Hot Pot Condiment Market Size

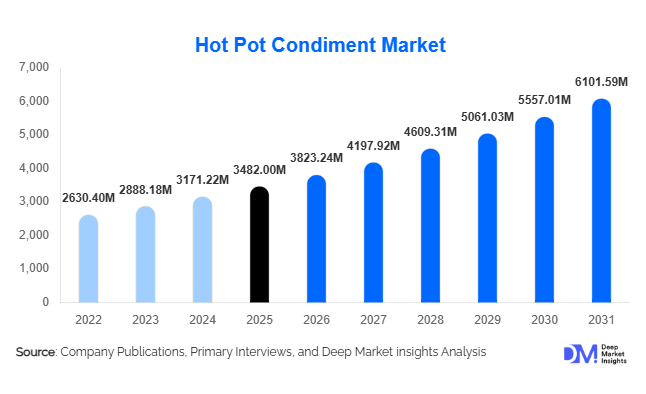

According to Deep Market Insights, the global hot pot condiment market size was valued at USD 3,482 million in 2025 and is projected to grow from USD 3,823.24 million in 2026 to reach USD 6,101.59 million by 2031, expanding at a CAGR of 9.8% during the forecast period (2026–2031). The market growth is driven by the globalization of Asian cuisines, rapid expansion of hot pot restaurant chains, increasing consumer preference for ready-to-use cooking sauces, and rising demand for authentic regional flavors across retail and foodservice channels.

Key Market Insights

- Asian cuisine globalization is accelerating adoption of hot pot condiments beyond China into North America, Europe, and Southeast Asia.

- Retail-ready dipping sauces and soup bases are gaining popularity among home cooks seeking restaurant-style experiences.

- Asia-Pacific dominates consumption, supported by strong cultural integration of hot pot dining traditions.

- E-commerce and cross-border food retail are enabling international brands to expand rapidly into new markets.

- Premiumization trends are driving demand for organic, low-sodium, and specialty-flavor condiments.

- Foodservice chains remain key volume drivers, particularly through standardized condiment procurement.

What are the latest trends in the hot pot condiment market?

Premium and Authentic Regional Flavor Expansion

Consumers are increasingly seeking authentic regional hot pot experiences such as Sichuan mala, Chongqing spicy broth, and Cantonese herbal flavors. Manufacturers are responding by launching geographically inspired condiment lines that replicate restaurant-grade taste profiles. Premium ingredients including fermented bean paste, sesame blends, specialty chili oils, and mushroom-based umami enhancers are becoming mainstream. This trend is particularly visible in export markets where authenticity is a primary purchase driver. Packaging innovation emphasizing provenance, ingredient transparency, and culinary storytelling is strengthening brand differentiation.

Rise of Home Hot Pot Consumption

Post-pandemic cooking habits permanently increased at-home dining experimentation. Consumers now purchase ready-to-use soup bases, dipping sauces, and customizable condiment kits to recreate social dining experiences at home. Retail chains and online grocery platforms are expanding dedicated Asian cooking sections, boosting accessibility. Single-serve sachets and family-sized condiment packs are gaining traction, particularly among urban households with limited preparation time. This shift is transforming hot pot condiments from niche ethnic products into mainstream cooking essentials.

What are the key drivers in the hot pot condiment market?

Expansion of Hot Pot Restaurant Chains

Global expansion of organized hot pot chains has significantly increased standardized condiment demand. Large restaurant operators require consistent flavor formulations and bulk procurement contracts, driving industrial-scale production. Franchise expansion across Southeast Asia, North America, and the Middle East has strengthened supply chain investments and brand visibility.

Growth of Packaged Sauce Industry

The broader cooking sauce category is experiencing strong growth due to convenience-driven lifestyles. Hot pot condiments benefit directly from this trend as consumers shift toward ready-made flavor solutions. Urbanization and dual-income households favor quick meal preparation, increasing retail penetration of soup bases and dipping sauces.

Rising Cross-Cultural Food Adoption

Younger consumers worldwide actively explore international cuisines through social media and food content platforms. Korean BBQ, Japanese ramen, and Chinese hot pot culture have gained global popularity, creating sustained demand for complementary condiments. Influencer-led recipes and cooking tutorials further accelerate trial and repeat purchases.

What are the restraints for the global market?

Flavor Localization Challenges

Highly spicy or fermented flavor profiles may limit acceptance in Western markets where taste preferences differ. Manufacturers must invest in localized product variants, increasing R&D costs and slowing expansion speed.

Raw Material Price Volatility

Key ingredients such as chili peppers, soybean derivatives, sesame seeds, and edible oils are subject to agricultural price fluctuations. Rising input costs can compress margins, particularly for export-oriented manufacturers competing on price.

What are the key opportunities in the hot pot condiment industry?

Retail Expansion in Emerging Markets

Countries such as India, Indonesia, Brazil, and the UAE are witnessing rising demand for Asian cuisines driven by urban youth populations and international restaurant expansion. Retail localization strategies and partnerships with modern trade retailers present significant growth opportunities for manufacturers entering new markets.

Health-Oriented Product Innovation

Low-sodium, preservative-free, vegan, and clean-label condiments represent a major opportunity. Consumers increasingly scrutinize ingredient lists, encouraging brands to develop healthier formulations without compromising flavor intensity. Functional ingredients such as mushroom extracts and plant-based umami enhancers are gaining traction.

Digital Commerce and Direct-to-Consumer Channels

E-commerce platforms enable smaller brands to reach global audiences without extensive distribution infrastructure. Subscription meal kits and bundled hot pot ingredient packages are emerging as new business models, improving recurring revenue potential and brand loyalty.

Product Type Insights

Hot pot soup bases dominate the global hot pot condiment market, accounting for approximately 46% of total revenue in 2025, primarily due to their indispensable role as the foundation of the hot pot dining experience. Unlike dipping sauces or dry seasonings, soup bases represent the core flavor carrier of the meal, driving higher consumption volumes per serving and repeat purchasing frequency across both foodservice and household channels. The strong dominance of soup bases is further reinforced by standardized procurement practices among restaurant chains, where consistency in flavor profiles is critical for brand identity and customer retention. Among product categories, spicy mala soup bases continue to lead globally, supported by widespread popularity of Sichuan-style cuisine and increasing international exposure through restaurant franchising and social media-driven food trends. Export demand for authentic Chinese hot pot flavors has accelerated the penetration of packaged soup bases into overseas retail markets, particularly through specialty Asian grocery stores and cross-border e-commerce platforms.Dipping sauces represent a rapidly expanding segment as consumer preferences increasingly shift toward personalization and interactive dining experiences. Modern consumers favor customizable flavor combinations, encouraging manufacturers to launch modular sauce kits and premium formulations incorporating sesame, garlic, mushroom, and fermented ingredients. Meanwhile, dry seasoning mixes are gaining traction within retail distribution due to their extended shelf life, lower transportation costs, and suitability for emerging markets where cold-chain logistics remain limited. These products appeal strongly to value-conscious households and first-time hot pot consumers seeking convenient entry-level solutions, thereby widening the consumer base beyond traditional markets.

Flavor Type Insights

Spicy flavor variants hold the largest share, representing approximately 41% of the global market in 2025, reflecting the international dominance of bold and heat-forward culinary profiles associated with Sichuan hot pot traditions. The growing consumer perception that authentic hot pot experiences should deliver intense sensory stimulation continues to reinforce demand for chili-based and mala-flavored products. Globalization of Asian cuisine, combined with increasing consumer willingness to experiment with stronger flavors, has positioned spicy variants as the leading growth driver across both mature and emerging markets. Manufacturers are also innovating with layered spice complexity, combining numbing peppercorn notes with umami-rich broths to enhance differentiation.At the same time, mild, herbal, and non-spicy flavor variants are witnessing accelerated adoption, particularly among health-conscious consumers and international markets where spice tolerance varies. Herbal broths emphasizing natural ingredients, reduced sodium formulations, and functional components such as mushrooms and medicinal herbs are gaining popularity as wellness-oriented eating trends influence purchasing behavior. This diversification of flavor portfolios enables brands to expand demographic reach, attracting families, older consumers, and first-time adopters unfamiliar with traditional spicy profiles.

Packaging Type Insights

Pouch packaging leads the market with nearly 52% share, driven by strong advantages in manufacturing efficiency, logistics optimization, and retail convenience. Lightweight flexible packaging significantly reduces transportation costs and supports scalable distribution across international markets, making it particularly attractive for exporters and online retailers. The format also aligns with consumer demand for portion-controlled products suitable for both single-use household cooking and foodservice preparation. Easy storage, resealability, and improved product shelf stability further reinforce pouch adoption.Innovation within packaging design is emerging as a competitive differentiator. Multi-compartment packaging solutions that separate oils, spices, and broths allow consumers to customize flavor intensity while preserving ingredient freshness. Sustainable packaging initiatives are also gaining momentum as manufacturers experiment with recyclable materials and reduced plastic usage to meet evolving environmental regulations and consumer expectations, particularly in Europe and North America.

Distribution Channel Insights

Offline retail channels account for approximately 58% of total sales, supported by extensive supermarket and hypermarket penetration across Asia-Pacific markets where consumers traditionally purchase cooking ingredients through physical stores. Strong in-store visibility, promotional bundling, and impulse purchasing behavior continue to sustain offline dominance. Retail chains benefit from high product turnover rates and established supplier relationships, especially in regions with mature hot pot consumption cultures.However, online distribution channels represent the fastest-growing segment, fueled by rapid expansion of e-commerce ecosystems and cross-border retail platforms. Digital marketplaces enable international consumers to access authentic brands previously limited to regional availability, accelerating globalization of hot pot cuisine. Subscription meal kits, influencer-driven marketing, and direct-to-consumer strategies are further enhancing online adoption. The integration of cold-chain logistics and improved last-mile delivery infrastructure is expected to significantly increase online market share over the forecast period.

End-Use Insights

Foodservice remains the dominant end-use segment, accounting for approximately 62% market share in 2025, largely driven by the rapid expansion of hot pot restaurant chains and standardized condiment usage across commercial kitchens. Restaurants rely heavily on consistent flavor formulations, resulting in bulk purchasing agreements that generate stable demand for manufacturers. The experiential and social nature of hot pot dining continues to attract younger consumers and group dining occasions, further strengthening foodservice consumption volumes.Household consumption is emerging as the fastest-growing segment, supported by rising popularity of home dining experiences, ready-to-cook meal kits, and convenient packaged solutions. Consumers increasingly replicate restaurant-style meals at home, particularly following behavioral shifts toward home cooking and shared family dining occasions. Product innovations emphasizing simplicity, pre-measured ingredients, and quick preparation are accelerating adoption among urban households worldwide.

End-Use Industry Analysis

The foodservice industry continues to serve as the primary demand generator for hot pot condiments, with hot pot restaurants, casual dining establishments, and buffet-style concepts driving large-scale procurement volumes. Global hot pot restaurant revenue is expanding at an annual rate exceeding 11%, directly influencing ingredient sourcing patterns and encouraging manufacturers to scale production capacity. Franchise expansion across international markets is further standardizing condiment usage, strengthening long-term supplier relationships.Household consumption represents a transformative growth opportunity as retail expansion and meal-kit culture reshape consumer behavior. Increasing availability of packaged hot pot solutions in supermarkets and online platforms enables consumers to recreate authentic dining experiences without restaurant visits. Additionally, condiment applications are expanding beyond traditional hot pot usage into ready meals, instant noodles, frozen meal kits, and fusion cuisine formats. This cross-category integration is broadening revenue streams and positioning hot pot condiments as versatile culinary ingredients rather than niche specialty products.

| By Product Type | By Flavor Profile | By Distribution Channel | By End Use |

|---|---|---|---|

|

|

|

|

Regional Insights

Asia-Pacific

Asia-Pacific dominates the global market with approximately 68% share in 2025, supported by deeply embedded cultural consumption patterns and a highly developed hot pot restaurant ecosystem. China alone contributes more than 55% of global consumption due to its long-standing culinary traditions, extensive restaurant networks, and strong domestic condiment manufacturers. Regional growth is driven by rapid urbanization, rising disposable incomes, and increasing frequency of social dining occasions. Japan and South Korea contribute steady expansion through premiumization trends, where consumers favor high-quality packaged broths and specialty flavors. Southeast Asian markets including Thailand, Vietnam, and Indonesia are experiencing double-digit growth fueled by expanding middle-class populations, shopping mall dining culture, and increasing exposure to regional cuisines through tourism and digital media. India is emerging as a high-growth opportunity as younger consumers show rising interest in East Asian flavors, supported by restaurant expansion, online food content influence, and growing availability of imported products in metropolitan retail channels.

North America

North America accounts for nearly 11% market share, led by the United States where multicultural demographics and strong penetration of Asian cuisine continue to drive adoption. Regional growth is supported by increasing consumer interest in experiential dining, expansion of hot pot restaurant chains in urban centers, and wider distribution through mainstream supermarket retailers. Immigration trends and cultural diversification are introducing authentic culinary practices to broader audiences, while e-commerce platforms allow consumers to access imported brands easily. Canada demonstrates similar momentum, with demand driven by urban population diversity, premium grocery retail expansion, and growing acceptance of international cooking formats within households.

Europe

Europe represents approximately 9% of global demand, with significant growth observed in the United Kingdom, Germany, and France. Market expansion is driven by rising popularity of experiential dining concepts, increased participation in Asian food festivals, and growing consumer curiosity toward global cuisines. Retailers are accelerating adoption by launching private-label Asian sauce ranges, improving affordability and accessibility for mainstream consumers. Regulatory emphasis on clean-label ingredients and sustainable packaging is encouraging manufacturers to reformulate products to align with European consumer expectations, thereby supporting long-term market penetration.

Middle East & Africa

The Middle East and Africa region is witnessing gradual but steady expansion, led by the UAE and Saudi Arabia as primary growth hubs. Increasing expatriate populations, strong tourism inflows, and investments in premium dining infrastructure are driving demand for imported hot pot condiments. Rising disposable incomes and expansion of international restaurant brands are strengthening foodservice consumption. In Africa, South Africa is emerging as a developing market supported by retail diversification, expanding supermarket networks, and growing exposure to international cuisines through urbanization and media influence.

Latin America

Latin America, led by Brazil and Mexico, represents an emerging opportunity within the global hot pot condiment market. Regional growth is supported by expanding Asian restaurant presence, increasing international travel exposure, and gradual diversification of consumer food preferences. Although adoption remains at an early stage compared to Asia-Pacific, improving retail infrastructure and rising middle-class consumption are accelerating product availability. The region is projected to record one of the fastest growth rates globally, with a CAGR exceeding 11% through 2031, driven by urban culinary experimentation, social dining trends, and expanding imports of Asian specialty foods.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Global Hot Pot Condiment Market

- Haidilao International Holding Ltd.

- Sichuan Haidilao Flavor Co., Ltd.

- Chongqing Dezhuang Food Co., Ltd.

- Little Sheep Group

- Lee Kum Kee Company Limited

- Foshan Haitian Flavoring & Food Co., Ltd.

- Inner Mongolia Xiao Wei Yang Food Co., Ltd.

- McCormick & Company, Inc.

- Uni-President Enterprises Corporation

- Nestlé S.A.

- Ajinomoto Co., Inc.

- Yihai International Holding Ltd.

- Otafuku Sauce Co., Ltd.

- Kikkoman Corporation

- Guangdong Meiweixian Flavoring Foods Co., Ltd.