IQF Freezing (Individual Quick Freezing) Market Size

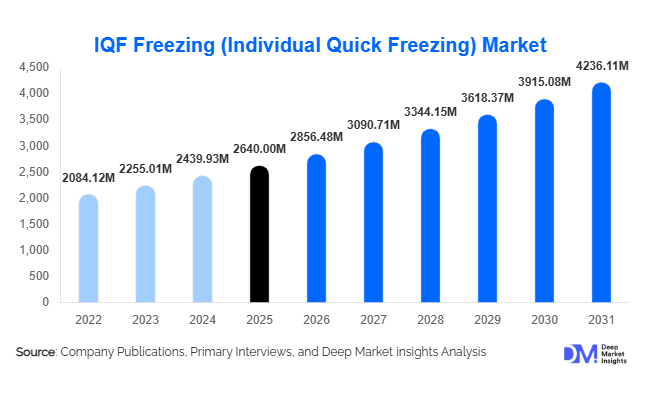

According to Deep Market Insights, the global IQF freezing (Individual Quick Freezing) market size was valued at USD 2,640 million in 2025 and is projected to grow from USD 2,856.48 million in 2026 to reach USD 4,236.11 million by 2031, expanding at a CAGR of 8.2% during the forecast period (2026–2031). The IQF freezing market growth is primarily driven by rising global demand for frozen fruits, vegetables, seafood, and ready-to-eat meals, along with rapid expansion of cold chain infrastructure and export-oriented food processing facilities. Increasing automation in food manufacturing plants and the need for improved product quality, extended shelf life, and reduced food waste are further strengthening adoption of IQF systems worldwide.

Key Market Insights

- Spiral freezers dominate the equipment segment, accounting for nearly 34% of the 2025 market share due to their space efficiency and high throughput capabilities.

- Mechanical refrigeration systems lead with over 70% share, supported by lower operating costs compared to cryogenic alternatives in large-scale processing plants.

- North America holds approximately 32% of the global market, driven by mature frozen food consumption and high automation levels.

- Asia-Pacific is the fastest-growing region, expanding at over 9% CAGR due to rising food exports and government-supported cold chain investments.

- Vegetables represent the largest application segment, contributing around 28% of the total market value in 2025.

- Top five companies collectively account for nearly 48% of global revenue, reflecting moderate market consolidation and strong technological competition.

What are the latest trends in the IQF freezing market?

Automation and Industry 4.0 Integration

Food processors are increasingly integrating smart automation into IQF systems, including IoT-enabled temperature monitoring, predictive maintenance software, and AI-driven production optimization. Fully automated IQF lines now account for nearly 58% of installations, particularly in North America and Europe where labor costs are high. Digital twins and real-time performance dashboards are being implemented to reduce downtime and energy consumption. These advancements are not only improving operational efficiency but also helping processors meet strict hygiene and food safety regulations such as HACCP and FDA compliance standards.

Shift Toward Energy-Efficient Refrigeration Systems

Energy efficiency has become a critical investment parameter in the IQF freezing industry. Manufacturers are adopting ammonia-CO₂ cascade refrigeration systems, variable frequency drives (VFDs), and heat recovery technologies to reduce operating costs. With energy representing up to 30% of total processing expenses, energy-efficient IQF solutions are gaining rapid traction. Cryogenic systems using liquid nitrogen and CO₂ are also expanding in niche high-value applications such as seafood and premium fruit freezing, where superior product quality justifies higher operational costs.

What are the key drivers in the IQF freezing market?

Rising Global Frozen Food Consumption

The expanding global frozen food industry, valued at over USD 300 billion, is a primary growth engine for IQF systems. Consumers increasingly prefer frozen fruits, vegetables, meat, and ready-to-cook meals due to convenience, longer shelf life, and reduced preparation time. Retail private labels are also expanding frozen product portfolios, further strengthening equipment demand across processing facilities.

Growth in Seafood and Meat Exports

Export-oriented economies such as India, Vietnam, Thailand, Norway, and Ecuador are significantly expanding seafood and poultry exports. IQF freezing ensures individual product integrity, rapid freezing, and compliance with international food safety standards, making it essential for export-grade production. Rising global shrimp and fish trade volumes are directly contributing to new IQF plant installations.

What are the restraints for the global market?

High Capital Investment Requirements

Large-scale IQF systems exceeding 10 tons per hour can require investments between USD 2–5 million, limiting adoption among small and mid-sized processors. Access to financing and ROI visibility remain critical decision factors, particularly in emerging economies.

Energy Consumption and Sustainability Pressures

IQF systems are energy-intensive, and rising electricity costs combined with carbon emission regulations pose operational challenges. Processors are under pressure to adopt environmentally friendly refrigerants and improve energy efficiency, increasing upfront costs.

What are the key opportunities in the IQF freezing industry?

Emerging Market Cold Chain Expansion

Rapid investments in cold chain infrastructure across India, Southeast Asia, Brazil, and Mexico are creating strong demand for medium-capacity IQF systems (2–10 tons/hour), which represent nearly 41% of current installations. Government-backed food parks and export processing zones are encouraging local processors to modernize freezing technology, creating sustained equipment demand.

Premium and Plant-Based Frozen Products

The rise of plant-based meat alternatives, organic frozen berries, avocado cubes, and ready-to-eat meal kits presents high-margin opportunities. IQF technology preserves texture and nutritional value, making it ideal for premium frozen SKUs. Retailers are expanding private-label frozen portfolios, creating recurring demand for technologically advanced freezing systems.

Equipment Type Insights

Spiral freezers dominate the global IQF freezing equipment market, accounting for approximately 34% of total revenue in 2025. Their leadership position is primarily driven by their space-efficient vertical design, high throughput capability, and suitability for continuous processing environments. These systems are particularly preferred in poultry and bakery operations where floor space optimization and production scalability are critical. The growing demand for processed chicken products, frozen baked goods, and ready-to-cook food items continues to reinforce spiral freezer adoption globally. Additionally, improvements in belt technology, airflow management, and energy efficiency are further strengthening their market position.

Tunnel freezers represent the second-largest segment, widely deployed in seafood and meat processing plants that require consistent airflow distribution and uniform freezing performance. Their ability to handle large batch volumes makes them ideal for export-oriented processors. Fluidized bed freezers remain highly popular for small particulate products such as peas, corn, diced vegetables, and shrimp, as they ensure individual separation and superior product integrity. Meanwhile, cryogenic IQF systems are gaining traction in niche and premium segments where ultra-fast freezing is essential to preserve texture, nutritional value, and appearance. Growth in high-value seafood, gourmet ready meals, and specialty fruit segments is supporting increased investment in cryogenic technology.

Application Insights

Vegetables constitute the leading application segment, accounting for nearly 28% of the global market in 2025. This leadership is driven by strong retail demand, expansion of private-label frozen vegetables, and increasing consumer preference for long-shelf-life plant-based foods. Rising urbanization and growing awareness of food waste reduction are also accelerating vegetable freezing capacity investments. The demand for pre-cut, pre-washed, and ready-to-cook vegetable products in both retail and foodservice channels continues to drive equipment installations.

Seafood and meat applications are witnessing accelerated growth, supported by expanding international trade and strict export quality standards. Countries with strong seafood processing industries are upgrading to advanced IQF systems to meet compliance requirements and maintain product quality during long-distance shipping. The dairy and ready-to-eat meal segments are also expanding steadily, particularly in developed economies where convenience foods dominate consumption patterns. Growth in frozen pizzas, snacks, and protein-rich meals is contributing to sustained equipment demand across multiple food categories.

Automation Level Insights

Fully automated IQF systems account for approximately 58% of global installations, making automation the leading segment in the market. This dominance is primarily driven by rising labor costs, stringent hygiene regulations, and the need for consistent production efficiency. Integration of robotics, automated conveyors, IoT-enabled monitoring systems, and predictive maintenance technologies is transforming freezing operations into highly controlled, data-driven environments. Large food processors are increasingly prioritizing automation to enhance traceability, minimize contamination risks, and optimize energy consumption.

Semi-automated systems continue to maintain relevance in cost-sensitive and emerging markets where capital investment constraints exist. However, their market share is gradually declining as processors transition toward higher levels of automation to meet international export standards and improve operational scalability.

End-Use Industry Insights

Food processing companies represent over 60% of total IQF equipment demand, positioning them as the dominant end-use segment. Export-oriented processors of seafood, poultry, fruits, and vegetables are the primary contributors, driven by the need to preserve product quality and extend shelf life for global distribution. Increasing consolidation within the food processing industry is also leading to large-scale facility upgrades and modernization initiatives.

Quick Service Restaurants (QSRs) and HoReCa chains are among the fastest-growing end-use segments, expanding at nearly 9–10% CAGR. The growth of standardized menus, centralized procurement systems, and global franchise expansion is increasing reliance on frozen ingredients processed through IQF technology. Retail private-label brands are further stimulating equipment demand as supermarkets expand frozen ready-meal offerings. Export-driven production, particularly in Asia-Pacific and Latin America, remains a critical demand catalyst across all end-use industries.

| By Equipment Type | By Refrigeration Technology | By Processing Capacity | By Application | By Automation Level | By End-Use Industry |

|---|---|---|---|---|---|

|

|

|

|

|

|

Regional Insights

North America

North America accounts for approximately 32% of the global IQF freezing market in 2025, making it the largest regional market. The United States leads demand due to its highly developed frozen food industry, strong retail distribution networks, and advanced automation adoption. Growth in plant-based frozen foods, premium seafood imports, and ready-to-eat meals continues to stimulate equipment upgrades. Labor shortages and high wage structures are accelerating automation investments across processing facilities. Canada contributes significantly through seafood processing and export-oriented plants, particularly in Atlantic provinces where frozen lobster, shrimp, and fish exports drive equipment installations.

Europe

Europe holds around 27% of the global market share, supported by established food processing hubs in Germany, France, Italy, and the Netherlands. Strict food safety regulations, energy efficiency mandates, and sustainability targets are key drivers influencing equipment modernization. Strong private-label penetration across European retail chains is boosting frozen vegetable and ready-meal production. Additionally, cross-border trade within the European Union supports consistent demand for standardized freezing technologies. Investments in environmentally sustainable refrigeration systems and carbon footprint reduction initiatives are further shaping regional market growth.

Asia-Pacific

Asia-Pacific represents nearly 29% of global revenue and is the fastest-growing region, expanding at over 9.5% CAGR. Rapid urbanization, rising disposable incomes, and growing demand for processed and convenience foods are driving significant expansion in freezing capacity. China and India are major contributors due to expanding agricultural output, rising food exports, and government-supported cold chain infrastructure development. Thailand and Vietnam dominate seafood IQF installations, supported by strong shrimp and fish exports. Japan and South Korea focus on premium ready-meal and high-quality frozen food applications, where advanced cryogenic systems are gaining traction. Increasing foreign direct investment in food processing facilities is further accelerating regional growth.

Latin America

Latin America accounts for approximately 7% of the global market, led by Brazil and Mexico. Poultry, beef, and tropical fruit exports are primary growth drivers across the region. Expanding agro-processing infrastructure and government incentives for export competitiveness are encouraging modernization of freezing facilities. Rising domestic consumption of frozen foods in urban areas is also contributing to steady equipment demand.

Middle East & Africa

The Middle East & Africa region contributes roughly 5% of global revenue, with growth supported by increasing investments in food security and import substitution strategies. The UAE and Saudi Arabia are expanding cold storage and food processing infrastructure to reduce reliance on imports and strengthen local production capacity. South Africa leads regional frozen food processing operations, driven by meat exports and retail expansion. Infrastructure development and diversification of food supply chains are expected to gradually enhance regional adoption of IQF technologies.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the IQF Freezing Market

- JBT Corporation

- GEA Group AG

- Marel hf.

- Tetra Pak International S.A.

- Buhler Group

- Air Products and Chemicals, Inc.

- Linde plc

- OctoFrost Group

- Starfrost Ltd

- FPS Food Process Solutions

- The Middleby Corporation

- Scanico A/S

- Advanced Equipment Inc.

- Optimar AS

- RMF Freezers