Hydrocolloids Market Size

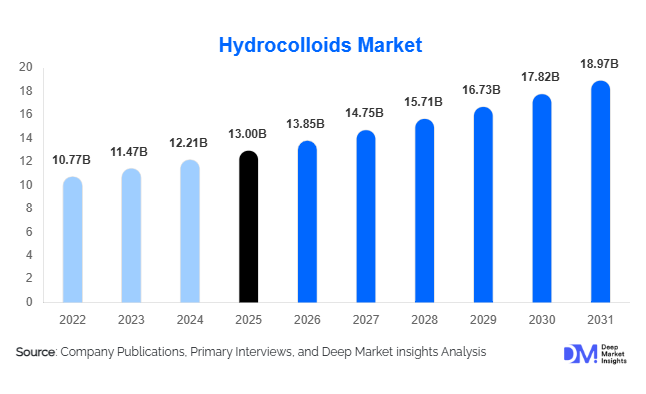

According to Deep Market Insights, the global hydrocolloids market size was valued at USD 13 billion in 2025 and is projected to grow from USD 13.85 billion in 2026 to reach USD 18.97 billion by 2031, expanding at a CAGR of 6.5% during the forecast period (2026–2031). The hydrocolloids market growth is primarily driven by increasing demand for natural and clean-label ingredients in food & beverages, rising applications in pharmaceuticals and advanced wound care, and the adoption of sustainable hydrocolloid-based solutions in personal care and industrial applications.

Key Market Insights

- Natural and plant-based hydrocolloids are gaining preference globally, as consumers demand clean-label, eco-friendly ingredients for processed foods, beverages, and personal care products.

- Advanced pharmaceutical and medical applications are expanding, with hydrocolloids used in controlled-release tablets, drug delivery systems, and hydrocolloid wound dressings.

- Asia-Pacific dominates hydrocolloids production and consumption, due to abundant raw materials, low-cost manufacturing, and strong demand from food processing industries.

- North America remains a major market for high-value hydrocolloid products, particularly in clean-label foods, pharmaceuticals, and personal care applications.

- Technological integration in extraction and processing, such as digital rheology modeling, AI-assisted formulation, and advanced purification, is enhancing product performance and operational efficiency.

- Emerging regions, including Latin America and parts of Africa, are witnessing rapid growth in processed food, healthcare, and personal care sectors, boosting regional hydrocolloid demand.

What are the latest trends in the hydrocolloids market?

Rising Clean-Label and Sustainable Ingredient Demand

Food and personal care manufacturers are increasingly reformulating products with hydrocolloids derived from natural sources such as seaweed (carrageenan, agar) and plants (pectin, guar gum). Sustainability and clean-label positioning have become key differentiators, as consumers demand transparent sourcing, environmentally responsible production, and chemical-free ingredients. Regulatory encouragement in Europe, North America, and Asia reinforces this trend, enabling faster adoption of plant- and seaweed-based hydrocolloids across global markets. The trend is particularly prominent in dairy, frozen desserts, beverages, sauces, and skincare formulations, where functional benefits like thickening, gelling, and emulsification are critical.

Medical and Pharmaceutical Applications Expanding

Hydrocolloids are increasingly used in advanced drug delivery systems, controlled-release tablets, and wound care dressings due to their biocompatibility, moisture-retention, and gel-forming properties. Rising chronic disease prevalence, aging populations, and healthcare infrastructure expansion are driving the adoption of hydrocolloid-based medical products. Novel hydrocolloid formulations are also being applied in tissue engineering and bioactive drug carriers, creating high-margin opportunities for specialty ingredient manufacturers.

What are the key drivers in the hydrocolloids market?

Growing Demand from the Food & Beverage Industry

The processed food and beverage sector is the largest consumer of hydrocolloids, using them for texture, stability, moisture retention, and shelf-life enhancement. Rising global consumption of sauces, dairy, bakery, confectionery, and beverages drives market growth. Clean-label trends and plant-based food adoption further accelerate demand for seaweed- and plant-derived hydrocolloids, which are increasingly preferred over synthetic alternatives.

Increased Use in Personal Care and Pharmaceuticals

Hydrocolloids are critical in creams, lotions, shampoos, and facial masks for viscosity control and sensory enhancement. In pharmaceuticals, they serve as excipients, wound dressings, and drug delivery agents. Growing personal care product innovation and healthcare expansion globally are strengthening hydrocolloid adoption across these high-value segments.

Preference for Natural and Sustainable Ingredients

Consumers and manufacturers are shifting away from synthetic stabilizers toward hydrocolloids sourced from plants and seaweed. Sustainability certifications, organic formulations, and environmental impact reduction are becoming key drivers for adoption in North America, Europe, and Asia-Pacific.

What are the restraints for the global market?

Raw Material Price Volatility

Hydrocolloid production relies on agricultural and seaweed resources, which are subject to seasonal fluctuations, climate variability, and supply chain disruptions. This volatility can affect product costs, pricing stability, and profitability, posing challenges for manufacturers in both commodity and specialty segments.

Regulatory and Technical Barriers

Stringent regulations on food additives, pharmaceuticals, and cosmetic ingredients can delay product launches and require substantial investment in compliance, certification, and testing. This slows market entry for new hydrocolloid types and advanced formulations, particularly in high-value applications such as medical or clean-label foods.

What are the key opportunities in the hydrocolloids market?

Clean-Label and Sustainable Product Innovation

Manufacturers can capitalize on the rising consumer demand for natural and eco-friendly ingredients by developing plant-based and seaweed-derived hydrocolloids with improved functionality. Innovations that enhance product stability, sensory appeal, and sustainability can create premium pricing opportunities across food, beverage, and personal care applications.

Expansion into Medical and Pharmaceutical Segments

Hydrocolloids’ biocompatibility and functional properties make them suitable for wound care, drug delivery, and advanced therapeutic formulations. Companies that invest in R&D and form strategic partnerships with healthcare providers can tap into high-margin specialty applications and rapidly growing medical markets.

Emerging Market Penetration

Rapid growth in Asia-Pacific and Latin America, driven by urbanization, rising middle-class incomes, and expanding food processing and personal care industries, presents significant market expansion opportunities. Early entrants establishing local production and distribution networks can leverage cost advantages and respond to rising regional demand.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 13 Billion |

| Market Size in 2026 | USD 13.85 Billion |

| Market Size in 2031 | USD 18.97 Billion |

| CAGR | 6.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Seaweed-derived hydrocolloids (carrageenan, agar, and alginate) dominate the global market, accounting for approximately 35% of total consumption in 2025. Their leadership is primarily driven by multifunctionality, cost efficiency, and wide regulatory acceptance across the food, pharmaceutical, and personal care industries. Carrageenan is extensively used in dairy and processed meat products for stabilization and water-binding, while agar finds strong application in confectionery and microbiological media. Alginate is widely utilized in wound dressings and dental impressions due to its gel-forming and biocompatible properties. The growth of processed food consumption, particularly dairy alternatives and ready-to-eat meals, remains the key driver for this segment. Additionally, the abundance of seaweed raw materials in the Asia-Pacific strengthens supply security and cost competitiveness, reinforcing segment dominance.

Plant-based hydrocolloids such as pectin, guar gum, and gum arabic are witnessing accelerated growth due to rising clean-label and vegan product demand. Pectin is heavily used in fruit-based beverages, jams, and low-sugar products, benefiting from the expansion of functional and reduced-calorie foods. Guar gum continues to grow across bakery and oilfield applications due to its strong thickening efficiency and affordability. Increasing plant-based food innovation globally acts as the primary driver for this category. Animal-derived hydrocolloids, particularly gelatin, hold a comparatively smaller but stable market share. Their niche relevance persists in confectionery (gummies, marshmallows), capsule manufacturing, and certain pharmaceutical applications. However, growth remains moderate due to rising plant-based substitution trends and dietary restrictions in key markets.

Application Insights

Food & beverage applications remain the dominant segment, accounting for approximately 60–65% of the global hydrocolloids market in 2025. The primary driver for this segment is the expanding global processed food industry, including dairy products, plant-based beverages, sauces, dressings, frozen desserts, and bakery goods. Hydrocolloids enhance texture, stability, viscosity, and shelf life, making them indispensable functional ingredients. The rapid rise of plant-based dairy alternatives and clean-label reformulations further strengthens demand for carrageenan, pectin, xanthan gum, and guar gum. Urbanization, convenience food demand, and premiumization trends continue to drive growth in this segment.

Pharmaceutical applications are among the fastest-growing categories, supported by increasing demand for controlled-release tablets, drug encapsulation systems, and hydrocolloid wound dressings. Aging populations, rising chronic diseases, and expanding healthcare infrastructure globally act as major drivers. Hydrocolloids’ biocompatibility and moisture-retention properties make them highly suitable for advanced therapeutic applications, particularly in North America and Europe. Personal care and cosmetics represent a steadily expanding segment, driven by consumer preference for natural, sulfate-free, and eco-friendly formulations. Hydrocolloids are widely used in creams, lotions, shampoos, facial masks, and serums for viscosity control and sensory enhancement.

Distribution Channel Insights

Direct sales to food, pharmaceutical, and personal care manufacturers remain the dominant distribution channel, as large-scale buyers prefer long-term contracts, technical support, and customized formulations. This channel ensures stable procurement volumes and stronger supplier-customer integration. Ingredient distributors and contract manufacturers play a crucial supporting role, particularly for small and medium-sized enterprises that require flexible purchasing volumes and technical advisory services. Regional distributors are especially important in emerging markets where localized warehousing and regulatory expertise are necessary.

Digital B2B platforms and integrated supply chain systems are increasingly transforming hydrocolloid procurement. Manufacturers are investing in traceability systems, blockchain-based quality verification, and AI-driven inventory forecasting to improve supply chain transparency. Companies that offer application labs, digital formulation tools, and technical consultation services are strengthening customer retention and differentiation in a competitive marketplace.

Explore more data points, trends and opportunities Download Free Sample Report

Hydrocolloids Market Segmentations

By Product Type

- Seaweed-Derived Hydrocolloids

- Plant-Based Hydrocolloids

- Microbial/Fermentation-Derived

- Animal-Derived Hydrocolloids

- Modified & Specialty Hydrocolloids

By Application

- Food & Beverage

- Pharmaceuticals

- Personal Care & Cosmetics

- Industrial Applications

By Function

- Thickening Agents

- Gelling Agents

- Stabilizing & Emulsifying Agents

- Water Retention & Film Forming

By Distribution Channel

- Direct Sales to Manufacturers

- Ingredient Distributors

- Online B2B Platforms

- Contract Manufacturing Supply Agreements

Regional Insights

Asia-Pacific

Asia-Pacific is the largest regional market, accounting for approximately 40–42% of global demand in 2025. The region’s dominance is driven by abundant raw material availability (particularly seaweed in China and Indonesia), cost-competitive manufacturing, and large-scale food processing industries. China leads both production and consumption due to its expansive dairy, beverage, and pharmaceutical sectors. India’s growing packaged food industry and expanding middle class are key demand drivers. Indonesia plays a strategic role as a major seaweed exporter, strengthening global supply chains. Rapid urbanization, rising disposable incomes, export-oriented processed food industries, and supportive government policies for food manufacturing collectively drive strong regional growth.

North America

North America holds approximately 25–28% of the global hydrocolloids market. The United States dominates regional demand due to strong clean-label reformulation trends, high processed food consumption, and advanced pharmaceutical R&D activities. The region’s strict food safety standards and preference for premium, specialty ingredients drive higher-value hydrocolloid adoption. Growth drivers include rising plant-based food consumption, expansion of nutraceuticals, and increased demand for advanced wound care products. Canada contributes through stable food processing growth and healthcare expansion.

Europe

Europe accounts for approximately 20–22% of global demand, led by Germany, France, and the United Kingdom. The region’s strong regulatory emphasis on natural and sustainable ingredients drives hydrocolloid adoption in clean-label foods and eco-friendly cosmetics. Vegan product growth, sugar reduction initiatives, and sustainability-focused reformulations act as major drivers. Additionally, Europe’s mature pharmaceutical sector supports steady demand for excipients and drug delivery applications.

Latin America

Latin America represents approximately 5–6% of the global market, with Brazil and Argentina as key contributors. Growth is driven by expanding processed food production, dairy exports, and increasing domestic consumption of packaged foods. Economic modernization and retail expansion are supporting higher demand for functional food ingredients. Export-oriented meat and dairy industries further stimulate hydrocolloid usage for texture and water retention enhancement.

Middle East & Africa

The Middle East & Africa account for approximately 8–10% of global demand. South Africa leads sub-Saharan demand due to food processing and pharmaceutical development, while Saudi Arabia and the UAE are key growth markets driven by rising processed food imports, personal care consumption, and healthcare investments. Government initiatives to enhance food security and local manufacturing capabilities are stimulating ingredient demand. Increasing urbanization and retail development are further supporting hydrocolloid consumption across the region.

Key Players in the Hydrocolloids Market

- Cargill, Incorporated

- Ingredion Incorporated

- DuPont de Nemours, Inc.

- Tate & Lyle PLC

- BASF SE

- Ashland Global Holdings, Inc.

- Kerry Group plc

- CP Kelco US Inc.

- Archer Daniels Midland Company

- Palsgaard A/S

- Nexira

- Darling Ingredients, Inc.

- Glanbia Nutritionals

- Fuerst Day Lawson

- Koninklijke DSM N.V.