Heavy Metal Testing Market Size

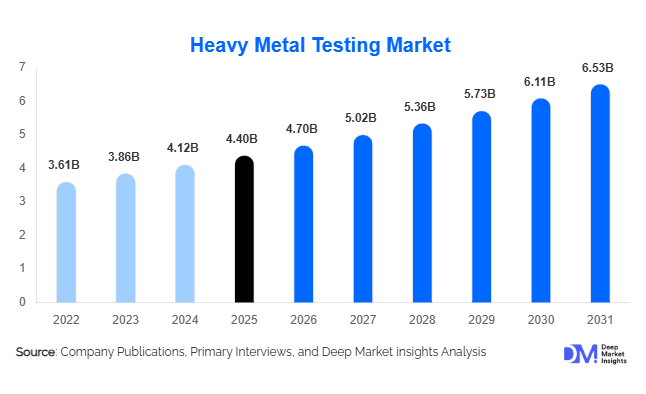

According to Deep Market Insights, the global heavy metal testing market size was valued at USD 4.4 billion in 2025 and is projected to grow from USD 4.7 billion in 2026 to reach USD 6.53 billion by 2031, expanding at a CAGR of 6.8% during the forecast period (2026–2031). The market growth is primarily driven by stringent regulatory standards, rising industrialization, public health concerns, and technological advancements in analytical testing instruments, enabling rapid and precise detection of toxic metals in food, water, soil, and consumer goods.

Key Market Insights

- Arsenic and lead testing dominate due to high toxicity and global regulatory focus, creating continuous demand across food, water, and environmental monitoring applications.

- ICP-MS technology is leading in instrument adoption globally, offering ultra-low detection limits, high throughput, and multi-element capabilities essential for compliance and industrial testing.

- Commercial laboratories are the largest end users, benefiting from centralized infrastructure, accreditation, and multi-sector sample processing capabilities.

- Asia-Pacific is the fastest-growing region, driven by industrial expansion, increasing food exports, and government investments in environmental monitoring in China and India.

- North America remains the largest regional market, supported by strong regulatory frameworks, advanced lab infrastructure, and high public awareness regarding heavy metal contamination.

- Portable field analyzers and digital integration are reshaping the market, allowing real-time monitoring, remote testing, and AI-assisted data analytics for industrial, environmental, and food safety applications.

What are the latest trends in the heavy metal testing market?

Technological Innovation and Portable Solutions

Analytical instrumentation is evolving rapidly, with the adoption of portable ICP-MS, XRF, and biosensor-based testing kits allowing on-site heavy metal analysis. These technologies reduce sample turnaround time and allow industrial operators, environmental agencies, and food processors to perform real-time testing. AI-driven predictive analytics and cloud-based compliance platforms are increasingly used to manage testing data, forecast contamination risks, and ensure regulatory adherence. This trend is accelerating adoption in both developed and emerging economies, enabling smaller labs and field operators to participate effectively in the market.

Regulatory-Driven Demand Expansion

Government agencies worldwide are tightening permissible limits for toxic metals such as arsenic, lead, cadmium, and mercury in food, water, and consumer products. Harmonization of international standards for exports is driving demand for certified testing to access global markets. Public awareness of contamination risks and food safety incidents also reinforces frequent testing. Compliance-driven adoption is strongest in food & beverage, water utilities, pharmaceuticals, and consumer goods sectors, resulting in recurring demand for both commercial lab services and in-house industrial testing.

What are the key drivers in the heavy metal testing market?

Stringent Environmental and Food Safety Regulations

Global agencies such as the FDA, EPA, and EU regulatory bodies enforce strict limits on heavy metal content, compelling manufacturers, municipalities, and industrial operators to conduct routine testing. This regulatory pressure ensures a stable, recurring demand for analytical services and instrumentation, particularly in high-risk sectors like food and water supply.

Rising Public Awareness and Health Concerns

High-profile contamination incidents, such as water lead crises and industrial effluent spills, have heightened awareness of heavy metal exposure risks. Consumers are increasingly demanding safer food and water products, encouraging manufacturers and service providers to proactively integrate testing into supply chains and production lines.

Technological Advancements in Analytical Instruments

Innovations in ICP-MS, AAS, XRF, and portable field analyzers have improved sensitivity, reduced testing time, and enabled multi-element detection. Integration with digital data platforms allows real-time monitoring, remote testing, and AI-assisted analytics, enhancing operational efficiency for both commercial labs and industrial clients.

What are the restraints for the global market?

High Instrumentation and Operational Costs

Advanced testing equipment, consumables, and trained personnel represent significant investments, restricting adoption among smaller laboratories and emerging-market players. Operational expenses for maintenance, calibration, and compliance also add financial pressure.

Regulatory Complexity Across Regions

Differences in testing standards between major markets (e.g., North America, EU, APAC) complicate compliance strategies for multinational operators. These variations necessitate multiple tests, certifications, and documentation processes, increasing operational and logistical challenges.

What are the key opportunities in the heavy metal testing industry?

Adoption of Portable and Rapid Testing Platforms

Portable ICP-MS, XRF, and biosensor-based solutions offer rapid and on-site testing capabilities, enabling industries to monitor heavy metal contamination in real-time. These tools are particularly valuable for environmental monitoring, field inspections, and quality assurance in food processing and mining operations. The growing demand for mobile testing solutions provides opportunities for instrument manufacturers and service providers to expand market penetration in emerging regions.

Expanding Industrial and Export-Driven Demand

Emerging economies such as China, India, and Brazil are investing heavily in industrial modernization, environmental monitoring, and food export compliance. The requirement for certified heavy metal testing to meet global standards creates recurring demand. Private manufacturers, government labs, and commercial service providers can leverage this growth through strategic investments and partnerships.

Integration of Digital Analytics and AI Solutions

The integration of AI-powered analytics, predictive modeling, and cloud-based compliance platforms presents opportunities for new entrants and existing players to differentiate their services. These solutions streamline data management, optimize testing schedules, and improve decision-making for regulatory compliance, industrial safety, and environmental protection, creating additional revenue streams for technology-enabled laboratories.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4.4 Billion |

| Market Size in 2026 | USD 4.7 Billion |

| Market Size in 2031 | USD 6.53 Billion |

| CAGR | 6.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The ICP-MS (Inductively Coupled Plasma Mass Spectrometry) segment dominates the heavy metal testing market due to its ultra-low detection limits, high throughput, and multi-element capabilities. These features make ICP-MS ideal for regulatory compliance, industrial monitoring, and complex sample matrices such as food, water, and environmental samples. AAS (Atomic Absorption Spectroscopy) and XRF (X-Ray Fluorescence) maintain strong adoption for routine laboratory and field-based testing because of their cost-effectiveness, simplicity, and reliability. Emerging technologies, such as biosensors and rapid test kits, are gaining traction in developing and emerging markets, particularly for on-site screening in water quality monitoring and food safety applications. The growth of portable and rapid testing solutions is further enabling smaller laboratories, industrial facilities, and field operators to conduct real-time heavy metal analysis efficiently, expanding market penetration across regions.

Application Insights

The food products segment is the largest application area for heavy metal testing, driven by stringent safety regulations, export compliance requirements, and increasing consumer demand for contaminant-free products. Regular testing of food ingredients, processed goods, and infant nutrition products ensures adherence to global standards and prevents health risks associated with heavy metal contamination. Water testing represents the second-largest application, supported by public health monitoring, municipal water quality programs, and industrial effluent management initiatives. Soil, air, and consumer goods testing are smaller but rapidly growing segments, reflecting expanding environmental regulations and industrial compliance mandates globally. The emphasis on food and water safety continues to be the primary growth driver, reinforcing ICP-MS as the preferred technology for high-precision, multi-element analysis.

Distribution Channel Insights

Direct laboratory services remain the dominant distribution channel, providing end-to-end testing solutions, certification, and regulatory reporting. OEM instrumentation sales also account for a significant share, with manufacturers supplying analytical devices to commercial laboratories, industrial facilities, and government agencies. The adoption of portable and field testing solutions is increasing through specialized dealers and direct-to-client models, enabling on-site testing in remote or industrial locations. Additionally, digital platforms and subscription-based services for compliance reporting, data analytics, and cloud-based monitoring are emerging as new channels, offering laboratories and industrial operators efficient and scalable solutions to manage heavy metal testing requirements across multiple sites.

End-Use Insights

Commercial laboratories lead the end-user segment due to their centralized infrastructure, accreditation standards, and ability to handle complex, multi-element testing requirements. The food & beverage industry is the fastest-growing application sector, driven by stringent safety regulations, international trade compliance, and rising consumer demand for contaminant-free products. Water utilities and pharmaceutical manufacturers follow closely, reflecting mandatory environmental and industrial compliance. Emerging applications include clinical toxicology testing, consumer product safety analysis, and environmental consulting services. Export-driven industries increasingly depend on certified heavy metal testing to access global markets, creating recurring demand for both services and advanced instrumentation solutions.

Explore more data points, trends and opportunities Download Free Sample Report

Heavy Metal Testing Market Segmentations

By Product Type

- ICP-MS

- AAS

- XRF

- Biosensors and Rapid Test Kits

By Application

- Food Products

- Water Testing

- Soil Testing

- Air Testing

- Consumer Goods Testing

By Distribution Channel

- Direct Laboratory Services

- OEM Instrumentation Sales

- Specialized Dealers

- Direct-to-Client Models

- Digital Platforms & Subscription Services

By End-Use

- Commercial Laboratories

- Food & Beverage Industry

- Water Utilities

- Pharmaceutical Manufacturers

- Environmental Consulting Services

- Clinical Toxicology

Regional Insights

North America

North America holds the largest market share (36%) in 2025, led by the U.S. and Canada. Market growth is fueled by stringent regulatory frameworks from agencies such as the FDA and EPA, advanced laboratory infrastructure, and high public awareness of contamination risks. The presence of numerous accredited commercial laboratories and industrial compliance requirements drives consistent demand for heavy metal testing. Industrial expansion, food export requirements, and public health initiatives further reinforce regional growth. ICP-MS is widely adopted in this region due to its high sensitivity and ability to meet complex regulatory standards.

Europe

Europe accounts for 21% of the market in 2025, with Germany, the U.K., and France leading adoption. Growth is driven by comprehensive EU food safety, environmental, and industrial regulations and the increasing emphasis on sustainability and eco-compliance initiatives. The adoption of multi-element testing technologies and rapid field-based solutions is accelerating across food, water, and environmental applications. Additionally, government-led investments in analytical infrastructure and growing public awareness about heavy metal exposure are encouraging laboratories and industrial users to adopt advanced testing solutions such as ICP-MS and AAS for reliable, high-throughput monitoring.

Asia-Pacific

Asia-Pacific is the fastest-growing region, with China and India at the forefront. Market expansion is driven by rapid industrialization, environmental monitoring initiatives, and export-driven compliance requirements. Rising consumer awareness of public health risks, coupled with government policies mandating regular testing of food, water, and industrial outputs, is fueling adoption. Investments in laboratory infrastructure, capacity-building, and advanced analytical instrumentation such as ICP-MS and portable field analyzers are further supporting growth. The region’s growing food processing and pharmaceutical sectors, combined with increasing cross-border trade, are key drivers of regional market demand.

Latin America

Latin America is witnessing steady growth, with Brazil, Mexico, and Argentina driving demand for food and environmental testing. Regional expansion is fueled by increasing industrial activity, government-mandated compliance testing, and the modernization of laboratory infrastructure. The growing food export industry requires certified heavy metal testing to meet global standards. Adoption of portable testing solutions and affordable rapid kits is enhancing accessibility for smaller laboratories and industrial facilities. ICP-MS and XRF technologies are increasingly deployed for regulatory compliance and high-precision analysis.

Middle East & Africa

Africa is experiencing growing testing demand primarily for mining, industrial, and environmental compliance, with South Africa, Nigeria, and Kenya leading adoption. Middle Eastern countries, including the UAE and Saudi Arabia, are investing in expanding analytical capabilities for food safety, environmental monitoring, and industrial compliance. Drivers include government-led modernization initiatives, industrial diversification, and increasing public health awareness. Portable analyzers and rapid testing kits are being deployed in remote mining and industrial zones, while ICP-MS adoption is increasing for high-precision testing in food and water applications. Export-oriented industries in the region further drive demand for certified testing services.

Key Players in the Heavy Metal Testing Market

- Eurofins Scientific SE

- SGS S.A.

- Intertek Group plc

- Bureau Veritas S.A.

- ALS Limited

- TUV SUD AG

- Merieux NutriSciences

- LGC Group

- AsureQuality

- Microbac Laboratories

- EMSL Analytical

- OMIC USA

- R J Hill Laboratories

- Pace Analytical Services

- NSF International