Japanese Curry Market Size

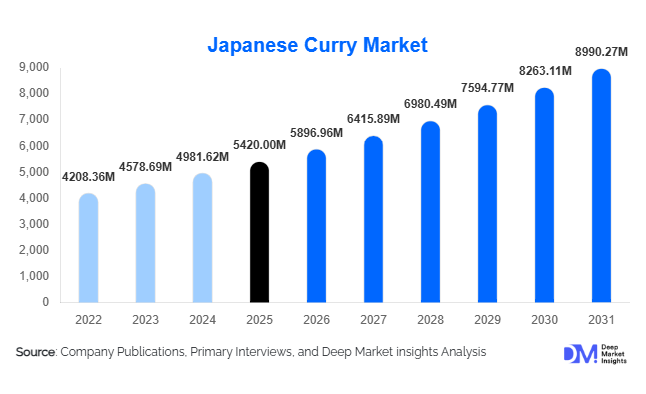

According to Deep Market Insights, the global Japanese curry market size was valued at USD 5,420 million in 2025 and is projected to grow from USD 5,896.96 million in 2026 to reach USD 8,990.27 million by 2031, expanding at a CAGR of 8.8% during the forecast period (2026–2031). The Japanese curry market growth is primarily driven by the increasing globalization of Japanese cuisine, rising demand for convenient ready-to-eat meals, and growing consumer preference for mild, adaptable flavor profiles suitable across diverse geographies.

Key Market Insights

- Japanese curry is gaining global popularity as an entry-level Asian cuisine due to its mild taste and versatility across meat, seafood, and plant-based dishes.

- Ready-to-eat (RTE) and retort-pack curry products are expanding rapidly, driven by urbanization and demand for convenient meal solutions.

- Asia-Pacific dominates the market, with Japan contributing the largest share due to strong domestic consumption.

- North America is emerging as a key growth region, supported by rising interest in Japanese cuisine and expansion of Asian retail chains.

- Plant-based and health-oriented variants, including vegan and low-sodium curry, are witnessing strong demand growth.

- E-commerce and global retail expansion are enhancing accessibility of Japanese curry products across non-traditional markets.

What are the latest trends in the Japanese curry market?

Premiumization and Health-Focused Innovation

The Japanese curry market is witnessing a strong shift toward premium and health-oriented offerings. Manufacturers are introducing organic, gluten-free, and plant-based curry variants to cater to evolving consumer preferences. Functional ingredients, reduced sodium formulations, and clean-label products are gaining traction, particularly in developed markets. Premium curry products featuring unique ingredients such as fruits (apple, honey) or regional spices are also expanding shelf presence. This trend is aligned with the broader global movement toward healthier and more transparent food consumption, encouraging brands to differentiate through quality and nutritional value.

Expansion of Ready-to-Eat and Convenience Formats

Convenience remains a major trend shaping the market, with ready-to-eat Japanese curry products witnessing rapid adoption. Retort packaging technology has enabled long shelf life without compromising taste or texture, making these products ideal for export markets. Consumers are increasingly opting for instant meal solutions due to busy lifestyles, particularly in urban areas. Meal kits and subscription-based food services are also integrating Japanese curry into their offerings, further boosting demand. The ease of preparation and consistent flavor profile make these products highly appealing across both household and foodservice segments.

What are the key drivers in the Japanese curry market?

Growing Global Popularity of Japanese Cuisine

The rising international appeal of Japanese cuisine is a major driver for the Japanese curry market. While sushi and ramen have traditionally dominated global awareness, Japanese curry is increasingly recognized as a comforting and accessible dish. Its mild flavor and adaptability make it suitable for a wide range of consumers, including those unfamiliar with traditional Asian spices. The expansion of Japanese restaurant chains and cultural exchange through media and tourism are further accelerating demand worldwide.

Rising Demand for Convenience Foods

Urbanization and fast-paced lifestyles are driving the demand for convenient meal solutions, positioning Japanese curry as an ideal option. Ready-to-eat and instant curry products offer quick preparation while maintaining authentic taste, making them highly attractive to working professionals and younger consumers. The growing penetration of supermarkets, hypermarkets, and online grocery platforms has also improved product accessibility, supporting market expansion.

What are the restraints for the global market?

Dependence on Raw Material Supply Chains

The Japanese curry market relies on a range of spices, oils, and processed ingredients, making it vulnerable to fluctuations in raw material prices. Supply chain disruptions can impact production costs and pricing stability, posing challenges for manufacturers operating in highly competitive markets.

Limited Awareness in Emerging Markets

Despite growing popularity, Japanese curry still faces limited awareness in several emerging regions compared to other Asian cuisines such as Chinese and Indian. This necessitates significant marketing investments and consumer education efforts to drive adoption, particularly in price-sensitive markets.

What are the key opportunities in the Japanese curry industry?

Growth of Plant-Based and Specialty Products

The increasing shift toward plant-based diets presents a major opportunity for the Japanese curry market. Vegan and allergen-free curry products are gaining traction among health-conscious consumers. Manufacturers can leverage this trend by innovating with alternative ingredients and expanding product portfolios to cater to niche dietary requirements.

Expansion into Emerging Markets

Emerging economies in Asia-Pacific, Latin America, and the Middle East offer significant growth potential due to rising disposable incomes and increasing exposure to international cuisines. Localization strategies, including adapting flavors to regional preferences, can help companies penetrate these markets more effectively and drive long-term growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5420.00 Million |

| Market Size in 2026 | USD 5896.96 Million |

| Market Size in 2031 | USD 8990.27 Million |

| CAGR | 8.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global Japanese curry market exhibits a well-diversified product structure, with curry roux blocks emerging as the dominant category, accounting for approximately 38% of the global market share in 2025. This dominance is primarily attributed to their exceptional convenience, long shelf stability, and ability to deliver consistent taste profiles that closely replicate traditional Japanese home-cooked curry. Curry roux blocks are deeply embedded in household cooking culture, particularly in Japan, where they are considered a pantry essential. Their pre-measured formulation eliminates the complexity of spice blending, making them highly attractive to time-constrained consumers in urban households across global markets.Ready-to-eat curry products represent the fastest-growing segment within the product type category. This growth is fueled by rapid urbanization, busy consumer lifestyles, and the expansion of convenience retail formats such as convenience stores and online grocery delivery platforms. The increasing penetration of microwaveable meals and shelf-stable packaged foods has also significantly boosted demand. These products are particularly popular among working professionals, students, and single-person households who prioritize speed and minimal preparation effort. The expansion of global food delivery ecosystems has further reinforced this trend, making ready-to-eat Japanese curry more accessible outside traditional restaurant settings.Curry powders and curry pastes continue to maintain stable demand, especially within foodservice and culinary customization segments. These forms are widely used by professional chefs and restaurant operators who require flexibility in flavor intensity and ingredient composition. The growth of fusion cuisine restaurants and Japanese-inspired dining establishments has further supported demand for these adaptable product formats. Their use in institutional catering and processed food manufacturing also highlights their importance in large-scale food production systems where standardized yet customizable flavor profiles are required.

Application Insights

Household consumption remains the largest application segment in the Japanese curry market, contributing nearly 55% of total global demand. The strong cultural integration of curry as a comfort food in Japanese households, combined with its ease of preparation and affordability, continues to reinforce its dominance. The leading driver for this segment is the growing preference for home-cooked meals that balance taste, nutrition, and convenience. Increasing health awareness has also encouraged consumers to prepare meals at home rather than rely on external dining, further strengthening household demand.Foodservice applications represent a rapidly expanding segment, driven by the global proliferation of Japanese restaurants, casual dining chains, and quick-service outlets. The increasing popularity of Japanese cuisine worldwide has positioned curry as a key menu item beyond traditional sushi and ramen offerings. Restaurants are leveraging Japanese curry as a versatile dish that appeals to a broad consumer base due to its mild spice profile and comforting taste. The primary growth driver in this segment is the globalization of Japanese food culture and the rising demand for authentic Asian dining experiences in international markets.Institutional and industrial applications are also emerging as important contributors to market expansion. Meal kit providers, airline catering services, school meal programs, and processed food manufacturers are increasingly incorporating Japanese curry due to its scalability, cost efficiency, and consumer acceptance. The growing demand for standardized ready meals across institutional settings is reinforcing this trend, making Japanese curry a preferred choice for bulk food production systems.

Distribution Channel Insights

Supermarkets and hypermarkets continue to dominate the distribution landscape, accounting for approximately 42% of total market share. These retail formats provide consumers with extensive product variety, competitive pricing, and the ability to physically evaluate products before purchase. The primary driver for this segment is strong consumer trust in established retail chains, combined with the convenience of one-stop shopping experiences. The availability of both domestic and imported Japanese curry products in these stores has significantly enhanced product visibility and accessibility across global markets.Specialty Asian stores continue to play a crucial role in market expansion, particularly in regions with significant expatriate populations and multicultural consumer bases. These stores offer authenticity-driven product assortments that cater to niche consumer preferences. Their importance is especially evident in urban centers where demand for ethnic and international foods is high. Additionally, foodservice distributors and wholesale channels support bulk purchasing requirements for restaurants and institutional buyers, contributing to the overall distribution network diversity.

Ingredient Type Insights

Conventional Japanese curry products dominate the market with nearly 70% share, primarily due to their affordability, widespread availability, and strong consumer familiarity. These products are deeply rooted in traditional consumption patterns and remain the default choice for most households. The leading driver of this segment is cost-effectiveness combined with consistent flavor delivery, making it highly accessible across all income groups and geographic regions.However, the market is witnessing a noticeable shift toward organic and plant-based variants. This transformation is being driven by rising global health consciousness, increasing incidence of food allergies, and growing demand for clean-label products. Consumers are becoming more attentive to ingredient transparency, pushing manufacturers to reformulate products with natural spices, reduced additives, and plant-based alternatives. This trend is particularly strong in developed markets where wellness-oriented food consumption is a key lifestyle factor.Gluten-free and allergen-free Japanese curry products are also gaining traction, especially among consumers with dietary restrictions. The expansion of vegan and vegetarian populations globally has further encouraged innovation in plant-based curry formulations, which substitute traditional meat-based ingredients with legumes, tofu, or vegetable protein alternatives. These developments indicate a gradual but steady shift toward premiumization and functional food positioning within the Japanese curry market.

Explore more data points, trends and opportunities Download Free Sample Report

Japanese Curry Market Segmentations

By Product Type

- Curry Roux Blocks

- Curry Powder

- Ready-to-Eat (RTE) Japanese Curry

- Curry Paste

- Instant Curry Mixes

By Flavor Profile

- Mild

- Medium Hot

- Hot/Spicy

- Specialty Flavors

By Ingredient Type

- Conventional

- Organic

- Plant-Based/Vegan

- Gluten-Free

By Packaging Type

- Boxes

- Pouches

- Bottles/Jars

- Sachets

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail

- Specialty Asian Stores

- Foodservice Distributors

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global Japanese curry market, accounting for over 55% of total market share in 2025. Japan remains the core market, driven by deep cultural integration of curry into everyday diets and strong domestic brand presence. The leading growth driver in Japan is the continuous evolution of convenience food culture, supported by high urbanization and aging demographics seeking easy-to-prepare meals.China and South Korea represent significant growth markets within the region, fueled by increasing exposure to Japanese cuisine and rising disposable incomes. The rapid expansion of modern retail infrastructure and food delivery platforms has significantly improved product accessibility. In Southeast Asia, countries such as Thailand, Indonesia, and Vietnam are experiencing the fastest growth rates. This is primarily driven by expanding middle-class populations, increasing westernization of diets, and strong tourism-driven culinary exchange. The region’s growth is further supported by robust retail modernization and aggressive market entry strategies by Japanese food brands.

North America

North America holds approximately 18% of the global market share, with the United States serving as the primary demand center. The growth of this region is driven by increasing multicultural population diversity and rising consumer interest in Asian cuisines. Japanese curry is increasingly being incorporated into mainstream food culture through restaurant chains, fusion cuisine concepts, and packaged food retail expansion.The leading driver in North America is the rapid growth of Japanese restaurant chains and the expansion of Asian grocery retail formats. Additionally, the increasing penetration of e-commerce grocery platforms has made authentic Japanese curry products more accessible to mainstream consumers. Health-conscious consumers in the region are also contributing to demand for lower-sodium, organic, and plant-based curry variants.

Europe

Europe accounts for around 15% of the global market, with strong demand concentrated in the United Kingdom, Germany, and France. The region’s growth is largely driven by increasing openness to international cuisines and a well-established multicultural food culture. Consumers in Europe are increasingly experimenting with Japanese cuisine as part of broader culinary exploration trends.The primary growth driver in Europe is the rising demand for premium, organic, and clean-label food products. Health-conscious consumers are highly receptive to products that emphasize natural ingredients and sustainability. The presence of specialty Asian supermarkets and the growth of online ethnic food retailers have also contributed to improved product accessibility across the region.

Middle East & Africa

The Middle East & Africa region is witnessing gradual but steady growth, led by the United Arab Emirates, Saudi Arabia, and South Africa. The presence of large expatriate populations from Asia and increasing exposure to global culinary trends are key factors driving demand. Japanese curry is gaining popularity in urban dining environments, particularly within international hotels, premium restaurants, and food courts.The leading driver in this region is the rapid expansion of the hospitality and foodservice sector, combined with increasing retail modernization. Governments in several countries are also investing in tourism development, which indirectly boosts demand for diverse international cuisines. The growth of premium retail outlets and specialty food stores is expected to further enhance market penetration in the coming years.

Latin America

Latin America represents an emerging market for Japanese curry, with Brazil and Mexico leading regional demand. Increasing urbanization, rising middle-class income levels, and growing exposure to global food trends are driving gradual adoption. Japanese cultural influence, particularly through anime and tourism, has also played a role in increasing awareness of Japanese cuisine.The primary growth driver in this region is the expansion of urban retail infrastructure and the increasing popularity of international dining experiences among younger consumers. Although the market is still in its early development stage, steady growth is expected as distribution networks improve and consumer familiarity increases over the forecast period.

Key Players in the Japanese Curry Market

- House Foods Group

- S&B Foods Inc.

- Ajinomoto Co., Inc.

- Ezaki Glico Co., Ltd.

- Otsuka Foods Co., Ltd.

- Hachi Foods Co., Ltd.

- McCormick & Company

- Nissin Foods Holdings Co., Ltd.

- Kraft Heinz Company

- Ankee Food Co.

- Yamamori Co., Ltd.

- Daiichi Sankyo Foods

- Morinaga & Co., Ltd.

- Kikkoman Corporation

- Mizkan Holdings Co., Ltd.