Lactose Free Dairy Products Market Size

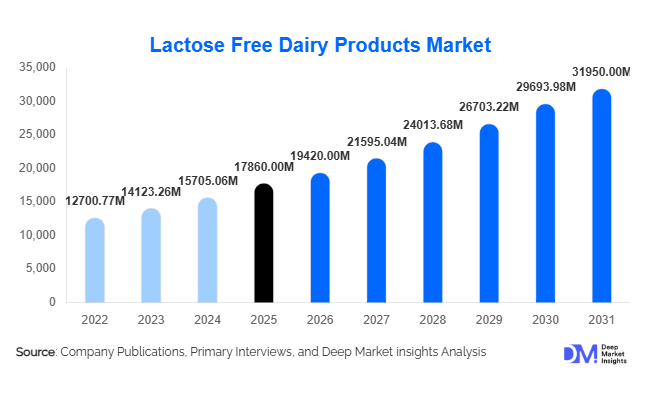

According to Deep Market Insights, the global lactose free dairy products market size was valued at USD 17,860 million in 2025 and is projected to grow from USD 19,420 million in 2026 to reach approximately USD 32,950 million by 2031, expanding at a CAGR of 11.2% during the forecast period (2026–2031). Market expansion is primarily driven by increasing global awareness of lactose intolerance, rising digestive health concerns, and growing consumer preference for functional and clean-label dairy alternatives. Lactose free dairy products are increasingly positioned as mainstream nutritional offerings rather than niche medical dietary solutions.

The market is witnessing strong momentum across developed and emerging economies as manufacturers introduce enzyme-treated milk, lactose free yogurt, cheese, butter, and infant nutrition products designed to maintain taste parity with conventional dairy. Rapid urbanization, evolving dietary habits, and increasing health-conscious consumption patterns are encouraging retailers and foodservice operators to expand lactose free product portfolios. Technological advancements in lactase enzyme processing and ultra-filtration methods are improving product texture and affordability, enabling wider consumer adoption.

In addition, demand is expanding beyond lactose-intolerant populations toward fitness-focused and wellness-oriented consumers seeking easier digestion and gut-friendly foods. Retail penetration through supermarkets, e-commerce platforms, and private-label brands is accelerating accessibility globally. Emerging markets across Asia-Pacific and Latin America are witnessing particularly strong growth as dairy consumption rises alongside disposable incomes. As innovation, affordability, and distribution networks strengthen, lactose free dairy products are transitioning into a core category within the global dairy industry.

Key Market Insights

- Lactose intolerance awareness is driving mainstream adoption, particularly in Asia-Pacific and Latin America where intolerance prevalence exceeds 60% of adults.

- Lactose free milk dominates product demand, supported by daily consumption patterns and improved flavor technologies.

- Retail private-label expansion is lowering price barriers and increasing accessibility worldwide.

- Asia-Pacific is the fastest-growing region, fueled by urbanization and rising nutritional awareness.

- Functional dairy positioning linking digestive health and protein intake is expanding the consumer base.

- Technological innovation in enzyme processing is reducing production costs and improving scalability.

What are the latest trends in the lactose free dairy products market?

Functional Nutrition and Digestive Health Positioning

Lactose free dairy products are increasingly marketed as digestive wellness foods rather than specialty alternatives. Consumers are actively seeking products that support gut health without eliminating dairy nutrition benefits such as calcium and protein. Manufacturers are incorporating probiotics, high-protein formulations, vitamin fortification, and clean-label ingredients to differentiate offerings. This trend is especially prominent among millennials and aging populations seeking digestive comfort without sacrificing taste or nutrition.

Premiumization and Product Diversification

The market is experiencing rapid diversification beyond lactose free milk into cheese spreads, flavored yogurts, ice creams, and ready-to-drink dairy beverages. Premium lactose free products emphasizing organic sourcing, grass-fed milk, and sustainable packaging are gaining traction in North America and Europe. Brands are focusing on taste equivalence with traditional dairy products, addressing earlier consumer skepticism regarding flavor differences.

What are the key drivers in the lactose free dairy products market?

Rising Global Lactose Intolerance Prevalence

Approximately two-thirds of the global adult population experiences some degree of lactose malabsorption, creating a large addressable consumer base. Increasing medical awareness and diagnostic rates are encouraging consumers to switch toward lactose free alternatives rather than eliminating dairy entirely. This structural demand driver continues to expand market penetration globally.

Growth of Health-Conscious Consumer Behavior

Consumers increasingly associate lactose free products with better digestion, lighter nutrition, and wellness-oriented lifestyles. Fitness communities, aging populations, and preventive healthcare trends are reinforcing demand. Marketing strategies highlighting protein intake, bone health, and digestive comfort are strengthening category adoption.

Retail and E-Commerce Expansion

Supermarkets and online grocery platforms are allocating greater shelf space to specialty dairy categories. Private-label lactose free lines introduced by large retailers have improved affordability, increasing penetration in price-sensitive markets.

What are the restraints for the global market?

Higher Production and Retail Pricing

Lactose removal requires enzyme processing and additional quality control steps, increasing manufacturing costs. As a result, lactose free products often carry price premiums of 15–30% compared with conventional dairy, limiting adoption in developing economies.

Cold Chain and Supply Constraints

Dairy logistics remain sensitive to refrigeration infrastructure. In emerging markets, inconsistent cold-chain systems restrict distribution reach, particularly for yogurt and fresh dairy categories.

What are the key opportunities in the lactose free dairy products industry?

Expansion Across Asia-Pacific and Africa

Regions with high lactose intolerance prevalence present strong opportunities for new entrants. Countries such as China, India, Indonesia, and Nigeria are witnessing rising dairy consumption combined with digestive sensitivity awareness. Localization of production facilities can significantly reduce costs and improve accessibility.

Integration with Functional and Sports Nutrition

Lactose free dairy proteins are increasingly used in sports beverages, medical nutrition, and elderly dietary products. Partnerships between dairy producers and nutrition brands are expected to create new revenue streams and premium product categories.

Government Nutrition Programs and School Milk Initiatives

Public health initiatives promoting calcium and protein intake are encouraging adoption of lactose free milk in institutional programs. Governments seeking to address malnutrition without digestive discomfort are incorporating lactose free dairy into nutrition schemes, opening long-term demand channels.

Product Type Insights

The global lactose free dairy products market is experiencing strong structural expansion, supported by increasing awareness of digestive health, rising diagnosis of lactose intolerance, and growing consumer preference for functional and specialized nutrition products. Among all product categories, lactose free milk continues to dominate the market landscape, accounting for approximately 46% of the global market share in 2025. The segment’s leadership is primarily attributed to its position as a daily staple product, making it the most frequently consumed lactose free dairy alternative across households worldwide. Unlike niche dairy alternatives, lactose free milk directly replaces conventional milk without requiring major dietary changes, enabling faster consumer adoption across age groups and income segments. Technological advancements in lactase enzyme processing have significantly improved taste neutrality and nutritional equivalence, allowing manufacturers to deliver products nearly identical to traditional milk while eliminating digestive discomfort.The leading driver supporting lactose free milk growth is its integration into routine consumption occasions such as breakfast beverages, coffee preparation, cereal consumption, and cooking applications. Increasing penetration in school nutrition programs, clinical dietary recommendations, and wellness-focused households further strengthens demand consistency. Additionally, expansion of fortified lactose free milk variants enriched with calcium, vitamin D, omega fatty acids, and protein has elevated the category beyond intolerance management into preventive health nutrition. Retailers increasingly allocate premium shelf space to lactose free milk due to high turnover rates and strong repeat purchase behavior, reinforcing its dominant share globally.Butter and cream products remain comparatively niche; however, they are gaining strategic importance within premium culinary applications. Growth in artisanal baking, specialty cafés, and gourmet cooking trends is encouraging adoption of lactose free butter and cream among chefs catering to dietary-sensitive consumers. The key driver here is foodservice inclusivity, allowing restaurants and bakeries to serve broader customer demographics without altering flavor profiles. Premium positioning and higher margins make this category attractive for manufacturers despite smaller volume share.Lactose free ice cream is emerging rapidly as indulgence-driven innovation reshapes consumer perception of dietary restriction products. Historically viewed as functional substitutes, lactose free desserts are now marketed as premium indulgence experiences. Advances in fat emulsification and plant-dairy hybrid formulations enable creamy textures comparable to traditional ice cream. The primary growth driver is the shift toward “permissible indulgence,” where consumers seek comfort foods aligned with health needs. Expansion of unique flavors, low-sugar options, and protein-enriched frozen desserts is attracting younger demographics and expanding seasonal consumption patterns.Overall, product innovation across the lactose free category is moving beyond intolerance management toward lifestyle nutrition. Manufacturers increasingly position lactose free dairy as part of holistic wellness, performance nutrition, and digestive optimization strategies, ensuring sustained category diversification and long-term growth momentum.

Application Insights

Application analysis indicates that household retail consumption dominates global demand, contributing nearly 62% of total market consumption. The leading driver behind this segment is the growing normalization of lactose free products within everyday diets rather than occasional medical usage. Consumers increasingly purchase lactose free dairy for entire households instead of only intolerance-affected individuals, driven by perceptions of easier digestion and lighter nutritional profiles. Rising home cooking trends, accelerated during recent years and sustained afterward, continue to support consistent retail consumption volumes.Another key factor strengthening household demand is product accessibility. Expanded product assortments across supermarkets, online grocery platforms, and private-label offerings have reduced price premiums historically associated with lactose free dairy. As affordability improves, adoption spreads into middle-income households across emerging economies. Educational campaigns by healthcare professionals recommending reduced-lactose diets for digestive comfort also reinforce routine consumption patterns.Foodservice applications represent a steadily expanding segment as cafés, quick-service restaurants, and specialty beverage chains introduce lactose free alternatives in coffee, smoothies, desserts, and bakery items. The primary growth driver is menu inclusivity. Restaurants increasingly recognize dietary accommodation as a competitive advantage, enabling them to serve lactose-sensitive consumers without operational complexity. Barista-friendly lactose free milk formulations with improved foam stability have accelerated adoption within specialty coffee chains, supporting higher consumption volumes in urban markets.Infant nutrition constitutes a high-value application segment supported by rising parental awareness regarding digestive sensitivity and pediatric nutrition requirements. Lactose reduced or lactose free dairy formulations are increasingly used in specialized infant formulas designed for temporary lactose intolerance or gastrointestinal sensitivity. Growth is driven by increasing healthcare guidance, higher birth rates in emerging markets, and premiumization trends within infant nutrition categories.Clinical nutrition and elderly dietary applications are also gaining traction globally. Aging populations in developed economies increasingly require easily digestible protein sources, positioning lactose free dairy as an ideal nutritional solution.

Distribution Channel Insights

Distribution dynamics highlight the continued dominance of supermarkets and hypermarkets, which account for nearly 48% of total global sales. The primary driver supporting this channel is consumer trust combined with advanced cold-chain infrastructure required for dairy preservation. Large retail formats enable wide product visibility, in-store comparison, and promotional pricing strategies that encourage trial purchases. Dedicated health-food aisles and refrigerated specialty sections further enhance category discoverability.Retailers also benefit from strong partnerships with dairy manufacturers that invest heavily in sampling campaigns, nutritional education, and shelf branding. As lactose free products transition into mainstream consumption, supermarkets increasingly treat them as core dairy offerings rather than specialty items, strengthening volume throughputOnline retail is emerging as the fastest-growing distribution channel, expanding at annual growth rates exceeding 14%. The leading driver behind this expansion is the rise of subscription-based grocery delivery models and personalized nutrition purchasing behavior. Digital platforms allow consumers to filter products based on dietary needs, enabling lactose free products to reach highly targeted audiences efficiently. E-commerce platforms also support product variety unavailable in physical stores, encouraging experimentation and brand switching.Urban consumers particularly favor online purchasing due to convenience, recurring delivery schedules, and bundled wellness products. Integration of lactose free dairy within broader health-focused digital marketplaces accelerates adoption among younger, tech-savvy demographics. Additionally, direct-to-consumer models allow manufacturers to gather consumer data insights, supporting product innovation and targeted marketing strategies.Convenience stores and specialty health retailers continue to support category growth, especially in densely populated urban regions. These outlets serve impulse purchases and niche consumer groups seeking premium or organic lactose free products. Specialty retailers play a critical role in early adoption of innovative formulations before mainstream retail expansion occurs.

End-Use Insights

From an end-use perspective, residential consumers remain the largest segment, reflecting the household-driven nature of lactose free dairy consumption. The primary growth driver is increased consumer recognition that lactose sensitivity varies in intensity, encouraging broader adoption even among individuals without formal diagnoses. Families increasingly choose lactose free dairy as a preventive dietary choice, expanding the addressable consumer base beyond medically necessary users.However, foodservice and industrial food manufacturing segments are growing at faster rates, supported by evolving formulation strategies across the global food industry. Bakery manufacturers, confectionery producers, and ready-to-drink beverage companies increasingly incorporate lactose free dairy ingredients to meet allergen-sensitive consumer demand while maintaining traditional taste profiles. The expansion of ready-to-eat meals and functional beverages significantly boosts industrial utilization.The leading driver within industrial applications is product reformulation aimed at expanding consumer inclusivity without sacrificing flavor authenticity. Manufacturers benefit from lactose free ingredients that allow “free-from” labeling claims, improving product differentiation in competitive retail environments. Export-oriented production is also rising as European and North American dairy producers supply Asia-Pacific markets where domestic lactose free processing capacity remains limited.The global functional foods industry, valued above USD 350 billion, increasingly integrates lactose free dairy proteins into high-protein snacks, sports nutrition beverages, and wellness-focused meal replacements. This integration positions lactose free dairy not merely as a substitute category but as a foundational ingredient supporting future nutrition innovation.

| By Product Type | By Distribution Channel | By End Use |

|---|---|---|

|

|

|

Regional Insights

North America

North America accounted for approximately 32% of global lactose free dairy market share in 2025, making it the leading regional market. The United States and Canada dominate regional demand due to advanced dairy processing infrastructure, high consumer awareness, and strong innovation ecosystems within the food industry. One of the primary drivers of regional growth is widespread consumer education regarding digestive health and food sensitivities. Healthcare professionals and nutrition organizations actively promote lactose free options, encouraging early adoption across diverse demographic groups.Another major growth driver is premium product innovation. North American consumers demonstrate strong willingness to pay for value-added dairy products, enabling rapid commercialization of organic, protein-enriched, and fortified lactose free variants. Retail maturity further accelerates adoption, with national supermarket chains ensuring consistent availability across urban and suburban regions. The region also benefits from strong private-label expansion, making lactose free dairy more affordable and accessible to mainstream consumers.Foodservice innovation significantly contributes to regional growth, particularly through specialty coffee chains incorporating lactose free milk into beverage menus. Additionally, rising demand for functional foods and sports nutrition products strengthens industrial utilization of lactose free dairy ingredients. Continuous product launches and aggressive marketing strategies by major dairy companies ensure sustained market leadership for North America.

Europe

Europe represents nearly 28% of global demand, supported by mature dairy traditions combined with strong regulatory frameworks promoting food transparency. A key regional growth driver is stringent labeling regulations that enhance consumer confidence in allergen declarations and nutritional claims. Countries including Germany, the United Kingdom, France, Italy, and the Netherlands demonstrate high adoption rates due to widespread digestive wellness awareness.European consumers increasingly prioritize clean-label and natural food products, aligning strongly with lactose free dairy positioning. Scandinavian countries exhibit particularly high per-capita consumption, driven by proactive health awareness and advanced dairy innovation. Another important driver is sustainability-focused dairy production, where manufacturers integrate environmentally responsible practices alongside functional nutrition benefits.Europe also benefits from strong export capabilities, supplying lactose free products to emerging markets with growing intolerance awareness. Continuous investment in enzyme technology and product diversification supports long-term regional competitiveness. The integration of lactose free dairy into bakery, confectionery, and prepared meal industries further expands market penetration across multiple consumption occasions.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market, expanding at a CAGR exceeding 13%. The leading driver is the exceptionally high prevalence of lactose intolerance across Asian populations, creating a naturally large target consumer base. China, Japan, South Korea, and India serve as key growth engines, supported by rising disposable income, rapid urbanization, and expanding modern retail infrastructure.China alone is expected to contribute more than 18% of incremental global market growth by 2031, fueled by increasing demand for digestive-friendly dairy products among middle-class consumers. Government nutrition initiatives encouraging balanced diets are also supporting dairy consumption growth. In India, increasing health awareness among younger consumers and expansion of organized retail chains are accelerating category visibility.Another major regional driver is import dependence. Limited domestic lactose free processing capacity in several Asian markets creates opportunities for international dairy exporters. Simultaneously, local manufacturers are investing in enzyme-processing technologies to reduce reliance on imports, fostering regional production expansion. Growth of e-commerce grocery platforms further accelerates accessibility in densely populated urban centers.

Latin America

Latin America is emerging as a promising growth region led by Brazil, Mexico, and Argentina. The primary growth driver is retail modernization, including expansion of supermarket chains and refrigerated logistics networks enabling wider dairy distribution. Rising consumer awareness regarding digestive health is gradually shifting purchasing behavior toward specialized dairy products.Economic development and urbanization are increasing demand for packaged and value-added food products, creating favorable conditions for lactose free dairy adoption. Regional dairy producers are beginning to diversify product portfolios to capture premium market segments, while multinational brands introduce affordable lactose free offerings tailored to local price sensitivity. Educational marketing campaigns emphasizing digestive comfort continue to expand consumer understanding and category acceptance.

Middle East & Africa

The Middle East & Africa region is witnessing steady demand growth driven by premium retail expansion and demographic diversification. Countries such as the United Arab Emirates, Saudi Arabia, and South Africa are key markets benefiting from increasing expatriate populations familiar with lactose free diets. Rising disposable incomes and growing health-conscious consumer segments further support adoption.A major regional growth driver is dependence on imported dairy products, which creates investment opportunities for localized manufacturing and cold-chain development. Modern retail expansion, particularly hypermarkets and specialty wellness stores, improves product availability across metropolitan areas. Hospitality and tourism sectors also contribute to demand as hotels and international restaurant chains incorporate lactose free options to serve global travelers.As awareness campaigns and healthcare recommendations expand across the region, lactose free dairy products are expected to transition from premium niche offerings to more widely consumed dietary staples, supporting long-term market expansion.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Lactose Free Dairy Products Market

- Nestlé S.A.

- Danone S.A.

- Arla Foods amba

- Lactalis Group

- Fonterra Co-operative Group Limited

- FrieslandCampina

- Valio Ltd.

- Dean Foods Company

- Saputo Inc.

- Yili Group

- Mengniu Dairy Company Limited

- Agropur Cooperative

- Emmi Group

- Meiji Holdings Co., Ltd.

- DMK Group