Industrial Sugar Market Size

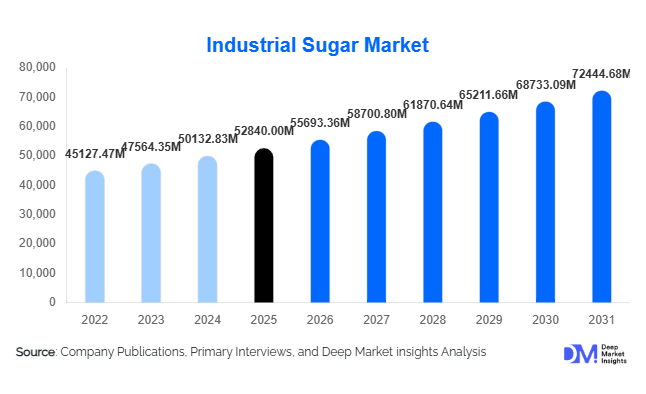

According to Deep Market Insights, the global industrial sugar market size was valued at USD 52,840 million in 2025 and is projected to grow from USD 55,693.36 million in 2026 to reach USD 72,444.68 million by 2031, expanding at a CAGR of 5.4% during the forecast period (2026–2031). Growth in the industrial sugar market is primarily driven by expanding processed food consumption, increasing beverage manufacturing volumes, and rising demand from pharmaceutical and fermentation-based industries worldwide. Industrial sugar remains a critical raw material across multiple value chains due to its functional properties including preservation, fermentation support, texture enhancement, and sweetness optimization.

Key Market Insights

- Processed food and beverage manufacturing accounts for the largest share of industrial sugar consumption, supported by urbanization and convenience food demand.

- Asia-Pacific dominates global consumption, driven by large-scale food processing expansion in China and India.

- Liquid sugar and customized sugar solutions are gaining traction among beverage and bakery manufacturers seeking operational efficiency.

- Bio-based industrial applications, including ethanol and fermentation products, are emerging as important growth drivers.

- Price volatility linked to raw sugarcane and beet production continues to influence procurement strategies globally.

- Automation and supply-chain digitization are improving efficiency in large-scale sugar refining and distribution networks.

What are the latest trends in the industrial sugar market?

Shift Toward Functional and Customized Sugar Formats

Industrial buyers increasingly demand application-specific sugar formats such as liquid sugar, invert sugar, and specialty blends tailored for bakery, dairy, and beverage processing. Manufacturers are investing in refining technologies that deliver consistent particle size, solubility, and purity levels to enhance production efficiency. Liquid sugar adoption is particularly rising among beverage bottlers due to reduced handling costs, faster dissolution, and improved quality control. Customized sugar blends are also enabling reduced formulation complexity while maintaining taste consistency, supporting large-scale industrial standardization.

Integration of Sugar into Bio-Industrial Value Chains

Industrial sugar is increasingly used beyond traditional food applications, particularly in fermentation industries producing bioethanol, organic acids, enzymes, and bioplastics. Growing investment in bio-based manufacturing is positioning sugar as a renewable feedstock supporting sustainable industrial chemistry. Governments promoting biofuel blending and green chemical production are indirectly increasing industrial sugar demand. This diversification reduces dependence on food-sector consumption alone and stabilizes long-term demand patterns for sugar processors.

What are the key drivers in the industrial sugar market?

Expansion of Global Processed Food Production

Rapid urbanization and changing dietary habits are accelerating demand for packaged foods, confectionery, bakery products, and ready-to-drink beverages. Industrial sugar acts as both a sweetener and functional ingredient, supporting preservation, texture formation, and browning reactions. Emerging economies are witnessing rapid expansion of food processing capacity, which directly increases bulk sugar procurement contracts. Large multinational food manufacturers continue expanding production facilities in Asia and Latin America, reinforcing sustained consumption growth.

Growth of Beverage Manufacturing Industry

Carbonated drinks, flavored beverages, juices, and energy drinks remain major consumers of industrial sugar. Rising consumption among younger populations and expanding retail distribution networks are boosting production volumes globally. Beverage companies increasingly rely on liquid sugar supply agreements to streamline operations and reduce logistical inefficiencies. Emerging markets show strong per capita beverage consumption growth, sustaining long-term industrial sugar demand.

Pharmaceutical and Fermentation Industry Demand

Sugar is widely used in pharmaceutical syrups, suspension formulations, and fermentation-based drug production. Expansion of global pharmaceutical manufacturing, particularly generic medicines, has increased demand for pharmaceutical-grade sugar. Additionally, fermentation-based biotechnology industries use sugar substrates for producing antibiotics, enzymes, and vitamins, creating stable industrial demand independent of food consumption cycles.

What are the restraints for the global market?

Health Regulations and Sugar Reduction Policies

Government initiatives aimed at reducing sugar consumption, including sugar taxes and labeling regulations, indirectly affect industrial demand. Reformulation efforts by food companies toward reduced-sugar alternatives and artificial sweeteners may slow volume growth in some developed markets. Regulatory pressures require manufacturers to innovate while maintaining taste and cost competitiveness.

Raw Material Price Volatility

Industrial sugar pricing remains highly dependent on agricultural output of sugarcane and sugar beet. Weather variability, water scarcity, and fluctuating global commodity prices create procurement uncertainty for industrial buyers. Volatility impacts long-term contracts and margins for refiners and downstream manufacturers, necessitating hedging and diversified sourcing strategies.

What are the key opportunities in the industrial sugar industry?

Biofuel and Green Chemical Expansion

Global decarbonization strategies are accelerating investment in bioethanol and bio-based chemicals. Sugar-derived fermentation feedstocks offer renewable alternatives to fossil-based inputs, creating large-scale industrial demand opportunities. Countries implementing ethanol blending mandates are encouraging sugar processors to diversify output streams, opening new revenue channels beyond food markets.

Emerging Market Food Processing Infrastructure

Rapid industrialization in Southeast Asia, Africa, and Latin America is driving investment in food manufacturing facilities. Governments are supporting domestic processing industries to reduce imports of finished foods, thereby increasing demand for locally supplied industrial sugar. Expansion of cold chains, retail networks, and quick-service restaurants further strengthens consumption growth.

Technological Optimization in Sugar Refining

Automation, energy-efficient refining systems, and digital supply-chain management are improving productivity and reducing production costs. Companies adopting advanced crystallization and purification technologies can offer higher-quality industrial sugar grades tailored to pharmaceutical and beverage sectors. These innovations create competitive advantages and support premium pricing segments.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 52840 Million |

| Market Size in 2026 | USD 55693.36 Million |

| Market Size in 2031 | USD 72444.68 Million |

| CAGR | 5.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

White refined sugar dominates the industrial sugar market, accounting for nearly 48% of global market share in 2025, primarily driven by its standardized quality, high purity levels, and neutral sensory profile that allow seamless integration across large-scale food and beverage manufacturing processes. The leading segment growth driver is the increasing demand for consistent ingredient functionality in automated industrial production lines, where uniform crystallization and predictable sweetness levels are essential for product stability and brand consistency. Beverage producers, bakery manufacturers, and confectionery companies continue to rely heavily on refined sugar due to its cost efficiency and formulation reliability.Liquid sugar represents the fastest-growing product category, supported by rising automation within beverage and processed food facilities where reduced dissolution time improves operational efficiency and lowers energy consumption. Large beverage bottlers increasingly prefer liquid sugar systems as they enable continuous processing and minimize handling losses. Brown sugar maintains steady demand, particularly in bakery and specialty food applications where flavor enhancement and texture differentiation are required. Meanwhile, invert sugar is gaining traction in confectionery and processed desserts owing to its moisture-retention capability, crystallization control, and shelf-life extension properties, making it particularly valuable for premium and export-oriented food production.

Application Insights

Food and beverage processing remains the leading application segment, contributing approximately 64% of total industrial sugar consumption in 2025. The primary growth driver for this segment is the sustained global expansion of packaged food consumption supported by urbanization, rising disposable income, and changing dietary patterns favoring convenience foods. Within this category, beverage manufacturing leads demand due to continuous production cycles, high-volume output requirements, and the growing popularity of carbonated drinks, flavored beverages, energy drinks, and ready-to-drink formulations.Pharmaceutical applications are expanding steadily as sugar continues to function as a stabilizing, flavor-masking, and viscosity-enhancing agent in syrups, suspensions, and pediatric formulations. Increasing healthcare accessibility in emerging markets is reinforcing this demand. Fermentation and bio-industrial applications are emerging as high-growth areas, supported by rising ethanol production, biotechnology innovation, and microbial fermentation processes used in enzymes, organic acids, and bio-based chemicals. These applications are expanding the role of industrial sugar beyond traditional food uses into broader industrial biotechnology ecosystems.

Form Insights

Granulated sugar holds the largest share at around 57% of the global market, driven primarily by its versatility across multiple industrial applications and its logistical advantages in storage, handling, and transportation. The leading segment driver is the compatibility of granulated sugar with diverse manufacturing equipment, allowing processors to maintain standardized dosing and blending across production batches. Its long shelf life and reduced risk of microbial contamination further strengthen its preference among large-scale manufacturers.Liquid sugar adoption is increasing among large industrial processors seeking improved process automation, faster mixing times, and reduced labor requirements. The shift toward integrated processing systems in beverage and dairy manufacturing is accelerating this transition. Powdered sugar remains essential in bakery and confectionery applications where fine particle size ensures smooth texture, uniform icing performance, and precise product finishing, particularly in premium baked goods and dessert manufacturing.

Distribution Channel Insights

Direct B2B supply contracts dominate industrial sugar distribution, accounting for nearly 72% of global sales, as large manufacturers prioritize long-term procurement agreements to ensure supply stability and price predictability in a commodity-sensitive market. The leading driver for this segment is the growing need for supply chain security amid fluctuating raw material prices and global trade uncertainties. Long-term contracts also enable processors to optimize production planning and maintain consistent input costs.Industrial wholesalers play a critical role in serving mid-sized and regional processors that require flexible purchasing volumes without direct refinery agreements. Ingredient solution providers are increasingly gaining traction by offering customized sugar blends, liquid formulations, and integrated ingredient systems tailored to specific manufacturing requirements. This value-added distribution approach is becoming increasingly important as food manufacturers seek formulation efficiency and supplier consolidation.

End-Use Industry Insights

Food processing industries represent the largest end-use segment, supported by expanding global consumption of packaged snacks, baked goods, dairy products, and confectionery items. The leading growth driver is the rapid expansion of convenience food categories aligned with urban lifestyles and modern retail distribution networks. Beverage manufacturers follow as a major consumer group and represent one of the fastest-growing segments due to rising demand for flavored beverages, functional drinks, and ready-to-consume products across both developed and emerging economies.Pharmaceutical producers continue to increase industrial sugar procurement for medicinal syrups and oral dosage formulations, particularly in developing regions experiencing healthcare infrastructure expansion. Export-oriented confectionery manufacturing hubs across Asia and Europe are further strengthening demand through large-scale production for international markets. Emerging applications such as plant-based dairy alternatives and fermentation-derived nutraceutical ingredients are expanding the industrial usage scope of sugar, positioning it as a multifunctional processing input across evolving food innovation sectors.

Explore more data points, trends and opportunities Download Free Sample Report

Industrial Sugar Market Segmentations

By Product Type

- White Refined Sugar

- Liquid Sugar

- Brown Sugar

- Invert Sugar

- Specialty & Customized Sugar Blends

By Application

- Food Processing

- Beverage Manufacturing

- Pharmaceutical & Nutraceutical

- Fermentation & Bio-industrial Applications

- Bakery & Confectionery

By Form

- Granulated

- Powdered

- Liquid

By Distribution Channel

- Direct Industrial Supply

- Industrial Wholesalers

- Ingredient Solution Providers

Regional Insights

Asia-Pacific

Asia-Pacific leads the global industrial sugar market with approximately 41% market share in 2025, supported by rapid industrialization of food manufacturing and strong population-driven consumption demand across China, India, Indonesia, and Thailand. Regional growth is primarily driven by expanding middle-class populations, increasing urbanization, and rising consumption of packaged foods and beverages. China’s large beverage and processed food industries sustain consistent bulk procurement, while India’s expanding confectionery, bakery, and dairy processing sectors significantly contribute to regional demand growth.Additional regional growth drivers include government support for food processing investments, expansion of modern retail infrastructure, and rising exports of processed foods from Southeast Asia. Increasing foreign direct investment in food manufacturing facilities and improvements in cold-chain logistics are further accelerating industrial sugar consumption, making Asia-Pacific the fastest-growing regional market with projected CAGR exceeding 6%.

North America

North America accounts for nearly 21% of global demand, supported by highly advanced food processing infrastructure and strong industrial automation across the United States and Canada. Regional growth is driven by continuous product innovation in beverages, bakery products, and functional foods, alongside stable demand from pharmaceutical manufacturing. The U.S. dominates regional consumption due to its large-scale beverage production capacity and diversified processed food sector.Additional growth drivers include technological advancements in manufacturing efficiency, increased demand for specialty and customized sugar formulations, and expansion of ready-to-drink beverage categories. Although growth remains moderate compared to emerging regions, consistent consumption patterns and supply chain sophistication ensure long-term market stability.

Europe

Europe maintains strong industrial sugar demand led by Germany, France, and the United Kingdom, supported by well-established sugar beet cultivation and advanced refining infrastructure. Regional growth is increasingly shaped by premium food production, reformulation initiatives, and demand for specialty sugar applications used in artisanal and high-quality processed foods.Key growth drivers include innovation in confectionery exports, strong bakery traditions, and rising demand for clean-label and functional food products. Additionally, regulatory frameworks encouraging product differentiation and sustainable sourcing practices are pushing manufacturers toward value-added sugar applications rather than purely volume-driven consumption.

Middle East & Africa

The Middle East and Africa region is witnessing rising industrial sugar demand driven by rapid population growth, urban expansion, and increasing investments in domestic food manufacturing aimed at reducing reliance on imports. Saudi Arabia, the UAE, South Africa, and Egypt represent major consumption centers supported by expanding beverage bottling operations and confectionery production facilities.Regional growth drivers include government-led food security initiatives, expansion of modern retail channels, and increasing consumption of packaged foods among younger populations. Investments in local processing plants and regional distribution networks are further strengthening industrial ingredient demand across the region.

Latin America

Brazil and Mexico dominate regional industrial sugar demand, supported by strong sugarcane production capabilities and export-oriented food and beverage industries. Brazil plays a particularly significant role due to its integrated sugar-ethanol industry, where industrial sugar demand is closely linked with biofuel production cycles.Growth in the region is driven by abundant raw material availability, competitive production costs, and expanding processed food exports to North America and global markets. Increasing beverage consumption, improving manufacturing infrastructure, and favorable agricultural conditions continue to position Latin America as a strategically important supplier and consumer within the global industrial sugar market.

Key Players in the Industrial Sugar Market

- Associated British Foods plc

- Südzucker AG

- Tereos Group

- Wilmar International Limited

- Cosan S.A.

- American Crystal Sugar Company

- Mitr Phol Group

- Nordzucker AG

- Rogers Sugar Inc.

- Thai Roong Ruang Group

- Illovo Sugar Africa

- Balrampur Chini Mills Ltd.

- Shree Renuka Sugars Ltd.

- Raízen S.A.

- LSU AgCenter Sugar Alliance Producers