Hydrolysed Vegetable Protein (HVP) Market Size

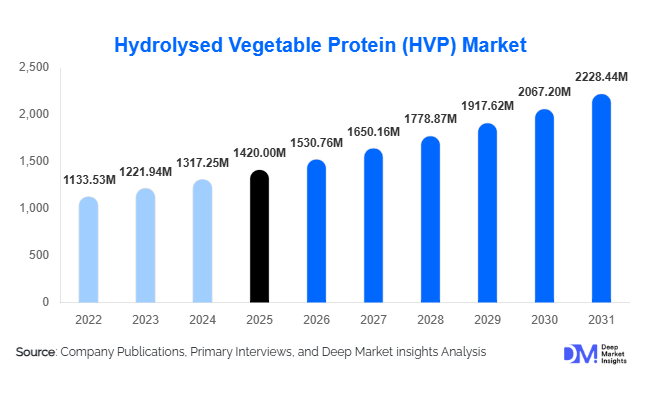

According to Deep Market Insights, theglobal hydrolysed vegetable protein (HVP) market size was valued at USD 1,420 million in 2025 and is projected to grow from USD 1,530.76 million in 2026 to reach approximately USD 2,228.44 million by 2031, expanding at a CAGR of 7.8% during the forecast period (2026–2031). Market expansion is primarily driven by the rapid adoption of plant-based ingredients, increasing demand for clean-label flavor enhancers, and rising consumption of processed and convenience foods globally. HVP is widely utilized as a cost-efficient umami enhancer and protein fortification ingredient across food processing, foodservice, and industrial seasoning applications.

The market continues to evolve alongside global dietary transitions toward plant-based nutrition and sustainable food systems. Food manufacturers are increasingly replacing animal-derived flavor bases with vegetable protein hydrolysates derived from soy, wheat, pea, and corn sources. Additionally, advancements in enzymatic hydrolysis technologies have improved flavor profiles, reduced bitterness, and enhanced functional performance, expanding applications in premium and health-oriented foods. Emerging economies across Asia-Pacific and Latin America are witnessing strong growth due to urbanization, expanding packaged food consumption, and rising middle-class spending. Meanwhile, developed markets in North America and Europe are emphasizing non-GMO, allergen-free, and low-sodium HVP variants aligned with regulatory and consumer expectations. The convergence of flavor innovation, sustainability goals, and protein diversification is positioning HVP as a strategic ingredient within the global food ingredients industry.

Key Market Insights

- Plant-based flavor enhancers are replacing traditional meat extracts across processed foods and instant meal categories.

- Asia-Pacific dominates production and consumption, supported by large-scale food manufacturing ecosystems.

- Enzymatic hydrolysis technology adoption is improving taste quality and clean-label positioning.

- Demand from snacks and ready-to-eat foods continues to drive bulk industrial consumption.

- Non-allergen and gluten-free HVP variants are emerging as premium product categories.

- Export-driven seasoning manufacturing in China and Southeast Asia strengthens global supply chains.

What are the latest trends in the hydrolysed vegetable protein market?

Shift Toward Clean-Label and Natural Flavor Systems

Food manufacturers are reformulating products to eliminate artificial flavor enhancers such as monosodium glutamate (MSG) while maintaining savory taste intensity. Hydrolysed vegetable protein serves as a natural umami ingredient, enabling label-friendly formulations. Clean-label positioning has become especially important in Europe and North America, where regulatory scrutiny and consumer awareness are higher. Manufacturers increasingly market HVP as a “natural flavor” or “plant protein extract,” supporting premium product positioning.

Expansion of Plant-Based Meat Alternatives

The growth of plant-based meat and dairy alternatives has significantly increased demand for functional protein ingredients capable of delivering meaty taste and mouthfeel. HVP provides amino acids and flavor precursors essential for replicating meat-like sensory attributes. Food innovators are integrating customized HVP blends into burgers, sausages, and ready meals to enhance flavor depth without increasing formulation costs.

What are the key drivers in the hydrolysed vegetable protein market?

Growth of Processed and Convenience Food Consumption

Urban lifestyles and dual-income households are accelerating demand for ready-to-eat meals, instant noodles, soups, and savory snacks. HVP plays a crucial role as a flavor enhancer and protein fortification ingredient in these categories. Global packaged food production continues to expand, particularly across Asia-Pacific, directly increasing ingredient demand.

Rising Adoption of Plant-Based Diets

Consumers are increasingly adopting flexitarian and vegetarian diets, creating demand for plant-derived protein solutions. HVP provides a cost-effective alternative to animal proteins while supporting sustainability narratives. Foodservice operators and quick-service restaurants are also reformulating menus using plant-derived flavor systems.

Technological Advancements in Enzymatic Hydrolysis

Modern enzymatic processes allow precise protein breakdown, improving flavor consistency and reducing undesirable notes historically associated with acid hydrolysis. These advancements enable broader applications in premium foods and health-focused formulations.

What are the restraints for the global market?

Allergen Concerns Related to Soy and Wheat Sources

A large portion of global HVP production relies on soy and wheat proteins, which are common allergens. Regulatory labeling requirements and shifting consumer preferences toward allergen-free foods may restrict adoption unless manufacturers diversify raw material sources.

Raw Material Price Volatility

Fluctuations in soybean, corn, and wheat prices significantly influence production costs. Climate variability and agricultural trade policies introduce supply uncertainties that can compress manufacturer margins.

What are the key opportunities in the hydrolysed vegetable protein industry?

Development of Allergen-Free and Novel Protein Sources

Pea, rice, chickpea, and fava bean proteins present strong opportunities for innovation. Companies investing in alternative protein hydrolysis technologies can capture premium market segments targeting gluten-free and soy-free consumers. These formulations are gaining traction in North America and Europe where food sensitivities influence purchasing behavior.

Expansion into Emerging Food Manufacturing Hubs

Rapid industrial food production growth across India, Vietnam, Indonesia, and Brazil creates opportunities for ingredient suppliers. Governments supporting domestic food processing industries through incentives and infrastructure development are accelerating ingredient demand.

Integration with Functional and Nutritional Foods

HVP is increasingly used in fortified foods, sports nutrition products, and high-protein snacks. Manufacturers are exploring low-sodium and bioactive peptide-enhanced formulations targeting health-conscious consumers, opening new high-margin application areas.

Product Type Insights

The global Hydrolyzed Vegetable Protein (HVP) market demonstrates strong diversification across product types; however, soy-based HVP continues to dominate the industry landscape, accounting for nearly 46% of the total market share in 2025. This leadership position is primarily attributed to the widespread availability of soybeans, well-established global supply chains, and the superior amino acid profile that closely mimics animal-derived protein flavor characteristics. Soy protein delivers strong umami enhancement capabilities, making it particularly suitable for savory formulations such as soups, processed meats, instant noodles, seasoning blends, and ready-to-eat meals. In addition, economies of scale in soybean processing significantly reduce production costs, enabling manufacturers to maintain competitive pricing while meeting large-volume industrial demand. The mature infrastructure supporting soybean cultivation and processing across major producing countries further reinforces the segment’s stability and scalability.Wheat-based HVP maintains a substantial market presence due to its functional properties derived from gluten proteins. Wheat proteins contribute desirable texture enhancement and flavor-binding characteristics, making them particularly valuable in bakery seasonings, processed snacks, and savory coatings. The segment benefits from strong demand within European markets where wheat processing infrastructure is highly developed. Additionally, wheat-derived HVP provides formulation flexibility for manufacturers seeking alternative protein sources that complement cereal-based food products. However, gluten-related allergen concerns and rising gluten-free dietary preferences moderately constrain growth compared to soy-based alternatives.Corn-based HVP plays a crucial role in snack flavor systems and processed food seasoning applications. Corn protein hydrolysates deliver mild flavor profiles that integrate effectively into flavored chips, extruded snacks, and instant meal seasonings. The widespread cultivation of corn across North America and Latin America ensures consistent raw material supply, supporting cost-effective manufacturing. This segment continues to expand alongside the global growth of convenience snack consumption, particularly among urban populations seeking affordable ready-to-eat products.The most dynamic growth trajectory is observed in pea-based HVP, which represents the fastest-growing product type segment. Rising consumer awareness regarding allergens, sustainability, and plant-based nutrition has accelerated demand for pea-derived proteins. Pea protein is naturally free from major allergens such as soy and gluten, making it attractive for clean-label and hypoallergenic product development. Manufacturers are investing heavily in research and development to enhance flavor performance and solubility characteristics of pea-based hydrolysates, enabling broader adoption in plant-based meat analogs and functional foods. Increasing investments in alternative protein innovation, combined with consumer preference for minimally processed plant ingredients, position pea-based HVP as a key future growth engine within the market.

Process Insights

Processing technology plays a decisive role in determining flavor quality, regulatory compliance, and commercial scalability within the HVP market. Enzymatic hydrolysis leads the global market with approximately 58% share in 2025, reflecting the industry’s transition toward natural processing methods and premium flavor development. This process utilizes specific enzymes to break down plant proteins into amino acids and peptides under controlled conditions, enabling precise flavor optimization while minimizing undesirable byproducts.The growing preference for enzymatic hydrolysis is strongly linked to clean-label trends and regulatory acceptance across developed markets. Food manufacturers increasingly seek ingredients that can be labeled as naturally derived, and enzymatic processing aligns with these expectations. The method also allows customization of flavor intensity, salt reduction strategies, and improved nutritional retention, making it highly suitable for health-conscious product reformulation. As global food companies prioritize transparency and ingredient traceability, enzymatic hydrolysis continues gaining adoption across premium product categories, including plant-based meat alternatives, functional foods, and organic packaged products.Technological innovation has further enhanced enzymatic efficiency, reducing processing time and improving yield optimization. Advanced enzyme engineering enables manufacturers to tailor peptide profiles that replicate meat-like umami characteristics, supporting the rapid expansion of alternative protein markets. Moreover, environmental sustainability advantages, including lower chemical usage and reduced waste generation, contribute to the increasing industry preference for enzymatic methods.In contrast, acid hydrolysis remains relevant primarily within large-scale industrial production environments where cost efficiency remains a dominant purchasing factor. Acid hydrolysis offers faster processing cycles and lower operational expenses, making it attractive in price-sensitive markets and bulk seasoning production. Emerging economies continue to rely on this method due to infrastructure familiarity and lower capital investment requirements. However, limitations related to flavor control, regulatory scrutiny, and consumer perception are gradually reducing adoption within premium and export-oriented food categories.Despite this gradual decline in high-value applications, acid hydrolysis maintains importance in commodity food manufacturing, ensuring continued coexistence of both processing methods within the global market structure. The long-term industry trajectory indicates increasing migration toward enzymatic systems as technological costs decline and regulatory frameworks increasingly favor naturally processed ingredients.

Form Insights

Based on physical form, the HVP market is dominated by powdered HVP, which accounts for nearly 62% of global demand. Powdered formulations provide significant logistical and functional advantages that align with industrial manufacturing requirements. The extended shelf life of powdered HVP reduces storage risks and transportation costs, enabling efficient global trade and inventory management. Its stability under varying environmental conditions makes it particularly suitable for export markets and large-scale food production facilities.Powdered HVP integrates seamlessly into dry seasoning blends, instant soups, snack coatings, spice mixes, and ready-to-cook meal kits. The form allows precise dosing during automated manufacturing processes, ensuring flavor consistency across high-volume production lines. Additionally, powdered ingredients support formulation flexibility, allowing manufacturers to customize flavor intensity and blend compatibility without affecting product texture or moisture balance.The dominance of powdered HVP is further strengthened by the rapid expansion of convenience foods and instant meal categories worldwide. Urbanization, increasing workforce participation, and evolving consumer lifestyles continue to drive demand for shelf-stable food solutions, indirectly supporting powdered ingredient adoption. Manufacturers also benefit from reduced microbial risks compared to liquid formats, improving food safety compliance.Liquid HVP, while representing a smaller share, is experiencing steady growth driven by applications requiring rapid solubility and uniform flavor dispersion. Sauces, marinades, gravies, and ready-to-use culinary bases increasingly utilize liquid HVP due to its ability to blend instantly without additional hydration steps. Foodservice operators and quick-service restaurant chains particularly favor liquid formats for operational efficiency and standardized taste delivery.Innovation in packaging technologies, including aseptic containers and concentrated liquid solutions, is further expanding the application scope of liquid HVP. As global demand for prepared sauces and ready-to-eat meal solutions rises, liquid formats are expected to witness sustained growth, complementing the continued dominance of powdered variants.

Application Insights

Food processing applications represent the largest application segment, accounting for approximately 68% of the global HVP market share. The leading driver behind this dominance is the increasing need for cost-effective flavor enhancement solutions capable of delivering consistent umami taste across mass-produced food products. HVP functions as both a flavor enhancer and protein-derived seasoning base, enabling manufacturers to improve taste profiles while optimizing ingredient costs.Processed soups, instant noodles, savory snacks, frozen meals, and seasoning blends rely extensively on HVP to achieve complex flavor depth without relying heavily on expensive meat extracts. The rapid growth of convenience food consumption across emerging economies significantly strengthens demand within this segment. As urban consumers prioritize affordability and quick meal preparation, processed food manufacturers increasingly incorporate HVP into formulations to maintain flavor intensity at scale.Another critical growth driver is sodium reduction reformulation initiatives undertaken by global food companies. HVP enhances perceived saltiness and umami richness, allowing manufacturers to lower sodium levels while preserving taste quality. This functionality aligns with public health initiatives encouraging reduced sodium consumption, thereby increasing adoption across health-focused product lines.The fastest-growing application area is the plant-based meat segment, fueled by rising global interest in alternative protein consumption. HVP provides essential savory flavor foundations that mimic meat taste characteristics, supporting the sensory acceptance of plant-based burgers, sausages, and meat substitutes. Continuous innovation in plant protein processing has enhanced the ability of HVP to deliver authentic meat-like flavor experiences, accelerating adoption among both traditional food manufacturers and emerging plant-based startups.Expansion of vegan and flexitarian dietary patterns, combined with investments in alternative protein technologies, ensures sustained growth of HVP usage in next-generation food products. As plant-based foods transition from niche offerings to mainstream consumption, HVP is expected to remain a foundational ingredient enabling flavor authenticity.

End-Use Insights

From an end-use perspective, industrial food manufacturers constitute the largest consumer group, contributing approximately 55% of total global demand. The primary driver behind this leadership is the need for scalable flavor standardization across large production volumes. Industrial manufacturers prioritize ingredients that deliver consistent sensory performance, predictable costs, and supply chain reliability—criteria strongly fulfilled by HVP.Global packaged food companies increasingly integrate HVP into product reformulation strategies aimed at improving taste while managing raw material price volatility. The ingredient’s multifunctionality as a flavor enhancer, protein derivative, and cost optimizer strengthens its value proposition within industrial operations. Additionally, automation in food manufacturing processes favors ingredients that are easy to store, measure, and incorporate into standardized recipes, further reinforcing adoption.Quick-service restaurants and foodservice operators represent a rapidly expanding end-use category. These businesses rely on HVP-based flavor systems to maintain uniform taste profiles across multiple locations while controlling ingredient expenses. As global fast-food chains expand into emerging markets, demand for standardized seasoning solutions continues to increase.Export-oriented seasoning manufacturers, particularly across Asia, are emerging as influential market participants. These companies produce customized flavor blends for international markets, leveraging HVP as a core component to deliver consistent umami profiles. Growth in global food trade and private-label manufacturing significantly contributes to rising demand within this segment.

| By Source Type | By Form | By Application | By Distribution Channel | By End Use Industry |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

Asia-Pacific

Asia-Pacific leads the global HVP market, accounting for approximately 41% of total market share in 2025, supported by a combination of large-scale manufacturing capacity, strong culinary demand for umami flavors, and rapidly expanding processed food industries. China serves as both the largest producer and consumer, benefiting from extensive soybean processing infrastructure and a mature seasoning export ecosystem. The country’s dominance is reinforced by strong domestic demand for instant noodles, sauces, and ready-to-eat meals, all of which rely heavily on flavor-enhancing ingredients.Japan and South Korea maintain stable demand driven by traditional culinary preferences emphasizing savory taste profiles. High consumption of soups, broths, and fermented sauces sustains consistent HVP usage. Technological innovation and premium food development further encourage adoption of enzymatically produced variants aligned with high-quality standards.India is emerging as one of the fastest-growing markets in the region due to rising urbanization, expanding middle-class populations, and government initiatives promoting food processing industries. Increasing consumption of packaged snacks, instant foods, and quick-service restaurant meals significantly drives demand for cost-effective flavor enhancers. Additionally, growth in domestic plant-based food startups and export-oriented seasoning production is strengthening regional market expansion.Regional growth is further supported by strong agricultural output, lower manufacturing costs, and expanding export networks supplying global food companies. The combination of supply-side advantages and increasing domestic consumption ensures Asia-Pacific’s continued leadership throughout the forecast period.

North America

North America accounts for nearly 24% of global market share, led primarily by the United States. The region’s growth is driven by rapid innovation in plant-based foods, increasing vegan product launches, and widespread clean-label reformulation initiatives. Food manufacturers are actively replacing artificial flavor enhancers with naturally derived alternatives such as enzymatically produced HVP, supporting sustained market demand.Consumer awareness regarding ingredient transparency and sustainability strongly influences purchasing decisions, encouraging adoption of non-GMO and allergen-friendly protein hydrolysates. Canada contributes significantly through advancements in functional food manufacturing and protein ingredient innovation, supported by investments in plant protein research and agricultural sustainability programs.The expansion of premium packaged foods, high-protein snacks, and health-oriented meal solutions further accelerates HVP adoption across North America. Strong research and development capabilities and collaboration between food technology companies and academic institutions continue to drive innovation in flavor science.

Europe

Europe represents approximately 22% of global demand, with Germany, France, and the United Kingdom leading regional consumption. The primary driver of market growth is the region’s strict food labeling regulations, which encourage manufacturers to adopt enzymatically produced and non-GMO HVP solutions that meet transparency requirements. European consumers increasingly prioritize sustainability, ethical sourcing, and plant-based nutrition, supporting strong adoption of vegetable-derived flavor ingredients.Government policies promoting reduced meat consumption and environmental sustainability are accelerating investment in alternative protein development. Food manufacturers across Europe are reformulating products to align with climate-conscious consumer preferences, indirectly boosting demand for plant-derived flavor enhancers. Additionally, the region’s advanced food processing infrastructure supports high-value product innovation, including organic and premium ready meals.

Middle East & Africa

The Middle East and Africa region is experiencing steady expansion driven by rising dependence on packaged food imports and rapid growth in the foodservice sector. Increasing urbanization and tourism development in countries such as Saudi Arabia and the United Arab Emirates are stimulating demand for processed foods and standardized flavor systems. HVP adoption is increasing as manufacturers seek cost-effective solutions capable of enhancing taste consistency across imported and locally produced products.South Africa serves as a regional manufacturing hub, supported by established food processing capabilities and growing retail distribution networks. Population growth, expanding modern retail infrastructure, and changing dietary habits are further contributing to long-term market development across the region.

Latin America

Latin America holds a smaller yet steadily expanding share of the global HVP market, led by Brazil and Mexico. Strong soybean production positions Brazil as a strategic manufacturing base for soy-derived HVP, providing raw material advantages and export opportunities. Increasing snack consumption, growth in seasoning exports, and expansion of processed food industries are key drivers supporting regional adoption.Mexico’s growing convenience food sector and rising demand for affordable flavor solutions further stimulate market expansion. Regional food manufacturers increasingly adopt HVP to enhance product flavor while maintaining competitive pricing in price-sensitive consumer markets. Improvements in agricultural productivity, trade agreements, and food manufacturing investments are expected to strengthen Latin America’s role within the global HVP supply chain over the coming years.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Hydrolysed Vegetable Protein Market

- Ajinomoto Co., Inc.

- Kerry Group plc

- Givaudan SA

- DSM-Firmenich

- Ingredion Incorporated

- Tate & Lyle PLC

- Archer Daniels Midland Company

- Cargill, Incorporated

- Roquette Frères

- Sensient Technologies Corporation

- Symrise AG

- Angel Yeast Co., Ltd.

- Fuji Oil Holdings Inc.

- International Flavors & Fragrances Inc.

- Bunge Limited