Indoor Golf Simulator Market Size

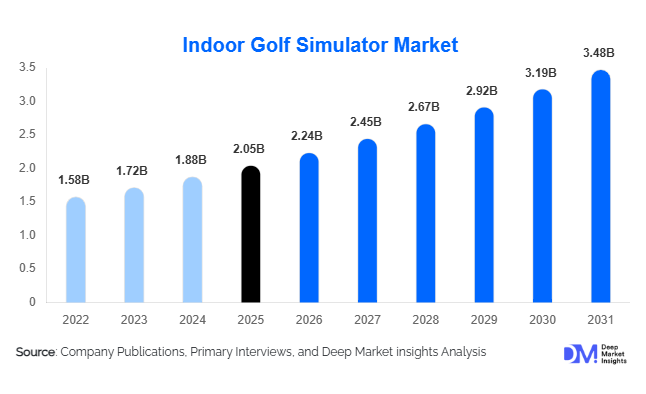

According to Deep Market Insights, the global indoor golf simulator market size was valued at USD 2.05 billion in 2025 and is projected to grow from USD 2.24 billion in 2026 to reach USD 3.48 billion by 2031, expanding at a CAGR of 9.2% during the forecast period (2026–2031). The market growth is primarily driven by increasing demand for year-round golf training, rising adoption of immersive sports entertainment solutions, technological advancements in launch monitoring and ball-tracking systems, and growing investments in golf entertainment venues globally. Indoor golf simulators have evolved from professional training tools into mainstream recreational platforms, supported by improvements in artificial intelligence (AI), virtual reality (VR), high-speed imaging technologies, and cloud-based performance analytics. Growing urbanization, limited availability of outdoor golf courses in densely populated regions, and rising consumer preference for premium home entertainment solutions are further contributing to market expansion.

Key Market Insights

- Commercial golf entertainment centers account for the largest share of global demand, supported by increasing consumer interest in social sports experiences and simulator-based competitions.

- AI-powered coaching and performance analytics are becoming major purchasing criteria, enabling users to access personalized training recommendations and real-time swing analysis.

- North America dominates the indoor golf simulator market, accounting for approximately 46% of global revenue due to strong golf participation rates and widespread adoption of premium simulator technologies.

- Asia-Pacific is the fastest-growing regional market, led by South Korea, China, Japan, and emerging opportunities in India.

- Residential installations are expanding rapidly, driven by affluent consumers seeking luxury home entertainment and sports training solutions.

- Advanced camera-based and hybrid tracking technologies are replacing traditional systems, improving accuracy, realism, and user engagement.

Indoor Golf Simulator Market Trends

AI-Powered Coaching and Performance Analytics Becoming Mainstream

Artificial intelligence is transforming the indoor golf simulator industry by enhancing player development and training efficiency. Modern simulator platforms increasingly incorporate machine learning algorithms capable of analyzing swing path, club speed, launch angle, spin rate, impact location, and shot dispersion. These systems provide customized coaching recommendations and personalized training plans that help golfers improve performance more efficiently than traditional practice methods. Cloud-connected software platforms allow users to track progress over time, compare results with peers, and participate in virtual tournaments. The growing popularity of data-driven coaching among amateur and professional golfers is accelerating software subscription revenues and creating recurring income streams for simulator manufacturers.

Growth of Golf Entertainment Venues and Simulator Lounges

Commercial golf entertainment venues are becoming a significant growth driver across North America, Europe, and Asia-Pacific. Indoor golf lounges, simulator cafés, hospitality venues, and golf entertainment centers are attracting consumers seeking social sports experiences that require less time commitment than traditional golf. These venues combine food and beverage offerings with competitive simulator gaming, creating attractive business models for operators. Urban consumers increasingly prefer convenient and weather-independent golf experiences, encouraging investments in multi-bay simulator facilities. Franchise expansion and private equity investment in golf entertainment concepts are expected to accelerate this trend over the forecast period.

Indoor Golf Simulator Market Drivers

Technological Advancements in Tracking and Simulation Accuracy

The increasing sophistication of launch monitors, radar systems, optical tracking technologies, and simulation software continues to drive market growth. Premium indoor golf simulators now provide highly accurate measurements of ball flight, club path, spin rates, and impact dynamics, enabling users to replicate real-world golf experiences indoors. Advancements in high-speed cameras, infrared sensors, and AI-powered analytics have improved realism and training effectiveness, encouraging adoption among professionals, academies, and recreational golfers alike.

Growing Demand for Year-Round Golf Participation

Indoor golf simulators enable uninterrupted golf practice regardless of weather conditions, seasonal limitations, or geographic constraints. In regions with harsh winters or dense urban environments, simulators offer a practical alternative to traditional outdoor courses. Rising consumer interest in maintaining golf performance throughout the year is supporting demand from residential users, golf academies, and commercial entertainment facilities. This trend is particularly evident in North America, Canada, Northern Europe, Japan, and South Korea.

Indoor Golf Simulator Market Restraints

High Initial Investment Costs

The adoption of premium simulator systems remains constrained by substantial upfront investment requirements. Commercial-grade simulators often cost between USD 20,000 and USD 100,000 or more when installation, software licensing, and supporting infrastructure are included. These costs can be prohibitive for small businesses, golf academies, and individual consumers, limiting market penetration in price-sensitive regions.

Space and Infrastructure Constraints

Indoor golf simulators require adequate ceiling height, room dimensions, and installation space to operate effectively. Residential users living in apartments or compact urban housing may face physical limitations that restrict installation feasibility. Commercial facilities also need dedicated infrastructure investments, creating additional barriers to adoption in certain markets.

Indoor Golf Simulator Market Opportunities

Expansion Across Emerging Asian Markets

Asia-Pacific presents substantial growth opportunities due to increasing golf participation rates, rising disposable incomes, and growing interest in sports technology. Countries such as China, India, Vietnam, Thailand, and Indonesia are witnessing increased investment in golf infrastructure and entertainment facilities. Urbanization and limited land availability make indoor golf simulators particularly attractive in densely populated metropolitan areas. As awareness of simulator technology improves, manufacturers and operators are expected to benefit from significant untapped demand throughout the region.

Integration of Virtual Reality and Mixed Reality Technologies

The convergence of golf simulation with VR and mixed reality technologies presents significant opportunities for market participants. Immersive virtual environments can enhance realism, engagement, and entertainment value, attracting younger demographics and non-traditional golfers. Future systems are expected to combine advanced graphics, haptic feedback, and real-time multiplayer functionality to create highly interactive golf experiences. These innovations could expand the addressable market beyond traditional golf enthusiasts into broader gaming and entertainment segments.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2.05 Billion |

| Market Size in 2026 | USD 2.24 Billion |

| Market Size in 2031 | USD 3.48 Billion |

| CAGR | 9.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Offering Insights

Hardware remains the dominant offering segment, accounting for approximately 58% of the global indoor golf simulator market revenue in 2025, primarily due to the high capital value associated with launch monitors, tracking systems, projectors, impact screens, simulator enclosures, and computing infrastructure. Hardware continues to lead because simulator performance, accuracy, and user experience are largely determined by sensor precision and tracking capabilities. Commercial operators, golf academies, and professional training facilities consistently prioritize investments in premium hardware to improve shot-tracking accuracy, ball-flight simulation, and player analytics. The growing adoption of high-speed camera systems, radar-based launch monitors, and integrated sensor platforms has further increased average selling prices across the hardware category. Among hardware components, launch monitors and tracking systems represent the largest revenue contribution owing to their critical role in capturing ball speed, launch angle, spin rates, club path, and impact data. The increasing use of simulator technology by golf coaches, professional players, and training facilities has accelerated demand for premium-grade tracking solutions capable of delivering near-real-world accuracy.

Software is the fastest-growing offering segment, supported by the industry's transition toward recurring subscription-based revenue models. Simulator providers are increasingly incorporating AI-powered swing analysis, cloud-based performance tracking, virtual course libraries, online tournaments, and personalized coaching recommendations into their software ecosystems. As operators seek to improve customer retention and engagement, software platforms are becoming a key differentiator within the market. Service revenues are also expanding steadily as commercial customers increasingly require installation, maintenance, calibration, technical support, and simulator management services to maximize operational uptime and customer experience.

Technology Insights

Camera-based tracking systems lead the indoor golf simulator market with an estimated 41% share of global revenue in 2025, driven by their superior indoor accuracy and ability to capture detailed club and ball movement data. These systems utilize multiple high-speed cameras to record impact conditions and ball flight immediately after contact, generating highly precise measurements that are particularly valuable for golf academies, professional golfers, and commercial simulator venues. The segment's leadership is supported by increasing demand for professional-grade training solutions and advancements in computer vision technologies. Camera-based systems perform exceptionally well in indoor environments where radar systems may face spatial limitations, making them the preferred choice for indoor golf centers and residential installations. The growing availability of AI-enabled analytics software further enhances the value proposition of camera-based systems by converting raw performance data into actionable coaching insights.

Hybrid tracking systems that combine radar, optical cameras, infrared sensors, and machine-learning algorithms are emerging as a high-growth category. These systems offer improved accuracy across diverse playing environments while reducing measurement errors associated with individual tracking technologies. Radar-based tracking systems continue to maintain strong demand among professional training facilities and outdoor-indoor hybrid applications due to their ability to track full ball-flight trajectories. Looking ahead, LiDAR-based sensing, sensor fusion platforms, and next-generation computer vision technologies are expected to significantly improve simulation realism and expand technology adoption across premium installations.

Facility Type Insights

Indoor golf centers represent the largest facility segment globally, accounting for an estimated 38-40% of total market revenue in 2025. The segment's leadership is primarily driven by the rapid expansion of simulator-based entertainment venues, golf lounges, and indoor sports centers across major urban markets. These facilities benefit from diversified revenue streams including hourly simulator rentals, memberships, coaching programs, league competitions, food and beverage sales, and corporate event hosting. The increasing popularity of social golf experiences among younger demographics has significantly strengthened demand for commercial simulator venues. Unlike traditional golf courses, indoor golf centers offer year-round accessibility regardless of weather conditions, making them particularly attractive in regions with harsh winters or high urban density. Operators are increasingly deploying multi-bay facilities equipped with advanced simulator systems to maximize utilization rates and customer throughput.

Golf academies and training facilities remain an important growth segment, leveraging simulator technology to enhance player development through advanced performance analytics and swing diagnostics. Hospitality venues including luxury hotels, resorts, and cruise operators are increasingly integrating simulators as premium guest amenities to differentiate their offerings. Corporate facilities are also emerging as a niche but growing segment, utilizing golf simulators for employee wellness initiatives, networking events, customer engagement programs, and executive entertainment.

End-User Insights

Commercial users dominate the indoor golf simulator market, accounting for approximately 64% of global revenue in 2025. The segment's leadership is driven by strong investment activity among indoor golf centers, entertainment venues, golf clubs, sports complexes, and golf academies seeking to enhance customer engagement while generating recurring revenue streams. Commercial facilities typically deploy multiple simulator bays, resulting in significantly higher average transaction values compared to residential installations. The growing popularity of simulator-based tournaments, corporate golf events, and membership-based entertainment concepts has further strengthened commercial demand. Additionally, commercial operators increasingly view simulator technology as a scalable business model capable of delivering consistent year-round utilization independent of outdoor weather conditions.

Residential users represent the fastest-growing end-user segment, supported by rising disposable incomes, growing interest in home-based recreation, and increasing demand for luxury home entertainment solutions. The expansion of premium residential real estate developments and smart-home ecosystems is creating favorable conditions for simulator adoption among affluent consumers. Educational institutions, sports science centers, and professional sports organizations are also expanding their use of simulator technologies to improve athlete development, biomechanics research, and performance monitoring, creating additional opportunities for market participants.

Explore more data points, trends and opportunities Download Free Sample Report

Indoor Golf Simulator Market Segmentations

By Offering

- Hardware

- Software

- Services

By Technology

- Camera-Based Tracking Systems

- Radar-Based Tracking Systems

- Infrared Tracking Systems

- Hybrid Tracking Systems

- LiDAR & Advanced Sensor Systems

By Facility Type

- Indoor Golf Centers

- Golf Academies & Training Facilities

- Sports & Recreation Centers

- Hospitality Venues

- Corporate Facilities

- Residential Installations

By End User

- Commercial Users

- Residential Users

- Educational Institutions

- Professional Sports Organizations

Regional Insights

North America

North America accounted for approximately 46% of global indoor golf simulator market revenue in 2025, making it the largest regional market. The United States remains the dominant contributor, supported by one of the world's largest golfer populations, extensive commercial golf infrastructure, and strong consumer spending on sports technology and recreation. The region's leadership is driven by widespread adoption of simulator-based training among golf academies, increasing investments in golf entertainment venues, and growing demand for premium residential installations.

The rapid expansion of golf entertainment concepts, rising participation among younger demographics, and increasing integration of simulator technology into sports training programs continue to support market growth. Canada represents a significant secondary market, benefiting from long winter seasons that create strong demand for year-round indoor golf participation. High disposable income levels, advanced technology adoption, and a mature golf culture collectively position North America as the industry's largest revenue-generating region.

Europe

Europe represents the second-largest regional market, led by the United Kingdom, Germany, France, Sweden, and the Netherlands. Regional growth is driven primarily by unfavorable winter weather conditions, increasing interest in year-round golf training, and rising adoption of simulator technology among commercial operators and golf academies. The United Kingdom remains the largest market within Europe due to its well-established golf ecosystem and growing demand for indoor golf entertainment venues.

Germany and France are experiencing increasing simulator adoption as golf participation rates continue to rise and commercial operators invest in sports entertainment concepts. The region is also benefiting from increasing consumer interest in data-driven coaching and performance analytics. Growing investments in premium leisure facilities, simulator lounges, and hospitality venues are expected to further strengthen demand throughout the forecast period.

Asia-Pacific

Asia-Pacific accounted for approximately 29% of global market revenue in 2025 and is expected to remain the fastest-growing regional market, with double-digit growth anticipated throughout the forecast period. South Korea continues to serve as the global benchmark for simulator golf adoption, supported by high urban density, limited golf course availability, and a deeply established indoor golf culture. The country maintains one of the highest simulator penetration rates globally, with thousands of commercial golf simulator facilities in operation.

China is witnessing rapid market expansion due to rising disposable incomes, urbanization, growing middle-class participation in golf, and increasing investments in sports technology infrastructure. Japan remains a mature market characterized by strong demand for premium simulator systems and advanced training solutions. India is emerging as one of the most attractive long-term opportunities, driven by luxury residential developments, increasing golf participation among affluent consumers, and expanding investments in sports and leisure infrastructure. The region's growth is further supported by rising technology adoption and increasing demand for premium indoor entertainment experiences.

Latin America

Latin America remains an emerging growth market, with Brazil and Mexico accounting for the majority of regional demand. Market expansion is being driven by rising awareness of simulator technology, increasing investments in premium sports infrastructure, and growing adoption among luxury hospitality properties and private golf clubs. The region's affluent consumer segment is increasingly investing in residential simulator installations as part of luxury home entertainment projects.

Additionally, the expansion of golf participation across major metropolitan areas and the growing popularity of sports-focused leisure experiences are supporting market development. While overall penetration remains relatively low compared to North America and Asia-Pacific, improving economic conditions and increasing availability of mid-priced simulator systems are expected to create new growth opportunities.

Middle East & Africa

The Middle East & Africa region is emerging as a high-potential market, led by the United Arab Emirates and Saudi Arabia. Regional growth is being driven by substantial investments in sports tourism, luxury hospitality projects, entertainment infrastructure, and premium real estate developments. Government diversification initiatives, particularly Saudi Vision 2031, are encouraging investments in recreational and sports facilities that incorporate advanced simulator technologies.

The UAE continues to attract significant demand due to its concentration of luxury resorts, golf tourism destinations, and high-net-worth consumers. Indoor golf simulators are increasingly being deployed in hotels, mixed-use developments, private clubs, and residential projects to enhance visitor experiences and provide year-round golf accessibility despite extreme outdoor temperatures. Growing tourism arrivals, rising disposable incomes, and increasing adoption of smart entertainment technologies are expected to support long-term regional market expansion.

Key Players in the Indoor Golf Simulator Market

- Golfzon

- TrackMan

- Foresight Sports

- Full Swing Golf

- SkyTrak

- Uneekor

- aboutGOLF

- FlightScope

- Toptracer

- Garmin

- Rapsodo

- HD Golf

- OptiShot Golf

- X-Golf

- TruGolf