King Arthur Bread Flour (Bulk) Market Size

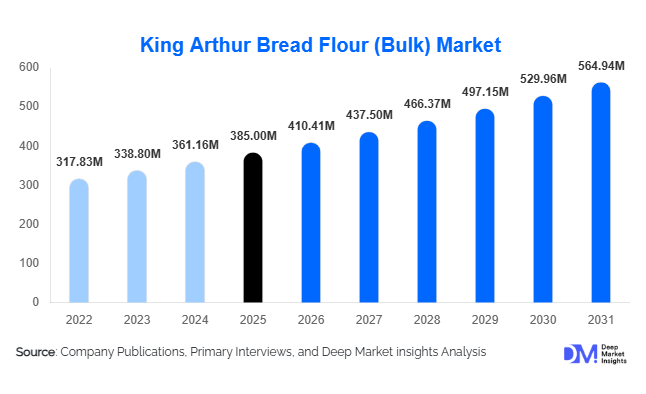

According to Deep Market Insights,the global King Arthur bread flour (bulk) market size was valued at USD 385 million in 2025 and is projected to grow from USD 410.41 million in 2026 to reach USD 564.94 million by 2031, expanding at a CAGR of 6.6% during the forecast period (2026–2031). The market growth is primarily driven by increasing demand for high-protein flour in commercial and artisan bakeries, rising preference for premium unbleached and organic flour, and expanding institutional procurement across North America and export markets. Growing global interest in sourdough, European-style breads, and specialty pizza crusts has strengthened demand for consistent, performance-grade bulk flour. Long-term supply contracts, stable foodservice recovery, and premiumization trends across bakery applications are further reinforcing steady value growth in the bulk segment.

Key Market Insights

- High-gluten bread flour dominates product demand, accounting for nearly 38% of total market share in 2025 due to its essential role in artisan and commercial bread production.

- Commercial bakeries represent the largest end-use segment, contributing approximately 48% of global demand through long-term procurement contracts.

- North America leads the global market, holding around 64% share in 2025, supported by strong brand recognition and established bakery infrastructure.

- Asia-Pacific is the fastest-growing region, expanding at nearly 8% CAGR, driven by rising café culture and premium bakery chains.

- Organic bulk flour is outpacing conventional variants, benefiting from clean-label and sustainability-driven purchasing trends.

- Direct-to-industrial distribution channels dominate, accounting for nearly 45% of market sales due to volume-based contracts.

What are the latest trends in the King Arthur bread flour bulk market?

Premiumization and Protein Standardization

Bulk flour buyers are increasingly prioritizing consistent protein content and baking performance. High-gluten flour variants with 12.7–13.5% protein content are gaining preference in artisan bread and pizza segments. Industrial bakeries are seeking reliable dough elasticity and fermentation tolerance, pushing demand for premium standardized blends. Precision milling technologies and protein calibration systems are being integrated to ensure batch consistency, particularly for export markets where uniformity is critical. This trend has allowed suppliers to maintain price premiums of 15–25% over commodity flour benchmarks.

Growth of Organic and Clean-Label Bulk Procurement

Certified organic bread flour is gaining traction across institutional buyers and specialty bakeries. Organic bulk flour commands 20–30% higher pricing compared to conventional variants, contributing disproportionately to revenue growth. Clean-label requirements and sustainability certifications are influencing purchasing decisions. Buyers are increasingly requesting traceability documentation, regenerative wheat sourcing, and non-GMO verification to align with evolving consumer preferences.

What are the key drivers in the King Arthur bread flour bulk market?

Expansion of Artisan and Specialty Bakeries

The global bakery industry continues expanding at approximately 5–6% annually, with artisan bread growing faster than industrial packaged bread. Rising consumer demand for sourdough, brioche, ciabatta, and European-style loaves requires high-protein flour for structural integrity. This shift has directly boosted bulk procurement volumes among commercial and craft bakeries worldwide.

Institutional and Export-Driven Demand

Institutional buyers including schools, hospitals, and foodservice providers are securing long-term supply contracts for premium flour to ensure quality consistency. Export demand from Japan, South Korea, and the UAE for high-protein North American flour is also contributing to growth. Bulk shipments through 25–50 lb commercial packs and tote bags have increased in line with global foodservice recovery.

What are the restraints for the global market?

Wheat Price Volatility

Fluctuating wheat prices significantly impact production costs and margins. High-protein wheat premiums create procurement risk, particularly during supply chain disruptions or adverse weather events. Margin pressures intensify when contract pricing lags raw material cost increases.

Private Label Competition

Large industrial bakeries increasingly explore private-label sourcing agreements to reduce costs. This trend can limit premium brand penetration in bulk industrial contracts, particularly in cost-sensitive markets.

What are the key opportunities in the King Arthur bread flour bulk industry?

Expansion into Asia-Pacific Artisan Markets

Rapid growth in café chains and specialty bakeries across Japan, South Korea, India, and Australia presents strong export opportunities. Establishing regional distribution hubs can reduce logistics costs and enhance responsiveness to demand.

Technology-Integrated Contract Supply Models

AI-driven demand forecasting and automated replenishment systems for large bakery clients represent a key opportunity. Integrating digital procurement platforms can enhance long-term contract retention and operational efficiency.

Product Type Insights

High-gluten bread flour remains the leading product category, accounting for nearly 38% of total revenue share in 2025. Its dominance is primarily driven by the expanding demand for premium-quality artisan bread, Neapolitan-style pizza crusts, bagels, and specialty fermented dough applications that require superior protein strength and gluten elasticity. Commercial bakeries and quick-service restaurant chains increasingly prefer high-gluten variants due to consistent dough performance, higher yield efficiency, and improved texture control in automated production environments. In addition, the growth of craft baking culture and the rising consumer preference for chewy, structured bread textures continue to reinforce the segment’s leadership position.

Organic bread flour represents the fastest-growing sub-segment, expanding at over 8% annually. Growth is supported by rising consumer inclination toward clean-label ingredients, non-GMO sourcing, and sustainable agricultural practices. Premium pricing power and expanding retail visibility of organic bakery products are further accelerating adoption among artisanal and specialty bakeries. Meanwhile, whole wheat and specialty artisan variants are gaining traction as health-conscious consumers increasingly demand fiber-rich and nutritionally enhanced bread options. Craft bakeries are leveraging these variants to differentiate through texture, flavor complexity, and perceived health benefits, contributing to steady diversification within the product landscape.

Packaging Format Insights

The 25–50 lb commercial packaging format dominates bulk sales, capturing approximately 42% market share in 2025. This format is widely preferred by mid-scale commercial bakeries due to its optimal balance between operational convenience, manageable storage requirements, and cost efficiency. The segment’s leadership is further supported by standardized palletization, reduced product handling loss, and compatibility with semi-automated bakery production systems.

Bulk tote bags ranging from 500–1,000 kg are experiencing increasing adoption among large industrial processors and contract manufacturers. The primary growth driver for this format is logistics optimization, including lower per-unit transportation costs, reduced packaging waste, and improved inventory management efficiency. Large-scale frozen dough producers and industrial bread manufacturers increasingly rely on bulk tote systems to streamline material flow and minimize downtime in continuous production facilities.

End-Use Industry Insights

Commercial bakeries represent the largest end-use segment, accounting for approximately 48% of total demand in 2025. The segment’s leadership is driven by high-volume bread production, standardized product lines, and long-term procurement contracts that ensure consistent supply. The expansion of supermarket in-store bakeries and private-label bread manufacturing continues to strengthen demand within this segment. Volume stability and recurring purchasing cycles provide predictable revenue streams for flour suppliers.

Artisan bakeries are the fastest-growing end-use category, expanding at nearly 7–8% annually. Growth is supported by consumer preference for handcrafted, small-batch bread products and premium baked goods with authentic fermentation techniques. The rise of specialty cafés and neighborhood bakeries in urban centers is further accelerating demand for high-protein and specialty flour variants. Industrial processed food manufacturers, including frozen dough producers and quick-service restaurant suppliers, contribute significantly through contract-based bulk procurement, benefiting from product standardization and scale efficiencies. Institutional buyers such as schools, hospitals, and hospitality chains provide stable, recession-resilient demand due to consistent foodservice requirements.

Distribution Channel Insights

Direct-to-industrial buyers dominate the distribution landscape with nearly 45% market share, reflecting the prevalence of volume-driven supply agreements and predictable procurement cycles. Long-term contracts between flour millers and commercial bakery chains enhance supply chain stability and pricing transparency. This channel benefits from reduced intermediary costs and efficient logistics coordination.

Foodservice wholesalers account for a substantial portion of mid-scale bakery distribution, particularly among independent and regional bakeries that require flexible order volumes. Meanwhile, B2B e-commerce platforms are gradually expanding their reach among smaller bakeries and emerging food entrepreneurs. Digital procurement systems improve price comparison, streamline repeat orders, and enhance accessibility for niche flour variants, contributing to gradual channel diversification.

| By Product Type | By End-Use Industry | By Packaging Format | By Distribution Channel |

|---|---|---|---|

|

|

|

|

Regional Insights

North America

North America holds approximately 64% of the global market share in 2025, led predominantly by the United States. Regional dominance is driven by a strong artisan baking culture, well-established commercial bakery infrastructure, and high per capita bread consumption. The presence of advanced milling technology, integrated grain supply chains, and efficient logistics networks further supports market leadership. Institutional demand from schools, hospitality chains, and foodservice operators provides volume stability. Canada contributes through cross-border trade efficiencies and growth in specialty bakery segments, while ongoing product innovation in clean-label and organic bread offerings continues to stimulate premium demand across the region.

Europe

Europe accounts for roughly 14% of global market share, with demand concentrated in the United Kingdom, Germany, and France. Regional growth is supported by strong consumer preference for specialty breads, sourdough varieties, and premium bakery craftsmanship. Although domestic flour milling competition remains intense, imported high-protein and specialty flours maintain niche demand among artisan and high-end bakery segments. Regulatory emphasis on quality standards and traceability further shapes procurement decisions. The increasing popularity of organic and heritage grain products across Western Europe also contributes to moderate yet stable expansion.

Asia-Pacific

Asia-Pacific holds nearly 12% market share but represents the fastest-growing region, expanding at approximately 8% CAGR. Growth is fueled by rising urbanization, westernization of diets, and rapid expansion of café chains and quick-service restaurants. Japan and South Korea remain major importers of high-protein flour for premium bakery applications, supported by strong consumer demand for specialty bread products. In India and Australia, expanding middle-class populations, increasing disposable income, and the proliferation of artisanal bakeries are accelerating consumption of high-gluten and specialty flour variants. Investments in modern retail infrastructure and cold-chain logistics further enhance regional growth prospects.

Middle East & Africa

The Middle East & Africa region represents approximately 6% of the global market. Growth is primarily driven by the United Arab Emirates and Saudi Arabia, where expanding hospitality sectors, tourism activity, and premium bakery outlets stimulate demand for high-protein wheat flour. Limited domestic wheat production in several countries increases reliance on imports, particularly for specialty flour grades. Rising population levels, urban foodservice expansion, and government initiatives supporting food security infrastructure also contribute to gradual market development across key urban centers.

Latin America

Latin America accounts for roughly 4% of the global market, led by Mexico and Brazil. Regional growth is supported by the steady expansion of processed food industries, rising bakery chain penetration, and increasing urban consumption of packaged bread products. Improvements in retail distribution networks and modernization of food processing facilities are strengthening procurement volumes. While growth remains moderate compared to Asia-Pacific, expanding middle-income populations and evolving dietary patterns continue to create incremental demand for specialty and high-protein flour products across major metropolitan areas.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the King Arthur Bread Flour (Bulk) Market

- King Arthur Baking Company

- Ardent Mills

- ADM

- General Mills

- Cargill

- Conagra Brands

- Gruma

- Associated British Foods

- Bay State Milling Company

- Bob's Red Mill

- Hodgson Mill

- Siemer Milling Company

- Mennel Milling Company

- Wilmar International

- Olam Group