Juice Testing Market Size

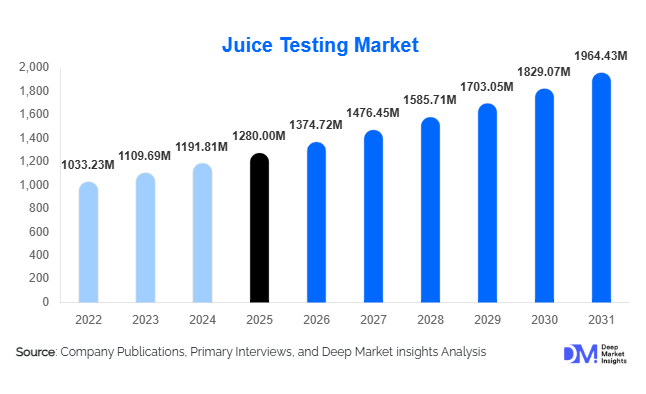

According to Deep Market Insights, the global juice testing market size was valued at USD 1,280 million in 2025 and is projected to grow from USD 1,374.72 million in 2026 to reach USD 1,964.43 million by 2031, expanding at a CAGR of 7.4% during the forecast period (2026–2031). The juice testing market growth is primarily driven by stringent global food safety regulations, rising export-oriented fruit juice production, and increasing demand for authenticity and adulteration detection in premium and organic beverages. Growing consumer awareness regarding pesticide residues, microbial contamination, and label accuracy has further strengthened regulatory scrutiny, making testing services a critical component of the global beverage value chain.

Key Market Insights

- Microbiological testing dominates the market, accounting for nearly 38% of total revenue in 2025 due to mandatory pathogen screening requirements.

- Third-party testing laboratories lead the service model segment, holding over 60% share as manufacturers increasingly outsource compliance verification.

- North America holds the largest regional share (32%), driven by strict regulatory frameworks and high juice consumption.

- Asia-Pacific is the fastest-growing region, expanding at nearly 9% CAGR due to rising juice exports from China and India.

- Authenticity and adulteration testing is the fastest-growing testing type, supported by rising food fraud incidents globally.

- Chromatography-based technologies remain the leading analytical platform, widely used for pesticide residue and additive analysis.

What are the latest trends in the juice testing market?

Growing Emphasis on Authenticity & Adulteration Detection

Juice adulteration through added sugars, synthetic coloring agents, and dilution has increased regulatory vigilance worldwide. As a result, isotope ratio mass spectrometry, advanced chromatography, and spectroscopy-based origin verification techniques are witnessing rapid adoption. Premium and organic juice brands are investing heavily in authenticity validation to protect brand equity. Clean-label positioning and traceability claims are pushing manufacturers to conduct routine authenticity testing beyond basic compliance requirements. This trend is particularly strong in export-driven markets where verification of fruit origin and absence of adulterants is mandatory for market entry.

Rapid Testing & Lab Automation Integration

Testing laboratories are adopting PCR-based rapid pathogen detection, automated chromatography platforms, and AI-enabled sample tracking systems to reduce turnaround time. Automation improves throughput, minimizes human error, and enhances compliance documentation. Digital reporting systems and blockchain-enabled traceability platforms are increasingly integrated into laboratory information management systems (LIMS), improving transparency for multinational beverage companies. These advancements are enabling testing providers to scale operations efficiently while maintaining margin stability.

What are the key drivers in the juice testing market?

Stringent Food Safety Regulations

Regulatory authorities across North America, Europe, and Asia have strengthened food safety mandates requiring mandatory microbial, pesticide residue, and heavy metal testing for fruit juices. Preventive control frameworks and international export compliance standards have significantly increased the frequency of testing per production batch. Regulatory enforcement remains the most structural and long-term growth driver for this market.

Rising Global Juice Consumption & Product Innovation

The global fruit juice industry exceeds USD 160 billion in value, with growing demand for functional, fortified, and cold-pressed juices. Each new product formulation requires nutritional validation, stability studies, and contaminant screening. Functional juices enriched with vitamins, botanicals, and probiotics have particularly increased testing complexity and frequency, positively impacting testing revenues.

What are the restraints for the global market?

High Capital Investment in Advanced Equipment

Advanced analytical instruments such as GC-MS, ICP-MS, and NMR require multi-million-dollar investments. Smaller laboratories often face financial barriers in adopting high-end equipment, limiting market entry and expansion.

Pricing Pressure from Large Beverage Corporations

Major multinational beverage producers negotiate bulk testing contracts, compressing margins for testing service providers. Competitive pricing environments particularly affect commoditized microbiological testing services.

What are the key opportunities in the juice testing industry?

Export-Driven Compliance Expansion

Emerging fruit-exporting economies such as Brazil, India, and Vietnam are expanding juice concentrate exports to North America and Europe. Export compliance mandates internationally accredited laboratory certifications, creating opportunities for private labs to establish regional facilities and public-private partnerships.

Growth in Organic & Cold-Pressed Juice Segment

Organic juice production requires pesticide residue testing and contamination monitoring at a higher frequency. Cold-pressed juices, with shorter shelf lives, require repeated microbial validation. These premium segments generate higher revenue per sample compared to conventional juice testing.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1280 Million |

| Market Size in 2026 | USD 1374.72 Million |

| Market Size in 2031 | USD 1964.43 Million |

| CAGR | 7.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Testing Type Insights

Microbiological testing leads the global juice testing market, accounting for approximately 38% of total revenue in 2025. The dominance of this segment is structurally driven by mandatory pathogen screening requirements across all commercial juice production batches. Regulatory authorities worldwide require routine testing for pathogens such as Salmonella, E. coli, and Listeria, particularly in ready-to-drink and cold-pressed juice formats that are more susceptible to contamination. The increasing consumption of minimally processed and preservative-free beverages has further elevated microbial risk exposure, compelling manufacturers to conduct more frequent batch-level testing. In addition, export shipments require pre-clearance microbial certification, reinforcing consistent demand.

Chemical testing represents the second-largest segment, driven by pesticide residue, heavy metal, and mycotoxin analysis. Stringent maximum residue limits (MRLs) imposed by North American and European regulators have significantly increased testing intensity for export-oriented producers. Authenticity and adulteration testing is the fastest-growing sub-segment, supported by rising food fraud incidents and growing premiumization of organic and not-from-concentrate juices. Techniques such as isotope ratio analysis and advanced spectroscopy are increasingly adopted to detect added sugars, synthetic colorants, and dilution practices.

Technology Insights

Chromatography-based platforms account for nearly 34% of total market revenue in 2025, making them the leading technology segment. High-Performance Liquid Chromatography (HPLC) and Gas Chromatography-Mass Spectrometry (GC-MS) are widely used for multi-residue pesticide screening, preservative detection, additive quantification, and mycotoxin profiling. The key driver behind chromatography’s leadership is its high sensitivity, regulatory acceptance, and versatility across multiple contaminant categories. Export-heavy markets particularly depend on chromatographic methods due to strict compliance documentation requirements.

PCR-based molecular diagnostics are gaining traction as a high-growth technology due to rapid pathogen detection capabilities, reducing turnaround time from days to hours. Immunoassay and rapid test kits are also expanding in smaller laboratories for preliminary screening; however, confirmatory testing continues to rely on advanced instrumentation platforms. Automation and laboratory information management systems (LIMS) integration are further improving efficiency and scalability in high-volume testing facilities.

Service Model Insights

Third-party contract laboratories dominate the service model landscape, holding approximately 62% of the 2025 market share. The primary driver for this leadership is regulatory acceptance and accreditation requirements, such as ISO/IEC 17025 certification, which many independent laboratories possess. Beverage manufacturers prefer accredited external labs to ensure neutrality, compliance, credibility, and global recognition of test reports. Outsourcing also enables cost optimization, as advanced analytical equipment requires substantial capital investment.

In-house laboratories are typically adopted by multinational beverage corporations for routine quality control and preliminary screening. However, confirmatory and export certification testing is often outsourced to maintain compliance integrity and reduce liability risk. Growing international trade in fruit concentrates and purees continues to strengthen demand for third-party testing partnerships.

End-Use Industry Insights

Juice manufacturers account for approximately 48% of total demand in 2025, making them the leading end-use segment. The segment’s dominance is driven by high production volumes, batch-level compliance requirements, and frequent product innovation in functional and fortified juices. Increasing launches of cold-pressed, organic, and immunity-boosting beverages have elevated testing frequency per SKU.

Private label beverage brands represent one of the fastest-growing sub-segments, expanding at an estimated 8–9% CAGR. Retail chains increasingly rely on third-party laboratories to validate product safety and label claims. Export-oriented producers in Brazil and India significantly drive testing demand due to stringent EU and U.S. import standards, which require multi-stage compliance testing before shipment clearance.

Explore more data points, trends and opportunities Download Free Sample Report

Juice Testing Market Segmentations

By Testing Type

- Microbiological Testing

- Chemical Testing

- Nutritional & Label Claim Verification

- Authenticity & Adulteration Testing

By Technology Platform

- Chromatography (HPLC, GC-MS)

- Spectroscopy (ICP-MS, FTIR, NMR)

- PCR & Molecular Diagnostics

- Immunoassay & Rapid Test Kits

By Service Model

- Third-Party Contract Testing Laboratories

- In-House Testing Laboratories

- On-Site & Mobile Testing Services

By End-Use Industry

- Juice Manufacturers

- Private Label & Retail Beverage Brands

- Exporters & Importers

- Government & Regulatory Agencies

By Juice Type

- Fruit Juices

- Vegetable Juices

- Cold-Pressed & Premium Juices

- Concentrates & Purees

- Functional & Fortified Juices

Regional Insights

North America

North America holds the largest share of the global juice testing market at approximately 32% in 2025. The United States dominates regional demand due to strict food safety enforcement, high per capita juice consumption, and advanced laboratory infrastructure. Regulatory frameworks emphasizing preventive controls and hazard analysis significantly increase testing frequency. The rapid growth of organic and cold-pressed juice brands further drives authenticity and pesticide residue testing demand. Canada contributes steadily to regional growth, particularly in premium and clean-label beverage categories.

Europe

Europe accounts for nearly 28% of global revenue, led by Germany, France, and the UK. The primary regional growth driver is the stringent enforcement of pesticide maximum residue limits (MRLs) and food fraud prevention policies. Europe remains a major importer of fruit juice concentrates from Latin America and Asia, increasing third-party compliance testing volumes at ports of entry. Strong consumer preference for organic and sustainably sourced beverages also elevates authenticity testing requirements. The region’s mature regulatory ecosystem ensures stable and recurring testing demand.

Asia-Pacific

Asia-Pacific represents around 26% of the global market and is the fastest-growing region, expanding at approximately 9% CAGR. China dominates concentrate exports and is investing heavily in food safety laboratory infrastructure to meet international trade standards. India is rapidly strengthening its testing capabilities under agri-export promotion initiatives, driving domestic and export-oriented demand. Rising middle-class consumption of packaged juices and expanding beverage manufacturing capacity across Southeast Asia further support regional growth. Increased government scrutiny following past food safety incidents has also heightened compliance requirements.

Latin America

Latin America holds approximately 9% market share, led by Brazil, the world’s largest orange juice exporter. The region’s growth is primarily export-driven, with producers conducting extensive pesticide residue, heavy metal, and microbial testing to meet European and North American import standards. Expanding fruit cultivation areas and processing capacity are expected to sustain compliance testing demand over the forecast period.

Middle East & Africa

The Middle East & Africa region accounts for nearly 5% of global revenue. Growth is driven by rising juice import volumes in the UAE and Saudi Arabia, which require strict compliance verification. South Africa serves as a regional production and export hub, contributing to domestic testing demand. Increasing urbanization, growth in packaged beverage consumption, and government-led food safety modernization programs are gradually strengthening the region’s testing ecosystem.

Key Players in the Juice Testing Market

- Eurofins Scientific

- SGS SA

- Bureau Veritas

- Intertek Group plc

- ALS Limited

- Mérieux NutriSciences

- TUV SUD

- TUV Rheinland

- AsureQuality

- Campden BRI

- Neogen Corporation

- Microbac Laboratories

- Fera Science Ltd

- IRCLASS Systems and Solutions

- Romer Labs