Heavy Cream Alternative Market Size

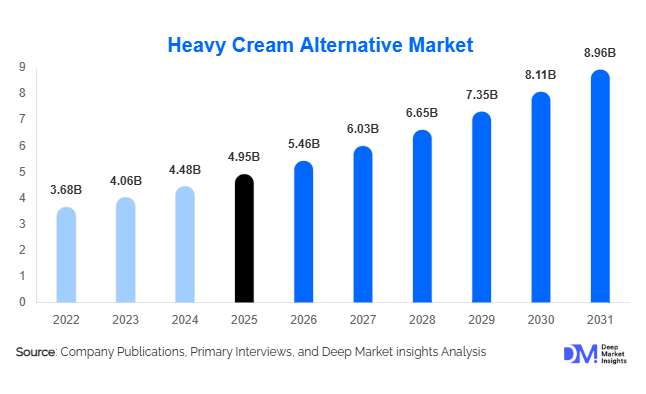

According to Deep Market Insights,the global heavy cream alternative market size was valued at USD 4.95 billion in 2025 and is projected to grow from USD 5.46 billion in 2026 to reach USD 8.96 billion by 2031, expanding at a CAGR of 10.4% during the forecast period (2026–2031). The heavy cream alternative market growth is primarily driven by the rising demand for plant-based dairy substitutes, increasing lactose intolerance among consumers, and the expanding adoption of vegan and flexitarian diets worldwide.

Heavy cream alternatives are designed to replicate the texture, richness, and functionality of traditional dairy cream while offering lactose-free, vegan, and often lower-fat options. These products are widely used in cooking, baking, desserts, sauces, and beverages. Ingredients such as coconut, almond, soy, oat, and cashew are increasingly being utilized to create plant-based cream substitutes that meet evolving consumer preferences for healthier and sustainable food options.

Growing consumer awareness regarding animal welfare, environmental sustainability, and health-conscious diets has significantly boosted demand for dairy alternatives. The rapid expansion of plant-based food products across retail and foodservice channels has further accelerated adoption. Food manufacturers are also incorporating cream substitutes into ready meals, bakery products, soups, and packaged desserts to cater to consumers seeking dairy-free alternatives.

Key Market Insights

- Plant-based cream alternatives are witnessing strong demand due to the global shift toward vegan and flexitarian diets.

- The foodservice industry is increasingly adopting dairy-free cream substitutes to develop vegan-friendly menus and lactose-free culinary offerings.

- North America dominates the global market due to strong consumer awareness, developed retail distribution, and widespread adoption of plant-based diets.

- Asia-Pacific represents the fastest-growing region, supported by high lactose intolerance rates and expanding urban middle-class populations.

- Product innovation in plant protein formulations is improving whipping performance and texture replication for cream substitutes.

- E-commerce platforms are expanding accessibility for plant-based dairy products, accelerating market penetration in emerging economies.

What are the latest trends in the heavy cream alternative market?

Clean Label and Natural Ingredient Formulations

One of the most prominent trends in the heavy cream alternative market is the rising consumer demand for clean-label products. Consumers are increasingly examining ingredient lists and preferring products that contain natural plant-based ingredients without artificial stabilizers or preservatives. As a result, manufacturers are focusing on developing formulations using simple ingredients such as coconut milk, almond milk, oat milk, and natural emulsifiers.

Food brands are also emphasizing organic certification, non-GMO ingredients, and allergen-free formulations to attract health-conscious consumers. Clean-label positioning is becoming a major competitive differentiator in the dairy alternatives industry, particularly in developed markets such as the United States, Canada, and Western Europe.

Technological Innovation in Plant-Based Cream Formulation

Advancements in food science and plant protein processing technologies are enabling manufacturers to develop cream alternatives that closely replicate the taste, texture, and whipping functionality of traditional dairy cream. New formulations incorporate advanced emulsifiers, plant proteins, and hydrocolloids that enhance product stability and mouthfeel.

These innovations allow cream substitutes to perform effectively in professional culinary applications, including baking, whipping, and cooking. Food technology companies are investing heavily in research and development to improve the sensory experience of dairy alternatives, enabling broader adoption in both household and commercial food preparation.

What are the key drivers in the heavy cream alternative market?

Rising Adoption of Plant-Based Diets

The increasing popularity of vegan and flexitarian diets is one of the most significant drivers of the heavy cream alternative market. Consumers are becoming more aware of the environmental and health impacts associated with animal-based food products, leading to a shift toward plant-based dietary choices.

Plant-based cream alternatives allow consumers to maintain the creamy texture and flavor in dishes while avoiding dairy ingredients. This trend has encouraged food manufacturers and restaurants to introduce dairy-free options across multiple food categories.

Growing Lactose Intolerance Among Consumers

Lactose intolerance affects a large portion of the global population, particularly in Asia-Pacific and Africa. As a result, consumers are increasingly seeking dairy-free alternatives that provide similar functionality without digestive discomfort.

Heavy cream alternatives made from coconut, soy, almond, and oat milk offer lactose-free options for cooking and baking. This demand is encouraging retailers and food manufacturers to expand their plant-based dairy product portfolios.

What are the restraints for the global market?

Higher Production Costs Compared to Dairy Cream

One of the primary challenges facing the heavy cream alternative market is the relatively higher production cost compared to traditional dairy cream. Plant-based ingredients such as almonds, oats, and coconut often involve complex processing and supply chain costs, which can increase retail prices.

Price sensitivity among consumers in emerging economies may slow market adoption, particularly where conventional dairy products remain more affordable.

Functional Limitations in Culinary Applications

Despite significant improvements in formulation technologies, some cream alternatives still face limitations in replicating the exact whipping performance and heat stability of traditional dairy cream. Professional chefs and bakery manufacturers may require consistent whipping properties and high heat tolerance, which some plant-based substitutes are still working to achieve.

Continuous investment in research and development will be essential for overcoming these functional limitations and expanding product applications.

What are the key opportunities in the heavy cream alternative industry?

Expansion of Plant-Based Foodservice Offerings

The rapid expansion of vegan and plant-based restaurant chains worldwide presents a major growth opportunity for heavy cream alternative manufacturers. Foodservice operators are increasingly offering plant-based versions of traditional dishes, including pasta sauces, soups, desserts, and specialty coffee beverages.

Heavy cream substitutes enable restaurants to replicate creamy textures while maintaining dairy-free formulations. This demand is expected to increase as more consumers adopt plant-based diets and seek vegan-friendly dining experiences.

Rising Demand in Emerging Asian Markets

Asia-Pacific represents a major growth opportunity due to high lactose intolerance rates and rapidly growing middle-class populations. Countries such as China, India, Japan, and South Korea are witnessing increasing consumer awareness of plant-based foods.

As retail distribution networks expand and e-commerce platforms improve accessibility, plant-based dairy alternatives are becoming more widely available across urban markets. Manufacturers are also developing regionally tailored products using ingredients familiar to local consumers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4.95 Billion |

| Market Size in 2026 | USD 5.46 Billion |

| Market Size in 2031 | USD 8.96 Billion |

| CAGR | 10.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

The plant-based cream alternatives segment represents the leading product category in the heavy cream alternative market, accounting for the largest share of global revenue. This dominance is primarily driven by the growing global shift toward plant-based diets, increasing awareness of lactose intolerance, and rising consumer demand for dairy-free food products that maintain the texture and functionality of traditional cream. Plant-derived cream substitutes made from coconut, almond, soy, oat, and cashew milk are widely used across food preparation, offering versatile solutions for cooking, baking, and beverage applications. These alternatives provide comparable creaminess and emulsification properties while appealing to vegan and health-conscious consumers seeking lower cholesterol and environmentally sustainable ingredients.

Coconut-based cream substitutes hold a particularly strong position within the plant-based segment due to their naturally rich fat content and thick consistency, which closely resembles traditional dairy cream. Their ability to perform well in both savory and sweet dishes makes them highly suitable for sauces, curries, soups, and desserts. Almond-based cream alternatives are gaining traction as consumers increasingly prefer lighter flavor profiles and products perceived as nutritious and low in saturated fat. Oat-based cream substitutes have also emerged as a rapidly expanding category, supported by their smooth texture, neutral taste, and compatibility with specialty coffee beverages. Additionally, cashew-based formulations are increasingly used in premium culinary applications due to their naturally creamy texture and ability to blend smoothly into sauces and spreads.

In addition to plant-derived options, dairy-derived alternatives such as lactose-free cream and reduced-fat cream substitutes continue to hold a measurable share of the market. These products appeal to consumers who experience lactose intolerance but still prefer dairy-based ingredients over fully plant-based replacements. Lactose-free cream alternatives are manufactured through enzymatic processes that break down lactose, making them easier to digest while preserving the taste and functionality of conventional dairy cream.

Functional cream substitutes based on starches, hydrocolloids, and plant proteins are also gaining attention within the food processing sector. These specialized formulations are designed to provide enhanced stability, emulsification, and shelf life for industrial food applications. Food manufacturers are increasingly incorporating these functional ingredients into processed foods, sauces, soups, and ready meals where consistent texture and performance are essential.

Application Insights

Cooking and culinary applications constitute the leading application segment of the heavy cream alternative market, driven by the increasing demand for dairy-free ingredients in everyday meal preparation. Cream substitutes are widely used in soups, sauces, pasta dishes, curries, and ready-to-eat meals, where they provide the creamy consistency and flavor traditionally associated with dairy cream. The growing popularity of plant-based home cooking and the expansion of vegan-friendly recipes across digital platforms have further accelerated the adoption of cream alternatives in culinary applications. Consumers are increasingly experimenting with dairy-free cooking at home, particularly as plant-based ingredients become more widely available through retail and online channels.

Beverage applications represent another rapidly expanding segment of the market, particularly in the specialty coffee industry. Coffee chains, independent cafés, and quick-service restaurants are increasingly offering plant-based cream substitutes to meet the preferences of vegan, lactose-intolerant, and health-conscious consumers. Plant-based creamers derived from oat, almond, and coconut milk are commonly used in lattes, cappuccinos, and flavored coffee beverages due to their ability to froth effectively and complement coffee flavor profiles. The rapid growth of premium coffee culture and the expansion of café chains across urban markets have significantly contributed to rising demand within this segment.

Bakery and dessert applications also account for a substantial portion of market demand. Cream alternatives are widely used in frostings, whipped toppings, fillings, custards, and dessert sauces. Manufacturers are developing specialized formulations that mimic the whipping, aeration, and stability characteristics of dairy cream, enabling their use in cakes, pastries, mousses, and frozen desserts. As consumer interest in plant-based sweets and dairy-free indulgence continues to rise, demand for cream substitutes in the bakery sector is expected to increase steadily.

Distribution Channel Insights

Supermarkets and hypermarkets represent the leading distribution channel for heavy cream alternatives, driven by their extensive product assortments and strong consumer footfall. These large retail outlets provide consumers with convenient access to a wide variety of plant-based dairy substitutes, including private-label and premium branded products. Supermarkets also play a critical role in educating consumers about plant-based food options by featuring dedicated dairy-free sections and promoting new product innovations through in-store displays and marketing campaigns. The ability of supermarkets to offer competitive pricing and broad product availability continues to strengthen their dominance within the distribution landscape.

Online retail channels are emerging as one of the fastest-growing distribution platforms for heavy cream alternatives. The increasing popularity of e-commerce grocery shopping has enabled consumers to access a broader range of specialty plant-based products that may not always be available in local retail stores. Online platforms allow manufacturers to reach geographically diverse customer bases while also supporting direct-to-consumer business models. Many brands are leveraging digital marketing, subscription services, and personalized product recommendations to build loyal customer communities and encourage repeat purchases. Additionally, online channels enable niche and emerging brands to enter the market with relatively lower distribution barriers.

End-Use Insights

The foodservice sector represents the leading end-use segment for heavy cream alternatives, primarily driven by the growing demand for plant-based menu offerings across restaurants, cafés, bakeries, and quick-service establishments. Foodservice operators are increasingly incorporating dairy-free cream substitutes into soups, sauces, beverages, and desserts to accommodate customers who follow vegan, vegetarian, or lactose-free diets. The expansion of plant-based menus in global restaurant chains and the rising popularity of specialty coffee beverages have further strengthened the role of cream alternatives in commercial kitchens. Foodservice providers also benefit from the extended shelf life and consistent performance of many plant-based cream formulations.

The food processing industry also represents a significant contributor to overall market demand. Manufacturers of packaged foods, ready meals, sauces, soups, and frozen desserts are integrating plant-based cream substitutes into their product formulations to align with evolving consumer preferences for dairy-free and clean-label ingredients. Industrial food producers increasingly rely on cream alternatives that provide functional properties such as emulsification, stability, and heat resistance during processing.

Household consumption continues to expand steadily as retail availability increases and consumer awareness of plant-based diets grows. Home cooks are increasingly incorporating dairy-free cream substitutes into everyday recipes, ranging from pasta sauces and baked goods to smoothies and coffee beverages. The growing influence of online cooking content, plant-based recipe platforms, and health-focused social media communities has also contributed to rising adoption among households.

Explore more data points, trends and opportunities Download Free Sample Report

Heavy Cream Alternative Market Segmentations

By Product Type

- Plant-Based Cream Alternatives

- Dairy-Derived Cream Alternatives

- Starch-Based Cream Substitutes

- Protein-Based Cream Alternatives

- Hydrocolloid-Stabilized Cream Substitutes

By Form

- Liquid Cream Alternatives

- Powdered Cream Alternatives

- Whippable Cream Alternatives

- Concentrated Cream Bases

By Application

- Cooking and Culinary Applications

- Whipping and Dessert Toppings

- Coffee and Beverage Creamers

- Bakery and Confectionery Applications

- Sauces and Ready Meal Preparations

By Distribution Channel

- Supermarkets and Hypermarkets

- Convenience Stores

- Specialty Vegan and Health Stores

- Foodservice Distribution

- Online Retail and Direct-to-Consumer

Regional Insights

North America

North America holds the largest share of the heavy cream alternative market, accounting for approximately 32% of global demand. The region’s leadership is primarily driven by strong consumer awareness of plant-based diets, widespread adoption of vegan and flexitarian lifestyles, and the strong presence of major dairy alternative manufacturers. The United States dominates the regional market due to its highly developed plant-based food industry, extensive product availability across retail channels, and growing demand for dairy-free ingredients in both foodservice and household applications. Increasing concerns about lactose intolerance, cholesterol intake, and environmental sustainability have further accelerated the adoption of plant-based cream substitutes across the country. Canada also represents a growing market within the region, supported by rising consumer interest in health-conscious diets, strong retail distribution networks, and increasing innovation in plant-based food products.

Europe

Europe represents one of the most mature and well-established markets for dairy alternatives, with strong demand across countries such as Germany, the United Kingdom, France, and the Netherlands. The region benefits from high consumer awareness of sustainability, animal welfare, and environmentally responsible food production. European consumers are highly receptive to plant-based ingredients, and many food manufacturers have expanded their product portfolios to include dairy-free alternatives. Regulatory frameworks in the European Union also emphasize transparency in ingredient labeling and food sourcing, which has increased consumer trust in plant-based products. Additionally, the growing popularity of vegan and flexitarian diets, combined with strong innovation in plant-based food technologies, continues to drive regional market growth.

Asia-Pacific

Asia-Pacific is the fastest-growing regional market for heavy cream alternatives, driven by the high prevalence of lactose intolerance among Asian populations and the rapid expansion of urban middle-class consumers. Countries such as China, India, Japan, and South Korea are witnessing increasing demand for plant-based dairy substitutes as consumers adopt healthier and more diverse dietary habits. The rapid growth of café culture, expanding foodservice industries, and rising interest in Western-style bakery products have also contributed to increased consumption of cream alternatives in the region. Additionally, the strong availability of plant-based raw materials such as coconut, soy, and cashews supports the development of locally produced dairy alternatives. As awareness of vegan diets and environmental sustainability grows, Asia-Pacific is expected to remain one of the most dynamic markets for heavy cream substitutes.

Latin America

Latin America is gradually emerging as a promising growth market for heavy cream alternatives. Countries such as Brazil and Mexico are experiencing increasing consumer awareness of plant-based diets, driven by rising health concerns, urbanization, and exposure to global food trends. The growing availability of plant-based products through supermarkets, specialty stores, and online retail platforms is also contributing to market expansion. Additionally, food manufacturers in the region are increasingly investing in dairy-free product innovation to cater to changing consumer preferences. As awareness of lactose intolerance and sustainable food consumption continues to increase, the demand for cream alternatives is expected to rise steadily across Latin America.

Middle East & Africa

The Middle East and Africa region is witnessing steady growth in the heavy cream alternative market as plant-based food products become more accessible in urban retail environments. Countries such as the United Arab Emirates, Saudi Arabia, and South Africa are experiencing rising demand for dairy alternatives among health-conscious and environmentally aware consumers. The expansion of international restaurant chains, specialty coffee shops, and premium grocery retailers has increased exposure to plant-based dairy substitutes across the region. Additionally, the growing expatriate population and increasing adoption of global dietary trends are encouraging retailers and foodservice providers to expand their offerings of plant-based cream products. Continued improvements in distribution networks and rising awareness of lactose intolerance are expected to further support regional market growth.