Hops Market Size

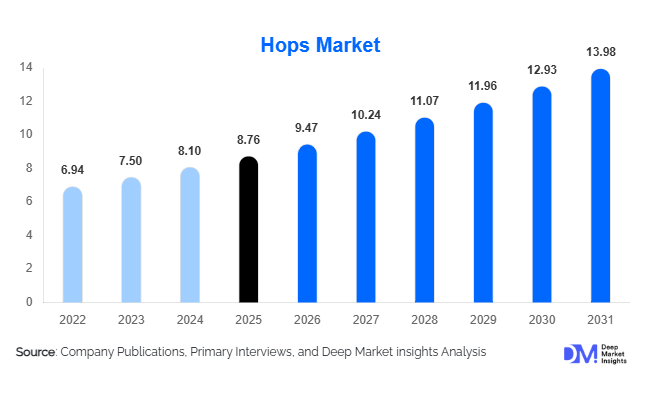

According to Deep Market Insights, the global hops market size was valued at USD 8.76 billion in 2025 and is projected to grow from USD 9.47 billion in 2026 to reach USD 13.98 billion by 2031, expanding at a CAGR of 8.1% during the forecast period (2026–2031). The hops market growth is primarily driven by the rapid expansion of craft brewing, rising premium beer consumption, increasing demand for differentiated flavor profiles, and the growing use of hop-derived ingredients in nutraceutical and wellness applications.

Hops remain a critical raw material in beer production due to their ability to provide bitterness, aroma, flavor stability, and preservation characteristics. The market is increasingly benefiting from the rising popularity of IPA-style beers, flavored alcoholic beverages, and premium craft beer offerings that require high-quality aroma and dual-purpose hop varieties. Breweries across North America and Europe are increasingly adopting specialty hop blends to create unique flavor experiences, supporting long-term demand for advanced hop products and extracts.

The market is also witnessing diversification beyond brewing applications. Hop-derived botanical compounds are gaining popularity in pharmaceuticals, nutraceuticals, herbal wellness products, and cosmetics due to their antioxidant, anti-inflammatory, and calming properties. Demand for organic and sustainably cultivated hops is accelerating as beverage manufacturers strengthen ESG commitments and consumers increasingly prioritize clean-label ingredients. Technological advancements in cryogenic hop processing, CO2 extraction, precision agriculture, and climate-resilient cultivation methods are further transforming the industry landscape and improving supply chain efficiency globally.

Key Market Insights

- Aroma hops dominate global demand, driven by the rapid expansion of craft beer and premium beverage categories worldwide.

- Hop pellets remain the leading product form, accounting for the majority of commercial brewery usage due to improved storage stability and brewing efficiency.

- North America and Europe collectively account for over 65% of global market demand, supported by established brewing industries and advanced hop cultivation infrastructure.

- Asia-Pacific is emerging as the fastest-growing regional market, fueled by increasing beer consumption and rising craft brewery penetration in China, India, Japan, and South Korea.

- Technological innovation in hop extraction and cryogenic processing is enabling breweries to achieve more concentrated flavor profiles while reducing production waste.

- Organic and sustainably cultivated hops are witnessing strong growth, supported by rising clean-label beverage trends and sustainability-focused procurement strategies.

Hops Market Trends

Premium Craft Brewing Driving Specialty Hop Demand

The increasing global popularity of craft beer continues to reshape the hops market. Craft breweries are demanding differentiated aroma profiles featuring tropical, citrus, pine, floral, and herbal characteristics, leading to strong growth for specialty and proprietary hop varieties such as Citra, Mosaic, Simcoe, and Galaxy. Breweries are increasingly experimenting with hop layering techniques, dry hopping, and late-stage hopping processes to create distinctive flavor experiences that appeal to younger consumers and premium beverage enthusiasts. Seasonal and limited-edition beer launches are further accelerating demand for experimental hop cultivars and advanced hop concentrates. The growth of hazy IPAs, sour beers, and low-alcohol craft beverages has significantly increased the requirement for high-oil-content aroma hops globally.

Rise of Sustainable and Climate-Resilient Hop Cultivation

Sustainability is emerging as a major trend across the global hops industry. Large breweries and ingredient manufacturers are increasingly investing in regenerative agriculture, water-efficient irrigation systems, and carbon reduction initiatives to secure environmentally sustainable supply chains. Climate volatility in key hop-growing regions such as the U.S. Pacific Northwest and Central Europe has accelerated investments in climate-resilient hop varieties with improved drought resistance and yield stability. Producers are adopting AI-enabled crop monitoring, drone-assisted field management, and precision farming technologies to optimize productivity while minimizing environmental impact. Organic hop cultivation is also expanding rapidly as breweries increasingly market clean-label and sustainably sourced beverage products to environmentally conscious consumers.

Hops Market Drivers

Expansion of the Global Craft Beer Industry

The rapid expansion of craft brewing remains the most significant growth driver for the global hops market. Craft breweries typically utilize substantially higher hop volumes per barrel compared to mass-market beer producers, especially in IPA, pale ale, and specialty beer categories. Countries such as the United States, Germany, the United Kingdom, Australia, Brazil, and Japan continue to witness strong growth in independent brewery operations. Consumer demand for premium beer experiences and differentiated flavor profiles is encouraging breweries to increase procurement of specialty aroma hops and advanced hop extracts. This trend is expected to remain a long-term growth catalyst for the market.

Rising Premiumization in Alcoholic Beverages

Consumers globally are increasingly shifting toward premium alcoholic beverages that emphasize quality ingredients, artisanal production methods, and innovative flavor combinations. Breweries are responding by launching limited-edition products, fruit-infused beer variants, barrel-aged formulations, and high-hop-content beverages. Premiumization has significantly increased demand for dual-purpose and aroma hops that provide complex sensory experiences. Growing disposable incomes and evolving consumer preferences toward experiential drinking are further supporting the expansion of premium brewing segments across both mature and emerging markets.

Technological Advancements in Hop Processing

Advanced processing technologies such as cryogenic separation, concentrated hop oils, and CO2 extraction systems are transforming the market. These innovations enable breweries to achieve more consistent flavor delivery while reducing raw material waste and improving operational efficiency. Cryo hops and liquid hop concentrates are increasingly adopted by commercial breweries because they offer higher aromatic intensity and lower vegetal matter content. Technological innovation is also improving shelf life, transportation efficiency, and brewing precision, further accelerating global market adoption.

Hops Market Restraints

Climate Volatility Affecting Crop Yield Stability

Hop cultivation is highly dependent on stable climatic conditions, making the market vulnerable to droughts, heatwaves, irregular rainfall, and temperature fluctuations. Major producing regions in North America and Europe are increasingly facing climate-related agricultural challenges that negatively affect alpha acid content, crop yield quality, and annual harvest consistency. Reduced yields often lead to raw material shortages and price volatility, creating procurement challenges for breweries and processors worldwide.

Raw Material Price Fluctuations and Supply Concentration

The global hops industry remains concentrated in a limited number of producing countries, including the United States, Germany, and the Czech Republic. Supply chain disruptions, transportation constraints, and regional crop failures can significantly impact global pricing structures. Smaller craft breweries are particularly vulnerable to sudden increases in hop prices because they often lack long-term procurement contracts and purchasing leverage. Fluctuating production costs and limited availability of proprietary hop varieties remain key restraints affecting overall market stability.

Hops Market Opportunities

Growth of Non-Alcoholic and Low-Alcohol Beer Production

The global shift toward healthier lifestyles and moderation-focused alcohol consumption is creating strong opportunities for hop manufacturers and processors. Non-alcoholic and low-alcohol beer producers increasingly rely on aroma-rich hops and advanced hop extracts to compensate for flavor losses during alcohol removal processes. This trend is particularly strong across Europe, North America, Japan, and urban Asian markets. The segment is expected to witness double-digit growth over the forecast period, creating new demand for customized hop formulations and concentrated aroma products.

Expansion into Nutraceutical and Wellness Applications

Hop-derived compounds such as xanthohumol and prenylflavonoids are increasingly utilized in sleep support supplements, relaxation products, hormonal wellness formulations, and herbal nutraceuticals. Rising consumer demand for natural botanical ingredients and plant-based wellness products is creating diversification opportunities beyond traditional brewing applications. Pharmaceutical and nutraceutical manufacturers are investing in standardized extraction technologies and clinical research to commercialize value-added hop ingredients with scientifically validated health benefits.

Product Type Insights

Aroma hops account for the largest share of the global hops market, representing nearly 38% of total market value in 2025. Their dominance is supported by increasing demand for premium and craft beer varieties that emphasize complex flavor and aroma characteristics. Popular varieties such as Mosaic, Citra, Cascade, and Galaxy are widely used in IPA and pale ale production due to their citrus, tropical fruit, and floral sensory profiles. Dual-purpose hops are also witnessing strong adoption because they provide both bitterness and aroma functionality, improving brewing efficiency and reducing ingredient complexity. Bittering hops continue to maintain stable demand among large commercial breweries focused on cost optimization and large-volume beer production. Specialty products such as cryo hops and advanced hop extracts are gaining traction rapidly due to their ability to enhance flavor intensity while improving brewing efficiency and reducing raw material waste.

Form Insights

Hop pellets dominate the global market, accounting for approximately 57% of total market share in 2025. Pellets are preferred by commercial breweries because they offer superior storage stability, transportation efficiency, and improved consistency during brewing operations. Type 90 pellets remain the industry standard due to their cost-effectiveness and broad application across beer categories. Hop extracts and concentrated hop oils are witnessing rapid growth due to increasing adoption by industrial breweries seeking greater process efficiency and enhanced flavor precision. Whole leaf hops maintain niche demand among traditional craft brewers and specialty beer producers that prioritize artisanal brewing methods and authentic flavor development.

Application Insights

The brewing industry continues to dominate the hops market, accounting for more than 82% of global demand in 2025. Craft brewing remains the fastest-growing application segment because independent breweries utilize significantly higher hop volumes per liter compared to conventional beer manufacturers. Rising consumer demand for flavored beer, hazy IPA styles, and premium alcoholic beverages continues to strengthen hop consumption globally. Beyond brewing, pharmaceutical and nutraceutical applications are gaining momentum due to increasing use of hop extracts in sleep aids, stress management products, and herbal wellness formulations. Cosmetic and personal care applications are also expanding steadily, with hop-derived antioxidants being increasingly incorporated into skincare and anti-aging formulations.

Cultivation Type Insights

Conventional hops continue to dominate global production, accounting for nearly 84% of total market share in 2025 due to large-scale commercial cultivation practices and stable production economics. However, organic hops are emerging as one of the fastest-growing cultivation categories, supported by increasing consumer preference for sustainable and clean-label alcoholic beverages. Breweries are increasingly promoting organic beer products to environmentally conscious consumers, encouraging farmers to transition toward certified organic cultivation methods. Sustainable and regenerative farming practices are also gaining traction as multinational breweries strengthen ESG-focused procurement policies and carbon reduction commitments.

End-Use Insights

Microbreweries and craft breweries account for approximately 41% of global hop consumption value despite producing lower beer volumes than multinational breweries. Their higher hop utilization rates and focus on differentiated flavor profiles continue to drive demand for aroma and specialty hop varieties. Large commercial breweries remain major consumers of bittering hops and advanced hop extracts due to their large-scale production operations. Nutraceutical companies represent an emerging end-use segment as demand grows for botanical wellness ingredients in sleep support and stress-relief products. Cosmetic manufacturers are increasingly incorporating hop-derived antioxidants and anti-inflammatory compounds into skincare formulations targeting premium wellness consumers.

| By Product Type | By Form | By Application | By Cultivation Type | By Distribution Channel |

|---|---|---|---|---|

|

|

|

|

|

Regional Insights

North America

North America accounts for nearly 32% of the global hops market, led primarily by the United States, which remains one of the world’s largest producers and consumers of hops. The Pacific Northwest region continues to dominate cultivation due to favorable climatic conditions and advanced agricultural infrastructure. The rapid expansion of craft breweries and strong consumer preference for hop-forward beer styles such as IPA and pale ale continue to support market growth. Canada is also witnessing increasing demand from independent breweries and premium beverage producers focused on artisanal beer production and flavored alcoholic beverages.

Europe

Europe remains the largest regional market, accounting for approximately 36% of global market share in 2025. Germany, the Czech Republic, Poland, and the United Kingdom are major contributors to regional demand and production. Germany maintains a dominant position due to its advanced cultivation infrastructure and strong brewing heritage, while the Czech Republic remains globally recognized for noble aroma hop production. European breweries are increasingly investing in sustainable sourcing, organic brewing, and premium beer innovation, further supporting long-term hops demand across the region.

Asia-Pacific

Asia-Pacific is projected to be the fastest-growing regional market, expanding at a CAGR exceeding 9.5% through 2031. China, India, Japan, Australia, and South Korea are driving regional demand growth due to rising urbanization, increasing disposable incomes, and westernized beverage consumption patterns. China’s expanding premium beer market and Japan’s growing demand for low-alcohol and flavored beer products are strengthening regional consumption. India is witnessing rapid growth in microbreweries and craft beer establishments across urban centers such as Bengaluru, Pune, Mumbai, and Gurugram, increasing imports of premium aroma hop varieties.

Latin America

Latin America is witnessing increasing hops demand, particularly from Brazil, Mexico, Argentina, and Chile. Brazil remains the region’s largest craft beer market and continues to import substantial quantities of aroma hops from North America and Europe. Mexico’s growing premium beer export industry and rising domestic beer innovation are supporting additional market expansion. Regional breweries are increasingly experimenting with imported hop varieties to create differentiated craft beer products targeted at younger consumers.

Middle East & Africa

The Middle East & Africa market remains comparatively smaller but demonstrates strong long-term growth potential. South Africa leads regional demand due to its established brewing sector and growing craft beer ecosystem. The UAE and Saudi Arabia are emerging as premium beverage consumption hubs due to rising tourism and hospitality investments. Increasing interest in non-alcoholic premium beverages across the Middle East is also creating opportunities for hop-derived flavoring applications and alcohol-free beer production.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Hops Market

- BarthHaas GmbH & Co. KG

- Yakima Chief Hops

- Hopsteiner

- John I. Haas

- HVG Hopfenverwertungsgenossenschaft

- NZ Hops Ltd.

- Charles Faram & Co. Ltd.

- Select Botanicals Group

- S.S. Steiner

- Hollingbery & Son Hops

- Puterbaugh Farms

- Hop Head Farms

- Freudenberger Hopfen

- Kalsec Inc.

- Totally Natural Solutions