Indian Ready-To-Eat Meals Market Size

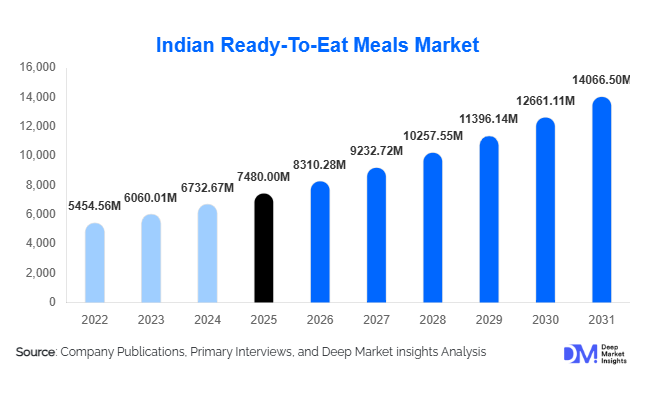

According to Deep Market Insights, the global Indian ready-to-eat (RTE) meals market size was valued at USD 7,480 million in 2025 and is projected to grow from USD 8,310.28 million in 2026 to reach approximately USD 14,066.50 million by 2031, expanding at a CAGR of 11.1% during the forecast period (2026–2031). The market growth is primarily driven by rising urbanization, increasing dual-income households, global demand for convenient ethnic cuisines, and technological advancements in food processing and packaging. Indian cuisine’s global popularity, supported by diaspora expansion and quick-service food culture, has transformed ready-to-eat meals into a mainstream convenience category across retail and foodservice channels.

The industry has evolved from shelf-stable packaged curries into a diversified ecosystem including frozen meals, chilled regional dishes, plant-based Indian foods, and premium gourmet offerings. Rapid expansion of organized retail, e-commerce grocery platforms, and direct-to-consumer food brands has significantly improved product accessibility worldwide. Consumers increasingly prefer authentic, preservative-minimized meals with restaurant-quality taste, encouraging manufacturers to invest in retort packaging, high-pressure processing, and clean-label ingredient sourcing. Additionally, export-oriented production hubs in India are strengthening global supply chains, allowing brands to scale distribution across North America, Europe, and Asia-Pacific. With changing lifestyles favoring convenience without compromising cultural familiarity, the Indian RTE meals market is transitioning into a high-growth segment within the global packaged foods industry.

Key Market Insights

- Convenience-led consumption patterns are driving adoption among urban professionals and students globally.

- Frozen and chilled Indian meals are growing faster than shelf-stable formats due to improved taste perception.

- North America leads global consumption, supported by strong Indian diaspora demand and ethnic food penetration.

- Asia-Pacific is the fastest-growing region, driven by urbanization and expanding modern retail infrastructure.

- Premiumization trends are encouraging gourmet regional Indian meal launches.

- Technological packaging innovations such as retort pouches and microwave-ready trays are improving shelf life and export feasibility.

What are the latest trends in the Indian ready-to-eat meals market?

Premium Regional Cuisine Expansion

Manufacturers are increasingly launching region-specific Indian dishes such as Chettinad curries, Kashmiri gravies, Gujarati thalis, and South Indian rice preparations to cater to authenticity-focused consumers. Premiumization is enabling brands to differentiate beyond generic curry offerings, capturing higher margins while appealing to global consumers seeking cultural culinary experiences. This trend is particularly strong in export markets where ethnic authenticity drives repeat purchases.

Clean-Label and Health-Oriented RTE Innovation

Consumers are shifting toward preservative-free, low-sodium, and plant-based ready meals. Brands are reformulating products using natural stabilizers, whole grains, and organic ingredients. Vegan Indian meals, millet-based dishes, and protein-enriched recipes are gaining traction among health-conscious buyers. Transparent labeling and shorter ingredient lists are becoming competitive differentiators in supermarkets and online retail platforms.

What are the key drivers in the Indian ready-to-eat meals market?

Urban Lifestyle Transformation

Rapid urbanization and time-constrained lifestyles are accelerating demand for convenient meal solutions. Working professionals increasingly rely on microwave-ready foods that reduce cooking time while maintaining traditional flavors. Rising female workforce participation globally further strengthens demand for packaged meals requiring minimal preparation.

Global Expansion of Indian Cuisine

Indian food has transitioned into a mainstream global cuisine category. Restaurants, food delivery apps, and international tourism have expanded familiarity with Indian flavors, encouraging retail consumption of packaged Indian meals. Diaspora populations across the U.S., U.K., Canada, and the Middle East act as core demand anchors, while non-Indian consumers are adopting Indian RTE products for variety and vegetarian meal options.

What are the restraints for the global market?

Perception of Processed Foods

Despite technological improvements, some consumers associate ready meals with preservatives and lower nutritional value. Overcoming this perception requires continuous innovation in clean-label processing and transparent marketing.

Cold Chain and Logistics Constraints

Frozen and chilled product expansion depends heavily on cold-chain infrastructure. Developing regions face logistical challenges that increase distribution costs and limit market penetration beyond major urban centers.

What are the key opportunities in the Indian ready-to-eat meals industry?

E-commerce and Direct-to-Consumer Growth

Online grocery platforms and subscription meal services present significant opportunities for new entrants. Digital channels enable brands to target niche audiences, launch limited regional menus, and gather real-time consumer insights for product innovation.

Export-Led Manufacturing Expansion

India’s role as a global production hub is strengthening due to cost advantages and government export incentives. Manufacturers are expanding export-certified facilities to meet international food safety standards, enabling penetration into Western retail chains.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 7480 Million |

| Market Size in 2026 | USD 8310.28 Million |

| Market Size in 2031 | USD 14066.50 Million |

| CAGR | 11.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Shelf-stable ready meals continue to dominate the global Indian ready-to-eat (RTE) meals market, accounting for nearly 42% of global revenue in 2025. The segment’s leadership is primarily supported by its extended shelf life, ease of transportation, and strong compatibility with export-oriented distribution models. Manufacturers increasingly prefer shelf-stable formats due to lower cold-chain dependency, improved inventory management, and suitability for cross-border trade. Growing demand from international retailers and institutional buyers further strengthens this segment, as shelf-stable meals reduce logistics complexity while ensuring consistent product availability. Frozen Indian meals represent the fastest-growing product category, driven by advancements in freezing technologies that preserve flavor authenticity and texture quality. Rising freezer penetration across developed economies, combined with premium positioning and restaurant-quality meal expectations, continues to accelerate adoption. Chilled ready meals are gaining traction in organized retail and premium grocery chains, particularly among consumers seeking fresher meal alternatives with minimal preparation time. Meanwhile, instant Indian snack meals are expanding rapidly among younger consumers and urban professionals, supported by changing lifestyles, smaller household sizes, and increasing demand for quick, affordable meal solutions aligned with on-the-go consumption patterns.

Meal Category Insights

Curry-based meals hold the leading share at approximately 38% of total market demand, supported by strong global familiarity with Indian cuisine and widespread acceptance of dishes such as paneer curries, lentil-based preparations, and spiced gravies. The segment’s leadership is driven by flavor versatility, compatibility with multiple dietary preferences including vegetarian and vegan diets, and strong adaptability across international markets. Rice-based meals follow closely, benefiting from one-bowl convenience formats that simplify meal preparation while delivering balanced nutrition and portion control. The increasing popularity of ready biryani, pulao, and rice-lentil combinations reflects consumer preference for complete meal solutions that require minimal preparation. Regional thali combinations are emerging as high-value offerings, enabling brands to deliver authentic culinary experiences through curated multi-dish formats. This trend aligns with growing consumer interest in cultural authenticity, premiumization, and experiential food consumption, encouraging manufacturers to innovate with region-specific recipes and heritage-inspired meal kits.

Packaging Format Insights

Retort pouches lead packaging adoption with around 46% market share, primarily due to their ability to extend shelf life without refrigeration while maintaining product safety and taste quality. The lightweight structure reduces transportation costs and supports export scalability, making retort technology a preferred choice among large-scale manufacturers. Continuous innovation in multilayer barrier films further enhances durability and heat resistance, strengthening the segment’s leadership. Microwaveable trays are expanding rapidly as consumers increasingly prioritize convenience and minimal preparation time. These formats are particularly popular in urban households and premium retail channels where ready-to-heat meals align with fast-paced lifestyles. At the same time, sustainable packaging solutions are gaining importance as brands respond to tightening environmental regulations and rising consumer awareness around packaging waste. Companies are investing in recyclable materials, reduced plastic usage, and eco-friendly packaging innovations to meet sustainability commitments while maintaining product integrity.

Distribution Channel Insights

Modern retail supermarkets account for approximately 40% of global sales, benefiting from strong product visibility, organized shelf placement, and impulse purchase behavior among consumers exploring international cuisines. Retail expansion and the growing presence of global supermarket chains have enabled wider accessibility of Indian RTE meals across developed markets. Online retail represents the fastest-growing distribution channel, supported by rapid digital grocery adoption, direct-to-consumer platforms, and subscription-based meal delivery services. E-commerce platforms allow brands to reach niche consumer groups, including diaspora communities and health-focused buyers, while enabling efficient product launches and targeted marketing strategies. Ethnic specialty stores continue to play a critical role, particularly in diaspora-driven markets, where authenticity, regional product variety, and brand familiarity strongly influence purchasing decisions.

End-Use Insights

Household consumption dominates overall demand with nearly 68% market share in 2025, driven by increasing preference for convenient home dining solutions amid busy lifestyles and rising dual-income households. Consumers increasingly rely on ready meals as substitutes for traditional cooking during weekdays while maintaining familiarity with cultural flavors. The foodservice segment is expanding rapidly as airlines, institutional catering providers, and quick-service restaurants adopt Indian RTE meals to enhance operational efficiency, reduce preparation time, and maintain menu consistency. Export-driven demand from hospitality and travel catering is emerging as a strong growth contributor, particularly within aviation catering, cruise tourism, and packaged travel services, where standardized meal formats improve scalability and cost management.

Explore more data points, trends and opportunities Download Free Sample Report

Indian Ready-To-Eat Meals Market Segmentations

By Product Type

- Shelf-Stable Meals

- Frozen Meals

- Chilled Meals

- Instant Snack Meals

By Meal Category

- Curry-Based Meals

- Rice-Based Meals

- Regional Thalis

- Snack Packs & Quick Meals

By Packaging Format

- Retort Pouches

- Microwave Trays

- Vacuum-Sealed Packs

- Eco-Friendly Sustainable Packaging

By Distribution Channel

- Modern Retail

- Online Retail / D2C Platforms

- Ethnic Specialty Stores

- Foodservice & Institutional Channels

By End-Use

- Household Consumption

- Foodservice & Hospitality

- Institutional Catering

Regional Insights

North America

North America accounted for nearly 32% of global market share in 2025, led by the United States and Canada. Market expansion is supported by large South Asian diaspora populations, strong purchasing power, and increasing consumer openness toward global cuisines. The rapid expansion of ethnic food aisles across major retail chains has significantly improved product accessibility. Additionally, rising demand for plant-based and vegetarian meals aligns well with Indian cuisine offerings, strengthening category penetration. Growth is further driven by busy urban lifestyles, increasing adoption of convenient meal formats, and strong e-commerce grocery ecosystems that enable direct access to international food brands. Institutional adoption across airlines and corporate catering also contributes to regional market expansion.

Asia-Pacific

Asia-Pacific held approximately 29% market share and represents the fastest-growing regional market. India serves as both the primary manufacturing hub and a major consumption center due to expanding urbanization, rising disposable incomes, and increasing demand for convenient packaged foods. Government initiatives supporting food processing infrastructure and export promotion further strengthen regional production capabilities. Markets such as Australia, Singapore, and Japan are witnessing rising adoption of packaged Indian cuisine among urban consumers seeking diverse international flavors. Growth is also supported by modern retail expansion, increasing working populations, and rapid digital commerce penetration across metropolitan areas.

Europe

Europe demonstrates strong growth led by the United Kingdom, Germany, and France, with the U.K. contributing a significant share due to long-standing cultural acceptance of Indian cuisine. Regional growth is driven by rising demand for vegetarian, vegan, and clean-label food products, categories where Indian meals naturally align with consumer preferences. Increasing multicultural populations, expansion of private-label ready meals, and premium supermarket offerings continue to accelerate adoption. Sustainability-focused consumption trends and regulatory emphasis on transparent labeling further encourage manufacturers to introduce healthier and ethically sourced meal options across Western Europe.

Middle East & Africa

The Middle East shows strong demand driven primarily by large expatriate populations in countries such as the UAE and Saudi Arabia. Ready meals are widely consumed by working professionals seeking familiar home-style food options that require minimal preparation. Rapid urban development, growing modern retail infrastructure, and expansion of premium supermarket chains continue to strengthen market penetration. Demand is further supported by hospitality growth, airline catering expansion, and increasing tourism inflows, which drive consistent consumption of standardized packaged meal solutions. In parts of Africa, gradual urbanization and retail modernization are beginning to create opportunities for market entry.

Latin America

Latin America represents an emerging growth market, with Brazil and Mexico showing gradual adoption through international retail expansion and increasing exposure to global cuisines. Rising middle-class populations, growing interest in international food experiences, and expanding supermarket networks are contributing to early-stage demand development. The increasing presence of multinational food brands and cross-cultural culinary influence through digital media platforms is expected to accelerate awareness and acceptance of Indian ready meals across major urban centers in the region.

Key Players in the Indian Ready-To-Eat Meals Market

- MTR Foods Pvt. Ltd.

- ITC Limited

- Tasty Bite Eatables Ltd.

- Haldiram’s

- Gits Food Products Pvt. Ltd.

- Kohinoor Foods Ltd.

- Deep Foods Inc.

- Saffron Road

- Nestlé S.A.

- General Mills Inc.

- McCormick & Company

- Amira Nature Foods Ltd.

- Bikaji Foods International Ltd.

- Godrej Tyson Foods Ltd.

- Patak’s (AB World Foods)