Hot Sauce Market Size

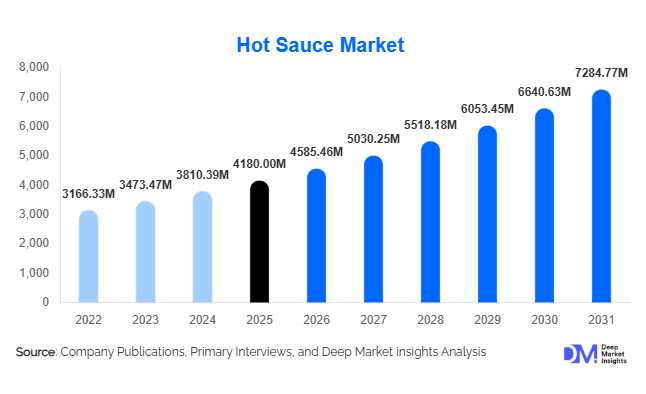

According to Deep Market Insights, the global hot sauce market size was valued at USD 4,180 million in 2025 and is projected to grow from USD 4,585.46 million in 2026 to reach USD 7,284.77 million by 2031, expanding at a CAGR of 9.7% during the forecast period (2026–2031). The hot sauce market growth is primarily driven by rising global demand for spicy and ethnic cuisines, increasing adoption of premium and clean-label condiments, and expanding consumption across quick-service restaurants and packaged food applications. Growing consumer experimentation with flavors, alongside the globalization of food culture and strong retail expansion, continues to position hot sauce as one of the fastest-growing condiment categories worldwide.

Key Market Insights

- Global consumers are increasingly embracing spicy flavor profiles, driven by exposure to international cuisines and food innovation trends.

- Premium and craft hot sauces are gaining strong traction, supported by demand for artisanal, fermented, and exotic pepper-based formulations.

- North America dominates the global market, supported by strong household penetration and foodservice consumption.

- Asia-Pacific is the fastest-growing regional market, fueled by urbanization, rising disposable income, and expansion of international restaurant chains.

- E-commerce and direct-to-consumer sales channels are enabling small and niche brands to scale globally.

- Clean-label and organic formulations are reshaping product innovation and premium pricing strategies.

What are the latest trends in the hot sauce market?

Premiumization and Craft Flavor Innovation

The hot sauce industry is witnessing a strong shift toward premiumization, with consumers increasingly seeking differentiated flavor experiences beyond traditional pepper sauces. Craft manufacturers are experimenting with fermented recipes, fruit-infused sauces, smoked peppers, and region-specific spice blends. Limited-edition releases and chef collaborations are becoming common marketing strategies to build brand loyalty. Premium sauces often command significantly higher price points, improving profitability while appealing to consumers interested in gourmet cooking and culinary experimentation. The rise of small-batch production and locally sourced peppers is also strengthening brand authenticity and sustainability positioning.

Technology-Driven Product Discovery and Digital Sales

Digital commerce platforms are transforming how consumers discover and purchase hot sauces. Social media trends, food influencers, and viral spicy food challenges are accelerating brand visibility globally. Manufacturers increasingly leverage data analytics to track consumer flavor preferences and optimize product launches. Subscription models and direct-to-consumer platforms allow companies to test experimental flavors while building recurring revenue streams. Advanced manufacturing technologies such as automated fermentation monitoring and quality analytics are improving consistency and scalability, enabling brands to expand internationally while maintaining flavor integrity.

What are the key drivers in the hot sauce market?

Globalization of Culinary Preferences

The widespread adoption of international cuisines has significantly increased hot sauce consumption worldwide. Mexican, Korean, Thai, and African flavors are becoming mainstream across restaurants and home kitchens. Increased travel exposure, digital food content, and multicultural urban populations have normalized spicy foods across traditionally mild-flavor markets. As consumers seek authentic dining experiences at home, hot sauce has emerged as an essential condiment supporting culinary exploration and personalization.

Expansion of Quick-Service Restaurants and Food Delivery

Quick-service restaurant chains are increasingly incorporating spicy menu offerings to attract younger consumers. Chicken chains, burger brands, and street-food franchises frequently introduce spicy variants, boosting bulk condiment demand. Growth in online food delivery and cloud kitchens has further accelerated consumption, as customizable sauces enhance meal differentiation. Proprietary sauces developed by restaurants are also strengthening long-term procurement partnerships with manufacturers.

What are the restraints for the global market?

Raw Material Price Volatility

The hot sauce industry depends heavily on chili pepper cultivation, which is vulnerable to climate variability, droughts, and crop diseases. Fluctuations in agricultural yields directly impact production costs and profit margins. Rising packaging and logistics expenses further add pricing pressure, particularly for smaller producers with limited supply chain bargaining power.

Market Fragmentation and Shelf Competition

Low entry barriers have resulted in thousands of regional and craft brands competing globally. While innovation is high, intense competition for retail shelf space increases marketing expenditures and limits scalability for emerging companies. Established multinational brands maintain advantages through distribution networks and promotional capabilities, creating competitive challenges for smaller entrants.

What are the key opportunities in the hot sauce industry?

Health-Oriented and Functional Hot Sauces

Growing health awareness is creating opportunities for functional hot sauces featuring organic ingredients, low sodium formulations, probiotic fermentation, and sugar-free recipes. Consumers increasingly associate chili peppers with metabolism benefits and natural food consumption. Brands investing in clean-label certifications and wellness positioning are expected to capture premium consumer segments and expand into health-focused retail channels.

Emerging Market Expansion

Asia-Pacific and Middle Eastern markets present significant growth opportunities as Western-style condiments gain popularity alongside local cuisines. Rising middle-class incomes, rapid urbanization, and the expansion of international restaurant franchises are accelerating adoption. Localization strategies that incorporate regional spices and flavor profiles are helping manufacturers penetrate new markets while maintaining cultural relevance.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4180 Million |

| Market Size in 2026 | USD 4585.46 Million |

| Market Size in 2031 | USD 7284.77 Million |

| CAGR | 9.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Pepper-based hot sauces continue to dominate the global hot sauce market, accounting for nearly 46% of total revenue share, primarily due to their widespread culinary adaptability, strong consumer familiarity, and compatibility with both traditional and modern food formats. Cayenne and jalapeño-based sauces remain leading products as they offer a balanced heat profile that appeals to mass-market consumers while maintaining authentic flavor characteristics. The leading segment growth is strongly supported by increasing global consumption of spicy foods, expanding fast-food menus incorporating hot condiments, and rising preference for versatile table sauces that can be used across multiple cuisines. In addition, manufacturers are investing in new pepper blends, regional chili varieties, and scalable production techniques to maintain consistent taste profiles while expanding product portfolios.Fermented hot sauces are witnessing accelerated adoption within premium product categories, driven by growing consumer awareness surrounding gut health, natural fermentation processes, and artisanal food preparation methods. These products appeal particularly to urban consumers seeking authentic flavors and perceived functional benefits. Fruit-based and specialty gourmet sauces represent rapidly emerging niches supported by culinary experimentation, fusion cuisine trends, and premium retail positioning. Ingredients such as mango, pineapple, and berry infusions are gaining popularity as consumers increasingly seek complex flavor experiences combining sweetness, acidity, and heat. Continuous innovation across Scoville heat levels, organic formulations, and clean-label ingredient sourcing is expanding category diversity while reinforcing long-term demand growth globally.

Application Insights

Household consumption represents the largest application segment, supported by sustained growth in home cooking trends, digital recipe consumption, and rising experimentation with international cuisines. The leading segment driver is the increasing incorporation of hot sauces into everyday meals, snacks, and convenience foods, transforming hot sauce from a niche condiment into a staple kitchen ingredient. Social media food culture, cooking shows, and global culinary exposure are encouraging consumers to experiment with heat-based flavor enhancement across breakfast, lunch, and dinner applications.Foodservice applications are expanding at the fastest pace as restaurants, casual dining establishments, and quick-service restaurant chains increasingly utilize spicy menu offerings to differentiate brand positioning and attract younger consumer demographics. Limited-time spicy menu launches and customizable heat levels are driving higher condiment usage per order. Processed food manufacturers are also integrating hot sauce flavors into packaged snacks, frozen meals, sauces, marinades, and ready-to-eat products, creating diversified demand streams beyond traditional table use. Additionally, street food vendors and cloud kitchens are emerging as influential application channels, particularly in emerging economies where affordable flavor enhancement and strong taste differentiation play a critical role in consumer purchasing decisions.

Distribution Channel Insights

Supermarkets and hypermarkets dominate global distribution channels, accounting for approximately 41% of total sales due to strong shelf visibility, brand comparison opportunities, and impulse purchasing behavior. The leading segment driver is the ability of large-format retail outlets to offer wide product assortments ranging from mass-market brands to premium and imported sauces, enabling consumers to explore diverse heat profiles and flavor innovations within a single shopping environment. Promotional pricing strategies and in-store sampling further contribute to sustained channel dominance.Online retail represents the fastest-growing distribution channel as digital commerce platforms enable niche, craft, and premium brands to access global audiences without traditional retail limitations. Consumer reliance on e-commerce for specialty food purchases, subscription-based condiment delivery, and direct brand engagement is accelerating channel expansion. Specialty gourmet stores continue to play a critical role in premium product discovery, particularly for small-batch and artisanal sauces targeting food enthusiasts. Meanwhile, foodservice distributors remain essential for bulk supply to restaurants, hotels, and catering businesses, ensuring consistent demand volumes. Direct-to-consumer sales models are increasingly adopted by emerging brands seeking higher profit margins, stronger brand storytelling, and deeper consumer relationships through digital engagement strategies.

End-Use Insights

Household retail consumption leads the global hot sauce market with around 52% share, supported by rising incorporation of spicy condiments into daily meal preparation and snacking habits. The leading segment driver is the growing normalization of spicy flavor preferences across diverse demographics, supported by globalization of food culture and increased accessibility of international cuisines. Consumers are increasingly purchasing multiple hot sauce variants simultaneously, reflecting experimentation with flavor intensity and cuisine pairing.Restaurants and quick-service establishments represent the fastest-growing end-use segment, driven by menu innovation, expansion of global fast-food chains, and increasing consumer demand for bold flavor experiences. Spicy flavor customization has become a key competitive strategy among restaurant operators, leading to higher condiment consumption volumes. Processed food manufacturers are emerging as significant institutional buyers as spicy flavors gain traction across packaged foods, seasoning blends, and ready-to-cook meal kits. Export-driven demand continues to strengthen major production hubs such as the United States, Mexico, Thailand, and China, where large-scale manufacturing capabilities support international trade and private-label production for global retailers.

Explore more data points, trends and opportunities Download Free Sample Report

Hot Sauce Market Segmentations

By Product Type

- Pepper-Based Hot Sauce

- Fermented Hot Sauce

- Fruit-Infused Hot Sauce

- Specialty & Gourmet Hot Sauce

- Extra-Hot & Specialty Chili Extract Sauces

By Application

- Household Consumption

- Foodservice & Quick-Service Restaurants

- Processed & Packaged Food Manufacturing

- Street Food & Cloud Kitchens

- Marinades, Cooking Ingredients & Meal Kits

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail & Direct-to-Consumer

- Specialty & Gourmet Stores

- Foodservice Distributors & Wholesale Channels

By End-Use Industry

- Retail & Household Sector

- Restaurants & Hospitality Industry

- Processed Food Manufacturers

- Catering & Institutional Buyers

Regional Insights

North America

North America accounts for approximately 34% of the global hot sauce market share, led by the United States where hot sauce consumption is deeply embedded in culinary culture and everyday dining habits. Regional growth is driven by strong penetration of quick-service restaurants, widespread household adoption of condiments, and continuous product innovation from established and craft brands. The growing influence of Hispanic and Latin American cuisines has significantly expanded consumer acceptance of diverse chili-based flavors. Additionally, premiumization trends, rising demand for organic and clean-label products, and strong retail infrastructure support sustained market expansion. Canada contributes steady growth through multicultural population dynamics, increasing experimentation with global cuisines, and rising demand for gourmet and specialty condiments.

Europe

Europe holds nearly 22% of global market share, supported by increasing consumer exposure to ethnic cuisines and a growing culture of gourmet home cooking. Regional growth is driven by rising demand for premium, artisanal, and small-batch hot sauces, particularly in countries such as the United Kingdom, Germany, and France. Expanding international restaurant chains and food delivery platforms are accelerating consumer familiarity with spicy flavor profiles. Additionally, stringent food quality standards and strong consumer preference for clean-label, organic, and sustainably sourced ingredients are shaping innovation strategies. Retailers are expanding international condiment sections, further improving product accessibility and encouraging market adoption across mainstream consumers.

Asia-Pacific

Asia-Pacific represents approximately 27% of the global market and remains the fastest-growing regional segment. Growth is primarily driven by rapid urbanization, increasing disposable incomes, and expansion of modern retail and foodservice infrastructure across China, India, South Korea, and Thailand. Rising youth populations and exposure to Western dining formats are accelerating demand for bottled hot sauces alongside traditional chili condiments. Localization strategies, including adaptation of heat levels and flavor combinations suited to regional taste preferences, are enhancing product acceptance. The rapid growth of food delivery platforms, cloud kitchens, and convenience food consumption further strengthens regional demand, while domestic chili production supports cost-effective manufacturing expansion.

Latin America

Latin America contributes around 11% of global market share, led by Mexico and Brazil. Regional growth is strongly supported by deep cultural integration of chili peppers within traditional cuisines and strong domestic consumption patterns. Mexico serves as both a major consumption center and export hub due to extensive chili pepper cultivation, established processing infrastructure, and strong global brand recognition. Increasing exports to North America and Europe, supported by trade agreements and growing international demand for authentic Mexican flavors, are further strengthening regional industry development. Rising urbanization and expansion of modern retail formats are also improving product availability across emerging urban populations.

Middle East & Africa

The Middle East & Africa region accounts for approximately 6% of global market share and is emerging as a high-potential growth region. Regional expansion is driven by increasing urbanization, rising disposable incomes, and rapid growth of international dining chains across markets such as the UAE and Saudi Arabia. Tourism expansion and diverse expatriate populations are introducing new flavor preferences, accelerating adoption of global condiment categories including hot sauces. Premium retail development, expanding supermarket chains, and growing demand for convenience foods are further supporting market penetration. Additionally, younger consumer demographics and increasing exposure to global food trends through digital media are expected to sustain long-term demand growth across the region.

Key Players in the Hot Sauce Market

- McIlhenny Company

- Huy Fong Foods Inc.

- McCormick & Company Inc.

- Kraft Heinz Company

- Unilever PLC

- Conagra Brands Inc.

- Campbell Soup Company

- Hormel Foods Corporation

- Cholula Food Company

- T. Marzetti Company

- Baumer Foods Inc.

- GraceKennedy Group

- Lee Kum Kee Company Limited

- Kikkoman Corporation

- Samyang Foods Co., Ltd.