Lactose-Free Protein Drink Market Size

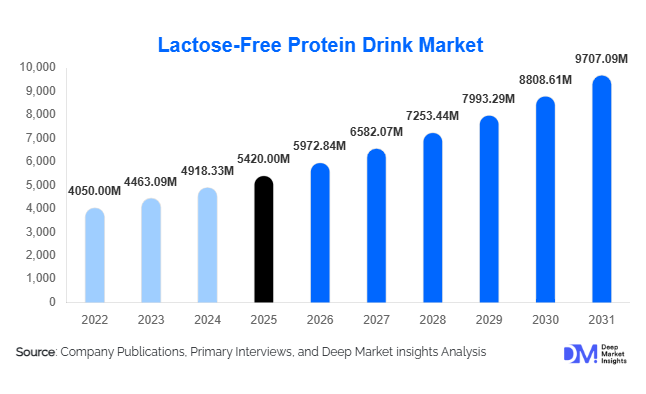

According to Deep Market Insights,the global lactose-free protein drink market size was valued at USD 5,420 million in 2025 and is projected to grow from USD 5,972.84 million in 2026 to reach USD 9,707.09 million by 2031, expanding at a CAGR of 10.2% during the forecast period (2026–2031). The lactose-free protein drink market growth is primarily driven by the rising prevalence of lactose intolerance, increasing adoption of high-protein diets, and the rapid expansion of the global sports nutrition industry. Consumers are increasingly seeking digestive-friendly protein beverages that deliver both nutritional value and convenience, leading to growing demand for ready-to-drink (RTD) lactose-free protein drinks. In addition, innovation in plant-based proteins such as pea, oat, and soy is further accelerating product development and market expansion across both developed and emerging economies.

Key Market Insights

- The market is witnessing strong demand for plant-based lactose-free protein beverages, driven by vegan and flexitarian dietary trends.

- Ready-to-drink protein beverages dominate global demand, offering convenience and consistent nutritional content for busy consumers.

- North America leads the market, supported by a mature sports nutrition industry and strong consumer awareness of high-protein diets.

- Asia-Pacific is the fastest-growing region, driven by high lactose intolerance rates and rising disposable incomes.

- Functional beverage innovation is accelerating with added ingredients such as probiotics, electrolytes, collagen, and adaptogens.

- E-commerce and direct-to-consumer sales channels are expanding rapidly, improving accessibility for specialty nutrition products.

What are the latest trends in the lactose-free protein drink market?

Plant-Based Protein Beverages Gaining Momentum

The shift toward plant-based nutrition is one of the most influential trends shaping the lactose-free protein drink market. Consumers increasingly prefer plant-derived proteins such as pea, soy, oat, and rice due to their sustainability, allergen-friendly profile, and compatibility with vegan lifestyles. Manufacturers are investing heavily in improving the taste, texture, and amino acid composition of plant protein beverages to make them comparable to traditional whey-based drinks. As a result, many beverage brands are launching blended protein formulations that combine multiple plant sources to deliver complete protein profiles while maintaining smooth flavor and texture.

Functional and Multi-Benefit Protein Drinks

Protein beverages are evolving from basic sports supplements to multifunctional wellness drinks. Manufacturers are incorporating additional health-promoting ingredients such as probiotics for gut health, collagen for skin and joint support, electrolytes for hydration, and adaptogens for stress management. These innovations are expanding the consumer base beyond athletes to include general wellness consumers, busy professionals, and aging populations seeking convenient nutrition solutions. Functional protein beverages are also commanding premium prices, allowing manufacturers to increase profit margins while differentiating their products in an increasingly competitive market.

What are the key drivers in the lactose-free protein drink market?

Growing Prevalence of Lactose Intolerance

Lactose intolerance affects a large portion of the global population, particularly in Asia, Africa, and Latin America. Consumers experiencing digestive discomfort from conventional dairy products are actively seeking lactose-free alternatives that still provide high-quality protein nutrition. Lactose-free protein drinks made from whey isolate or plant-based proteins offer a practical solution for individuals who require protein supplementation without digestive issues. Increasing awareness of lactose intolerance and the availability of lactose-free labeling are further accelerating consumer adoption worldwide.

Expansion of the Global Sports Nutrition Industry

The global sports nutrition industry is expanding rapidly due to increasing participation in fitness activities, bodybuilding, and recreational sports. Protein beverages are widely used by athletes and gym-goers to support muscle recovery and performance. Lactose-free formulations are particularly popular among fitness enthusiasts who prefer protein drinks that are easy to digest and rapidly absorbed. With the number of fitness centers, gyms, and wellness programs rising globally, demand for convenient protein beverages continues to grow.

What are the restraints for the global market?

High Production and Ingredient Costs

Lactose-free protein beverages often require premium ingredients such as whey protein isolate or specialized plant proteins, which are more expensive than standard dairy proteins. Additional processing technologies are also required to remove lactose or improve plant protein functionality. These factors increase manufacturing costs and lead to higher retail prices, which can limit adoption among price-sensitive consumers.

Taste and Texture Challenges in Plant-Based Formulations

While plant-based proteins offer clear health and sustainability benefits, they can present formulation challenges related to flavor, texture, and solubility. Some plant proteins may produce a grainy mouthfeel or undesirable aftertaste, which can affect consumer acceptance. Manufacturers must invest significantly in research and development to improve sensory characteristics and maintain competitive product quality.

What are the key opportunities in the lactose-free protein drink industry?

Growth of Functional Wellness Beverages

The rapid expansion of the functional beverage industry presents major opportunities for lactose-free protein drink manufacturers. Consumers increasingly demand beverages that provide multiple health benefits beyond basic nutrition. By integrating ingredients such as vitamins, minerals, probiotics, and adaptogens, companies can position lactose-free protein drinks as comprehensive wellness solutions rather than simple sports supplements. This strategy allows brands to enter new consumer segments and increase product value.

Rising Demand in Emerging Markets

Emerging economies across Asia-Pacific and Latin America present significant growth potential for lactose-free protein drinks. Countries such as China, India, Brazil, and Indonesia have high lactose intolerance rates and rapidly expanding fitness cultures. Rising disposable incomes and urbanization are enabling consumers in these regions to spend more on health and wellness products. Establishing localized manufacturing and developing region-specific flavors can help companies capture market share in these fast-growing markets.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5420 Million |

| Market Size in 2026 | USD 5972.84 Million |

| Market Size in 2031 | USD 9707.09 Million |

| CAGR | 10.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Protein Source Insights

Plant-based proteins are the dominant force in the lactose-free protein drink market, capturing nearly 41% of global revenue in 2025. The surge in demand for plant-based formulations is fueled by increasing adoption of vegan and flexitarian diets, growing consumer awareness of environmental sustainability, and the pursuit of cleaner label products. Pea protein and soy protein are particularly popular due to their well-balanced amino acid profiles and functional properties that enhance texture and solubility in beverages. Dairy-based lactose-free proteins, such as whey protein isolate, continue to play a significant role, especially in sports nutrition, where rapid absorption and high protein quality are essential for muscle recovery and performance enhancement.

Product Type Insights

Ready-to-drink (RTD) lactose-free protein beverages remain the largest product segment, accounting for approximately 58% of global market share in 2025. The convenience, portability, and consistent nutritional content of RTD products make them highly preferred by busy consumers. Protein shakes and smoothies maintain robust demand among fitness enthusiasts and athletes for post-workout recovery and muscle building. Emerging clear protein beverages are gaining traction as a lighter, refreshing alternative to traditional creamy shakes, appealing to consumers who seek high-protein drinks with lower viscosity and improved taste experience.

Distribution Channel Insights

Supermarkets and hypermarkets are the dominant distribution channels, representing around 36% of total global sales. These outlets offer extensive product visibility and easy accessibility, making them a preferred choice for mainstream consumers. Meanwhile, online retail channels are experiencing rapid growth, driven by the convenience of e-commerce, detailed product information, and home delivery. Direct-to-consumer subscription models are also becoming increasingly popular, allowing brands to foster deeper consumer relationships, provide personalized offerings, and collect valuable insights into purchasing behavior and preferences.

Consumer Category Insights

Sports and fitness consumers constitute the largest segment, accounting for approximately 39% of the global market in 2025. This segment includes athletes, bodybuilders, and gym-goers who regularly consume protein beverages for muscle recovery, endurance, and performance enhancement. The general wellness category is expanding as consumers integrate protein drinks into daily diets for energy, weight management, and overall health. Additionally, the senior nutrition segment is emerging as a key growth area, driven by an aging population seeking convenient protein sources to maintain muscle mass, support bone health, and promote healthy aging.

Explore more data points, trends and opportunities Download Free Sample Report

Lactose-Free Protein Drink Market Segmentations

By Protein Source

- Plant-Based Protein

- Whey Protein Isolate

- Casein Protein

- Blended Protein Formulations

By Product Type

- Ready-to-Drink (RTD) Protein Beverages

- Protein Shakes

- Protein Smoothies

- Clear Protein Drinks

By Distribution Channel

- Supermarkets and Hypermarkets

- Convenience Stores

- Online Retail / E-Commerce

- Health and Nutrition Stores

- Pharmacies and Drugstores

By Consumer Category

- Sports and Fitness Consumers

- General Wellness Consumers

- Clinical Nutrition Consumers

- Senior Nutrition Segment

Regional Insights

North America

North America leads the global lactose-free protein drink market, accounting for approximately 34% of global revenue in 2025. The United States is the largest contributor, propelled by high consumer awareness of protein-rich diets, a mature sports nutrition market, and widespread health-conscious behaviors. Canada is also a significant market, driven by growing interest in digestive health, plant-based nutrition, and robust retail networks. Factors such as increasing fitness club memberships, rising demand for functional beverages, and ongoing product innovation are further supporting regional growth.

Europe

Europe holds the second-largest share of the market at around 27% globally. Key countries including Germany, the United Kingdom, France, and the Netherlands are driving demand for lactose-free protein beverages. The rise of plant-based diets, heightened focus on digestive health, and increased adoption of sports and wellness nutrition are primary market drivers. Additionally, strong government support for nutritional labeling, coupled with well-established retail and e-commerce infrastructure, is fostering growth across Western and Northern European markets.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, supported by high lactose intolerance rates and rapid expansion of the middle-class population. Major markets include China, Japan, India, and South Korea, where increasing health and fitness awareness, rising disposable incomes, and rapid urbanization are fueling demand for functional beverages. The expansion of modern retail infrastructure, greater availability of international brands, and the growing popularity of protein-enriched diets are additional factors driving market growth across the region.

Latin America

Latin America is gradually emerging as an important market for lactose-free protein drinks. Brazil and Mexico are the leading markets, supported by expanding fitness culture, growing interest in sports nutrition, and increased consumer spending on health and wellness products. The region benefits from improving retail distribution networks, growing e-commerce penetration, and rising disposable incomes, which collectively drive adoption of lactose-free protein beverages.

Middle East & Africa

The Middle East and Africa region is witnessing steady growth in demand for lactose-free protein drinks. Key markets include the United Arab Emirates, Saudi Arabia, and South Africa, where rising health consciousness, increasing participation in fitness activities, and the influence of global nutrition trends are significant drivers. Additionally, the expansion of modern retail outlets, growing penetration of imported functional beverages, and increasing awareness of plant-based nutrition are contributing to the region’s market development.

Key Players in the Lactose-Free Protein Drink Market

- Nestlé S.A.

- PepsiCo Inc.

- The Coca-Cola Company

- Danone S.A.

- Abbott Laboratories

- Glanbia plc

- Orgain Inc.

- Huel Ltd.

- Oatly Group AB

- Ripple Foods

- Soylent Nutrition Inc.

- Arla Foods

- Herbalife Nutrition Ltd.

- BellRing Brands Inc.

- Garden of Life LLC