains the leading application segment, contributing approximately 72% of global demand, primarily driven by the rising global incidence of mosquito-borne diseases such as malaria, dengue, chikungunya, and Zika virus infections. The leading driver for this segment is the expansion of government-led vector surveillance and prevention programs focused on reducing disease transmission at the larval stage, which is considered more cost-effective than adult mosquito control. Water body treatment and ground spraying continue to represent the most widely deployed application methods due to operational scalability, affordability, and suitability for urban and rural environments. Increasing urbanization has expanded the number of artificial breeding sites, including drainage systems, construction zones, and water storage infrastructure, further accelerating demand. Industrial applications are emerging as an important growth area as wastewater treatment facilities, manufacturing plants, and construction projects adopt preventive vector management practices to comply with occupational health and environmental regulations. Additionally, the adoption of automated dosing and smart water management systems in developed cities is enabling continuous larval monitoring and treatment, supporting long-term demand growth.

Distribution Channel Insights

Government procurement channels dominate the larvicides market, accounting for nearly 52% of global sales, reflecting the central role of public health agencies as primary purchasers. The leading driver for this segment is the expansion of national vector control programs funded through public budgets and international health partnerships, which rely on structured tender systems and long-term institutional contracts. These procurement mechanisms provide stable revenue visibility for manufacturers while ensuring large-scale deployment efficiency. Pest control service providers represent a rapidly expanding secondary channel as commercial establishments, residential communities, and hospitality sectors increasingly adopt preventive pest management strategies. Agrochemical distributors continue to facilitate market penetration in agricultural regions where irrigation systems create breeding habitats. Furthermore, digitalization is gradually transforming distribution dynamics, with online specialty platforms enabling small-scale buyers, private contractors, and municipal authorities to access specialized larvicide products more efficiently.

End-Use Insights

Public health authorities represent the largest end-use segment, accounting for approximately 46% of global consumption, primarily driven by nationwide disease prevention initiatives and international malaria elimination targets. The leading driver for this segment is sustained government investment in preventive healthcare infrastructure aimed at reducing healthcare costs associated with vector-borne diseases. Agriculture and irrigation systems are among the fastest-growing end-use sectors, as standing water environments in rice cultivation, canal systems, and irrigation reservoirs create ideal breeding conditions requiring proactive pest management. Livestock and aquaculture industries are increasingly deploying larvicides to minimize parasite transmission, improve animal welfare, and enhance productivity outcomes. Industrial end users, including mining operations, wastewater treatment facilities, oil and gas installations, and large infrastructure projects, are emerging contributors to market expansion due to stricter environmental compliance standards and workplace safety regulations that mandate vector control measures.

Explore more data points, trends and opportunities Download Free Sample Report

Larvicides Market Segmentations

By Product Type

- Biological Larvicides

- Chemical Larvicides

- Botanical/Plant-Based Larvicides

By Target Vector

- Mosquito Larvae

- Fly Larvae

- Midge Larvae

- Blackfly Larvae

- Other Aquatic Pest Larvae

By Formulation Type

- Liquid Formulations

- Granules

- Briquettes & Tablets

- Wettable Powders

- Slow-Release Formulations

By Application Method

- Ground Spraying

- Aerial Spraying

- Water Body Treatment

- Fogging Integration Programs

- Automated Dosing Systems

By End User

- Public Health Authorities & Municipalities

- Agriculture & Irrigation Systems

- Residential & Commercial Pest Control

- Industrial Facilities

- Livestock & Aquaculture Operations

By Distribution Channel

- Government Procurement Tenders

- Direct Institutional Sales

- Pest Control Service Providers

- Agrochemical Distributors

- Online & Specialty Retail

Regional Insights

North America

North America accounts for nearly 24% of the global larvicides market, supported by advanced public health infrastructure and highly organized mosquito abatement programs. The United States leads regional demand through well-established mosquito control districts that conduct continuous surveillance, habitat monitoring, and preventive larval treatment. Regional growth is driven by increasing climate variability extending mosquito breeding seasons, rising awareness of West Nile virus and other vector-borne diseases, and strong adoption of environmentally safe biological larvicides. Technological integration, including GIS-based surveillance and drone-assisted application methods, further enhances operational efficiency. Canada contributes through seasonal vector management programs emphasizing ecological conservation, wetland protection, and public safety initiatives.

Europe

Europe holds approximately 19% market share, largely driven by stringent pesticide regulations and sustainability policies encouraging biological larvicide adoption. Regional growth is supported by regulatory frameworks under environmental protection directives that limit chemical pesticide usage while promoting integrated pest management solutions. Countries such as France, Germany, Italy, and Spain increasingly implement urban ecological management strategies, wetland conservation programs, and climate adaptation policies addressing expanding mosquito habitats. Rising temperatures linked to climate change and the northward spread of invasive mosquito species are also increasing demand for preventive larval control solutions across both urban and rural environments.

Asia-Pacific

Asia-Pacific leads the global market with around 38% share in 2025 and represents the fastest-growing region, expanding at over 11% CAGR. Regional growth is primarily driven by high population density, favorable tropical climates, and recurring outbreaks of mosquito-borne diseases across countries such as India and China. Government-led sanitation initiatives, including urban cleanliness programs and vector surveillance campaigns, significantly support larvicide adoption. Rapid urbanization and infrastructure expansion are increasing stagnant water accumulation in construction zones and peri-urban areas, creating sustained demand. Additionally, expanding public healthcare investment, growing awareness campaigns, and increasing local manufacturing capabilities for biological larvicides are strengthening regional market development.

Latin America

Latin America accounts for roughly 12% of global demand, with Brazil and Mexico serving as major consumption hubs due to recurring dengue, Zika, and chikungunya outbreaks. Regional market growth is driven by continuous public health intervention programs, municipal vector control initiatives, and seasonal emergency response measures. Urban population growth, inadequate drainage infrastructure in certain metropolitan areas, and tropical climatic conditions contribute to persistent mosquito breeding risks. International funding support and cross-border disease surveillance collaborations further enhance larvicide deployment across the region.

Middle East & Africa

The Middle East and Africa region is experiencing rapid market expansion, supported by increasing investments in disease prevention and infrastructure development. African countries such as Nigeria and Kenya demonstrate strong demand growth driven by malaria elimination programs supported by global health organizations and donor-funded initiatives. In the Middle East, countries including Saudi Arabia are expanding larvicide usage to support public health safety during large-scale urban development and tourism projects. Rapid urbanization, water scarcity management systems, and growing awareness of preventive healthcare practices are key regional growth drivers. Improvements in healthcare access, expanding sanitation programs, and rising government collaboration with international agencies continue to accelerate larvicide adoption across the region.

Key Players in the Larvicides Market

- BASF SE

- Bayer AG

- Sumitomo Chemical Co., Ltd.

- Syngenta Group

- Valent BioSciences LLC

- Corteva Agriscience

- FMC Corporation

- Nufarm Limited

- UPL Limited

- Clarke Mosquito Control

- Central Life Sciences

- Rentokil Initial plc

- ADAMA Ltd.

- Koppert Biological Systems

- Russell IPM