Infant Formula Market Size

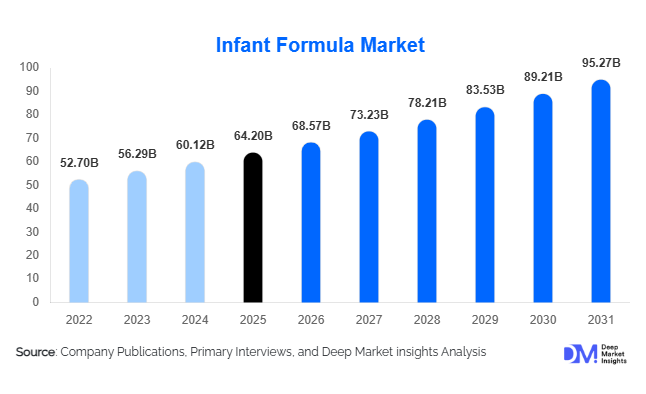

According to Deep Market Insights,the global infant formula market size was valued at USD 64.20 billion in 2025 and is projected to grow from USD 68.57 billion in 2026 to reach USD 95.27 billion by 2031, expanding at a CAGR of 6.8% during the forecast period (2026–2031). Market growth is primarily driven by rising female workforce participation, increasing awareness regarding early-life nutrition, growing demand for specialty and organic infant formulas, and expanding middle-class populations in emerging economies. Premiumization trends, particularly in Asia-Pacific and North America, are further supporting revenue expansion, while product innovation in hypoallergenic and A2-based formulations continues to reshape competitive dynamics.

Key Market Insights

- Asia-Pacific dominates the global infant formula market, accounting for nearly 44% of global revenue in 2025, led by strong demand from China and India.

- Cow milk-based formula remains the leading ingredient segment, contributing approximately 62% of total market share due to cost efficiency and established supply chains.

- Powdered infant formula leads by form, holding nearly 72% of total global sales owing to longer shelf life and affordability.

- Specialty and hypoallergenic formulas are the fastest-growing category, driven by rising cases of infant allergies and digestive sensitivities.

- Online retail channels are expanding rapidly, supported by subscription-based purchasing and cross-border e-commerce demand.

- Top five companies control nearly 58% of global market revenue, reflecting moderate-to-high industry concentration.

What are the latest trends in the infant formula market?

Premiumization and Organic Formula Expansion

Consumers are increasingly shifting toward premium, organic, and A2 protein-based infant formulas, particularly in developed markets such as the United States, Germany, and Australia. Parents are prioritizing clean-label formulations free from artificial additives, palm oil, and genetically modified ingredients. Organic certification and traceable dairy sourcing are becoming competitive differentiators. Premium products typically command 30–40% higher pricing than conventional formulas, contributing significantly to revenue growth despite stable birth rates in developed economies.

Digitalization and Subscription-Based Sales Models

The rapid expansion of e-commerce platforms has transformed purchasing behavior in the infant formula industry. Subscription-based models allow recurring monthly deliveries, improving customer retention and lifetime value. Cross-border e-commerce, particularly into China and Southeast Asia, has strengthened global brand reach. Digital platforms also integrate pediatric guidance, product comparisons, and consumer education, increasing transparency and brand loyalty. Online retail now accounts for over 15% of global sales and continues to grow steadily.

What are the key drivers in the infant formula market?

Rising Female Workforce Participation

Growing employment among women globally is a primary driver of infant formula demand. Dual-income households increasingly rely on formula feeding for convenience and nutritional reliability. Urbanization and evolving family structures further reinforce this shift, particularly in North America, Europe, and parts of Asia-Pacific. Ready-to-feed and easy-mix powder formats are gaining traction among working parents.

Advancements in Pediatric Nutrition Science

Continuous research in infant gut health, immunity, and brain development has led to product innovation in probiotics, DHA/ARA fortification, and hydrolyzed protein formulas. Specialty products addressing lactose intolerance and cow milk protein allergy are expanding rapidly. Clinically validated formulations are strengthening brand trust and enabling companies to command premium margins.

What are the restraints for the global market?

Declining Birth Rates in Developed Economies

Countries such as Japan, Germany, and Italy are experiencing sustained declines in birth rates, limiting long-term volume growth. Companies operating in mature markets are increasingly dependent on premiumization strategies rather than unit expansion to sustain revenue growth.

Stringent Regulatory Frameworks

Infant nutrition products are highly regulated under global standards, including Codex Alimentarius guidelines and region-specific safety norms. Compliance costs, labeling requirements, and product registration procedures increase time-to-market and operational expenses. Any quality lapse can severely impact brand reputation and sales.

What are the key opportunities in the infant formula industry?

Emerging Market Expansion

Countries such as India, Indonesia, Vietnam, Nigeria, and Brazil present strong untapped potential. Rising disposable income, improving healthcare awareness, and expanding modern retail infrastructure are driving formula adoption. Local manufacturing investments can reduce import dependency and enhance price competitiveness in these regions.

Specialty and Medical Nutrition Integration

Integration with hospital neonatal care units and pediatric clinics represents a significant opportunity. Preterm infant formulas and low-birth-weight nutritional solutions are witnessing increased institutional demand. Partnerships with hospitals and healthcare professionals enhance brand credibility and secure recurring institutional contracts.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 64.20 Billion |

| Market Size in 2026 | USD 68.57 Billion |

| Market Size in 2031 | USD 95.27 Billion |

| CAGR | 6.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Standard infant formula (0–6 months) continues to dominate the global infant formula market, accounting for approximately 38% of total revenue in 2025. The leadership of this segment is primarily driven by universal nutritional requirements during the first six months of life, particularly in cases where breastfeeding is partially supplemented or not feasible due to medical, professional, or lifestyle factors. Rising maternal employment rates, increasing urbanization, and growing awareness of scientifically formulated early-life nutrition further strengthen demand for standard formula products. Additionally, hospital recommendations and pediatric endorsements contribute significantly to consistent global uptake. Follow-on formula (6–12 months) and growing-up milk (12 months and above) segments are expanding steadily, particularly across emerging economies in Asia-Pacific where parents increasingly prioritize extended nutritional supplementation during toddlerhood. Specialty formulas, including hypoallergenic, lactose-free, soy-based, and extensively hydrolyzed variants, represent the fastest-growing sub-segment, supported by increasing diagnosis of infant allergies, lactose intolerance, and digestive sensitivities. Growing parental awareness, improved pediatric screening, and rising demand for premium therapeutic nutrition products are accelerating growth within this category.

Ingredient Insights

Cow milk-based formula remains the leading ingredient segment, capturing nearly 62% of global market share in 2025. Its dominance is supported by well-established global dairy supply chains, cost efficiency, regulatory familiarity, and long-standing clinical validation of safety and nutritional adequacy. Economies of scale in dairy production and stable raw material sourcing further reinforce its widespread adoption across both developed and developing markets. Meanwhile, goat milk-based and A2 protein-based formulas are experiencing rapid growth, particularly in premium markets across Asia-Pacific and Europe, driven by perceptions of improved digestibility and reduced allergenic potential. These products are increasingly positioned as premium alternatives targeting health-conscious and affluent consumers. Hydrolyzed protein formulas are gaining strong traction in North America and Europe, where higher allergy diagnosis rates and pediatric recommendations encourage their adoption. Continuous product innovation, including the addition of human milk oligosaccharides (HMOs), probiotics, and DHA/ARA fortification, is further enhancing ingredient differentiation and value positioning across the market.

Form Insights

Powder infant formula dominates the global market, accounting for approximately 72% of total sales in 2025. The segment’s leadership is primarily driven by its extended shelf life, lower transportation and storage costs, and affordability compared to liquid alternatives. Powdered formula also offers logistical advantages in large-scale distribution and cross-border trade, making it particularly suitable for emerging markets with price-sensitive consumers. In contrast, ready-to-feed liquid formulas are expanding steadily in developed regions such as North America and Europe, supported by convenience benefits, precise portion control, and time-saving preparation. Increasing participation of women in the workforce and rising demand for on-the-go feeding solutions are key drivers of growth for ready-to-feed formats. Concentrated liquid formulas maintain a niche presence, primarily serving institutional and hospital settings where controlled preparation is required.

Distribution Channel Insights

Supermarkets and hypermarkets account for nearly 34% of global sales in 2025, maintaining leadership due to strong product visibility, promotional pricing strategies, established supply chains, and consumer preference for bulk purchasing. Large retail chains also provide trust and authenticity assurance, which is particularly important in categories such as infant nutrition. However, online retail is emerging as the fastest-growing distribution channel globally. Growth is fueled by subscription-based purchasing models, competitive pricing, convenience, access to international brands, and detailed product comparisons. Cross-border e-commerce is especially influential in China and Southeast Asia, where demand for imported premium formula brands remains strong. Pharmacies and specialty baby stores continue to play a critical role in premium and therapeutic formula sales, supported by professional recommendations and consumer trust.

Explore more data points, trends and opportunities Download Free Sample Report

Infant Formula Market Segmentations

By Product Type

- Standard Infant Formula

- Follow-on Formula

- Growing-Up Milk

- Specialty Infant Formula

By Ingredient Type

- Cow Milk-Based Formula

- Soy Protein-Based Formula

- Hydrolyzed Protein Formula

- Goat Milk-Based Formula

- Organic & A2 Protein-Based Formula

By Form

- Powder Formula

- Liquid Concentrate Formula

- Ready-to-Feed (RTF) Formula

By Distribution Channel

- Supermarkets & Hypermarkets

- Pharmacies & Drug Stores

- Specialty Baby Stores

- Online Retail / E-commerce

- Hospital & Institutional Sales

By Age Group

- 0–6 Months

- 6–12 Months

- 12–24 Months

- 24–36 Months

Regional Insights

Asia-Pacific

Asia-Pacific holds approximately 44% of the global infant formula market share in 2025, making it the largest regional market. China contributes nearly 24% of global demand, driven by strong consumer preference for premium imported brands, rising disposable incomes, evolving dietary patterns, and heightened awareness of product quality and safety standards. Urbanization and expansion of modern retail infrastructure further support growth. India is the fastest-growing country in the region, with an expected CAGR above 8%, fueled by rising birth rates in certain states, increasing urban middle-class households, growing female workforce participation, and improving pediatric healthcare awareness. Southeast Asian countries such as Indonesia and Vietnam are witnessing steady expansion due to expanding healthcare access, increasing penetration of modern retail channels, and rising parental awareness regarding early-life nutrition. Government nutrition programs and expanding e-commerce ecosystems across the region also contribute significantly to sustained demand growth.

North America

North America accounts for around 20% of global market share in 2025, led by the United States. The U.S. market benefits from strong institutional demand through programs such as WIC, high product awareness, advanced healthcare infrastructure, and strong pediatric recommendations. Growth is further driven by rising demand for organic, non-GMO, and specialty formulas, reflecting premiumization and clean-label trends among consumers. Innovation in ingredient fortification, including HMOs and plant-based alternatives, also supports market expansion. Canada contributes stable and moderate growth, supported by premium product adoption, high per capita income, and stringent regulatory standards that reinforce consumer trust in locally manufactured and imported products.

Europe

Europe represents approximately 23% of global demand in 2025, with Germany, France, and the United Kingdom leading regional sales. The region’s growth is supported by stringent quality and safety regulations, strong consumer confidence in domestic dairy production, and high penetration of premium and organic infant formula products. Western Europe demonstrates particularly strong demand for organic and clean-label formulations, reflecting environmentally conscious consumer behavior and established organic food markets. In Eastern Europe, rising disposable incomes, improving retail infrastructure, and increasing urbanization are contributing to steady market expansion. Continuous innovation in specialty and allergy-focused formulas also supports regional growth.

Latin America

Latin America accounts for nearly 7% of global revenue in 2025, with Brazil and Mexico serving as the primary contributors. Regional growth is driven by increasing urbanization, rising female workforce participation, expanding middle-class populations, and the rapid development of modern retail channels. Improvements in healthcare awareness and pediatric nutrition education are further supporting formula adoption. Economic stabilization in key markets and expanding access to international brands through both retail and e-commerce platforms are expected to sustain long-term growth across the region.

Middle East & Africa

The Middle East & Africa region contributes around 6% of global market share in 2025. Key markets such as Saudi Arabia, the UAE, and South Africa are driven by high import dependence, strong preference for premium international brands, rising expatriate populations, and increasing disposable incomes. In Gulf Cooperation Council (GCC) countries, high birth rates and government healthcare investments further stimulate demand. Nigeria is emerging as a high-growth market due to rapid population expansion, rising urbanization, and improving maternal and child healthcare awareness. Expansion of organized retail and growing digital commerce penetration are expected to enhance product accessibility across the region.

Key Players in the Infant Formula Market

- Nestlé S.A.

- Danone S.A.

- Abbott Laboratories

- Reckitt Benckiser Group plc

- Meiji Holdings Co., Ltd.

- FrieslandCampina

- Yili Group

- China Mengniu Dairy Company Limited

- Fonterra Co-operative Group

- Arla Foods