Kuwait Food and Drink Market Size

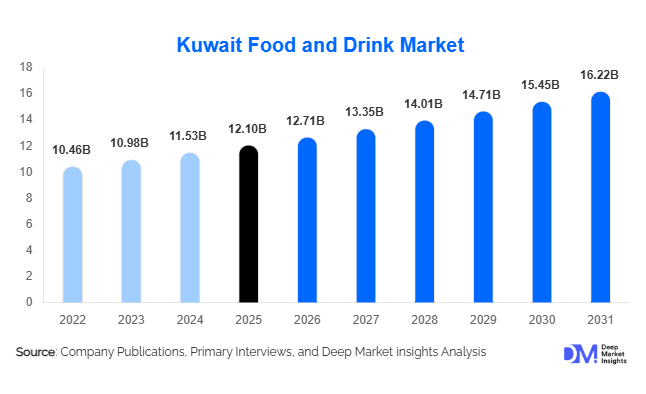

According to Deep Market Insights, the Kuwait food and drink market size was valued at USD 12.1 billion in 2025 and is projected to grow from USD 12.71 billion in 2026 to reach USD 16.22 billion by 2031, expanding at a CAGR of 5.0% during the forecast period (2026–2031). The Kuwait food and drink market growth is primarily driven by rising disposable income, increasing urbanization, strong demand for imported premium food products, expansion of organized retail infrastructure, and changing consumer preferences toward convenience and healthier packaged foods.

Key Market Insights

- Kuwait remains heavily dependent on imported food products, creating strong opportunities for international manufacturers and regional distributors.

- Packaged and processed foods dominate market demand, supported by busy urban lifestyles and rising demand for convenience-oriented consumption.

- Health-conscious consumption is rapidly increasing, driving demand for organic foods, low-sugar beverages, plant-based dairy alternatives, and functional nutrition products.

- Hypermarkets and supermarkets continue to dominate distribution, while online grocery platforms and quick-commerce applications are witnessing rapid growth.

- The expatriate population contributes significantly to food demand, influencing multicultural food preferences and imported cuisine categories.

- Premiumization is accelerating across beverage and snack categories, particularly in specialty coffee, dairy products, gourmet confectionery, and functional drinks.

What are the latest trends in the Kuwait food and drink market?

Health and Functional Foods Gaining Strong Momentum

Consumers across Kuwait are increasingly prioritizing health and wellness in their purchasing decisions. Demand for low-calorie beverages, sugar-free drinks, plant-based dairy alternatives, protein-enriched snacks, and organic packaged foods is growing rapidly among younger demographics and affluent households. Manufacturers are reformulating products to reduce sugar and artificial ingredients while launching functional products focused on immunity, digestive health, sports nutrition, and wellness-oriented lifestyles. Rising awareness regarding obesity and diabetes is also accelerating demand for healthier food alternatives across supermarkets, cafés, and digital retail platforms.

Rapid Growth of Digital Grocery and Food Delivery Platforms

Digital transformation is significantly reshaping Kuwait’s food and beverage retail ecosystem. Online grocery applications and food delivery platforms are witnessing strong adoption due to high smartphone penetration and convenience-driven consumer behavior. Retailers and restaurant operators are investing heavily in omnichannel infrastructure, AI-based recommendation systems, and rapid delivery logistics. Cloud kitchens and app-based food brands are becoming increasingly popular, especially among urban consumers seeking convenience, product variety, and faster delivery experiences. The growing popularity of subscription-based meal services and direct-to-consumer food brands is further transforming purchasing patterns.

What are the key drivers in the Kuwait food and drink market?

High Disposable Income and Premium Consumption Trends

Kuwait’s strong household purchasing power remains one of the key growth drivers for the food and beverage sector. Consumers are increasingly willing to spend on premium imported foods, gourmet confectionery, specialty coffee, organic dairy products, and international restaurant experiences. High-income consumers continue to support strong demand for luxury packaged foods and premium beverages, encouraging multinational companies to expand their regional presence and premium product portfolios.

Urbanization and Changing Consumer Lifestyles

Rapid urbanization, changing dietary habits, and increasing workforce participation are accelerating demand for ready-to-eat meals, frozen foods, packaged snacks, and quick-service restaurants. Younger consumers increasingly prefer convenience-oriented food products that align with fast-paced urban lifestyles. The expansion of café culture and dining-out habits is also contributing significantly to beverage and foodservice market growth.

Expansion of Organized Retail Infrastructure

The rapid expansion of hypermarkets, supermarkets, and convenience store chains has significantly improved access to international food brands and diversified product offerings. Retailers are investing in advanced refrigeration systems, automated inventory management, and cold-chain infrastructure to support growing imports of fresh and packaged food products. Improved retail accessibility is helping accelerate consumption across multiple categories.

What are the restraints for the global market?

Heavy Dependence on Food Imports

Kuwait’s harsh climatic conditions and limited agricultural land make the country highly dependent on imported food products and raw materials. This exposes the market to global supply chain disruptions, commodity price fluctuations, geopolitical risks, and freight cost increases. Rising shipping costs and import dependency continue to create pricing volatility across packaged foods, meat products, grains, and beverages.

Rising Regulatory and Operational Costs

Increasing food safety regulations, nutritional labeling requirements, and stricter quality compliance standards are raising operational costs for manufacturers and distributors. Discussions surrounding sugar taxes and health-focused regulations could also impact certain beverage categories. Additionally, rising logistics expenses, warehousing costs, and labor expenditures are creating margin pressures across retail and foodservice operations.

What are the key opportunities in the Kuwait food and drink industry?

Expansion of Health-Oriented Product Categories

The growing wellness movement presents substantial opportunities for manufacturers of organic foods, fortified beverages, functional dairy products, and plant-based alternatives. Health-conscious consumers are increasingly seeking clean-label ingredients, nutritional transparency, and fitness-oriented food products. Companies capable of launching innovative health-focused offerings are expected to gain strong competitive advantages over the coming years.

Growth in Online Grocery and Quick Commerce

Rapid growth in e-commerce grocery platforms and quick-commerce delivery applications presents major opportunities for both retailers and food manufacturers. Investments in AI-enabled logistics, last-mile delivery networks, and digital retail experiences are expected to improve customer retention and market penetration. Online grocery channels are also enabling easier access to imported premium food products and niche dietary categories.

Food Security and Local Manufacturing Investments

Kuwait’s increasing focus on food security and strategic reserves is encouraging investments in local food processing, hydroponic farming, cold-chain infrastructure, and packaging facilities. Government-backed initiatives aimed at improving supply resilience are creating opportunities for private sector participation in food manufacturing and regional distribution operations.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 12.1 Billion |

| Market Size in 2026 | USD 12.71 Billion |

| Market Size in 2031 | USD 16.22 Billion |

| CAGR | 5.0% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Category Insights

Packaged and processed foods continue to dominate the Kuwait food and drink market, accounting for nearly 38% of total market value in 2025. The segment’s leadership is primarily driven by rapid urbanization, increasingly busy lifestyles, growing dual-income households, and rising consumer preference for convenience-oriented meal solutions. Demand for frozen foods, ready-to-eat meals, canned products, instant noodles, packaged snacks, and shelf-stable grocery items has increased substantially among working professionals and younger consumers seeking time-efficient food options. The expansion of modern retail infrastructure and the availability of international food brands across supermarkets and e-commerce platforms have further accelerated growth in this category. Within the beverage segment, bottled water remains the leading category, contributing approximately 14% of the total market share in 2025. Kuwait’s extremely hot climatic conditions, increasing awareness regarding hydration and wellness, and consumer concerns surrounding sugary beverage consumption continue to support strong bottled water demand. Premium bottled water, flavored hydration drinks, and vitamin-enriched water products are gaining traction among affluent and health-conscious consumers. Functional beverages, including energy drinks, sports drinks, and nutritional beverages, are also emerging as high-growth sub-segments due to rising fitness awareness and changing lifestyle preferences.

Dairy products, confectionery, bakery products, and specialty beverages are witnessing strong premiumization trends across Kuwait’s high-income consumer base. Consumers are increasingly demanding imported gourmet chocolates, artisanal bakery products, specialty coffee, and organic dairy products with clean-label ingredients. Premium dairy products such as Greek yogurt, probiotic drinks, and protein-fortified milk are experiencing rising demand due to growing focus on wellness and nutritional value. In addition, plant-based food categories, including oat milk, almond milk, and vegan snacks, are gradually expanding within urban retail channels as consumers increasingly adopt healthier dietary patterns.

Distribution Channel Insights

Hypermarkets and supermarkets remain the leading distribution channel in the Kuwait food and drink market, accounting for approximately 46% of total market sales in 2025. The dominance of this segment is driven by extensive product assortments, strong availability of imported international brands, competitive promotional pricing, and well-established retail infrastructure across Kuwait City, Salmiya, Hawalli, and other urban areas. Large retail chains continue to expand shelf space dedicated to premium imported foods, organic products, frozen foods, and convenience-oriented meal categories. Investments in refrigeration systems, automated inventory management, and in-store customer engagement technologies are further strengthening organized retail growth. Convenience stores continue to maintain strong demand in densely populated urban locations due to quick accessibility and extended operating hours. These outlets are particularly important for impulse purchases, beverages, snacks, dairy products, and ready-to-consume food items. Rising urban mobility and changing consumption habits are supporting the expansion of neighborhood convenience retail formats across residential and commercial districts.

Online grocery and e-commerce platforms are emerging as the fastest-growing distribution segment, supported by increasing smartphone penetration, digital payment adoption, and rapid delivery services. Consumers are increasingly shifting toward app-based grocery purchasing due to convenience, broader product availability, personalized promotions, and time savings. Retailers are heavily investing in AI-powered inventory systems, last-mile delivery infrastructure, and omnichannel retail strategies to strengthen digital competitiveness. Subscription grocery models, quick-commerce platforms, and cloud-based food retail operations are expected to become increasingly important growth drivers over the forecast period. Specialty stores are also gaining traction within premium organic foods, imported gourmet products, nutritional supplements, and health-focused categories. Rising demand for niche dietary products such as gluten-free foods, keto-friendly snacks, vegan products, and functional beverages is supporting the growth of specialized food retail formats targeting affluent and health-conscious consumers.

Consumer Type Insights

Residential and household consumers account for the largest share of demand in the Kuwait food and drink market, supported by high per capita food expenditure, premium consumption habits, and strong retail grocery spending patterns. Household food consumption continues to rise due to increasing urbanization, population growth, and growing preference for packaged and convenience-oriented products. Consumers are increasingly allocating larger portions of discretionary income toward premium imported foods, healthier beverages, and ready-to-eat meal categories. Expatriate consumers contribute more than 55% of total food demand in Kuwait and remain one of the most influential consumer groups shaping the market landscape. The country’s large expatriate population drives substantial demand for ethnic food products, imported spices, rice, frozen foods, packaged grocery items, and international cuisine categories. Indian, Filipino, Egyptian, and broader Asian food products continue to witness strong demand across supermarkets, specialty stores, and foodservice establishments due to Kuwait’s highly multicultural population structure.

Health-conscious consumers represent one of the fastest-growing consumer segments within the market. Rising awareness regarding obesity, diabetes, cardiovascular health, and nutritional wellness is encouraging consumers to shift toward low-sugar beverages, organic foods, functional snacks, clean-label dairy products, and protein-enriched nutrition products. Younger demographics, particularly millennials and Gen Z consumers, are increasingly prioritizing fitness-oriented food choices and wellness-focused consumption patterns. Premium and luxury consumers are also contributing strongly to market growth through rising demand for gourmet packaged foods, artisanal bakery products, imported confectionery, premium dairy products, specialty coffee, and high-end dining experiences. Kuwait’s affluent consumer base continues to support strong growth in luxury food retail and premium imported product categories, particularly across urban centers and upscale retail outlets.

End-Use Insights

Retail household consumption remains the dominant end-use segment in the Kuwait food and drink market, accounting for nearly 61% of total market demand in 2025. Rising grocery expenditure, increasing preference for home consumption, and growing demand for packaged convenience foods continue to drive growth in this segment. Consumers are increasingly purchasing ready-to-cook meals, frozen products, packaged snacks, dairy products, and bottled beverages for in-home consumption, particularly through organized retail and digital grocery platforms. The hotels, restaurants, and cafés (HORECA) segment is currently among the fastest-growing end-use industries, supported by rapid café culture expansion, tourism recovery, rising entertainment spending, and increasing demand for international dining experiences. Kuwait’s growing preference for premium café chains, quick-service restaurants, and fine dining establishments is significantly boosting foodservice demand. Younger consumers are increasingly driving demand for specialty coffee, gourmet desserts, artisanal bakery products, and international fast-food concepts, accelerating growth across the HORECA sector.

Institutional catering demand from healthcare facilities, corporate offices, educational institutions, and government establishments is also increasing steadily. Rising employment levels, expanding educational infrastructure, and increasing healthcare investments are supporting long-term demand for bulk food procurement and catering services. Corporate catering and meal subscription services are witnessing growing adoption across urban business centers. Export-oriented demand for halal-certified packaged foods, dairy products, and processed beverages is gradually expanding across GCC markets. Kuwait-based food manufacturers and distributors are increasingly targeting regional export opportunities in Saudi Arabia, the UAE, Bahrain, and Qatar, particularly within premium halal food and processed dairy categories.

Explore more data points, trends and opportunities Download Free Sample Report

Kuwait Food and Drink Market Segmentations

By Product Category

- Packaged and Processed Foods

- Dairy Products

- Bakery and Confectionery

- Meat, Poultry, and Seafood

- Snacks and Savory Foods

- Bottled Water

- Carbonated Soft Drinks

- Functional and Energy Drinks

- Tea and Coffee

- Fresh and Organic Foods

By Distribution Channel

- Hypermarkets and Supermarkets

- Convenience Stores

- Traditional Grocery Stores

- Online Retail and E-Commerce Platforms

- Specialty Stores

- Foodservice and Institutional Sales

By Consumer Type

- Residential and Household Consumers

- Expatriate Consumers

- Health-Conscious Consumers

- Premium and Luxury Consumers

- Institutional Buyers

By End Use

- Retail Household Consumption

- Hotels, Restaurants, and Cafés (HORECA)

- Corporate and Institutional Catering

- Healthcare Institutions

- Educational Institutions

- Aviation and Travel Catering

Regional Insights

Middle East & Africa

The Middle East & Africa region dominates the Kuwait food and drink market ecosystem due to strong GCC trade integration, high per capita food expenditure, and substantial regional demand for imported food products. Kuwait, Saudi Arabia, and the UAE remain the primary consumption hubs for packaged foods, bottled beverages, dairy products, and premium grocery categories. Saudi Arabia contributes significantly to regional food trade volumes due to its large population base and expanding retail sector, while the UAE serves as a major logistics and re-export hub for premium imported foods across the Gulf region.

Regional growth is being driven by rising disposable incomes, rapid urbanization, tourism expansion, and increasing adoption of convenience-oriented food consumption patterns. The expansion of organized retail chains, café culture, and quick-service restaurant networks across GCC countries continues to accelerate food and beverage demand. Government-led food security initiatives, investments in strategic food reserves, and improvements in cold-chain logistics are also strengthening regional market growth. Additionally, younger consumers across the Gulf are increasingly demanding healthier food products, specialty beverages, and premium international brands, further driving premiumization trends across the region.

Asia-Pacific

Asia-Pacific represents the fastest-growing supplier region for Kuwait’s food imports, led by India, China, Thailand, Malaysia, and Indonesia. India remains one of Kuwait’s largest suppliers of rice, spices, frozen foods, tea products, and packaged grocery items due to strong expatriate-driven demand and long-standing trade relationships. China continues expanding exports of processed foods, canned goods, food ingredients, and food processing equipment into GCC markets.

The region’s growth is supported by competitive manufacturing costs, large-scale agricultural production capabilities, and improving trade connectivity with Gulf countries. Expanding halal food manufacturing in Southeast Asia is also strengthening exports into Kuwait and neighboring GCC markets. Rising production capacity, lower product costs, and increasing investments in food processing technologies are enabling Asia-Pacific suppliers to strengthen their position within Kuwait’s import-driven food ecosystem. In addition, growing demand for Asian cuisine and ethnic food products among expatriate consumers continues to support import growth from the region.

Europe

European countries such as Italy, France, Germany, the Netherlands, and Switzerland remain major suppliers of premium dairy products, chocolates, bakery ingredients, gourmet foods, confectionery, and specialty beverages to Kuwait. European brands benefit from strong consumer preference for authenticity, premium quality, and imported luxury food products among Kuwait’s affluent population.

Growth in European food exports to Kuwait is being driven by increasing premiumization trends, rising demand for organic and clean-label products, and growing consumer interest in artisanal and gourmet food categories. European manufacturers are also benefiting from strong brand recognition in specialty coffee, luxury confectionery, premium dairy, and bakery products. The expansion of premium supermarkets and gourmet retail outlets across Kuwait is further supporting demand for imported European food brands.

North America

The United States remains an important supplier of processed foods, cereals, sauces, packaged snacks, frozen foods, and branded beverages to Kuwait. American fast-food and quick-service restaurant chains continue to maintain strong market penetration across Kuwait, significantly contributing to foodservice sector growth.

Regional growth is driven by strong consumer preference for international food brands, increasing popularity of American-style dining concepts, and rising demand for convenience-oriented packaged foods. The expansion of quick-service restaurants, café chains, and entertainment-driven dining experiences is also supporting continued demand for North American food products. Additionally, growing consumer interest in functional beverages, protein-rich snacks, and sports nutrition products is strengthening imports from the U.S. food industry.

Latin America

Latin America plays an important role in Kuwait’s meat, poultry, sugar, and coffee supply chain, particularly through exports from Brazil and Argentina. Brazil remains one of the leading exporters of poultry and halal meat products to GCC markets due to its large-scale production capabilities and strong halal certification infrastructure.

Regional growth is being supported by rising demand for affordable protein sources, increasing consumption of processed meat products, and expanding coffee imports across Kuwait’s café and foodservice sectors. Competitive agricultural production costs and expanding trade partnerships with GCC countries are also helping Latin American exporters strengthen their presence within Kuwait’s food import ecosystem.

Key Players in the Kuwait Food and Drink Market

- Nestlé S.A.

- PepsiCo Inc.

- The Coca-Cola Company

- Unilever PLC

- Americana Restaurants International PLC

- Kuwait Dairy Company (KDD)

- Almarai Company

- Agthia Group PJSC

- Mondelez International

- Danone S.A.

- Kraft Heinz Company

- Kuwait Flour Mills & Bakeries Co.

- Kout Food Group

- JBS S.A.

- Mars Incorporated