Iced Coffee Market Size

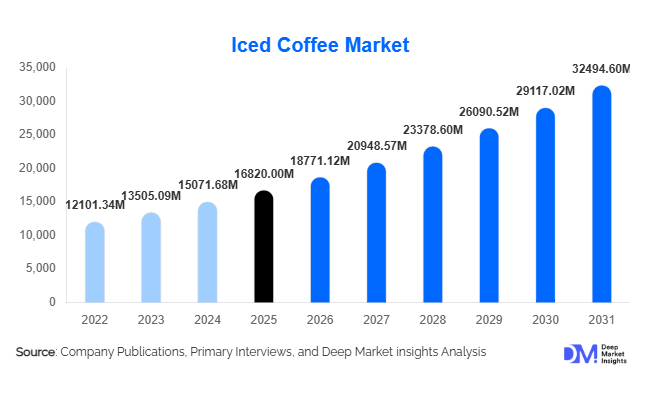

According to Deep Market Insights, the global iced coffee market size was valued at USD 16,820 million in 2025 and is projected to grow from USD 18,771.12 million in 2026 to reach USD 32,494.60 million by 2031, expanding at a CAGR of 11.6% during the forecast period (2026–2031). Market expansion is primarily driven by rising demand for ready-to-drink (RTD) beverages, increasing café culture adoption, and shifting consumer preference toward convenient, premium, and cold coffee formats. Rapid urbanization, evolving consumption habits among millennials and Gen Z, and innovation in plant-based and functional beverage formulations are further accelerating global adoption of iced coffee products.

Key Market Insights

- Ready-to-drink iced coffee dominates global consumption, supported by expanding retail distribution and on-the-go beverage demand.

- Premium and specialty iced coffee formats are gaining traction as consumers seek café-quality experiences at home and workplaces.

- North America leads global demand, driven by strong cold brew adoption and high per-capita coffee consumption.

- Asia-Pacific is the fastest-growing regional market, fueled by urban youth demographics and expanding café chains.

- Plant-based milk integration is reshaping product innovation, attracting health-conscious and lactose-intolerant consumers.

- Technological advancements in nitrogen infusion and cold brewing are enhancing product differentiation and shelf stability.

What are the latest trends in the iced coffee market?

Premiumization and Cold Brew Innovation

Cold brew and nitro iced coffee formats are transforming the competitive landscape by positioning iced coffee as a premium lifestyle beverage rather than a seasonal refreshment drink. Consumers increasingly associate cold brew with smoother taste profiles, higher caffeine concentration, and artisanal preparation methods. Beverage companies are investing heavily in nitrogen infusion technologies and flash brewing processes to replicate café-quality beverages in packaged formats. Premium packaging, sustainable sourcing certifications, and specialty bean selections are also becoming central to brand differentiation. As consumers shift away from sugary carbonated beverages, premium iced coffee is emerging as a healthier indulgence category with strong pricing power and higher margins.

Functional and Health-Oriented Beverage Expansion

The convergence of coffee and functional beverages represents one of the most significant trends shaping market growth. Manufacturers are introducing iced coffee enriched with protein, vitamins, adaptogens, and nootropics to appeal to wellness-focused consumers. Low-sugar, keto-friendly, and plant-based formulations are gaining popularity, particularly among younger demographics prioritizing health-conscious consumption. Functional iced coffee products are increasingly marketed as energy alternatives to traditional energy drinks, expanding consumption occasions beyond breakfast into fitness, work productivity, and afternoon refreshment segments.

What are the key drivers in the iced coffee market?

Growth of Ready-to-Drink Beverage Culture

Fast-paced urban lifestyles have significantly increased demand for convenient beverage solutions. RTD iced coffee products offer portability, consistent taste, and extended shelf life, making them ideal for modern consumers. Expansion of supermarkets, convenience stores, and online grocery platforms has enhanced accessibility, driving impulse purchases and repeat consumption. The integration of iced coffee into vending machines, corporate offices, and travel retail further supports sustained growth.

Expansion of Global Café Culture

The rapid proliferation of specialty coffee chains worldwide has educated consumers about cold coffee varieties, flavor customization, and premium brewing techniques. Café exposure has increased consumer willingness to pay premium prices for iced coffee beverages in retail formats. Emerging economies, particularly in Asia-Pacific, are witnessing strong café culture adoption among younger consumers, translating into higher retail iced coffee demand.

What are the restraints for the global market?

Volatility in Coffee Bean Prices

Fluctuating Arabica and Robusta coffee prices caused by climate variability and supply disruptions pose a major challenge for manufacturers. Rising input costs directly impact profit margins and retail pricing strategies, especially for premium iced coffee products reliant on specialty beans. Companies must increasingly rely on long-term sourcing agreements and diversified supplier networks to stabilize costs.

Cold Chain and Distribution Constraints

Iced coffee products often require temperature-controlled logistics to maintain quality, particularly in emerging markets with limited cold-chain infrastructure. Higher transportation and storage costs can limit penetration into rural and developing regions, slowing expansion despite rising consumer interest.

What are the key opportunities in the iced coffee industry?

Plant-Based and Dairy Alternative Expansion

The rising popularity of oat, almond, and soy milk presents significant opportunities for iced coffee manufacturers. Plant-based iced coffee appeals to vegan consumers, environmentally conscious buyers, and lactose-intolerant populations. Partnerships between coffee brands and alternative dairy producers are enabling rapid product diversification while supporting premium pricing strategies.

Emerging Market Urbanization

Rapid urbanization in countries such as India, China, Indonesia, and Vietnam is creating new consumer bases for iced coffee products. Younger populations exposed to Western beverage trends through social media and international café chains are accelerating category adoption. Affordable RTD formats tailored to local taste preferences are expected to unlock substantial growth potential across developing economies.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 16820 Million |

| Market Size in 2026 | USD 18771.12 Million |

| Market Size in 2031 | USD 32494.60 Million |

| CAGR | 11.6% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Ready-to-drink (RTD) iced coffee continues to dominate the global iced coffee market, accounting for nearly 48% of total market share in 2025. The leadership of this segment is primarily driven by shifting consumer lifestyles that favor convenience-oriented beverages requiring minimal preparation time. Increasing urbanization, busy work schedules, and the growing preference for portable caffeine solutions have significantly accelerated RTD adoption across both developed and emerging markets. Additionally, extended shelf life, wide flavor availability, and strong penetration across supermarkets, convenience stores, and online retail platforms further reinforce segment growth. Beverage manufacturers are continuously investing in functional formulations, including low-sugar, plant-based, and protein-enriched variants, which strengthen consumer engagement and repeat purchases.Cold brew iced coffee represents the fastest-growing product category, supported by rising consumer demand for smoother, less acidic flavor profiles and premium beverage experiences. The longer steeping process associated with cold brew enhances perceived quality, allowing brands to position products at higher price points. Increasing consumer awareness regarding specialty coffee preparation methods, coupled with café-driven education and social media influence, continues to accelerate cold brew adoption globally. Premiumization trends within beverages further support expansion as consumers increasingly trade up from traditional iced coffee options.Nitro iced coffee is gaining substantial momentum, particularly in developed markets, as nitrogen infusion creates a creamy texture and visually appealing cascading effect that enhances sensory appeal. This innovation allows brands and foodservice operators to differentiate offerings while replicating draft-style beverage experiences. Freshly prepared iced coffee remains highly relevant within foodservice environments, supported by the rapid expansion of café chains, specialty coffee outlets, and quick-service restaurant beverage programs. Customization options, including flavor additions and milk alternatives, continue to strengthen consumer preference for freshly prepared formats.

Coffee Type Insights

Arabica-based iced coffee leads the market with approximately 62% share of global consumption, driven by strong consumer preference for smoother taste profiles, balanced acidity, and premium brand positioning. The growing influence of specialty coffee culture has reinforced Arabica’s dominance, as consumers increasingly associate the variety with quality and authenticity. Expanding availability of ethically sourced and certified coffee beans also supports the segment’s growth, aligning with sustainability-conscious purchasing behaviors.Blended coffee variants maintain significant relevance within mass-market categories due to their cost efficiency and flavor consistency. These blends enable manufacturers to balance pricing strategies while maintaining scalable production, particularly in emerging economies where price sensitivity remains a key purchasing factor. Blended formulations also allow brands to tailor flavor intensity to regional taste preferences, supporting broader market accessibility.Specialty and single-origin iced coffee products are expanding rapidly within premium retail and online channels, reflecting increasing consumer interest in origin transparency, traceability, and artisanal production methods. Younger consumers and specialty coffee enthusiasts are driving demand for differentiated flavor experiences, encouraging brands to introduce limited-edition offerings and region-specific sourcing narratives that enhance brand storytelling and perceived value.

Packaging Insights

Aluminum cans account for nearly 41% of global iced coffee packaging demand, emerging as the leading packaging format due to their lightweight structure, portability, and strong recyclability profile. The compatibility of cans with nitrogen infusion technology has further strengthened adoption within the growing nitro coffee segment. In addition, aluminum packaging supports faster cooling and improved product preservation, making it particularly suitable for on-the-go consumption environments.Bottled formats continue to maintain widespread usage across supermarkets and convenience retail channels, offering larger serving sizes and resealable functionality that appeal to household consumers. Plastic and glass bottles remain popular in regions where multi-serve consumption and family purchasing patterns are common. Meanwhile, carton packaging is expanding steadily in environmentally conscious markets, supported by increasing regulatory pressure and consumer demand for sustainable packaging alternatives.On-tap keg systems are emerging within foodservice environments, enabling cafés and restaurants to serve fresh nitro iced coffee efficiently while reducing packaging waste. This format aligns with experiential beverage trends, allowing operators to deliver premium draft-style beverages while improving operational efficiency.

Distribution Channel Insights

Supermarkets and hypermarkets remain the dominant distribution channel, contributing roughly 36% of global sales. Their leadership is supported by high product visibility, diversified brand assortments, promotional pricing strategies, and consumer preference for one-stop shopping experiences. The expansion of organized retail infrastructure across developing economies continues to strengthen this channel’s influence, enabling wider accessibility of RTD iced coffee products.Convenience stores play a critical role in driving impulse consumption, particularly among urban consumers seeking immediate refreshment solutions. Strategic product placement near checkout areas, refrigerated displays, and single-serve packaging formats significantly enhance purchase frequency within this channel. Increasing commuter populations and extended retail operating hours further support demand growth.Online retail and direct-to-consumer platforms are witnessing rapid expansion as beverage brands increasingly leverage digital marketing, subscription-based delivery models, and personalized promotions. E-commerce enables niche and premium brands to reach wider audiences without heavy reliance on physical retail distribution, while data-driven consumer insights allow companies to optimize product offerings and pricing strategies.

End-Use Insights

Household consumption represents the largest end-use segment, driven by the growing trend of replicating café-style beverage experiences at home. The expansion of remote and hybrid working models has accelerated at-home beverage consumption, encouraging consumers to purchase ready-to-drink iced coffee as a convenient alternative to traditional brewing. Increased availability of premium and functional variants further supports household adoption.Foodservice applications represent the fastest-growing segment, supported by aggressive expansion of café chains, specialty coffee outlets, and quick-service restaurant beverage innovation. Operators are increasingly incorporating iced coffee into seasonal menus and customizable beverage programs, which drives higher customer engagement and incremental revenue generation.Corporate offices, universities, and travel hubs are emerging as important consumption channels through vending machines, smart beverage dispensers, and institutional beverage partnerships. Rising demand for convenient caffeine solutions in workplaces and transit environments continues to strengthen institutional adoption. Export-driven demand is also increasing as Asian markets import branded RTD iced coffee products from North America and Europe, contributing to cross-border brand expansion.

Explore more data points, trends and opportunities Download Free Sample Report

Iced Coffee Market Segmentations

By Product Type

- Ready-to-Drink (RTD) Iced Coffee

- Cold Brew Iced Coffee

- Nitro Iced Coffee

- Freshly Prepared Iced Coffee

By Coffee Type

- Arabica Iced Coffee

- Robusta Iced Coffee

- Coffee Blends

- Specialty & Single-Origin Coffee

By Packaging

- Aluminum Cans

- Plastic & Glass Bottles

- Carton Packaging

- Kegs & On-Tap Systems

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail & Direct-to-Consumer

- Foodservice & Café Chains

- Vending Machines & Institutional Sales

By End Use

- Household Consumption

- Foodservice Industry

- Corporate & Institutional Consumption

- Travel, Hospitality & Leisure

Regional Insights

North America

North America holds approximately 34% of the global iced coffee market share, led primarily by the United States. Regional growth is driven by strong cold brew adoption, high per-capita coffee consumption, and a well-established specialty coffee ecosystem. Advanced retail infrastructure enables rapid product launches and nationwide distribution, while consumer willingness to experiment with premium beverages accelerates innovation. The rising popularity of functional beverages, including low-sugar, dairy-free, and protein-enriched iced coffee variants, further supports demand expansion. Additionally, strong café culture, widespread adoption of mobile ordering platforms, and continuous menu innovation by major coffee chains sustain long-term market growth.

Europe

Europe accounts for nearly 21% of global market share, supported by increasing adoption of iced coffee beyond traditionally hot-coffee-dominated markets. Growth across the United Kingdom, Germany, and France is driven by evolving consumer preferences among younger demographics seeking convenient and refreshing coffee alternatives. Sustainability-focused purchasing behavior plays a significant role, encouraging brands to adopt recyclable packaging, ethical sourcing certifications, and carbon-conscious production practices. Expansion of premium private-label offerings by major retailers has improved affordability while maintaining quality perception, contributing to broader market penetration. Seasonal consumption trends and expanding café culture further reinforce regional demand.

Asia-Pacific

Asia-Pacific represents about 29% of global demand and remains the fastest-growing regional market, expanding at nearly 14% CAGR. Rapid urbanization, rising disposable incomes, and Western lifestyle influence are major growth drivers across China, India, and Southeast Asia. Japan and South Korea continue to lead innovation in canned and vending-machine coffee formats, setting global benchmarks for convenience beverages. The rapid expansion of international and domestic café chains, coupled with increasing youth population and digital retail adoption, significantly accelerates iced coffee consumption. Growing acceptance of ready-to-drink beverages among first-time coffee consumers further strengthens long-term growth potential across the region.

Latin America

Latin America holds approximately 9% market share, led by Brazil and Mexico. Despite being major coffee-producing regions, RTD iced coffee consumption is still in an early development phase, creating substantial untapped opportunities. Regional growth is supported by increasing urban middle-class populations, modernization of retail infrastructure, and rising exposure to global beverage trends. Product localization strategies, including sweeter flavor profiles and culturally tailored formulations, are helping brands improve consumer adoption. Expanding supermarket penetration and growing investment by multinational beverage companies are expected to accelerate market maturity over the forecast period.

Middle East & Africa

The Middle East & Africa region accounts for nearly 7% of global demand, with the UAE and Saudi Arabia emerging as key premium consumption hubs. Market growth is driven by rising café culture, expanding tourism sectors, and increasing youth demographics seeking modern beverage experiences. High temperatures across many countries naturally support demand for chilled beverages, strengthening iced coffee consumption throughout the year. Rapid development of shopping malls, hospitality infrastructure, and international coffee chains further enhances product visibility and accessibility. Additionally, growing disposable income levels and social-media-driven lifestyle trends are encouraging adoption of premium ready-to-drink coffee formats across urban centers.

Key Players in the Iced Coffee Market

- Starbucks Corporation

- Nestlé S.A.

- The Coca-Cola Company

- PepsiCo Inc.

- JAB Holding Company

- Dunkin’ Brands Group

- Suntory Holdings Limited

- UCC Ueshima Coffee Co.

- Illycaffè S.p.A.

- Strauss Group Ltd.

- Tata Consumer Products Ltd.

- Califia Farms LLC

- Danone S.A.

- Asahi Group Holdings Ltd.

- Luigi Lavazza S.p.A.