Isoflavones Market Size

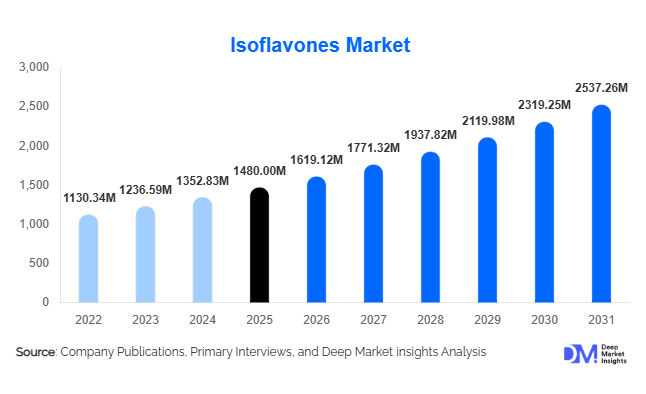

According to Deep Market Insights,the global isoflavones market size was valued at USD 1,480 million in 2025 and is projected to grow from USD 1,619.12 million in 2026 to reach USD 2,537.26 million by 2031, expanding at a CAGR of 9.4% during the forecast period (2026–2031). Market growth is primarily driven by rising adoption of plant-based bioactive ingredients, increasing demand for preventive healthcare solutions, and expanding applications of phytoestrogens across nutraceutical, functional food, pharmaceutical, and cosmetic industries. Growing consumer awareness regarding hormonal health, cardiovascular wellness, and bone health management continues to strengthen demand for naturally derived isoflavones globally.

Key Market Insights

- Dietary supplements remain the dominant application segment, supported by rising demand for menopause and hormonal health formulations worldwide.

- Soy-derived isoflavones account for the largest share of global production due to established supply chains and high genistein concentrations.

- Asia-Pacific leads global manufacturing and consumption, supported by strong soybean processing infrastructure and traditional dietary familiarity.

- Functional foods and beverages represent the fastest-growing application, driven by plant-based nutrition trends and clean-label product innovation.

- Bio-fermentation technologies are emerging as sustainable alternatives to agricultural sourcing, improving purity and supply stability.

- Cosmetics and personal care applications are expanding rapidly, leveraging antioxidant and anti-aging properties of isoflavones.

What are the latest trends in the isoflavones market?

Shift Toward Plant-Based Preventive Nutrition

Consumers are increasingly incorporating functional ingredients into daily diets to prevent chronic health conditions rather than relying solely on pharmaceutical treatments. Isoflavones, recognized for their phytoestrogenic and antioxidant properties, are gaining traction in preventive healthcare formulations. Supplement manufacturers are launching targeted solutions addressing menopause symptoms, bone density support, and cardiovascular wellness. Clean-label positioning and vegan-friendly claims further strengthen consumer acceptance. Product innovation now focuses on standardized extracts with improved absorption rates, allowing manufacturers to differentiate premium formulations in competitive nutraceutical markets.

Advancements in Extraction and Fermentation Technologies

Technological innovation is reshaping production processes within the isoflavones industry. Companies are adopting solvent-free extraction, enzymatic processing, and microbial fermentation technologies to enhance purity and bioavailability. Fermentation-based production reduces dependence on agricultural yield fluctuations while enabling consistent active compound concentrations. These advancements are particularly important for pharmaceutical and cosmetic applications that require standardized ingredient quality. Automation and digital monitoring in extraction facilities are also improving efficiency, lowering operational costs, and enabling scalable production aligned with growing global demand.

What are the key drivers in the isoflavones market?

Rising Demand for Women’s Health Supplements

The growing global population of women aged above 45 years is significantly driving demand for isoflavone-based supplements. Isoflavones are widely used as natural alternatives to hormone replacement therapies, supporting menopause symptom management and bone health. Increasing healthcare awareness and preference for plant-derived solutions are accelerating adoption across developed and emerging markets. Premium supplement brands are investing in clinical validation studies to strengthen efficacy claims and build consumer trust.

Growth of Plant-Based and Functional Food Industries

The rapid expansion of plant-based diets has encouraged food manufacturers to incorporate functional ingredients that provide both nutritional and health benefits. Isoflavones enhance product value by enabling heart-health and antioxidant claims. Fortified beverages, dairy alternatives, snack bars, and protein-based foods increasingly include isoflavone ingredients. As consumers prioritize natural wellness solutions, food companies are integrating bioactive compounds into mainstream products, expanding market reach beyond traditional supplements.

What are the restraints for the global market?

Regulatory Complexity Across Regions

Regulatory frameworks governing health claims and phytoestrogen usage vary widely across countries. Strict approval requirements in certain regions, particularly Europe, limit marketing flexibility and slow product launches. Manufacturers must invest heavily in clinical evidence and compliance documentation, increasing operational costs and extending commercialization timelines.

Volatility in Soybean Raw Material Prices

Isoflavone production remains largely dependent on soybean cultivation, making manufacturers vulnerable to agricultural price fluctuations. Climate variability, trade policies, and supply chain disruptions can significantly influence raw material costs. These factors create pricing pressure and margin uncertainty for producers relying heavily on soy-derived inputs.

What are the key opportunities in the isoflavones industry?

Expansion of Functional Food Fortification

The integration of isoflavones into everyday food products presents substantial growth opportunities. Food manufacturers are developing fortified beverages, cereals, and plant-based dairy alternatives enriched with bioactive compounds. Improved microencapsulation techniques now allow flavor-neutral incorporation, expanding usage across multiple food categories. This shift positions isoflavones as mainstream functional ingredients rather than niche supplement additives.

Development of Non-Soy and Fermented Isoflavones

Growing consumer concerns regarding allergens and genetically modified crops are encouraging diversification beyond soy sources. Red clover and fermentation-derived isoflavones offer new avenues for innovation. Biotechnology-driven production enables higher purity and sustainability credentials, attracting pharmaceutical and premium nutraceutical manufacturers seeking consistent ingredient quality.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1480 Million |

| Market Size in 2026 | USD 1619.12 Million |

| Market Size in 2031 | USD 2537.26 Million |

| CAGR | 9.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Source Insights

Soy-derived isoflavones continue to dominate the global isoflavones market, accounting for approximately 68% of total revenue in 2025. The segment’s leadership is primarily driven by the extensive availability of soybean raw materials, well-established global cultivation networks, and mature extraction technologies that enable cost-efficient large-scale production. High concentrations of bioactive compounds such as genistein and daidzein further strengthen soy’s commercial viability, making it the preferred source for nutraceutical, pharmaceutical, and functional food manufacturers. Additionally, strong supply chain integration across Asia-Pacific and North America ensures consistent quality and pricing stability, supporting widespread adoption. Red clover-derived isoflavones are gaining momentum within premium supplement categories due to their allergen-free positioning and appeal among consumers seeking non-soy alternatives. Meanwhile, fermentation-derived isoflavones are emerging as a high-growth niche, supported by advancements in biotechnology, precision fermentation processes, and sustainability-driven manufacturing approaches that reduce agricultural dependency while improving compound purity and bioavailability.

Type Insights

Genistein leads the isoflavones market with nearly 34% share of total demand, primarily driven by strong clinical evidence demonstrating benefits related to cardiovascular health, bone density maintenance, and menopausal symptom management. Increasing scientific validation and growing physician recommendations have enhanced consumer confidence, positioning genistein as the most commercially significant compound within the category. Mixed isoflavone complexes maintain strong adoption across dietary supplements due to their synergistic physiological effects, allowing manufacturers to deliver broad-spectrum health benefits through combined formulations. Daidzein and glycitein are witnessing increasing utilization in pharmaceutical research, functional nutrition, and fortified food products as companies diversify ingredient applications and invest in targeted health solutions. Expanding research into hormone balance, metabolic health, and antioxidant activity continues to widen the application scope of individual isoflavone compounds across multiple end-use industries.

Form Insights

Powdered isoflavones account for approximately 52% of global consumption, making them the leading product form due to superior stability, extended shelf life, and high formulation flexibility. Manufacturers favor powdered formats for their compatibility with capsules, tablets, sachets, protein blends, and functional food matrices, enabling efficient large-scale production and transportation. The versatility of powders also supports customized dosage formulations and improved manufacturing efficiency, reinforcing segment dominance. Capsules and tablets remain highly popular within finished dietary supplement products because they provide precise dosing, convenience, and strong consumer familiarity. Liquid extracts are gaining traction in functional beverages and ready-to-drink wellness products, where rapid absorption characteristics and ease of blending align with evolving consumer preferences for convenient health solutions.

Application Insights

Nutraceuticals and dietary supplements represent the leading application segment, accounting for approximately 46% of total market share. Growth is largely driven by rising consumer adoption of preventive healthcare practices, increasing aging populations worldwide, and growing awareness of plant-based alternatives for hormonal and cardiovascular wellness support. The shift toward self-directed health management and natural supplementation continues to strengthen demand within this segment. Functional food and beverage applications are emerging as the fastest-growing category, supported by increasing consumer demand for everyday wellness solutions integrated into regular diets. Manufacturers are incorporating isoflavones into dairy alternatives, fortified snacks, and health beverages to meet clean-label and plant-based product trends, expanding market penetration beyond traditional supplement formats.

End-Use Industry Insights

The dietary supplement industry remains the largest consumer of isoflavones, supported by sustained global expansion of the supplement sector, which exceeds USD 180 billion in value. Strong consumer preference for natural, plant-derived bioactive ingredients continues to drive ingredient incorporation across menopause support, heart health, and bone health formulations. Functional food manufacturers are rapidly increasing isoflavone usage as plant-based diets gain mainstream acceptance and consumers seek nutritional enhancement within daily food consumption. Cosmetic and personal care applications are also emerging strongly, with isoflavones incorporated into anti-aging and skin-rejuvenation formulations due to their antioxidant and phytoestrogen properties. In addition, export-oriented demand is strengthening global trade dynamics, as Asian producers supply standardized extracts to nutraceutical brands across North America and Europe, improving international supply integration and supporting consistent market expansion.

Explore more data points, trends and opportunities Download Free Sample Report

Isoflavones Market Segmentations

By Source

- Soy Isoflavones

- Red Clover Isoflavones

- Kudzu Root Isoflavones

- Fermentation-Derived Isoflavones

- Other Botanical Sources

By Type

- Genistein

- Daidzein

- Glycitein

- Mixed Isoflavone Complexes

By Form

- Powder

- Capsules & Tablets

- Liquid Extracts

- Granules

By Application

- Dietary Supplements & Nutraceuticals

- Functional Food & Beverages

- Pharmaceutical Applications

- Cosmetics & Personal Care

- Animal Nutrition

By Distribution Channel

- Direct B2B Ingredient Supply

- Online Retail

- Pharmacies & Health Stores

- Supermarkets & Hypermarkets

- Specialty Nutrition Stores

Regional Insights

Asia-Pacific

Asia-Pacific holds the largest share of the global isoflavones market, representing approximately 41% of total revenue in 2025. Regional dominance is driven by extensive soybean cultivation, cost-efficient manufacturing ecosystems, and strong ingredient export capabilities led by China’s large-scale processing infrastructure. Japan and South Korea contribute significantly through high consumption of premium nutraceutical products and advanced functional food innovation. India is emerging as a high-growth market supported by expanding nutraceutical manufacturing capacity, favorable government initiatives promoting domestic production, and rising consumer awareness regarding preventive healthcare and plant-based supplementation. Long-standing dietary familiarity with soy-based foods across the region further accelerates acceptance, ensuring sustained long-term demand growth.

North America

North America accounts for nearly 27% of global demand, led primarily by the United States. Regional growth is supported by high dietary supplement penetration, strong consumer awareness regarding hormonal balance and women’s health, and increasing preference for clean-label and plant-derived ingredients. Expanding vegan and flexitarian populations are encouraging incorporation of isoflavones into functional foods and beverages. Continuous innovation in nutraceutical formulations, combined with strong clinical research infrastructure and advanced distribution networks, further drives market expansion. Canada contributes through growing demand for fortified plant-based products and increasing adoption of preventive nutrition strategies among aging populations.

Europe

Europe represents approximately 20% of global consumption, with Germany, France, Italy, and the United Kingdom serving as major markets. Regional growth is driven by rising demand for scientifically validated nutraceutical products and strong consumer preference for premium-quality formulations. Although regulatory frameworks remain stringent, they promote product standardization, safety assurance, and higher consumer trust, enabling premium pricing opportunities. Increasing adoption of plant-based diets, combined with expanding functional food innovation and wellness-focused lifestyles, continues to support steady market development across the region.

Latin America

Latin America is experiencing gradual but consistent growth, led by Brazil and Mexico. Rising middle-class income levels, improving healthcare awareness, and expanding retail distribution channels are encouraging adoption of dietary supplements and functional nutrition products. Increasing local manufacturing capabilities and growing interest in preventive healthcare solutions are supporting regional demand expansion. The popularity of plant-based nutrition trends and growing exposure to global wellness products are expected to further accelerate isoflavone consumption across the region over the forecast period.

Middle East & Africa

The Middle East and Africa market is developing steadily, with the United Arab Emirates and South Africa emerging as key growth hubs. Regional expansion is driven by increasing imports of nutraceutical ingredients, rapid growth of premium wellness retail channels, and rising consumer awareness regarding lifestyle-related health conditions. Urbanization, higher disposable incomes, and expanding access to international supplement brands are encouraging adoption of plant-based health products. Government initiatives promoting healthcare diversification and preventive wellness strategies are expected to further support long-term market growth across the region.

Key Players in the Isoflavones Market

- Archer Daniels Midland Company (ADM)

- Cargill Incorporated

- International Flavors & Fragrances Inc.

- DSM-Firmenich

- BASF SE

- Fuji Oil Holdings Inc.

- Aushadh Limited

- Nutra Green Biotechnology Co., Ltd.

- Shaanxi Pioneer Biotech Co., Ltd.

- Herbo Nutra Extract Pvt. Ltd.

- Xi’an Greena Biotech Co., Ltd.

- Bio-gen Extracts Pvt. Ltd.

- Frutarom Health

- SK Bioland Co., Ltd.

- SunOpta Inc.