Healthy Low Fat Desserts Market Size

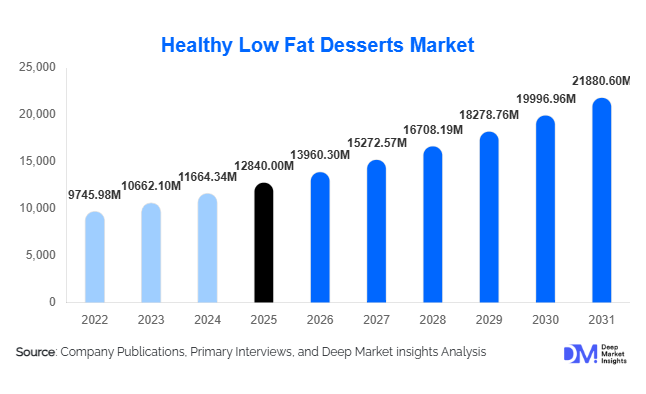

According to Deep Market Insights, the global healthy low fat desserts market size was valued at USD 12,840 million in 2025 and is projected to grow from USD 13,960 million in 2026 to reach USD 21,880 million by 2031, expanding at a CAGR of 9.4% during the forecast period (2026–2031). Market expansion is primarily driven by rising global health awareness, increasing adoption of calorie-conscious diets, and strong consumer demand for indulgent yet nutritionally balanced dessert alternatives. The shift toward preventive healthcare, weight management lifestyles, and reduced sugar consumption has significantly reshaped dessert consumption patterns worldwide.

Key Market Insights

- Consumers are increasingly replacing traditional desserts with low-fat and reduced-calorie alternatives aligned with fitness and wellness goals.

- Plant-based and dairy-free low-fat desserts are witnessing rapid adoption, particularly among vegan and lactose-intolerant consumers.

- North America dominates global demand due to strong functional food adoption and established healthy snacking culture.

- Asia-Pacific is the fastest-growing region, supported by urbanization, rising disposable income, and growing obesity awareness.

- Clean-label formulations and natural sweeteners are becoming key purchasing factors among younger consumers.

- Technology-led reformulation, including fat mimetics and sugar-reduction technologies, is improving taste parity with conventional desserts.

What are the latest trends in the healthy low fat desserts market?

Functional and Protein-Enriched Desserts

Healthy low fat desserts are increasingly positioned as functional foods rather than indulgence-only products. Manufacturers are incorporating high-protein ingredients, probiotics, fiber enrichment, and micronutrient fortification into desserts such as yogurts, puddings, frozen desserts, and snack bars. Fitness-focused consumers are driving demand for desserts that support muscle recovery, satiety, and metabolic health. Protein ice creams and low-fat Greek yogurt desserts have become mainstream offerings across retail shelves. Functional positioning also allows brands to command premium pricing while appealing to consumers seeking guilt-free indulgence.

Clean Label and Natural Ingredient Innovation

Consumers increasingly prefer desserts made with recognizable ingredients and minimal processing. Artificial additives, synthetic sweeteners, and hydrogenated fats are being replaced with natural alternatives such as stevia, monk fruit, fruit concentrates, and plant-based stabilizers. Transparency in labeling has become a competitive differentiator, particularly in developed markets. Brands are reformulating products to reduce fat while maintaining texture through natural emulsifiers and fiber-based fat replacers, significantly improving consumer acceptance of healthier desserts.

What are the key drivers in the healthy low fat desserts market?

Rising Global Health Awareness

The growing prevalence of obesity, diabetes, and cardiovascular conditions has accelerated consumer migration toward healthier food options. Governments and healthcare organizations worldwide promote reduced fat intake and calorie moderation, encouraging consumers to adopt healthier dessert alternatives. Low-fat desserts allow consumers to maintain indulgence habits while aligning with nutritional goals, making them a sustainable dietary substitute rather than a temporary trend.

Expansion of Modern Retail and E-commerce Channels

The proliferation of supermarkets, health-focused specialty stores, and online grocery platforms has improved accessibility to niche healthy dessert categories. Digital retail platforms enable brands to educate consumers through nutritional storytelling and targeted marketing campaigns. Subscription-based healthy snack models and direct-to-consumer channels are further accelerating adoption among urban populations.

Advances in Food Processing Technologies

Innovations in fat-reduction technologies, aeration techniques, and ingredient engineering are enabling manufacturers to replicate the texture and flavor of traditional desserts without excessive fat content. Advances in plant proteins and dairy alternatives have enhanced mouthfeel, overcoming historical taste limitations associated with low-fat products.

What are the restraints for the global market?

Higher Production Costs

Low-fat dessert formulations often require specialized ingredients, advanced processing technologies, and strict quality controls. These factors increase manufacturing costs, leading to premium pricing compared to conventional desserts and limiting adoption in price-sensitive markets.

Taste Perception Challenges

Despite technological progress, some consumers still perceive low-fat desserts as less indulgent. Maintaining taste parity while achieving nutritional targets remains a significant challenge for manufacturers, requiring continuous R&D investments.

What are the key opportunities in the healthy low fat desserts industry?

Emerging Market Urbanization

Rapid urbanization across Asia-Pacific, Latin America, and the Middle East is creating a new consumer base seeking healthier packaged foods. Rising middle-class populations and increasing exposure to global dietary trends are enabling strong penetration opportunities for international brands and regional innovators.

Plant-Based and Dairy-Free Expansion

The convergence of veganism, lactose intolerance awareness, and sustainability concerns is creating strong opportunities for plant-based low-fat desserts. Almond, oat, coconut, and soy-based desserts are expanding rapidly, supported by improved formulations and growing retail visibility.

Personalized Nutrition and Functional Positioning

Digital health ecosystems and wearable fitness technologies are encouraging personalized dietary choices. Brands offering targeted low-fat desserts for keto-friendly, diabetic-friendly, or protein-enhanced diets can unlock premium consumer segments and recurring demand.

Product Type Insights

Low-fat frozen desserts continue to dominate the global market, accounting for nearly 34% of the market share in 2025. The surge in demand for guilt-free indulgence products, such as low-fat ice cream, frozen yogurt, and protein-enriched desserts, is a key driver of this segment. Consumers in North America and Europe are increasingly seeking healthier alternatives to traditional high-fat desserts, prompting manufacturers to innovate extensively with novel flavors, fortified ingredients, and functional formulations. Additionally, the growing prevalence of lifestyle diseases, including obesity and cardiovascular conditions, reinforces the consumer preference for low-fat options. The segment benefits from robust marketing campaigns, social media influence, and widespread consumer familiarity, making low-fat frozen desserts the preferred choice for health-conscious individuals. Seasonal variations, such as the summer peak demand in temperate regions, also contribute to sustained sales growth. Emerging trends in indulgence combined with nutrition, like protein-infused frozen yogurts, are further expanding the segment’s appeal to fitness-focused demographics globally.

Ingredient Type Insights

Plant-based ingredients represent the fastest-growing category, capturing approximately 29% of the 2025 market. The adoption of veganism, lactose intolerance awareness, and a global shift toward sustainable food production are major drivers of growth. Consumers are increasingly prioritizing natural and ethical consumption, which has led to an expansion of plant-based frozen dessert offerings. Innovations in ingredients such as almond milk, oat milk, soy protein, and coconut-based formulations allow manufacturers to meet both taste and nutritional expectations without compromising dietary preferences. North America and Europe lead in adoption due to strong consumer education and regulatory support for plant-based alternatives. Meanwhile, in Asia-Pacific, the growing urban middle class and rising awareness of lifestyle diseases are prompting a surge in demand for plant-based desserts. Manufacturers are also capitalizing on the perception of plant-based ingredients as cleaner and healthier, aligning with the global trend of functional and wellness-oriented foods. Research and development in this segment continues to focus on improving texture, taste, and protein content to replicate traditional dairy experiences while appealing to ethical and health-conscious consumers.

Distribution Channel Insights

Supermarkets and hypermarkets remain the leading distribution channel with nearly 41% market share in 2025. These retail formats benefit from strong cold-chain infrastructure, high product visibility, and the capacity to host impulse purchase behaviors, particularly for premium or seasonal products. The dominance of supermarkets and hypermarkets is reinforced by partnerships with leading frozen dessert brands that ensure wide availability and shelf prominence. E-commerce and online grocery platforms are emerging as complementary channels, especially in North America, Europe, and Asia-Pacific, allowing consumers to conveniently access a wide range of low-fat and plant-based dessert options. Retailers increasingly offer promotions, bundle packs, and loyalty programs to encourage repeat purchases. The convenience and accessibility of these modern retail formats, coupled with the trust they command among consumers, make them indispensable for driving sales in both developed and emerging markets. Smaller convenience stores and specialty retailers, though less dominant in market share, cater to urban consumers seeking single-serve or on-the-go options, complementing the broader distribution landscape.

Category Insights

Reduced-sugar and low-calorie desserts hold approximately 38% of the global market, reflecting a growing consumer focus on calorie management, weight control, and balanced nutrition. The rise of lifestyle diseases, along with the influence of social media and wellness trends, has heightened awareness of sugar consumption and its health implications. Consumers are increasingly demanding products that combine indulgence with health benefits, leading manufacturers to innovate with alternative sweeteners, fiber fortification, and functional ingredients such as prebiotics and probiotics. North America and Europe remain the largest markets due to high awareness and regulatory encouragement for reduced-sugar formulations, while Asia-Pacific is witnessing rapid adoption as urban millennials adopt calorie-conscious lifestyles. The category also benefits from premium positioning strategies, with brands emphasizing natural ingredients, clean labels, and nutritional transparency. Cross-segment innovations, such as low-calorie plant-based desserts or fortified frozen yogurts, further drive the growth of this category across multiple consumer touchpoints.

Packaging Type Insights

Single-serve packaging leads the market with around 46% share, reflecting urban consumer trends toward portion control, convenience, and on-the-go consumption. Single-serve portions address dietary concerns, enabling consumers to enjoy desserts without overindulgence, which is particularly attractive in North America and Europe where calorie-conscious diets are prevalent. In Asia-Pacific, the rise of nuclear families and busy urban lifestyles has significantly contributed to demand for portable and ready-to-eat packaging formats. Sustainable packaging is emerging as a secondary growth driver, with consumers favoring recyclable and eco-friendly options. Manufacturers are responding by introducing biodegradable containers, smaller multipacks, and resealable formats, enhancing convenience while aligning with environmental responsibility. The combination of health consciousness, busy lifestyles, and environmental awareness ensures that single-serve packaging remains a critical growth engine in the frozen dessert market globally.

End-Use Insights

Retail household consumption continues to dominate with nearly 63% share, driven by increased home consumption and healthier snacking habits emerging post-pandemic. Consumers increasingly prepare dessert-oriented meals at home, supplemented with convenient low-fat and plant-based frozen desserts. The surge in remote work, digital entertainment consumption, and wellness-oriented lifestyles have accelerated demand for at-home indulgence products. Meanwhile, the foodservice and quick-service restaurant (QSR) segment is the fastest-growing end-use channel. Cafés, fitness centers, corporate cafeterias, and QSR chains are introducing low-fat, reduced-sugar, and plant-based dessert menus to cater to health-conscious consumers. Export-driven demand is also rising as leading North American and European brands expand their presence in Asia-Pacific and Latin American markets through premium retail chains and e-commerce platforms. The global healthy foodservice industry, valued at over USD 1 trillion, is increasingly integrating healthier dessert offerings, creating sustainable downstream demand for functional frozen desserts across commercial establishments and institutional catering.

| By Product Type | By Ingredient Type | By Distribution Channel | By Category | By Packaging Type | By End-Use |

|---|---|---|---|---|---|

|

|

|

|

|

|

Regional Insights

North America

North America accounted for approximately 36% of the global market share in 2025, with the United States and Canada leading the region. The dominance is underpinned by strong consumer awareness of calorie reduction, a deep-rooted fitness culture, and high acceptance of functional foods. Innovation in protein-rich and low-fat frozen desserts, coupled with aggressive marketing campaigns, has fueled adoption. The presence of major multinational frozen dessert brands, coupled with well-established cold-chain infrastructure and modern retail penetration, further supports market expansion. Additionally, government-led nutrition awareness programs and regulatory emphasis on sugar reduction have created a conducive environment for healthier dessert options. Seasonal promotions, holiday gifting trends, and the proliferation of indulgent yet low-fat product lines also contribute to sustained consumption growth. North America’s preference for premium, convenient, and functional desserts continues to drive product development and market competitiveness.

Europe

Europe holds nearly 27% of the global market share, with Germany, the U.K., France, and the Netherlands as key contributors. The European market is largely influenced by stringent regulations on sugar content, labeling standards, and clean-label product requirements. Consumers increasingly prefer organic, natural, and functional desserts, driving manufacturers to innovate with plant-based and low-calorie offerings. Health awareness campaigns and lifestyle changes emphasizing calorie management have accelerated adoption in both urban and semi-urban areas. Premiumization trends, such as artisanal flavors, locally sourced ingredients, and eco-friendly packaging, resonate strongly with European consumers. The robust presence of supermarkets, hypermarkets, and specialty organic stores enhances product accessibility. Additionally, rising demand from health-conscious millennials and working professionals, coupled with sustained marketing and sampling initiatives, underpins Europe’s position as a leading region in the global low-fat frozen dessert market.

Asia-Pacific

Asia-Pacific is the fastest-growing region, expanding at over 11% CAGR. Major growth engines include China, India, Japan, and South Korea, fueled by urbanization, rising disposable incomes, and growing health consciousness. Consumers are increasingly aware of obesity and lifestyle-related diseases, creating demand for low-fat, reduced-sugar, and plant-based desserts. In India, rapid urbanization and changing dietary habits among millennials are significant drivers, while in China, premiumization and brand-conscious consumption spur demand for high-quality frozen dessert products. The expansion of modern retail, e-commerce penetration, and cold-chain infrastructure further facilitate market access. Moreover, cross-cultural influences, global travel experiences, and exposure to Western dietary trends are driving innovative product adoption. The proliferation of international dessert brands, coupled with government health awareness initiatives, ensures continued market growth. Local flavors, regional ingredients, and fusion desserts are also gaining traction, appealing to culturally diverse consumers while maintaining nutritional benefits.

Middle East & Africa

The Middle East & Africa region is witnessing steady growth, with the UAE and Saudi Arabia leading adoption due to rising urbanization, premium retail expansion, and increasing prevalence of lifestyle diseases such as diabetes and obesity. Rising health consciousness and awareness of sugar reduction among consumers are driving adoption of low-fat and reduced-sugar desserts. The expansion of modern retail chains, supermarkets, and hypermarkets, coupled with the influx of international brands, facilitates product accessibility. Consumers are increasingly inclined toward indulgent yet healthier alternatives, often driven by social media influence, wellness campaigns, and premium positioning of products. Corporate cafeterias, fitness centers, and luxury QSR outlets are also integrating low-fat and plant-based dessert options, further boosting regional demand. Government initiatives promoting healthier lifestyles and food labeling regulations provide additional support for market expansion in this region.

Latin America

Latin America, led by Brazil and Mexico, is demonstrating significant growth in health-oriented frozen desserts. Rising urbanization, growing middle-class populations, and increasing health awareness among consumers are key drivers. The demand for low-fat, reduced-sugar, and plant-based desserts is being supported by the expansion of modern retail outlets and import of premium international products. Consumers are becoming increasingly conscious of caloric intake and lifestyle-related diseases, encouraging the adoption of healthier alternatives. Marketing campaigns promoting indulgence with nutrition, coupled with rising internet penetration and e-commerce adoption, enhance product accessibility. Regional flavors and ingredients are also integrated into frozen desserts to cater to local taste preferences, driving market differentiation. The segment is further bolstered by the growth of the retail household segment, increased home consumption, and rising presence of healthy options in foodservice channels, such as QSRs and cafés. Collaborative efforts by local manufacturers and multinational companies to innovate with functional ingredients ensure sustained growth in this emerging region.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Healthy Low Fat Desserts Market

- Nestlé S.A.

- Danone S.A.

- Unilever PLC

- General Mills Inc.

- The Kraft Heinz Company

- Chobani LLC

- Yasso Inc.

- Halo Top (Wells Enterprises)

- Blue Diamond Growers

- Oatly Group AB

- Arla Foods

- Lactalis Group

- Dean Foods Company

- Nature's Fynd

- Ripple Foods