Lactose Free Milk Market Size

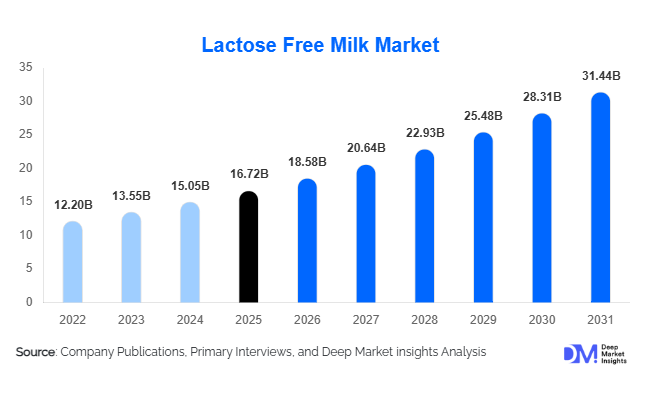

According to Deep Market Insights,the global lactose free milk market size was valued at USD 16.72 billion in 2025 and is projected to grow from USD 18.45 billion in 2026 to reach USD 31.44 billion by 2031, expanding at a CAGR of 11.1% during the forecast period (2026–2031). The lactose free milk market growth is primarily driven by the increasing prevalence of lactose intolerance globally, rising consumer awareness regarding digestive health, and the growing demand for functional dairy products that provide nutritional benefits without causing gastrointestinal discomfort.

Lactose free milk is produced by adding lactase enzymes that break down lactose into easily digestible sugars. This allows consumers who experience lactose intolerance to continue consuming dairy products while avoiding digestive complications. As global dietary habits evolve and consumers increasingly prioritize gut health, lactose free milk has emerged as a popular alternative to conventional dairy milk.

The expansion of modern retail channels, improved dairy processing technologies, and the introduction of flavored and fortified lactose free milk products are also contributing to market expansion. Manufacturers are launching innovative variants enriched with calcium, vitamins, and high-protein formulations to attract health-conscious consumers. Furthermore, the rapid growth of specialty beverage chains, cafés, and foodservice outlets offering lactose free milk options is broadening market adoption across both developed and emerging economies.

Key Market Insights

- Rising lactose intolerance prevalence worldwide is significantly increasing demand for lactose free dairy products across both developed and emerging markets.

- Functional dairy innovation is expanding rapidly, with manufacturers introducing fortified, high-protein, and flavored lactose free milk products targeting health-conscious consumers.

- North America dominates the lactose free milk market due to strong consumer awareness and widespread availability across retail channels.

- Asia-Pacific is the fastest-growing region, supported by high lactose intolerance prevalence and rising disposable incomes in countries such as China and Japan.

- Supermarkets and hypermarkets remain the leading distribution channels, accounting for a significant share of global lactose free milk sales.

- Technological advancements in enzyme processing and ultra-filtration are improving taste, shelf life, and production efficiency.

What are the latest trends in the lactose free milk market?

Growth of Functional and Fortified Dairy Products

Consumers are increasingly seeking dairy products that offer additional health benefits beyond basic nutrition. This trend has encouraged manufacturers to develop lactose free milk variants enriched with vitamins, calcium, omega-3 fatty acids, and protein. Functional dairy products are becoming particularly popular among urban consumers, athletes, and health-conscious individuals who want the nutritional benefits of milk without digestive discomfort. Fortified lactose free milk is also being promoted as a suitable option for children and elderly consumers who require enhanced calcium and vitamin intake. As consumer interest in wellness-oriented nutrition continues to grow, the functional dairy segment is expected to remain a major trend shaping the lactose free milk industry.

Expansion of Lactose Free Options in Foodservice and Coffee Chains

Foodservice operators, including cafés and specialty coffee chains, are increasingly offering lactose free milk as an alternative dairy option for beverages. Lactose free milk retains the natural taste and texture of traditional milk, making it ideal for cappuccinos, lattes, milkshakes, and desserts. Coffee chains and bakeries are expanding their beverage menus to include lactose free milk options, catering to consumers with dietary sensitivities. This trend is particularly prominent in North America, Europe, and urban Asia-Pacific markets where café culture continues to grow rapidly.

What are the key drivers in the lactose free milk market?

Growing Awareness of Digestive Health

Consumers worldwide are becoming increasingly aware of digestive health and food sensitivities. Lactose intolerance affects a significant portion of the global population, particularly in Asia, Africa, and Latin America. As awareness grows regarding the symptoms associated with lactose intolerance, many consumers are switching to lactose free dairy products that allow them to enjoy milk without digestive discomfort. Health campaigns and nutrition education programs are further supporting the adoption of lactose free milk products across global markets.

Product Innovation and Retail Expansion

Continuous innovation within the dairy industry is playing a major role in driving lactose free milk market growth. Manufacturers are introducing flavored variants such as chocolate and vanilla lactose free milk to attract younger consumers. At the same time, improvements in dairy processing technology have enhanced product quality, taste, and shelf life. The rapid expansion of supermarkets, hypermarkets, and online grocery platforms has also increased product accessibility, making lactose free milk widely available to consumers around the world.

What are the restraints for the global market?

Higher Production and Retail Costs

The production of lactose free milk involves additional processing steps such as enzyme treatment or filtration technologies, which increase manufacturing costs. These additional costs are reflected in retail prices, making lactose free milk more expensive than conventional milk. Price-sensitive consumers in emerging markets may therefore continue to prefer traditional dairy milk, limiting market penetration in certain regions.

Competition from Plant-Based Milk Alternatives

The growing popularity of plant-based milk alternatives such as almond milk, soy milk, and oat milk is creating competitive pressure on lactose free dairy products. These alternatives are widely marketed as lactose free and environmentally sustainable options. While lactose free milk retains the nutritional benefits of dairy, competition from plant-based beverages may influence consumer purchasing decisions, particularly among vegan or environmentally conscious consumers.

What are the key opportunities in the lactose free milk industry?

Expanding Demand in Emerging Markets

Emerging economies in Asia-Pacific and Latin America represent major growth opportunities for lactose free milk manufacturers. These regions have some of the highest rates of lactose intolerance globally, yet awareness and product availability remain relatively limited. As urbanization accelerates and retail infrastructure improves, dairy companies have an opportunity to introduce lactose free milk products to large consumer populations. Strategic marketing campaigns and competitive pricing strategies will be key to capturing these markets.

Integration into Functional Beverage and Nutrition Segments

The growing global demand for functional beverages presents another major opportunity for lactose free milk producers. Manufacturers can develop lactose free milk products enriched with protein, probiotics, and vitamins to position them as health-enhancing beverages. Such products appeal to athletes, health-conscious consumers, and individuals seeking convenient nutritional solutions. As functional nutrition trends expand globally, lactose free milk is expected to gain greater traction in the wellness beverage segment.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 16.72 Billion |

| Market Size in 2026 | USD 18.58 Billion |

| Market Size in 2031 | USD 31.44 Billion |

| CAGR | 11.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Lactose free semi-skimmed milk dominates the global market, accounting for nearly 34% of total demand. This segment benefits from consumer preference for a balanced combination of reduced fat content and creamy taste, making it suitable for everyday consumption and health-conscious diets. Lactose free whole milk continues to be popular among households seeking the traditional dairy flavor and texture, particularly in regions where milk consumption is culturally ingrained. Flavored lactose free milk, including chocolate and vanilla variants, is experiencing rapid adoption among younger consumers and children. Its versatility in ready-to-drink beverages, smoothies, and dairy-based desserts further expands its role in the broader dairy industry, positioning it as a key growth driver for the flavored segment.

Application Insights

Household consumption represents the largest application segment in the lactose free milk market, accounting for nearly 65% of global demand. Increasing prevalence of lactose intolerance and growing awareness of digestive health are driving consumers to adopt lactose free milk as a direct substitute for regular dairy milk. The food and beverage processing industry is also emerging as a high-growth segment, with manufacturers incorporating lactose free milk into ice cream, yogurt drinks, bakery items, and nutritional beverages. Additionally, the foodservice sector, particularly cafés, restaurants, and specialty coffee shops, is expanding the use of lactose free milk in beverages and culinary applications. The growing trend of functional foods and personalized nutrition is further supporting market adoption across urban regions worldwide.

Distribution Channel Insights

Supermarkets and hypermarkets dominate global lactose free milk sales, accounting for approximately 42% of the market. These channels provide extensive product variety, enabling consumers to explore premium and specialty lactose free options alongside conventional dairy products. Convenience stores are an important distribution channel in densely populated urban areas where consumers prioritize speed and accessibility. Online retail and e-commerce platforms are experiencing the fastest growth, driven by increasing consumer preference for digital shopping and home delivery. E-commerce enables manufacturers to reach niche consumer segments seeking specialized dairy products that may not always be available in physical stores, thus expanding market penetration and driving overall growth.

Explore more data points, trends and opportunities Download Free Sample Report

Lactose Free Milk Market Segmentations

By Product Type

- Lactose Free Whole Milk

- Lactose Free Semi-Skimmed Milk

- Lactose Free Skimmed Milk

- Flavored Lactose Free Milk

- Fortified & Functional Lactose Free Milk

By Application

- Household Consumption

- Food & Beverage Processing

- Foodservice & Hospitality

- Nutritional & Functional Beverage Production

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail & E-Commerce

- Specialty Dairy & Health Stores

- Foodservice & Institutional Sales

Regional Insights

North America

North America represents the largest market for lactose free milk, accounting for approximately 31% of global demand. The United States leads the region due to high consumer awareness of lactose intolerance, digestive health, and nutritional benefits. The presence of a well-established dairy industry, advanced processing infrastructure, and strong retail networks, including supermarkets and e-commerce platforms, supports market growth. Additionally, increasing demand for functional foods, organic products, and clean-label dairy beverages is accelerating consumption. In Canada, rising interest in health-conscious diets and the adoption of international dairy trends contribute to steady market expansion.

Europe

Europe accounts for nearly 28% of global lactose free milk demand, driven by a strong preference for specialized and health-focused dairy products. Key markets include Germany, the United Kingdom, France, and Italy, where consumers actively seek products with digestive benefits and natural ingredients. Government support for dairy innovation, robust production capabilities, and a culture of premium dairy consumption further boost growth. Additionally, increasing availability through supermarkets, specialty stores, and online channels is enabling wider adoption of lactose free milk across diverse consumer segments.

Asia-Pacific

Asia-Pacific is the fastest-growing lactose free milk market globally. High lactose intolerance prevalence in countries such as China, Japan, and South Korea has created substantial demand for digestive-friendly dairy alternatives. Rising disposable incomes, growing health awareness, and urbanization are fueling consumption, while the rapid expansion of modern retail networks—including supermarkets, convenience stores, and e-commerce platforms—is increasing product accessibility. China, in particular, represents one of the largest emerging markets for lactose free milk, driven by growing consumer interest in premium dairy, functional foods, and child nutrition products.

Latin America

Latin America is an emerging market for lactose free milk, with Brazil and Mexico accounting for the majority of regional demand. Key drivers include rising urbanization, increasing health awareness, and diversification of dairy product portfolios by manufacturers. Improvements in retail infrastructure, growing supermarket chains, and expanding modern trade channels are facilitating greater product availability. Additionally, changing consumer lifestyles and higher disposable income levels are encouraging households to adopt lactose free alternatives, creating long-term growth opportunities for the market.

Middle East & Africa

The Middle East and Africa region is witnessing gradual growth in lactose free milk consumption. Countries such as Saudi Arabia, the United Arab Emirates, and South Africa are emerging markets where rising consumer awareness of digestive health is driving demand. Expansion of modern retail formats, including supermarkets and convenience stores, along with the presence of international dairy brands, is enhancing product accessibility. Furthermore, increasing exposure to Western dietary trends and a growing interest in premium and functional dairy products are contributing to steady market growth across the region.

Key Players in the Lactose Free Milk Market

- Nestlé S.A.

- Danone S.A.

- Arla Foods

- Lactalis Group

- Fonterra Co-operative Group

- Dairy Farmers of America

- FrieslandCampina

- Saputo Inc.

- Yili Group

- Mengniu Dairy

- Meiji Holdings

- Organic Valley

- Parmalat

- Amul

- Dean Foods