Ipriflavone Market Size

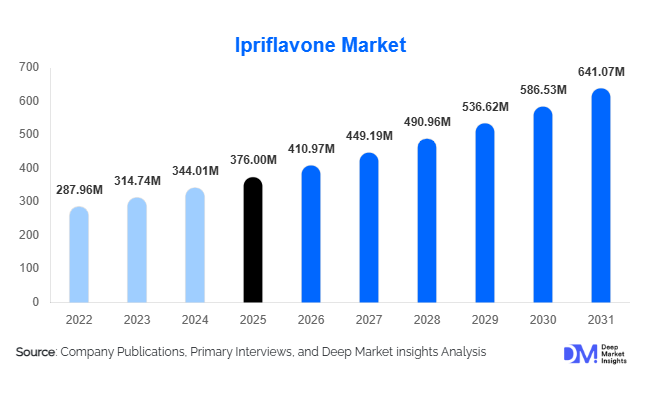

According to Deep Market Insights,the global ipriflavone market size was valued at USD 376 million in 2025 and is projected to grow from USD 410.97 million in 2026 to reach USD 641.07 million by 2031, expanding at a CAGR of 9.3% during the forecast period (2026–2031). The ipriflavone market growth is primarily driven by rising global awareness of bone health management, increasing prevalence of osteoporosis among aging populations, and growing adoption of non-hormonal nutraceutical ingredients for preventive healthcare. Expanding demand for dietary supplements, combined with innovation in high-purity formulations and combination bone-health products, continues to strengthen market expansion across developed and emerging economies.

Key Market Insights

- Ipriflavone demand is shifting toward preventive healthcare applications, particularly in bone density maintenance and menopause-related supplementation.

- The nutraceutical industry dominates consumption, accounting for more than half of global ingredient demand due to lower regulatory barriers and rising supplement adoption.

- North America leads global consumption, supported by mature dietary supplement markets and strong consumer awareness.

- Asia-Pacific is the fastest-growing region, driven by aging populations, expanding e-commerce supplement sales, and increasing healthcare spending.

- High-purity (98–99%) formulations are becoming industry standards, balancing efficacy with manufacturing affordability.

- Technological improvements in micronization and bioavailability enhancement are improving product performance and differentiation.

What are the latest trends in the ipriflavone market?

Rise of Combination Bone-Health Formulations

Manufacturers are increasingly incorporating ipriflavone into multi-ingredient supplements combining calcium, vitamin D3, magnesium, and vitamin K2. Consumers prefer comprehensive bone-health solutions rather than single-ingredient supplements, encouraging brands to develop synergistic formulations supported by clinical positioning. This trend allows companies to command premium pricing while improving therapeutic perception. Personalized nutrition platforms are also accelerating the adoption of customized formulations targeting menopausal women and elderly consumers, strengthening long-term demand stability.

Expansion of Digital Nutraceutical Distribution

E-commerce platforms are transforming ingredient commercialization by enabling global supplement brands to reach consumers directly. Online health marketplaces and subscription-based supplement models are accelerating adoption of specialized ingredients such as ipriflavone. Digital education campaigns, influencer-led health awareness, and telehealth consultations are further improving consumer understanding of bone-health supplementation. Cross-border online trade has allowed Asian manufacturers to supply North American and European brands efficiently, reshaping global distribution dynamics.

What are the key drivers in the ipriflavone market?

Growing Aging Population and Osteoporosis Prevalence

The increasing global elderly population is significantly driving demand for bone-health ingredients. Aging-related bone density loss has become a major healthcare concern, encouraging preventive supplementation. Healthcare systems are promoting early intervention strategies to reduce fracture-related costs, positioning ipriflavone as a supportive ingredient for long-term skeletal health management. Countries with rapidly aging demographics, including Japan, Germany, and the United States, represent strong demand centers.

Shift Toward Non-Hormonal Menopause Solutions

Concerns associated with hormone replacement therapy have encouraged consumers to adopt safer alternatives. Ipriflavone provides a non-estrogenic mechanism supporting calcium metabolism without hormonal side effects, increasing adoption among women aged above 45 years. Growing awareness of natural and plant-associated compounds further supports consumer preference for nutraceutical-based solutions.

What are the restraints for the global market?

Limited Consumer Awareness Compared to Mainstream Supplements

Despite strong clinical backing, ipriflavone remains less recognized than calcium or collagen supplements. Limited marketing visibility and lower consumer education slow adoption rates, particularly in developing markets where purchasing decisions are driven by familiar ingredients.

Regulatory Classification Differences Across Regions

Varying regulatory frameworks classify ipriflavone differently as either a pharmaceutical compound or dietary supplement. These inconsistencies increase compliance costs and prolong approval timelines, creating barriers for new entrants and delaying product commercialization in certain regions.

What are the key opportunities in the ipriflavone industry?

Preventive Healthcare Policy Integration

Governments worldwide are emphasizing preventive healthcare to reduce long-term medical expenditures. Bone-health screening programs and aging-care initiatives present opportunities for supplement manufacturers to integrate ipriflavone into standardized wellness protocols. Partnerships with pharmacies and healthcare providers are expected to strengthen recurring demand patterns.

Expansion in Asia-Pacific Nutraceutical Markets

Rapid growth in supplement consumption across China, India, South Korea, and Southeast Asia offers substantial expansion opportunities. Rising disposable incomes, digital retail penetration, and growing wellness awareness are enabling both established and emerging brands to introduce specialized bone-health formulations incorporating ipriflavone.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 376.00 Million |

| Market Size in 2026 | USD 410.97 Million |

| Market Size in 2031 | USD 641.07 Million |

| CAGR | 9.3% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Powder-form ipriflavone dominates the global market, accounting for nearly 42% of total demand, primarily driven by its superior formulation flexibility, cost efficiency, and scalability across multiple delivery formats. The powdered format enables manufacturers to seamlessly integrate ipriflavone into tablets, capsules, sachets, and functional beverage premixes, making it the preferred choice for nutraceutical and pharmaceutical producers seeking standardized dosing and production efficiency. Its longer shelf stability and compatibility with large-scale contract manufacturing processes further enhance its commercial attractiveness, particularly for bulk ingredient procurement. Capsule- and tablet-grade variants remain widely utilized due to increasing consumer preference for convenient supplementation formats and accurate dosage control. Meanwhile, liquid and suspension formats are gradually emerging within functional beverage innovation, particularly in fortified nutrition drinks and ready-to-consume wellness products, reflecting broader industry movement toward alternative delivery systems. However, the continued dominance of powdered ipriflavone is supported by manufacturing versatility, reduced transportation costs, and expanding global private-label supplement production.

Application Insights

Bone health supplements represent the largest application segment, contributing approximately 46% of global market demand in 2025, driven primarily by rising osteoporosis prevalence, aging populations, and growing consumer focus on preventive skeletal health. Increasing awareness regarding bone density maintenance, particularly among postmenopausal women and elderly populations, continues to accelerate adoption of ipriflavone-based formulations. Menopause-health and osteoporosis management applications closely follow, supported by clinical interest in non-hormonal nutritional interventions that support calcium metabolism and bone regeneration. Functional foods and beverages are emerging as a significant growth avenue as manufacturers incorporate bone-support ingredients into fortified dairy alternatives, nutritional beverages, and health-focused snack formulations to appeal to wellness-oriented consumers. Additionally, sports nutrition and recovery products are increasingly adopting ipriflavone to support skeletal resilience and injury prevention among active individuals, reflecting expanding use cases beyond traditional therapeutic supplementation.

Distribution Channel Insights

Direct B2B ingredient supply dominates the distribution landscape, accounting for roughly 55% of global sales, largely driven by long-term procurement agreements between ingredient manufacturers and nutraceutical companies seeking consistent quality assurance and supply chain stability. Large supplement brands increasingly rely on direct sourcing models to maintain formulation control, regulatory compliance, and cost optimization. Contract manufacturing organizations are gaining strategic importance by enabling emerging and private-label brands to accelerate product launches without significant capital investment in manufacturing infrastructure. The growing globalization of supplement production has further strengthened this channel, particularly as brands diversify sourcing partners to enhance resilience against supply disruptions. Online ingredient marketplaces and digital procurement platforms are also gaining traction, improving pricing transparency, expanding supplier accessibility, and streamlining international trade processes, thereby modernizing traditional ingredient distribution ecosystems.

End-Use Industry Insights

The nutraceutical industry leads global ipriflavone consumption with nearly 58% market share, supported by expanding consumer adoption of dietary supplements and increasing awareness surrounding preventive healthcare and healthy aging. Rising demand for science-backed wellness solutions has encouraged supplement manufacturers to integrate bone-support compounds into daily health regimens, reinforcing the sector’s leadership. Pharmaceutical applications maintain stable demand, particularly in therapeutic formulations targeting bone-density maintenance and osteoporosis support, where standardized ingredient quality and clinical validation remain essential. Functional food and beverage manufacturers are gradually incorporating ipriflavone into fortified nutrition products as consumers increasingly seek health benefits through everyday dietary intake rather than standalone supplementation. Additionally, animal health applications are emerging as a niche but promising segment, driven by growing expenditure on pet wellness and the rising popularity of bone and joint support supplements for aging companion animals.

Explore more data points, trends and opportunities Download Free Sample Report

Ipriflavone Market Segmentations

By Product Type

- Powder Ipriflavone

- Capsule/Tablet Grade Ipriflavone

- Granulated Ipriflavone

- Liquid & Suspension Forms

By Application

- Bone Health Supplements

- Osteoporosis Management

- Menopause Health Products

- Functional Foods & Beverages

- Sports Nutrition & Recovery Products

By Distribution Channel

- Direct B2B Ingredient Supply

- Contract Manufacturers (CMOs/CDMOs)

- Online Ingredient Platforms

- Specialty Nutraceutical Distributors

By End-Use Industry

- Nutraceutical Industry

- Pharmaceutical Industry

- Functional Food & Beverage Industry

- Animal Health & Veterinary Supplements

Regional Insights

North America

North America accounted for approximately 32% of the global ipriflavone market in 2025, led by the United States, where strong dietary supplement penetration and advanced healthcare awareness continue to drive adoption. Regional growth is supported by an aging demographic profile, increasing incidence of osteoporosis, and widespread acceptance of preventive health strategies. Physician-recommended supplementation programs, strong retail and e-commerce supplement distribution networks, and high consumer spending on wellness products further reinforce market expansion. Additionally, innovation in nutraceutical formulations and growing investment in clinical research surrounding bone-health ingredients continue to strengthen long-term regional demand.

Europe

Europe held nearly 27% market share, driven by sustained demand across Germany, Italy, France, and the United Kingdom. Regional growth is supported by structured healthcare systems emphasizing preventive care and early intervention for age-related health conditions. Rising osteoporosis prevalence, particularly among aging populations, has increased adoption of both pharmaceutical-grade and nutraceutical bone-health formulations. Strong regulatory frameworks promoting product quality and safety enhance consumer confidence, while expanding plant-based and natural supplement trends further encourage ipriflavone integration into wellness products. Increasing collaboration between pharmaceutical and nutraceutical sectors also contributes to steady market development across the region.

Asia-Pacific

Asia-Pacific represents the fastest-growing regional market, expanding at over 11% CAGR, driven by demographic shifts, rising healthcare awareness, and rapid expansion of supplement manufacturing capabilities. China and Japan collectively account for more than 60% of regional demand due to large aging populations, high supplement consumption rates, and established functional food cultures. Japan’s long-standing focus on functional nutrition and bone-health maintenance supports mature adoption, while China benefits from expanding domestic nutraceutical production and growing middle-class health expenditure. India is emerging rapidly as a growth hub supported by increasing urban health awareness, expanding e-commerce supplement distribution, and government-backed pharmaceutical and nutraceutical manufacturing initiatives that strengthen regional supply chains.

Latin America

Latin America represents around 7% of global demand, with Brazil and Mexico leading regional consumption. Market growth is driven by expanding urban wellness trends, improving access to dietary supplements through organized retail channels, and rising consumer awareness regarding preventive healthcare. Increasing middle-class purchasing power and growing investment by international supplement brands are improving product availability, while regional manufacturers are introducing affordable formulations tailored to local consumer preferences, supporting steady long-term expansion.

Middle East & Africa

The Middle East & Africa region accounts for roughly 5% market share, led by the UAE and South Africa. Growth in this region is supported by rising disposable incomes, increasing health consciousness, and expanding premium wellness product adoption among urban populations. Government initiatives promoting healthcare diversification and preventive wellness programs are gradually improving supplement penetration. Additionally, the expansion of modern retail infrastructure, cross-border e-commerce platforms, and growing awareness of bone and joint health are contributing to gradual but consistent market development across the region.

Key Players in the Ipriflavone Market

- DSM Nutritional Products

- BASF SE

- Zhejiang Medicine Co., Ltd.

- CSPC Pharmaceutical Group

- Shanghai Freemen LLC

- Xi’an Natural Field Bio-Technique

- Hangzhou Think Chemical

- Hubei Yuancheng Pharmaceutical

- Shaanxi Pioneer Biotech

- Chengdu Okay Pharmaceutical

- Wuhan Yuancheng Gongchuang Technology

- Jinan Jinda Pharmaceutical Chemistry

- Bio-gen Extracts Pvt. Ltd.

- NutraScience Labs

- Sabinsa Corporation