High Pressure Processing (HPP) Juices Market Size

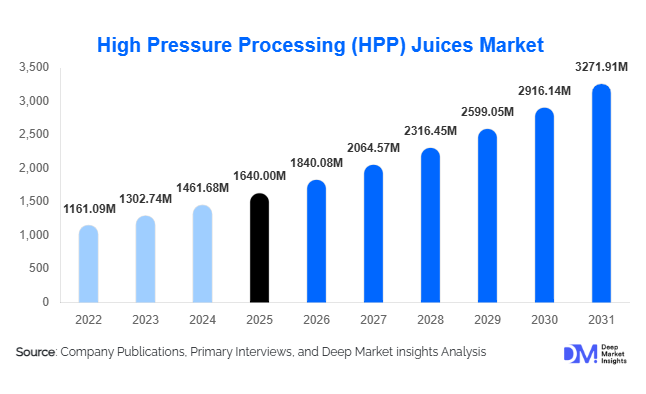

According to Deep Market Insights, the global high pressure processing (HPP) juices market size was valued at USD 1,640 million in 2025 and is projected to grow from USD 1,840.08 million in 2026 to reach USD 3,271.91 million by 2031, expanding at a CAGR of 12.2% during the forecast period (2026–2031). The HPP juices market growth is primarily driven by increasing consumer demand for clean-label beverages, rising preference for minimally processed products, and growing awareness regarding nutrient retention and food safety.

Key Market Insights

- HPP juices are gaining strong traction due to clean-label positioning, as they eliminate the need for preservatives while maintaining freshness and safety.

- Functional and immunity-boosting beverages are expanding rapidly, with HPP technology preserving vitamins, enzymes, and antioxidants.

- North America dominates the global market, supported by premium beverage consumption and advanced cold chain infrastructure.

- Asia-Pacific is the fastest-growing region, driven by urbanization, rising disposable income, and expanding organized retail.

- Retail consumption accounts for the majority of demand, particularly through supermarkets and hypermarkets.

- Technological advancements in HPP equipment are reducing processing costs and enabling scalability for mid-sized manufacturers.

What are the latest trends in the HPP juices market?

Rising Demand for Functional and Nutraceutical Juices

The HPP juices market is witnessing a strong shift toward functional beverages enriched with vitamins, probiotics, and plant-based nutrients. Consumers are increasingly prioritizing immunity, gut health, and overall wellness, leading to the rapid adoption of detox juices, protein-enriched blends, and antioxidant-rich formulations. HPP technology plays a crucial role by preserving bioactive compounds without thermal degradation. Brands are introducing innovative formulations such as cold-pressed green juices, adaptogenic blends, and fortified fruit juices. This trend is particularly strong among urban consumers and fitness-focused demographics, where demand for convenient yet nutritious beverages continues to rise.

Expansion of Premium and Cold-Pressed Juice Segments

Premiumization is a defining trend in the HPP juices market. Consumers are willing to pay higher prices for quality, freshness, and transparency in sourcing. Cold-pressed juices processed through HPP are increasingly positioned as premium offerings in retail shelves. Companies are investing in branding, sustainable packaging, and product differentiation to attract high-value customers. Additionally, the rise of direct-to-consumer and subscription-based juice delivery models is reshaping the distribution landscape, allowing brands to build stronger customer engagement and recurring revenue streams.

What are the key drivers in the HPP juices market?

Growing Demand for Clean-Label and Natural Products

Consumers are increasingly shifting away from artificial additives and preservatives, driving demand for natural and minimally processed beverages. HPP juices align perfectly with this trend, offering extended shelf life without compromising nutritional quality. Regulatory bodies are also encouraging clean-label formulations, further supporting market growth. This shift is particularly prominent in developed markets, where transparency and ingredient traceability are key purchasing factors.

Increasing Health Awareness and Immunity Focus

Rising awareness about lifestyle diseases and the importance of preventive healthcare is significantly boosting demand for nutrient-rich beverages. HPP juices retain essential vitamins and antioxidants, making them highly appealing to health-conscious consumers. Post-pandemic, the focus on immunity has intensified, with consumers actively seeking functional beverages that support overall well-being. This trend is expected to sustain long-term growth in the market.

What are the restraints for the global market?

High Capital Investment and Operational Costs

The adoption of HPP technology requires substantial initial investment in specialized equipment and infrastructure. This creates entry barriers for small and medium-sized manufacturers. Additionally, maintenance and operational costs remain relatively high, impacting profit margins. These factors limit widespread adoption, particularly in price-sensitive markets.

Dependence on Cold Chain Infrastructure

Despite extended shelf life compared to fresh juices, HPP products still require refrigeration throughout the supply chain. This dependence on cold storage and logistics increases distribution costs and restricts market penetration in regions with underdeveloped infrastructure. Ensuring consistent cold chain management remains a critical challenge for manufacturers and distributors.

What are the key opportunities in the HPP juices industry?

Expansion in Emerging Markets

Emerging economies such as India, China, and Southeast Asian countries present significant growth opportunities due to rising disposable incomes and increasing awareness of premium health products. Rapid urbanization and expansion of modern retail formats are facilitating the availability of HPP juices in these markets. Government initiatives supporting food processing industries further enhance growth prospects.

Integration with Sustainable Packaging Solutions

Sustainability is becoming a major focus area for beverage companies. Combining HPP technology with recyclable and eco-friendly packaging can create strong brand differentiation. Consumers are increasingly favoring brands that align with environmental values, providing opportunities for companies to enhance their market positioning through sustainable innovations.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1640.00 Million |

| Market Size in 2026 | USD 1840.08 Million |

| Market Size in 2031 | USD 3271.91 Million |

| CAGR | 12.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The global HPP (High Pressure Processing) juices market is strongly shaped by evolving consumer preferences toward minimally processed, nutrient-rich beverages that preserve natural taste and functional benefits. Within this landscape, fruit juices continue to dominate the market, accounting for nearly 48% of the total market share in 2025. This dominance is primarily driven by long-standing consumer familiarity, widespread availability, and the inherent appeal of natural sweetness combined with perceived health benefits. Citrus-based juices such as orange and lemon remain highly popular due to their refreshing taste and vitamin C content, while tropical fruit variants like mango, pineapple, and passion fruit are gaining traction in both developed and emerging markets. The strong growth of fruit juices is also supported by advancements in cold-pressed and HPP technologies that allow manufacturers to maintain fresh-like sensory profiles without relying on preservatives, thereby enhancing consumer trust in product quality and safety.Vegetable juices, particularly green blends such as kale, spinach, cucumber, and celery-based beverages, are also witnessing steady adoption. This growth is driven by the expanding vegan population and the rising popularity of plant-based diets. Consumers perceive vegetable juices as detoxifying and alkalizing, contributing to weight management and overall wellness. Although taste remains a challenge for mainstream adoption, manufacturers are addressing this through flavor balancing with fruits and natural sweeteners. The segment is particularly strong among fitness communities and health-conscious millennials seeking low-sugar beverage alternatives.

Application Insights

Retail consumption remains the dominant application segment in the HPP juices market, accounting for approximately 60% of global demand. This dominance is driven by the premium positioning of HPP juices in supermarkets, hypermarkets, and specialty stores, where consumers actively seek healthier beverage alternatives. The increasing penetration of health-focused retail aisles and chilled beverage sections has significantly enhanced product visibility. Additionally, rising disposable incomes and shifting consumption patterns toward ready-to-drink functional beverages have strengthened retail demand. The convenience of grab-and-go packaging and growing awareness of clean-label products further reinforce retail leadership in this segment.Foodservice applications are experiencing rapid expansion as hotels, restaurants, cafes, and juice bars increasingly incorporate HPP juices into their premium beverage offerings. The primary driver for this segment is the growing consumer expectation for fresh, high-quality, and minimally processed drinks in dining experiences. Hospitality providers are leveraging HPP juices to differentiate their menus and align with health-conscious dining trends. Additionally, the rise of wellness tourism and premium hospitality experiences has further accelerated adoption. Foodservice operators also benefit from the extended shelf life of HPP products, which reduces waste and improves operational efficiency.The growing popularity of subscription-based juice delivery services is also reshaping application dynamics. Consumers increasingly prefer personalized nutrition delivered directly to their homes, driven by convenience and lifestyle optimization. This model is supported by digital platforms that offer customized juice plans based on dietary needs, further enhancing consumer engagement and retention.

Distribution Channel Insights

Supermarkets and hypermarkets continue to dominate distribution channels, holding approximately 46% market share. Their leadership is driven by strong consumer trust, extensive product assortment, and high visibility of refrigerated beverage sections. These retail formats allow consumers to physically evaluate premium juice products, which is particularly important for HPP beverages that emphasize freshness and quality. Strategic product placement, promotional campaigns, and private-label offerings further strengthen their dominance.Online retail and e-commerce channels are expanding at a rapid pace, fueled by increasing digital adoption, smartphone penetration, and changing shopping behaviors. The primary growth driver in this segment is convenience, as consumers prefer doorstep delivery and subscription-based models. E-commerce platforms also enable brands to reach niche health-conscious audiences through targeted marketing. The COVID-19 pandemic significantly accelerated this shift, and the trend continues as consumers become more comfortable purchasing perishable beverages online with reliable cold-chain logistics.Foodservice channels are also expanding as hospitality and quick-service restaurants increasingly integrate HPP juices into their beverage menus. The growing emphasis on premium dining experiences and health-oriented offerings is driving adoption across these channels.

Packaging Insights

PET bottles lead the packaging segment with approximately 52% market share, primarily due to their lightweight nature, durability, cost efficiency, and compatibility with high-pressure processing systems. PET packaging ensures product safety while maintaining visual appeal and convenience, making it highly suitable for retail distribution. The key driver behind PET dominance is its balance between performance and affordability, particularly in mass-market distribution.Glass bottles are preferred for premium HPP juice offerings, driven by consumer perception of purity, sustainability, and superior product preservation. Glass packaging enhances brand positioning in high-end retail and foodservice environments, where aesthetics and environmental consciousness play a significant role in purchasing decisions. The rising demand for eco-friendly packaging solutions is further strengthening glass adoption despite higher costs.Pouches and cartons are gaining traction, particularly in on-the-go consumption segments. Their growth is driven by portability, reduced packaging weight, and improved logistics efficiency. These formats are increasingly used in single-serve functional juice products targeting busy urban consumers.Overall, packaging innovation is increasingly focused on recyclability, biodegradable materials, and extended shelf-life technologies. Sustainability regulations and consumer environmental awareness are pushing manufacturers toward greener packaging solutions.

Explore more data points, trends and opportunities Download Free Sample Report

High Pressure Processing (HPP) Juices Market Segmentations

By Product Type

- Fruit Juices

- Vegetable Juices

- Mixed Juices

- Functional & Fortified Juices

By Application

- Retail Consumption

- Foodservice

- Institutional Supply

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail/E-commerce

- Specialty Health Stores

- Foodservice Channels

Regional Insights

North America

North America holds the largest share of the HPP juices market at approximately 38% in 2025, driven by strong consumer demand in the United States and Canada. The primary growth drivers in this region include high disposable income levels, advanced cold-chain infrastructure, and a well-established functional beverage culture. Consumers in North America are highly health-conscious, with increasing preference for clean-label, organic, and non-GMO beverages. The presence of leading juice brands and widespread availability across supermarkets, convenience stores, and foodservice outlets further reinforces market leadership. Additionally, strong innovation in functional beverages, particularly immunity-boosting and detox juices, continues to fuel growth.

Europe

Europe accounts for around 28% of the global market, with key demand originating from Germany, the United Kingdom, France, and the Nordic countries. The region’s growth is driven by stringent food safety regulations, strong sustainability mandates, and high consumer awareness regarding healthy lifestyles. European consumers demonstrate a strong preference for organic and minimally processed beverages, aligning well with HPP technology. The expansion of vegan and plant-based diets is also contributing to increased demand for vegetable and functional juices. Furthermore, regulatory support for clean-label products and eco-friendly packaging is accelerating adoption.

Asia-Pacific

Asia-Pacific is the fastest-growing region, expanding at a CAGR of approximately 14%. The growth is driven by rapid urbanization, rising disposable incomes, and increasing awareness of health and wellness trends across China, India, Japan, and Southeast Asia. The expanding middle-class population is increasingly shifting toward premium packaged beverages. The proliferation of modern retail infrastructure and rapid growth of e-commerce platforms are significantly improving product accessibility. Additionally, the influence of Western dietary habits and rising fitness culture are driving demand for functional and fruit-based HPP juices. Domestic manufacturers are also investing heavily in cold-chain logistics and product innovation.

Latin America

Latin America is experiencing steady growth, particularly in Brazil and Mexico, supported by abundant fruit production and favorable climatic conditions. The region benefits from strong agricultural output, which ensures a consistent supply of raw materials for juice production. The key driver in this region is increasing export opportunities, as Latin American producers supply tropical fruit concentrates and juices to global markets. Rising urbanization and growing awareness of health and wellness are also contributing to domestic consumption growth.

Middle East & Africa

The Middle East & Africa region is gradually expanding, with the United Arab Emirates, Saudi Arabia, and South Africa leading demand. Growth is driven by increasing urbanization, rising expatriate populations, and growing adoption of premium lifestyle products. The expansion of modern retail infrastructure and hospitality sectors is also contributing to market development. Consumers in urban centers are increasingly shifting toward healthier beverage options, particularly imported premium juices. Additionally, rising disposable incomes in Gulf countries are supporting demand for high-quality functional beverages.

Key Players in the HPP Juices Market

- Hain Celestial Group

- Suja Life LLC

- Evolution Fresh

- Coldpress

- Pressed Juicery

- Raw Pressery

- Innocent Drinks

- PepsiCo (Naked Juice)

- Coca-Cola Company

- Tropicana Brands Group

- Goodnature Products

- HPP Italia

- Liquiteria

- Village Juicery

- Jus Jus