L-Carnitine Supplements Market Size

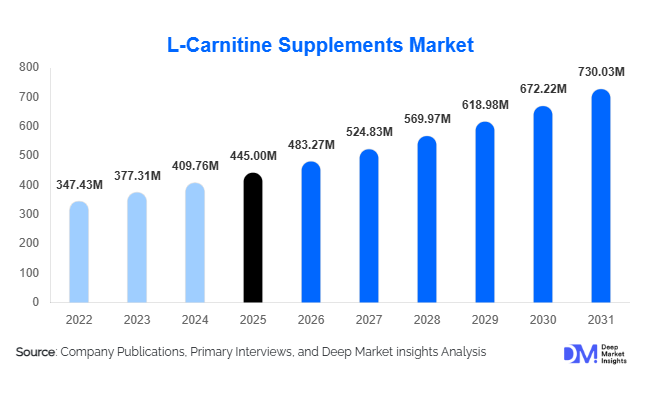

According to Deep Market Insights,the global L-carnitine supplements market size was valued at USD 445 million in 2025 and is projected to grow from USD 483.27 million in 2026 to reach USD 730.03 million by 2031, expanding at a CAGR of 8.6% during the forecast period (2026–2031). Market growth is primarily driven by rising consumer focus on metabolic health, increasing sports nutrition consumption, expanding preventive healthcare adoption, and the growing integration of L-carnitine into functional beverages and performance-enhancing formulations. As global awareness around fat metabolism, cardiovascular wellness, and energy optimization increases, L-carnitine supplements are witnessing strong demand across both developed and emerging economies.

Key Market Insights

- Sports nutrition remains the dominant application, accounting for nearly 35% of total demand in 2025, driven by gym culture and endurance sports participation.

- Capsules lead the product form segment, contributing approximately 34% of the global market share due to dosage accuracy and consumer convenience.

- Fermentation-based production holds over 50% share, reflecting growing preference for sustainable and high-purity ingredients.

- North America dominates the global market, accounting for around 35% of total revenue in 2025, led by strong supplement penetration in the U.S.

- Asia-Pacific is the fastest-growing region, expanding at over 10% CAGR through 2031, supported by rising fitness adoption in China and India.

- Online retail channels contribute nearly 29% of sales, with subscription models and direct-to-consumer platforms accelerating growth.

What are the latest trends in the L-carnitine supplements market?

Premiumization and Clinical Validation

Manufacturers are increasingly investing in clinically validated formulations to differentiate their products in a competitive landscape. Acetyl-L-carnitine (ALCAR) and L-carnitine L-tartrate are being positioned for cognitive health and athletic recovery benefits, supported by scientific studies. Brands emphasizing evidence-backed claims and third-party testing certifications are gaining higher consumer trust and commanding premium pricing. Clean-label positioning, vegetarian capsules, and allergen-free formulations are becoming key differentiators in developed markets.

Expansion into Functional Beverages and RTD Formats

L-carnitine is increasingly being incorporated into ready-to-drink (RTD) energy beverages and metabolic boosters. Younger consumers prefer flavored liquid formats over traditional tablets, encouraging companies to innovate in convenient delivery systems. Functional beverage integration not only expands the consumer base but also increases frequency of consumption, contributing to volume growth. This trend is particularly visible in Asia-Pacific and North America, where performance drinks are gaining mainstream popularity.

What are the key drivers in the L-carnitine supplements market?

Growing Sports Nutrition Consumption

Rising gym memberships, bodybuilding culture, and participation in endurance sports are significantly driving demand. L-carnitine L-tartrate is widely used in pre-workout and fat metabolism formulations, making it a staple ingredient in sports nutrition. Increasing consumer awareness about recovery enhancement and muscle performance continues to stimulate repeat purchases.

Rising Metabolic and Cardiovascular Health Awareness

The global increase in obesity and metabolic syndrome cases is encouraging consumers to seek supplements supporting fat oxidation and energy metabolism. Aging populations, particularly in Japan and Europe, are adopting acetyl-L-carnitine for cardiovascular and cognitive health benefits. Preventive healthcare trends are reinforcing long-term market growth.

What are the restraints for the global market?

Regulatory and Health Claim Restrictions

Strict dietary supplement regulations in North America and Europe limit aggressive marketing claims. Compliance with FDA and EFSA standards increases operational costs and restricts product positioning flexibility.

Raw Material Price Volatility

Production costs are influenced by fluctuations in chemical intermediates and fermentation inputs. Rising input costs can compress profit margins, particularly for mid-sized manufacturers operating in price-sensitive markets.

What are the key opportunities in the L-carnitine supplements industry?

Emerging Asia-Pacific Demand

China, India, South Korea, and Southeast Asia present high-growth opportunities. Rising disposable income and expanding digital commerce penetration support supplement adoption. Localization strategies, including vegetarian-friendly formulations and regional flavor preferences, can unlock new demand pools.

Direct-to-Consumer and Subscription Models

Brands leveraging e-commerce platforms and subscription-based sales models are improving customer retention and margins. Personalized nutrition and bundled supplement packages provide cross-selling opportunities and recurring revenue streams.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 445 Million |

| Market Size in 2026 | USD 483.27 Million |

| Market Size in 2031 | USD 730.03 Million |

| CAGR | 8.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Form Insights

The capsules segment leads the global L-carnitine market in 2025, accounting for approximately 34% of total revenue share. This dominance is primarily driven by consumer preference for convenience, precise dosage control, longer shelf life, and ease of swallowing compared to traditional tablets. Capsules also support advanced delivery technologies that enhance bioavailability, making them particularly attractive for sports nutrition and cardiovascular formulations. Tablets remain a strong secondary format, especially in pharmacy and drugstore channels, where cost-effectiveness and familiarity influence purchasing decisions. Powder formats are witnessing accelerated adoption among athletes and bodybuilders due to their flexibility in dosage customization and compatibility with protein shakes and pre-workout blends. Liquid and ready-to-drink (RTD) formulations are expanding rapidly in urban markets, supported by busy lifestyles and on-the-go consumption trends. Softgels continue to gain traction in premium product categories, particularly for cardiovascular and metabolic health applications, as they offer improved absorption characteristics and higher perceived product quality.

Type Insights

L-carnitine L-tartrate holds the leading position in 2025 with nearly 30% market share, supported by its superior absorption rate and strong clinical validation in sports recovery and muscle performance applications. Its widespread use in pre- and post-workout supplements continues to drive segmental growth, particularly as athletic performance and muscle recovery remain core consumer priorities. Acetyl-L-carnitine represents the fastest-growing variant, benefiting from expanding research on cognitive health, neurological support, and age-related mental decline. Its dual positioning in both sports nutrition and brain health supplements strengthens its cross-functional appeal. Propionyl-L-carnitine and Glycine Propionyl-L-Carnitine (GPLC) are emerging as niche but steadily expanding segments, particularly in vascular health and clinical nutrition applications. Growth in these specialized variants is supported by increasing physician recommendations and rising consumer awareness regarding cardiovascular and endothelial health benefits.

Distribution Channel Insights

Online retail accounts for approximately 29% of global sales in 2025, reflecting rapid digital transformation across supplement purchasing behavior. Direct-to-consumer brand models, subscription-based services, influencer marketing, and cross-border e-commerce platforms significantly enhance online penetration. Pharmacies and drug stores continue to play a critical role, particularly for clinically positioned and prescription-adjacent formulations where consumer trust and professional guidance are essential. Specialty nutrition stores remain important for performance-oriented buyers seeking expert recommendations and premium sports formulations. Supermarkets and hypermarkets contribute to mass-market accessibility, particularly for entry-level and weight management products, expanding the consumer base beyond fitness-focused demographics.

End-Use Insights

Sports nutrition remains the largest end-use segment, contributing approximately 35% of global revenue in 2025. The segment’s leadership is driven by increasing participation in fitness activities, rising gym memberships, and growing awareness of muscle recovery and endurance optimization. Weight management applications account for nearly 28% of total demand, supported by rising global obesity rates and growing consumer preference for metabolism-enhancing supplements. Cognitive and cardiovascular health segments are expanding at a CAGR exceeding 10%, particularly in aging economies where preventive healthcare is prioritized. Countries such as Japan and Germany are witnessing increasing adoption in memory support and heart health formulations. Clinical nutrition integration is emerging as a promising niche, with hospitals and healthcare providers incorporating L-carnitine into therapeutic dietary regimens, particularly for metabolic disorders and deficiency management.

Explore more data points, trends and opportunities Download Free Sample Report

L-Carnitine Supplements Market Segmentations

By Product Form

- Capsules

- Tablets

- Powder

- Liquid

- Softgels

- Ready-to-Drink (RTD) Shots & Functional Beverages

By L-Carnitine Type

- L-Carnitine (Base)

- L-Carnitine L-Tartrate

- Acetyl-L-Carnitine (ALCAR)

- Propionyl-L-Carnitine

- Glycine Propionyl-L-Carnitine (GPLC)

By Application

- Sports Nutrition

- Weight Management

- Cardiovascular Health

- Cognitive Health

- Energy & Metabolism Support

- Clinical Nutrition

By Distribution Channel

- Online Retail

- Pharmacies & Drug Stores

- Supermarkets & Hypermarkets

- Specialty Nutrition Stores

- Direct-to-Consumer (Brand Websites)

By Consumer Category

- Sports & Fitness Consumers

- Weight Management Consumers

- Geriatric Population

- Clinical & Therapeutic Users

- General Wellness Consumers

Regional Insights

North America

North America holds approximately 35% of the global market share in 2025, with the United States contributing nearly 28% alone. Regional growth is driven by high dietary supplement penetration, strong sports nutrition culture, and widespread adoption of performance-enhancing products among both professional and recreational athletes. Advanced e-commerce infrastructure and well-established direct-to-consumer brands further accelerate market expansion. Preventive healthcare awareness, high disposable income, and increasing demand for weight management solutions continue to reinforce growth. Canada supports steady expansion through rising consumer awareness regarding cardiovascular and metabolic health, along with regulatory clarity that strengthens consumer confidence in supplement safety.

Europe

Europe represents around 22% of the global market, led by Germany, the United Kingdom, Italy, and France. Regional demand is largely influenced by aging populations, strong cardiovascular health awareness, and increasing adoption of cognitive support supplements. The region’s stringent regulatory framework ensures high product quality and safety standards, which benefits established brands and pharmaceutical-grade manufacturers. Growing interest in preventive health, expanding sports participation, and increasing demand for clean-label formulations further contribute to stable long-term growth. Eastern European markets are gradually emerging as new growth pockets due to improving retail infrastructure and rising disposable incomes.

Asia-Pacific

Asia-Pacific accounts for roughly 30% of global revenue and is the fastest-growing region, expanding at over 10% CAGR. China leads regional demand, supported by rapid fitness industry expansion, rising middle-class income, and strong cross-border e-commerce platforms that facilitate access to international supplement brands. India is experiencing double-digit growth exceeding 11% CAGR, driven by increasing urbanization, growing gym penetration, rising sports participation among youth, and heightened awareness of weight management solutions. Japan represents a mature yet stable market, with demand concentrated in cognitive health and geriatric nutrition applications due to its aging population. Southeast Asian countries are also contributing to growth through expanding retail channels and increasing adoption of Western fitness trends.

Latin America

Latin America contributes approximately 6% of global demand, with Brazil and Mexico serving as primary markets. Brazil demonstrates growth nearing 10% CAGR, fueled by strong sports culture, expanding bodybuilding communities, and improved availability of imported supplements. Expanding retail distribution networks and rising health consciousness among urban populations further stimulate demand. Mexico benefits from increasing weight management awareness and the growing presence of international supplement brands, while regulatory modernization efforts are gradually strengthening consumer confidence.

Middle East & Africa

The Middle East & Africa region accounts for nearly 7% of global market share. In the Middle East, the United Arab Emirates and Saudi Arabia drive demand due to high disposable incomes, premium supplement consumption patterns, and strong interest in fitness and lifestyle enhancement. Expanding gym chains and international retail brands are supporting market penetration. In Africa, South Africa anchors regional demand, benefiting from rising sports nutrition awareness and gradual expansion of organized retail channels. Growing urbanization, improving healthcare infrastructure, and increasing preventive health awareness are expected to support steady long-term growth across the broader region.

Key Players in the L-Carnitine Supplements Market

- Lonza Group

- GNC Holdings

- NOW Foods

- Amway

- Herbalife Nutrition

- Glanbia Plc

- Nature’s Bounty

- Olimp Laboratories

- Universal Nutrition

- MuscleTech

- Nutrex Research

- NutraBio Labs

- Scitec Nutrition

- Twinlab

- Vitacost